Special situation Quickie: Axel Springer voluntary tender offer EUR 63/share

A few weeks ago, PE big weight KKR had announced to make a voluntary tender offer for German publisher Axel Springer at EUR 63 per share.

It is an interesting case as the offer is targeting only a minority stake. The threshold for the offer is set at only 20%.

The background seems to be that the biggest shareholder, Friede Springer and the CEO Döpfner, who own together ~45% want to make sure that they control the company together with KKR as they have entered into a shareholder agreement.

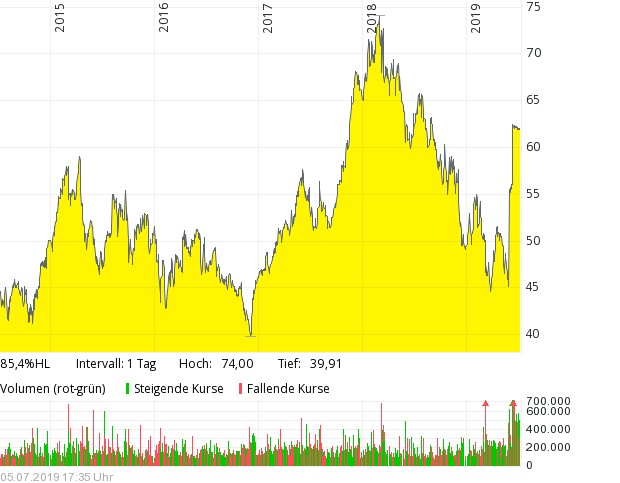

Looking at the stock price we can see that the offer has been made at a significant premium (~40%) but still below 2018 prices:

There seem to have been other attempts to make sure that Friede and Döpfner control the company but they didn’t succeed.

According to the offer document, which was published on July 5th outlines that the offer period including extension will run until Auguts 21st, and payment if successful is expected not later than 10 banking days after August 21st which is then the beginning of September.

Attractiveness as a special situation:

The offer is a friendly one, however at the current price of 62 EUR, the spread is only 1 EUR or 1,6%. Even with the relatively short time frame I think the spread is small compared to the potential downside of -40%.

The threshold of 20% looks low, however around 15% of the other shares are held by long term shareholders & family who might not sell. So the offer is actually for around 50% of the free float and reaching the 20% is maybe not that easy.

So as a summary, this is not attractive for me at the moment. I would get interested if the price of the shares would dip for whatever reason below 60 EUR.

Another special situation: Grandvision (NL) takeover bid from EssilorLuxottica at € 28.

In my understanding, there is no explicit bid yet. Essilor only confirmed that there are talks. That’s too early for me.

Hi! I’m seeing you’re looking for arbitrage opportunities after reading “Merger Masters”. I also read it, and i’m searching for differences in some deals. Last week Cisco announced the acquisition of Acacia Communications in cash, for 70 dollars per share. The spread is more than 9%, and i decided to buy some shares. The deal is friendly and Cisco executed different similar acquisitions during last months. I think the probabilities of success are high. Maybe that deal is of your interest.

Have a nice day and thanks for sharing your thoughts in your webpage! 😉

Great insight!

Unless they change their mind, there will be no squeeze-out at Springer.

Page 38 of the Travita offer document: https://www.traviata-angebot.de/wp-content/uploads/2019/07/Traviata-Angebotsunterlage-en-neu.pdf

hi – think you are confusing domination agreement and squeeze-out for delisting. They spell it out on numerous occasion that they intend to de-list.

e.g. 8.2.4 – para 2 page 30

Delisting can occur without Squeez-out. The intention to delist for me is clearly a negative and supports my thesis that there is only very limited upside.

Why are the untendered shares of Axel Springer trading above the bid if there is no squeeze out?

Is this the opportunity to short the hell out of it?

Domination / Squeeze out expectations I guess… short?

to make 30 bps vs possibly losing big?

Thanks for the interesting thought. However it might be difficult to reach the 95% here depending on what the other Springer heirs do…..

Sure it’s not done deal but this is why it is just an additional optionality.

Re family holders, think safe to assume anyone handed a 300m cheque at 60+ yo would cash it out vs roll-over? esp if you take into account bad blood with Friede who is staying in.

I think you should look at the GFK deal, executed a year ago by the very same KKR team.

You will also find out they went for a squeeze-out which resulted in a ~6% cash bump.

Granted you gotta get to 95% for this to happen.

Still, at similar time in offer period, GFK was trading at 20-25 bps, vs 1.6% here. Still think attractive given the 40d or so time to closing?