FEMSA is a family owned conglomerate, consisting of an (economic) 15% stake in Heineken, a 47% stake in Coca Cola FEMSA (fully consolidated due to majority in votes) and an operating business consisting mostly of Mexican convenience stores called OXXO plus some other LatAm assets that is named the “Commercio” segment

Especially OXXO is a growing, high ROCE business which justifies a significant valuation multiple

It is expected that FEMSA monetizes its Heineken stake soon plus the big story is, that based on an existing OXXO prepaid debit card there is the option for OXXO to become the “Super App” of Mexico like WeChat/Tencent in China or Grab and GoJek in SE Asia

The stock chart of the ADR looks unimpressive, basically flat over the last 8 years in EUR terms after a huge rebound from the GFC:

A very quick sum of parts valuation:

Doing a “sum of parts” valuation at FEMSA is not so easy because they don’t provide a detailed segment reporting, but using 2019 annual reports, I “deconsolidated” Coca Cola FEMSA with their report. This is the summary of my calculation:

Summary FEMSA Sum of part

Value mn USD

Comment

Market Cap

24,905

A and B shares

Value Heineken

8,234

7% block discount

Value Coca Cola Femsa

5,475

30% Control premium

“Stub” Value Commercio

11,197

FEMSA Commercio EBIT 2019

1,017

FEMSA Cons minus CC FEMSA

implicit EV/EBIT

11

Lower bound EV/EBIT

15

Higher bound EV/EBIT

20

Value Commercio lower bound

15,255

Value Commercio upper bound

20,340

Theoretical Value FEMSA at 15X

28,963

Theoretical Value FEMSA at 20X

34,048

Upside 15x EV/EBIT

16.30%

Upside 20xEV/EBIT

36.71%

So the “stub” which is FEMSA’s Commercio segment is valued implicitly at 11x EV/EBIT. Looking at comparable businesses, a 15-20 EV/EBIT would be justified which would result in a potential “sum of part” upside of somewhere between 16-36%.

At first sight, this is more or less where a conglomerate discount for a slightly intransparent/complicated Mexican conglomerate should be.

Are Heineken & Coca Cola Femsa undervalued ?

First, both, Heineken and Coca-Coal could be undervalued. Heineken is a good company but I haven’t looked deeply into them. Heineken’s share price is pretty much where it was one year ago however 9M top line is -8% yoy, so there is no obvious “covid-19” discount. Coca Cola FEMSA still trades below pre Covid-19 levels but I have assumed a 30% control premium anyway and Coca Cola FEMSA doesn’t really move the needle that much.

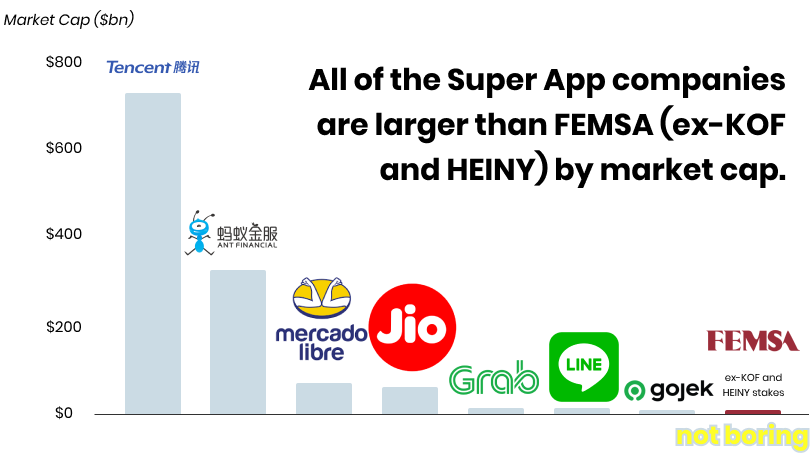

The “super app” story

Second, we have the “super App” story. This is what the US blog writes:

Building the digital wallet is a multi-billion opportunity in its own right. But it also means grabbing the lead position to add more services and build the leading Mexican, and potentially Latin American, SuperApp. Latin America is fertile ground for Super Apps because of its underdeveloped infrastructure and unbanked population. It’s less like the United States, which may be past the point of Super Apps, and more like Asia, where multiple Super Apps sit at the heart of multi-billion dollar companies.

Indonesia’s Gojek is valued at $10 billion, nearly half of FEMSA’s valuation and more than FEMSA’s stub ex-Coca-Cola and Heineken stakes. Indonesia’s GDP is nearly 20% lower than Mexico’s. Gojek is backed by Chinese giant Tencent, whose own Super App, WeChat, is the key to its $726 billion valuation. Also in China, Alibaba spin-off Ant Financial’s digital wallet/SuperApp, Alipay, was preparing to go public at a market cap north of $300 billion before the Chinese government scuttled its plan. That’s over $1 trillion in market cap driven by Super Apps, in just one country.

And then there’s India, where Reliance raised over $20 billion for Jio at a $60 billion valuation, including $5.7 billion from Facebook, in part to grease the wheels for WhatsApp to become the Super App there. Earlier this month, it began rolling out WhatsApp Pay, a big step towards realizing that vision, and confirmation that in emerging markets, partnering, instead of competing, with the local powerhouse is smart business.

There’s a long way to go between where OXXO Pay is today and what even Gojek, Grab, or Line offer, and the larger Super App companies like Tencent, Ant, Mercado Libre, and Jio are a lot more than a Super App, but those companies success show the bull case for FEMSA. Given that the core business is already undervalued, OXXO’s strategic position in the value chain means that investors have a free option on a $10+ billion opportunity.

I fully agree that these days a story alone can move stocks to extremely high levels. However fundamentally i have an issue especially with the peer Group.

The companies from the peer group that I know at least to a certain extent (Tencent, Ant Financial, Grab and Gojek) have one major difference vs. FEMSA:These are all “digital first” technology companies. Yes, being emerging market players they needed to develop an online/Offline business model, but the companies themselves are pure tech companies with all required capabilities and competitive advantages against “legacy” players. In none of these markets any “legacy” player had any chance to play a role of becoming a “super App”. The only exception is JIo, which is part of the Ambani empire but was founded as a Mobile Telecom company which again is at the core a tech business.

Just having a lot of convenience stores and a “low tech” prepaid debit card with 10 mn+ users does not guarantee any success in becoming the leading digital financial ecosystem in Mexico. Plus, the way to a “super app” dominance has been very different in many countries. Tencent started out as a Whatsapp Clone, Grab and Gojek are ride hailing platforms. In Brazil for instance, with a relative similar proportion of unbanked inhabitants, the leading emerging fintech players for the “unbanked” are the digital Neobanks with Nubank being the clear leader, having reached 25 mn customers in a few years time.

To be honest, I have no idea how good FEMSA/OXXO are on the tech side, but so far I cannot think of any “traditional” company anywhere on the globe that has made a successful move to become a leading (Fin)tech player. Maybe FEMSA will be the one but I can’t see it. Therefore I would allocate no value to this “option” as I think this option is at the moment extremely far out of the money and they would need to execute very good and very fast to become a Fintech player against some pretty tough competitors.

Summary:

Based on my calculations (which might be wrong), the discount of FEMSA’s current valuation to a sum-of-part calculation is somewhere in the range of 16-36%. In my opinion and for my risk appetite, this is a pretty normal “discount” for a relatively complicated Emerging Markets conglomerate.

The company seems to indeed interesting and well run, but for me, a discount would need to be higher to compensate for some additional EM related risks and my lack of experience with the Mexican economy and stock market.

As mentioned above, the “Super App” story could actually lead to a rally in the stock price if enough investors believe it but I am not so sure that they can execute. So what you get with the FEMSA stock is clearly an option of an “equity story” but I am not a “story investor”.

Nevertheless I will put FEMSA on my “core” watch list. If the discount becomes bigger or if they actually do something with the Heineken stake, the case could become more interesting. I would also be interested if any readers have more information about the tech organization and capabilities of FEMSA/OXXO(is this a separate unit and at par with leading players like Nubank etc.) . I would also be interested from a Mexican point of view how potential customers see these players and whom they actually would trust with a digital wallet which is often a problem in Emerging Markets.

OXXO has a special role in Mexican society. They basically have deals with all banks so people can pay their bills at OXXO. Very convenient as it is literally at every corner. This biz model gets challenged by digital forms for making payments. Thats why OXXO is reacting and introduce their app. You can be sure that they will have a very high user base who would probably do their payments through the app rather than local store.

Thanks for reminding me of FEMSA – I liked the “Not boring” blog in particular.

Have you looked into the share structure of FEMSA? It’s an interesting one.

They got B (full voting rights, 100% dividend), D (limited voting rights, 125% dividend) and L shares (no voting rights?, 125% dividend). See https://femsa.gcs-web.com/faq – the first 3 points under Capital Stock.

These are bundled up into FEMSAUB (5xB) and FEMSAUBD (1B, 2D, 2L). The ADR is 10x FEMSAUBD.

In short, FEMSAUB can vote and get’s 500% dividend, FEMSAUBD has a limited vote but gets 600% dividend.

100% Dividend in 2019 was 0.483Pesos, or around 2.5P for FEMSAUB or 3P for FEMSAUBD – that’s a dividend yield of 2-3%, roughly.

FEMSAUBD trades for around 150MXP, while FEMSAUB tades currently around 110MXP.

Liquidity in FEMSAUB is very limited, to a couple of 100 shares per day.

1 clip is roughly 11kMXP or 550USD. So this would require patience.

On the other side, leaving the dividends aside, the economic interest of the share classes is the same (am I missing something here?). Hence, in particular if we’re talking about a potential sale of Heineken, the FEMSAUB could be very interesting.

For me, the additional dividend benefit does not explain the price difference. Liquidity might be the better explanation. In particular, as only FEMSAUBD is packaged as ADRs and hence available in the US.

Current discount of FEMSAUB over FEMSAUBD is around 20-25%, whereas historic discount is more in the range of 15-20%. But that’s been quite volatile, recently.

Many thanks for yet again a good write-up as well as sharing new ideas. I love reading your blogg. In this case I have a realtively stupid question: You mentioned that FEMSA holds 47% of Coca Cola but consolidates the business 100%. For your SOTP calculation does it make sense to take the entire 100% EBIT? Or do you have to substract the 53% which they don’t economically own? The same with other minorities in the company? Sorry to ask this silly question – maybe I have missed something or maybe you already done that?

I believe the first time I read about femsa was from langfristig. I liked it. Now I read the case several times and basically still like it, from what I read (never looked more into the details on my own). But, if I remember correctly, risks are not discussed at length in any case. What if, the loose ag a tech pure play, Mexicans discover the global health trend and drink 50% less coke or government regulation goes against sugar, or…?

OXXO has a special role in Mexican society. They basically have deals with all banks so people can pay their bills at OXXO. Very convenient as it is literally at every corner. This biz model gets challenged by digital forms for making payments. Thats why OXXO is reacting and introduce their app. You can be sure that they will have a very high user base who would probably do their payments through the app rather than local store.

Thanks for reminding me of FEMSA – I liked the “Not boring” blog in particular.

Have you looked into the share structure of FEMSA? It’s an interesting one.

They got B (full voting rights, 100% dividend), D (limited voting rights, 125% dividend) and L shares (no voting rights?, 125% dividend). See https://femsa.gcs-web.com/faq – the first 3 points under Capital Stock.

These are bundled up into FEMSAUB (5xB) and FEMSAUBD (1B, 2D, 2L). The ADR is 10x FEMSAUBD.

In short, FEMSAUB can vote and get’s 500% dividend, FEMSAUBD has a limited vote but gets 600% dividend.

100% Dividend in 2019 was 0.483Pesos, or around 2.5P for FEMSAUB or 3P for FEMSAUBD – that’s a dividend yield of 2-3%, roughly.

FEMSAUBD trades for around 150MXP, while FEMSAUB tades currently around 110MXP.

Liquidity in FEMSAUB is very limited, to a couple of 100 shares per day.

1 clip is roughly 11kMXP or 550USD. So this would require patience.

On the other side, leaving the dividends aside, the economic interest of the share classes is the same (am I missing something here?). Hence, in particular if we’re talking about a potential sale of Heineken, the FEMSAUB could be very interesting.

For me, the additional dividend benefit does not explain the price difference. Liquidity might be the better explanation. In particular, as only FEMSAUBD is packaged as ADRs and hence available in the US.

Current discount of FEMSAUB over FEMSAUBD is around 20-25%, whereas historic discount is more in the range of 15-20%. But that’s been quite volatile, recently.

Curious about your thoughts.

I Haven’t looked deeply into the share structure. However different valuation for different share classes is not unusual.

Sixt voting share trade almost 100% higher than Sixt non-voting shares despite a dividend disadvantage. No one knows why.

Many thanks for yet again a good write-up as well as sharing new ideas. I love reading your blogg. In this case I have a realtively stupid question: You mentioned that FEMSA holds 47% of Coca Cola but consolidates the business 100%. For your SOTP calculation does it make sense to take the entire 100% EBIT? Or do you have to substract the 53% which they don’t economically own? The same with other minorities in the company? Sorry to ask this silly question – maybe I have missed something or maybe you already done that?

Hi,

subtracted the complete EBIT of Coca Cola Femsa as I value it with the market value of the shares. Heineken doesn’t show up in the EBIT anyway.

I believe the first time I read about femsa was from langfristig. I liked it. Now I read the case several times and basically still like it, from what I read (never looked more into the details on my own). But, if I remember correctly, risks are not discussed at length in any case. What if, the loose ag a tech pure play, Mexicans discover the global health trend and drink 50% less coke or government regulation goes against sugar, or…?

I think the backlash against unhealthy food is already there. That explains a little bit the weak performance of CC FEMSA.