PerfOrmance Review Q2 2021 – Comment “Expectation Management”

In the first 6 months of 2021, the Value & Opportunity portfolio gained +14,7% (including dividends, no taxes) against a gain of +13.8% for the Benchmark (Eurostoxx50 (25%), Eurostoxx small 200 (25%), DAX (30%), MDAX (20%), all TR indices).

Links to previous Performance reviews can be found on the Performance Page of the blog. Some other funds that I follow have performed as follows in the first 6M 2021:

Partners Fund TGV: +22,1%

Profitlich/Schmidlin: 13,3 %

Squad European Convictions +18,54%

Ennismore European Smaller Cos +16,01% (in EUR)

Frankfurter Aktienfonds für Stiftungen 12,35%

Greiff Special Situation 3,45%

Squad Aguja Special Situation 10,37%

Paladin One 5,94%

Performance review

For the first 6 months, the portfolio more or less ended up in line with the underlying Benchmark although my readers know that the composition is very different, plus I had around 10% on average allocated to cash.

On the plus side, I only made few obvious mistakes, such as selling SFPI too early. On the minus side, I am a little bit angry that I didn’t turn some of my brighter moments (BionTech, Couche Tard) into bigger positions.

I am very surprised how strong the overall stock market still performs. In total, YTD 2021 surpassed my expectation on potential returns by far but more on that later.

Transactions Q2:

In Q2 I liquidated my remaining travel basket positions (Southwest, JD Wetherspoon) as I had growing doubts on how well tourism recovers. This seems to have been one of my better “timing calls” as both shares trade now significantly below the level I realized. I guess there are many reasons for this, for JD Wetherspoon also the lack of willing employees and potential wage inflation might play a role.

I also sold SFPI, obviously too early in hindsight. The reason was as explained that I had initially bough into DOM Security and that I should have exited SFPI after the take over /exchange offer as SFPI is very different from DOM Security (more cyclical, lower margins, turn around). I also exited Just Eat Takeway.com Grubhub (JET). As I have written, I feel that my analysis was incomplete and that at the moment the stock and the business is “Too hard” for me to get comfortable.

In addition, I reduced Euronext by the amount that I bought via the rights offer and I reduced Agfa by 1/4.

The new position in Q2 all went in the the Energy transition basket: Aker Horizon, Orsted, Nexans and NKT. AT the end of the quarter, all these positions were “in the green” but the stocks are surprisingly volatile.

The current portfolio as always can be seen on the portfolio page of the blog.

Comment: “Expectation Management”

As I have mentioned a couple of times, I do believe that behavioral aspects of investing are as least as important as technical aspects in investing.

Being able to analyze complex balance sheets is good, but it doesn’t help if the expert is not able to manage a portfolio through the unavoidable booms and busts of the stock market.

A very important point in my opinion both, in business is how to set challenging but realistic expectations. Especially these days there are a lot of books about very successful founders who are famous for setting very unrealistic expectations and succeeding. Steve Jobs with his “reality distortion field”, Elon Musk, Jeff Bezos, Jack Ma or Masa Son are some of the most popular founders that have become mega billionaires by aiming super high and pushing their companies always to the extreme.

On the business side, these success stories are subject to the so-called survivor bias. These individuals are indeed successful but it is never clear if they have been successful because of or despite of their “aiming very high” approach.

In contrast to the founders mentioned before, Adam Neumann. Lex Greensill and Markus Braun were also founders/CEOs who aimed very high, but in their cases (and in many others), this approach often ends in disaster. There are now several books for instance on Wirecard and what stands out is the disconnect between Markus Braun who formulated growth targets and the business, which had now way to reach these unrealistic targets and at some points turned to fabricate profits. The same happened at WeWork and most likely also at Greensill as well as Enron and General Electric. I think when the current Tech Mania ends, we will see much wore Wirecard or Greensill like situations than the next Google/Amazon/Alibaba etc.

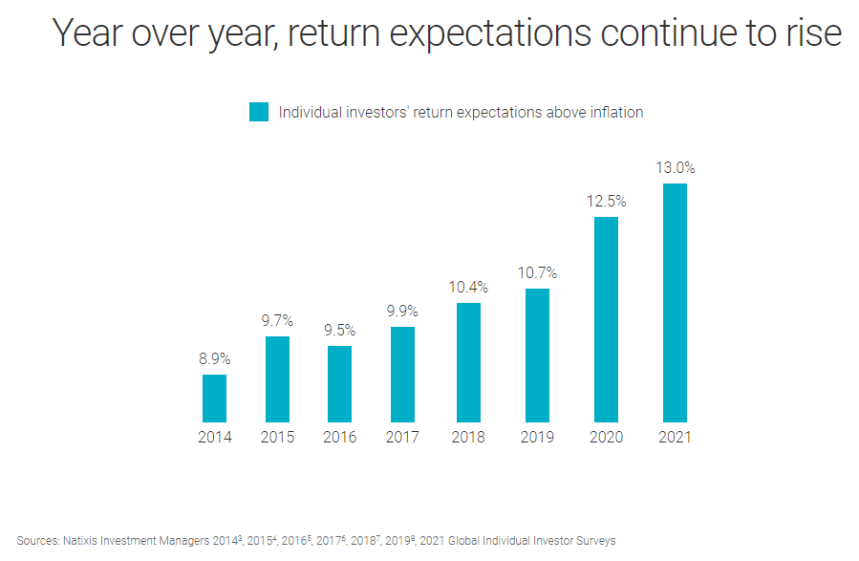

On the investment side, I already linked to a very interesting post from Michael Batnick that shows that investors seem to have increased their return expectations over the past few years significantly. I found this graph especially stunning:

As the graph states, these are return expectations above inflation, so in nominal terms this transaltes into current return expectations of 15%+.

Such expectations are in my opinion dangerous, especially when this leads to the following behavior:

- increased risk taking to achieve these expectations (leverage, theme/hype/meme stocks, Crypto)

- a reliance on these returns to materialize (i.e. return targets in pension funds, paying of expensive mortgages etc.)

The combination of these two aspects often leads to a catastrophic outcome for those who are hit and often these investors don’t survive a downturn that will inevitable come.

I think for the “average investor” it is very important to set realistic expectations and achievable benchmarks. Ted Weschler with his 40 years, 30% p.a. track record is maybe not the right benchmark. if you start playing golf and you think that Tiger Woods is your benchmark, You are most likely on track to long term disappointment.

And to achieve one’s own saving goals, one should be aware that a “normal” long term equity return from the current level is more in the 5-6% nominal range than the 15%+ nominal in the graph above.

To be successful in the stock market, the most important “super power” is the ability to stay invested over long periods of time. I do think this can be achieved better by lowering expectations to realistic levels and then enjoying potential better outcomes than the other way round.

For my own portfolio, I do not think that the 14% p.a. since the inception of the blog is a good indicator of what I can expect going forward. I would be pretty happy if I can achieve the nominal equity premium of 5-6% plus maybe 2-3% outperformance (before taxes) going forward for the next 10-15 years, assuming taht interest rates stay low.

{kind=link}

Nice results! This is a year when many brand name funds (mostly in long/short space) are having a tough time!

SFPI: Still long, but I also think this is not a forever investment. As you have seen alternatives with better risk-adjusted expected returns, it must not have been a mistake to sell. (I would not look at the sell decision in isolation.) At least you have no problem to find new buys. My mistake was shorting GME at the wrong time (arguably more stupid).

Expectations: I am at 25% cash (ex long-term “Altbestand”) now and my return expectations are lowest since the financial crisis. Nonetheless, I am up 30% ytd. Just cannot find screaming buys and I am patient. I would be very happy with 5-6% real returns over the next 10 yrs (even without outperformance who cares). After tax 3% real returns would be really great. If inflation would be 10%, that would be unrealistic though (just typical German angst). Inflation would be taxed. We have been very lucky being in the market the past years and I cannot understand those high expectations.

Good luck + skill alpha!