Paypal – Too old for Rock n’ Roll and too young to die ?

Management summary:

In this post I try to explore if Paypal is suffering only from temporary issues or if they have structural problems. My take away from a rather short analysis is that the problems are indeed structural and therefore the stock is not of interest to me for the time being.

Introduction

Paypal is one of those stocks that is both very present on my “”TwiX” timeline as well as has been mentioned in a couple of recent discussions with investors that I value highly.

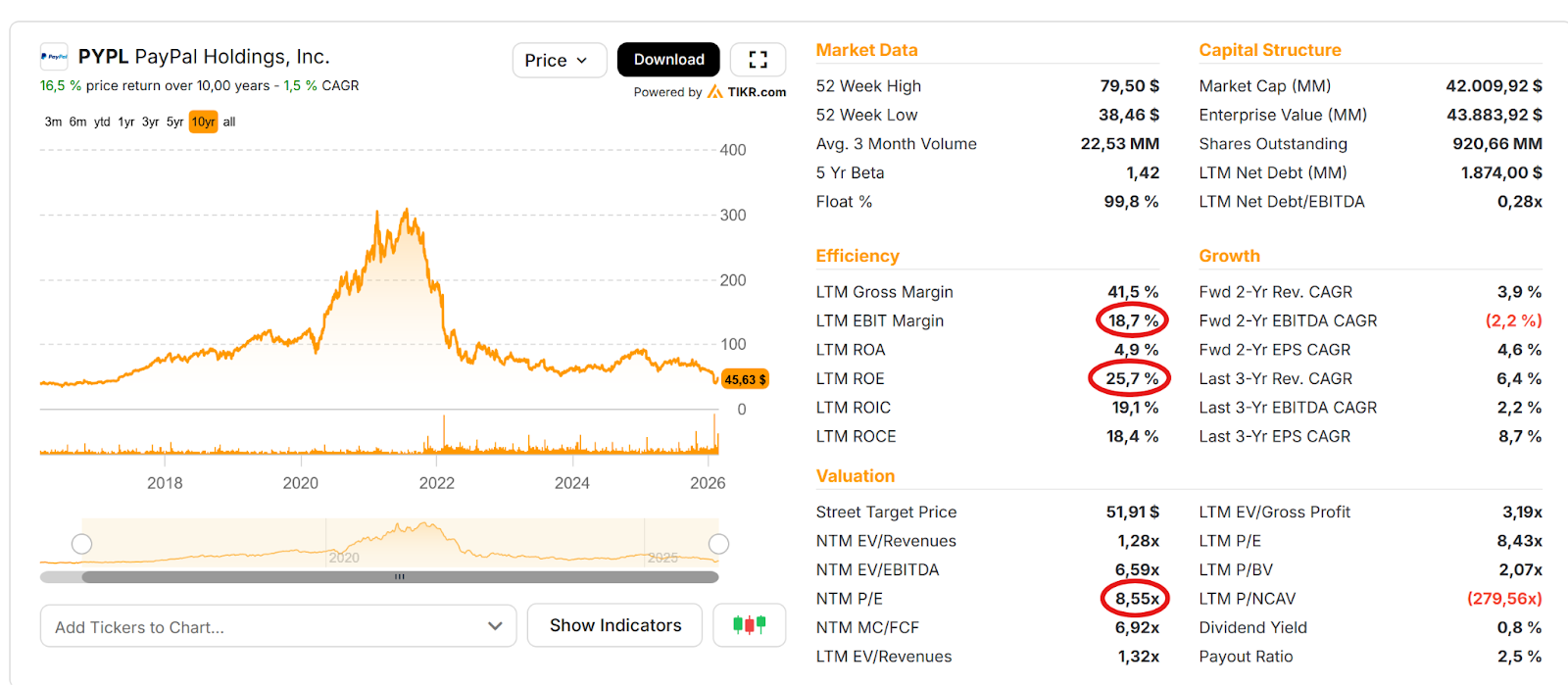

At first sight it looks like a decent “Value” stock. Single digit P/E, large share buy backs, high free cash flow, good margins, decent ROE, hundreds of millions of clients etc. So what is not to like ? Here is the TIKR overview:

Paypal is also one of those stocks where everyone has an opinion as almost everyone has a Paypal account or is using other payment services frequently So at first sight, it looks like an easy to understand business which might lower their “barrier to entry” even for more inexperienced investors

Personally I have to admit that I find the payment space super complex and not easy to understand.

What problem does Paypal solve ?

Paypal’s main business is to allow retail customers to pay online for E-commerce activities and/or send money from one user to another within the Paypal network or via their additional P2P service Venmo.

Paypal has become successful because for consumers it used to provide a very convenient way without a lot of friction as compared to typing in your credit card details every time you use a new online merchant for instance. Paypal was also one of the first widely available services to send P2P money. You just need to know the Email address of the recipient.

Paypal describes itself as a “2-sided market place” connecting retail clients with E-commerce merchants.

For merchants, this was initially also very attractive as Paypal removed friction and increased the probability that a customer would actually finalize the purchase.

What Problems does Paypal have ?

When a widely known stock such as Paypal looks obviously cheap, my first thought is always the following:

What obvious problems does that company have and do I have a “variant perspective” ?

Especially for larger US stocks, assuming that everyone else is just stupid and you are the only one who can identify a single digit P/E ratio is naive to say it in a friendly way.

For me, temporary problems would be an invitation to dig deeper, whereas structural problems are much harder to handicap.

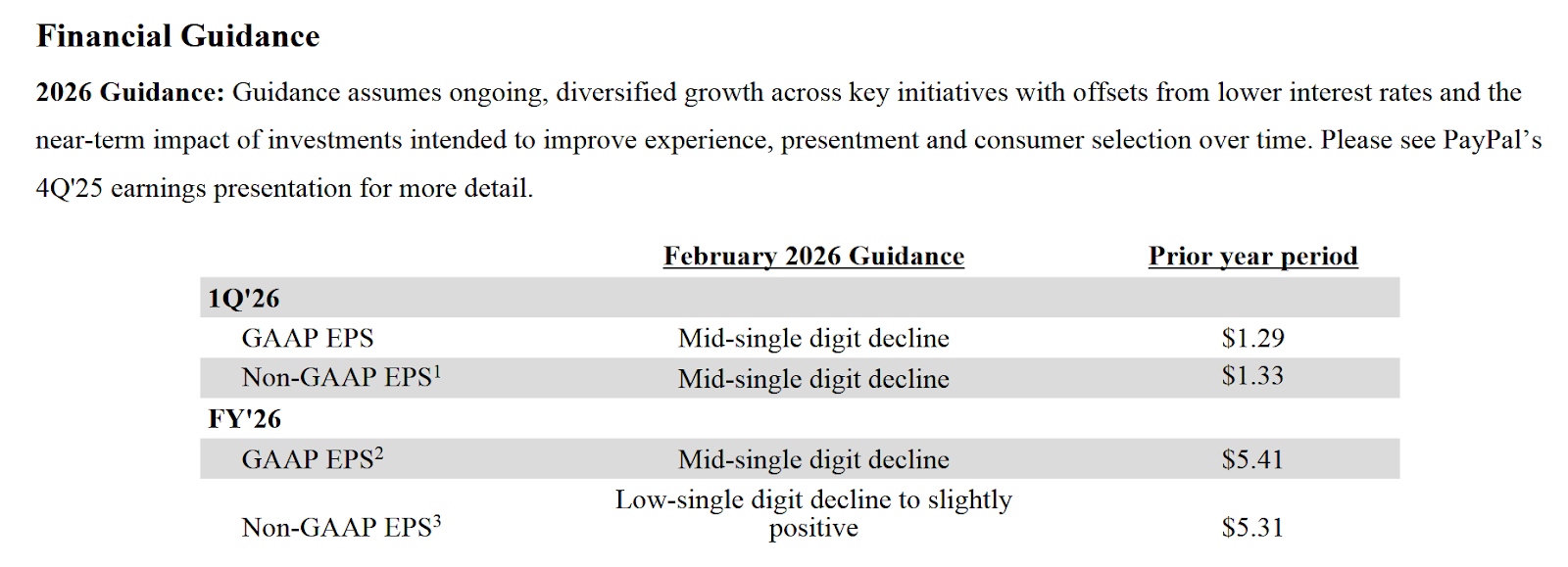

Paypal has some obvious issues, one of them being having a new CEO with little experience in the actual business and having guided to lower sales and profits in 2026

The new CEO since March 1st, Enrique Lores, is a long time HP Executive, who, according to Linkedin, has no direct payment or financial services experience.

Lores has some strong incentives directly linked to the share price. He will achieve the maximum amount if the share price hits 125 USD until 2029. His maximum compensation would be ~125 mn USD. This sounds like a large sum, but for Lorres, an long term HP executive, even that might not be life changing. He seemed to have earned around 19 mn USD and his net worth is estimated to be at least 50 mn USD. So he is rich already.

The bigger problem is clearly that the 2026 outlook looked very bleak. Especially compared to competitor Adyen which guided to 20% revenue growth in 2026 and beyond and not to speak of Stripe which has grown gross transaction volume by +34% in 2025.

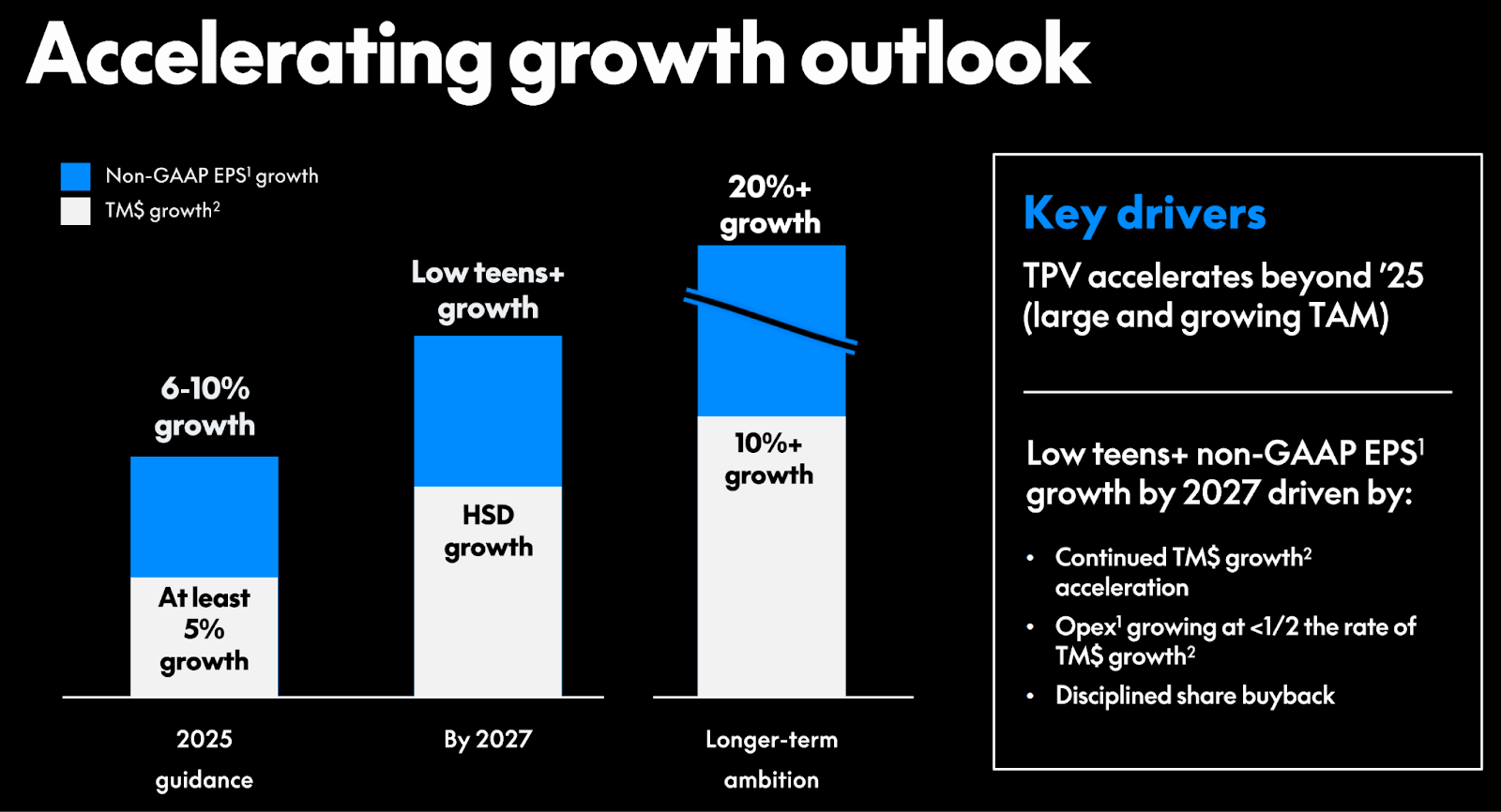

It’s especially interesting to look at the 2025 investor day presentation. Back then, the former CEO Alex Chriss, who had at least some financial services background from Intuit actually made a pretty convincing pitch positioning Paypal as a “commerce platform”. This was their ambition back then:

After shrinking in 2023, Paypal delivered some growth in 2024 and also some growth in 2025 but as mentioned above, next year looks like shrinking again.

2025 results looke d“okayish” but on a quarterly basis, growth decelerated each quarter which most likely led to the dismissal of the old CEO-.

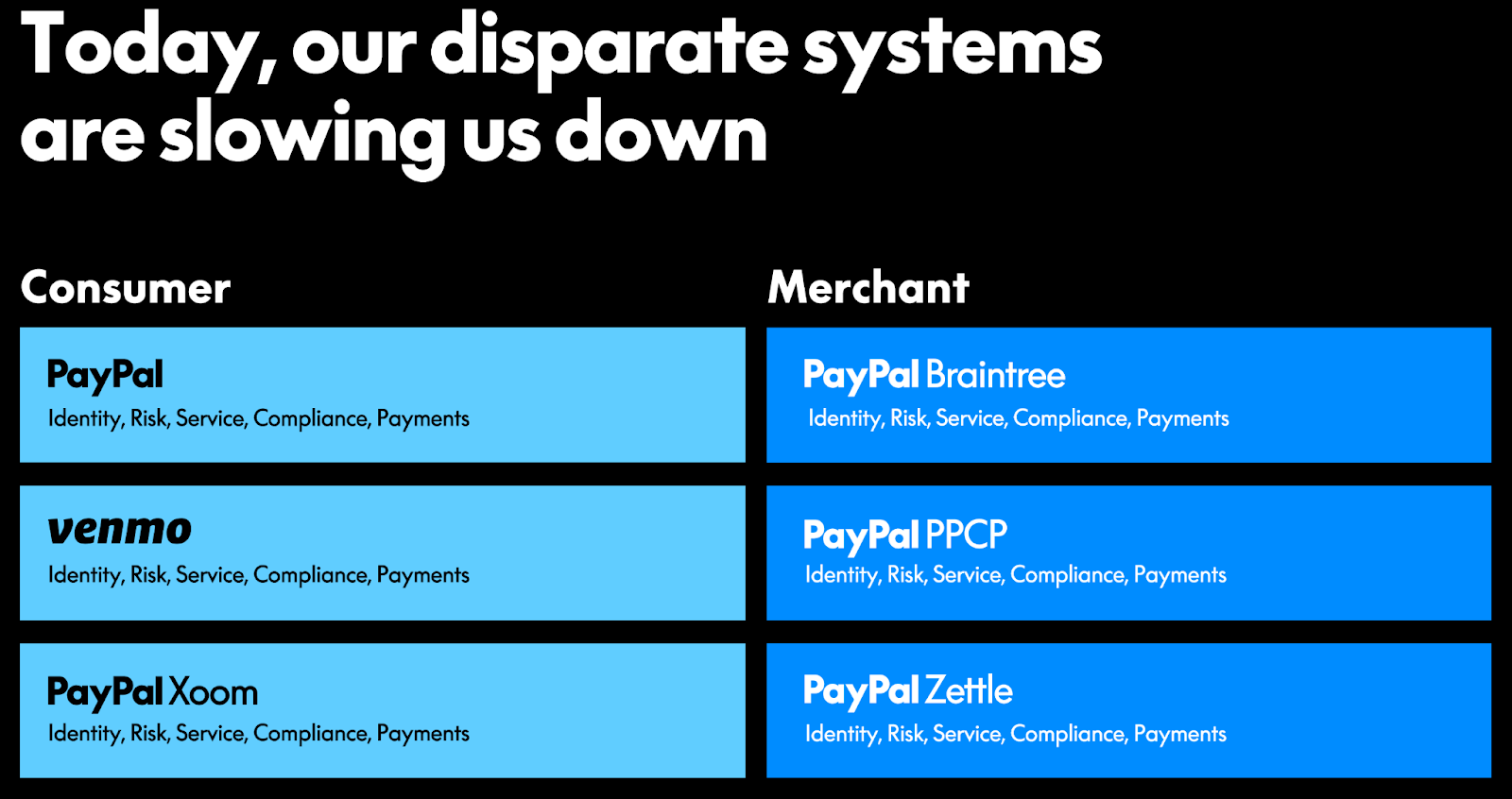

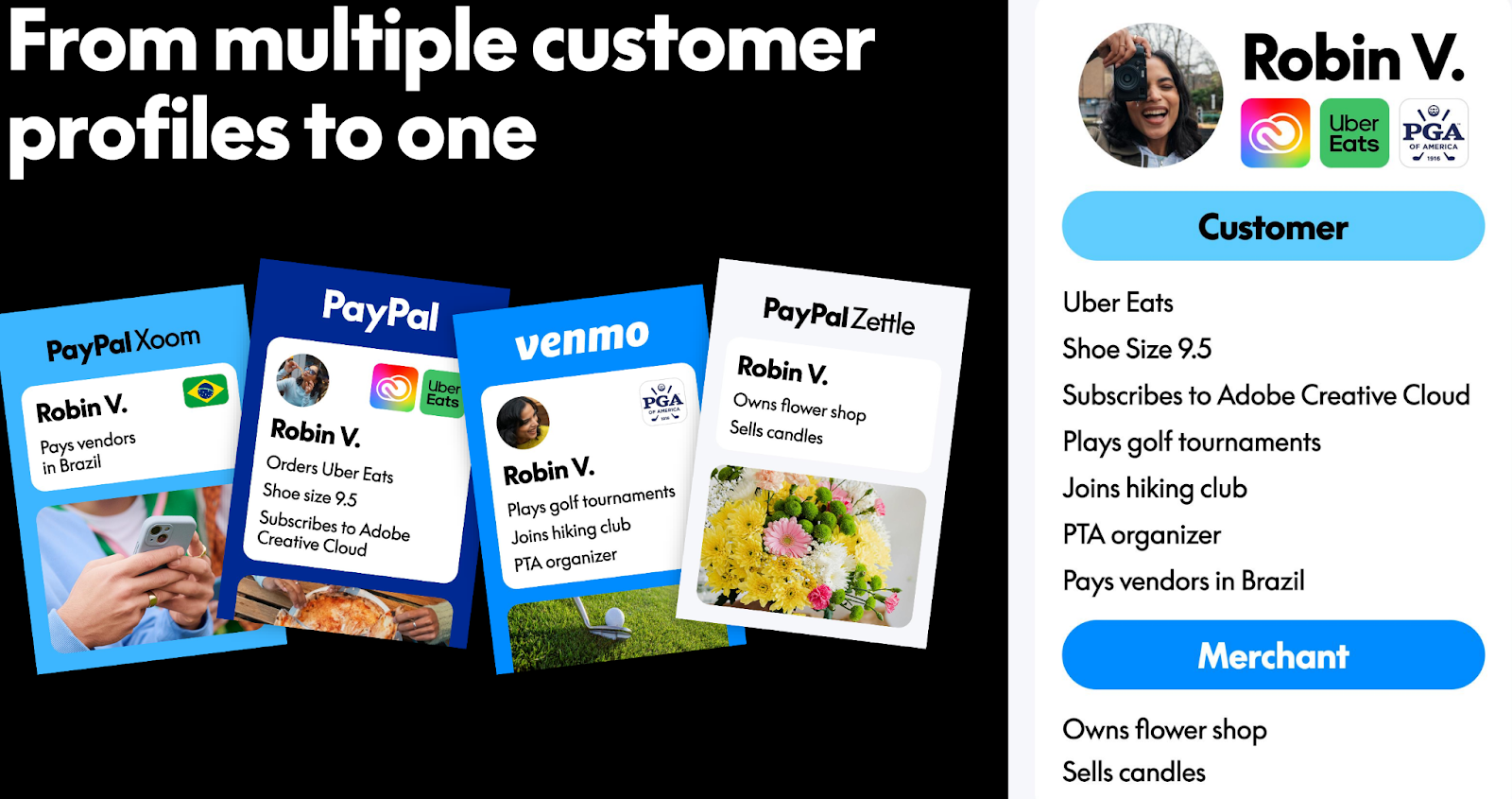

One of the major issues seems to be that Paypal runs at least 6 different platforms within Paypal according to this slide:

According to this slide, one user might have 4 different IDs across the Paypal services which are not connected so far:

Technical debt: Separate & outdated technical infrastructure vs, competitors on the merchant side

The chart points to one of the main weaknesses of Paypal: Paypal can be considered already a legacy player in the payments space. They have created separate platforms for separate use cases that are now just very difficult and expensive to handle.

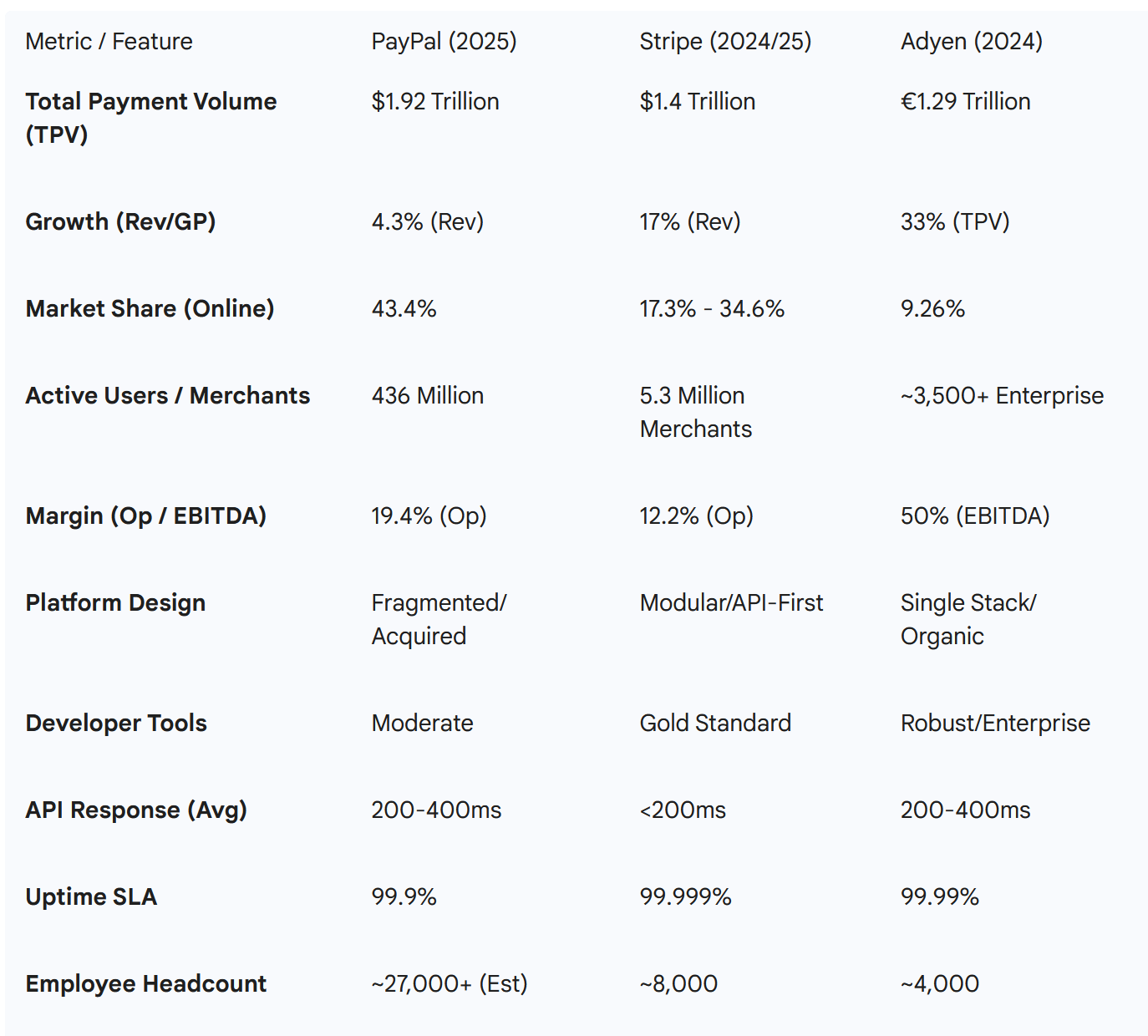

The newer competitors from the merchant side like Stripe or Adyen all have one platform that runs all of their activities which makes it a lot easier to react and improve upon.

What is also interesting is that Paypal employs more than twice the employees of Stripe and Adyen combined. This is a table that Gemini compiled for me.

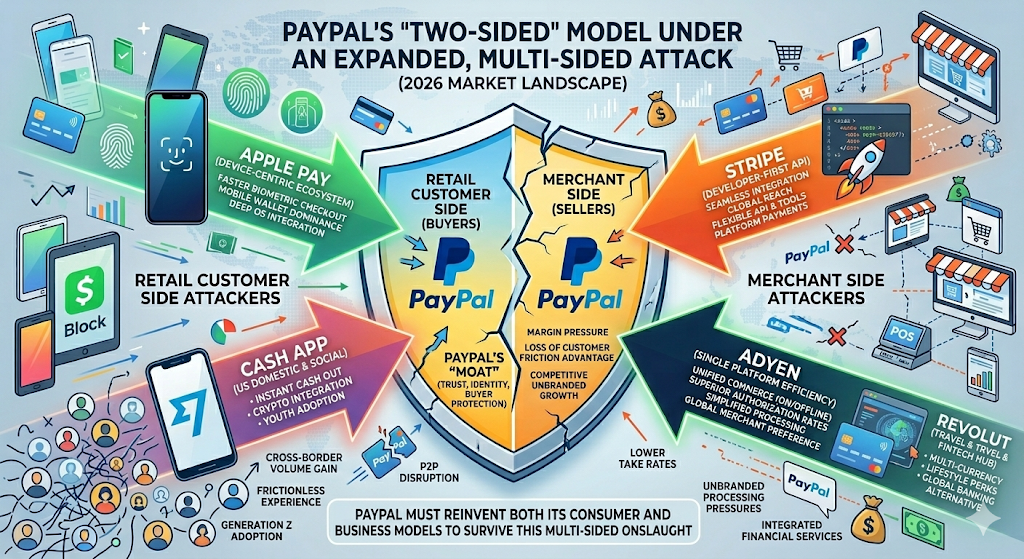

Additional attacks on the retail client side: Google Pay & Apple Pay, Revolout, Wise, Cash App etc.

As a “2 sided market palace”, Paypal unfortunately is also subject to massive disruption on the retail customer side.

If you are a mobile user, the probability is high that if you purchase something offline or online it is most likely down directly via your phone. You either hold your phone to a POS terminal in a physical shop or you confirm the purchase with a finger print or face scan of your phone which is even more convenient thant the Paypal Check-out.

At P2P level, both Paypal services are subject to a lot of competitors, such as Block’s Cash app, Revolut’s free transfers or Wise’s international transfers.

So simply said: there is no place to hide for Papyal.

Paypal is the most expensive option

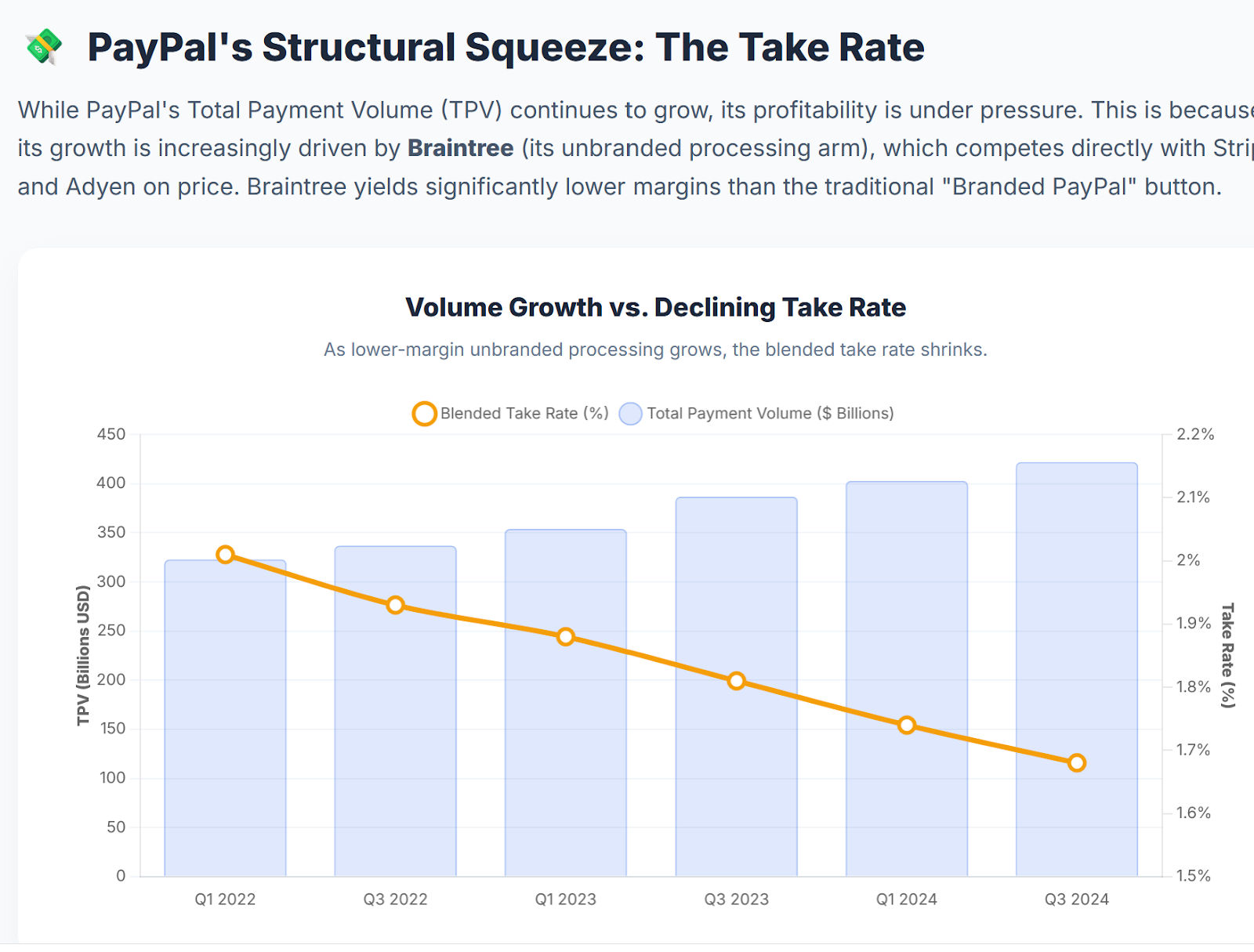

Some people will argue that Paypal is currently maybe the most profitable of the payments players. The main driver of this profitability is that Paypal charges significantly higher prices, both to merchants but also for instance for international transfers.

What looks now as a strength could turn out to be a weakness. “Your margin is my opportunity” was the famous motto of Jeff Bezos. The “take rate” of Paypal is heading down for quite some time (Chart from Gemini) as growth comes mainly from lower margin products:

Paypal is under attack from all sides

Bringing it altogether is this graph that I asked Nano banana to create:

Paypal is the legacy player that gets attacked from all side from very agile and large competitors who have a much more modern infrastructure,

That’s the reason why Paypal is cheap. The last CEO tried to counter that but obviously was not very successful.

The Stripe take-over rumour

In the past few days, suddenly a rumour came up that Stripe might buy Paypal. To be honest, these kind of “someone told Bloomberg” rumours are often false.

As far as I understand Stripe’s business model, Stripe would have little to gain from a takeover. As a pure B2B company, I am not sure that the retail client base is of interest to them and if they could leverage that. And on the B2B side, Stripe can already do what Paypal is doing and I am not sure if they want to clean up the technical debt.

I guess Paypal would be a more interesting target for someone who might be able to leverage the retail customer base, but at 40 bn plus market cap plus premium it is maybe to big to be swallowed by most of the Fintech players.

“Too hard” for me

For me, the outcome of this quick exercise is that Paypal’s problem seems to be much more structural than temporary which for me makes it “too hard” to invest into.

Maybe the new CEO will pull all the levers and manage to turn around the business. But maybe he will not. It will be interesting to see if he will be able to implement a “kitchen sink” approach and maybe sacrifice a few quarters with really bad results or if the pressure is high to keep up share buy backs which will make it difficult to pay off the “technical debt”.

For the time being, Paypal looks similar to the hero of Jethro Tull’s song “Too old to Rock’n Roll”:

The old rocker wore his hair too long

Wore his trouser cuffs too tight

Unfashionable to the end

Drank his ale too light

Death’s head belt buckle, yesterday’s dreams

The transport caf’, prophet of doom

Ringing no change in his double-sewn seams

In his post-war-babe gloom

Now he’s too old to rock and roll

But he’s too young to die

Yes, he’s too old to rock and roll

But he’s too young to die

But anyway, this does not look like something that I would be comfortable to be invested in despite the superficially attractive “value KPIs”.

If someone has a very different view from the business perspective with regard to the competitive landscape, I am willing to listen 😉

Bonus Soundtrack:

Of course my choice is Jethro Tull – Too old to Rock n’Roll

Jethro Tull – Too Old To Rock’n’ Roll (Supersonic, 27.3.1976)

Why does your blog say “100% hand crafted, no AI Slob allowed” – but now there is AI generated content everywhere…

I write every article by hand but as I explained in detail, LLMs have become an important tool for me during my research process.

If I use the output of an AI Model, I clearly state it which I did in this article.

If you don’t like it, then my advise would be not to read it.

In payments, Nexi is single digit PE, pays 10% dividend yield with market leadership in Italy and Nordics.

Thanks. I didn’t have them on the radar.

>”Especially for larger US stocks, assuming that everyone else is just stupid and you are the only one who can identify a single digit P/E ratio is naive to say it in a friendly way”

This is an excellent quote!

I also think that PayPal will be around for a long time, especially since shops cannot easily/legally pass the fees on in a transparent fashion and thus incentivize switching to other payment options when you have been using PayPal for 10-20 years.

And who knows: If the EU does come up with a payment system to bypass the US companies, that might change the sentiment for payment providers quite a bit. But we’ll see whether this ever materializes… I have my doubts.

Anyway, investing in PayPal may be more like investing in a utility company, alas without receiving dividends 😉

Thanks for all the work!

There is actually a new European payment system called Wero. We will need to see how this works.

Of course papypal´s different “storefronts” to the customers are too many and make little sense. However I think it is quite normal that a person has to use different service-providers in different situations/roles. One does not use the company´s credit-card for personal shopping and vice versa.

As far a management is concerned I would agree that adyen for example is more founder-led and aligned with shareholders´ interests. To me the main problem seems to be a weak management culture over the last years and a general perception that shareholders get ripped off. Since 2016 paypal has spent roughly $30 bn on share-buybacks (most of it over the last 5 years) , however, share count has only come down by aprox. 250 mn shares versus the 500 mn shares that could have been reduced (assuming a an avg. purchase price of $60/share which was available in the market for roughly 5 out of those 10 years). So $15 bn went to the employees/management.

If you read their annual report 2024 the first 120 pages or so are all about management compensation. The firrst interesting information reagarding results from operations comes on page 169. Just another indicator of priorities here.

On the positive side one might argue that they will profit from ai (reduce headcount) and I think it is also plausible, that there is a certain stickyness of business-partners (does one really expect airlines or train-operators to move exclusively to Stripe or Wise?). However a gradual migration is certainly possible and even likely if large partners start to work also with paypal´s competitiors.

Since the management-history of paypal seems to be still intact this an investment I would not consider for the time being.

Thanks for the comment. Good point, both,Adyen and Stripe are still founder led. Block, too.

Good analysis.

Concerning technical debt and headcount, I think the market is currently quite inconsistent in its assessment of AI and software companies. Using essentially the same argument applied in many other software company sell-offs, one could argue that “technical debt” — as well as a cleaner or newer technical platform — should be heavily discounted and no longer represents much of a moat.

In general I think the market underestimates a bit PayPal’s network effect and also brand. But we will see.

Thanks. Indeed we will see. At least, the previous CEO was very aware of the problem. That’s at least a start.

I follow your blog and really enjoy the content. Maybe one comment on this….

“Especially for larger US stocks, assuming that everyone else is just stupid and you are the only one who can identify a single digit P/E ratio is naive to say it in a friendly way”

I think it is possible and there has been many examples of mispriced assets. Look at Meta at 130 EUR or Google last year at 150 USD both with very low P/E ratios at that time. With the current market sentiment is the main driver and value comes later.

Keep writing and wish you good luck on the market.

Have followed this blog for probably a decade via an RSS feed. Going to unsubscribe because I have zero interest in analysis based on an AI output that I don’t trust to deliver consistent, accurate information. Thanks for the memories!

Well, then I would say ” Hasta la vista”. Maybe to clarify: I write and analyze myself, but I use AI as a tool.

And I clearly mark any output from AI tools.

Good riddance to paying attention to a blog too lazy to do their own work. No wonder your performance is tanking. Expect you will continue to underperform the market because of it.