Private Equity Series (8): The “Stonepeak precedent”, a “Dirty PE Industry Secret” and what it could mean for the Industry

No one has asked for it, but here it is, the next episode of my Private Equity series. Previous episodes of the Private Equity series can be found here:

Private Equity Mini Series (1): My IRR is not your Performance

Private Equity Mini series (2) – What kind of “Alpha” can you expect from Private Equity as a Retail Investor compared to public stocks ?

Private Equity Mini Series (3): Listed Private Asset Managers (KKR, Apollo & Co)

Private Equity Mini series (4) : “Investing like a “billionaire” for retail investors in the UK stock market via PE Trusts

Private Equity Mini Series (5): Trade Republic offers Private Equity for the masses (ELTIFs) -“Nice try, but hell no”

Private Equity (Mini) Series 6: Private Equity for the masses – Y2K edition

Private Equity Series (7): Secondaries – The Magic Money Machine for the PE industry

Background:

Everyone in the alternative (non-listed) investment space has been talking about the Blue Owl Private Debt “redemption gating” event lately, but in my personal opinion, another story which has not been so widely reported is much more interesting.

The case of the first Stonepeak Infrastructure Flagship fund is at least equally interesting for the whole Private Equity sector and I will try to explain why.

Traditionally, the Private Equity business model can be summarized from the the perspective of the Asset Manager or General Partner (“GP”) as follows:

GPs take a big junk out of any upside (usually 20% ,sometimes more) but themselves have very little downside risk as they charge a hefty 2% p.a. fee in any case and only, if at all, invest relatively little money themselves into the funds they manage.

So let’s look at Stonepeak. Stonepeak is one of the leading Alternative Infrastructure Equity Asset Managers in the world and has 89 bn USD Assets under Management. It is still privately owned.

Infrastructure was actually one of the few bright spots in the Private Equity space in the past few years, where fundraising still works, in contrast to the “normal” private Equity funds.

Although the dividing line between Infrastructure and Private Equity is a little bit blurry, Infrastructure investments are often “capital heavy” and considered more safe despite usually significant leverage. Typical assets are ports, Airports, railways, toll roads but also stuff like container leasing, warehouses etc. (among others Stonepeak bought the Canadian Port Operator Logistec which I owned)

Target returns for Infrastructure funds are usually a bit lower than for Private Equity (usually maybe 10-15% p.a. vs. 15-20%) and fund duration is often a bit longer. But infrastructure should be also be more robust, i.e. have less downside than a PE fund.

Stonepeak was founded in 2011 and launched its inaugural “Flagship” fund in 2012.

Now comes the interesting part:

A few weeks ago, the founder of Stonepeak, Mr. Dorrell, pledged personal support for the rather badly performing initial flagship fund.

Although it is not unusual that Alternative Assetmanagers might maybe reduce fees going forward if a fund performs really badly, this is the first time that I have actually seen that an owner actually puts in personal money to make good on the not so great performance of the investors. Here is how it should work:

According to the article, the initial fund had “promised” 12% net IRR to investors at launch but currently, after 14 years it only shows an IRR of 7,4%. Not a catastrophy at first glance but also not great either for such a vintage that should have benefitted from a significant decline in interest rates which was especially beneficial for “long duration” infrastructure assets.

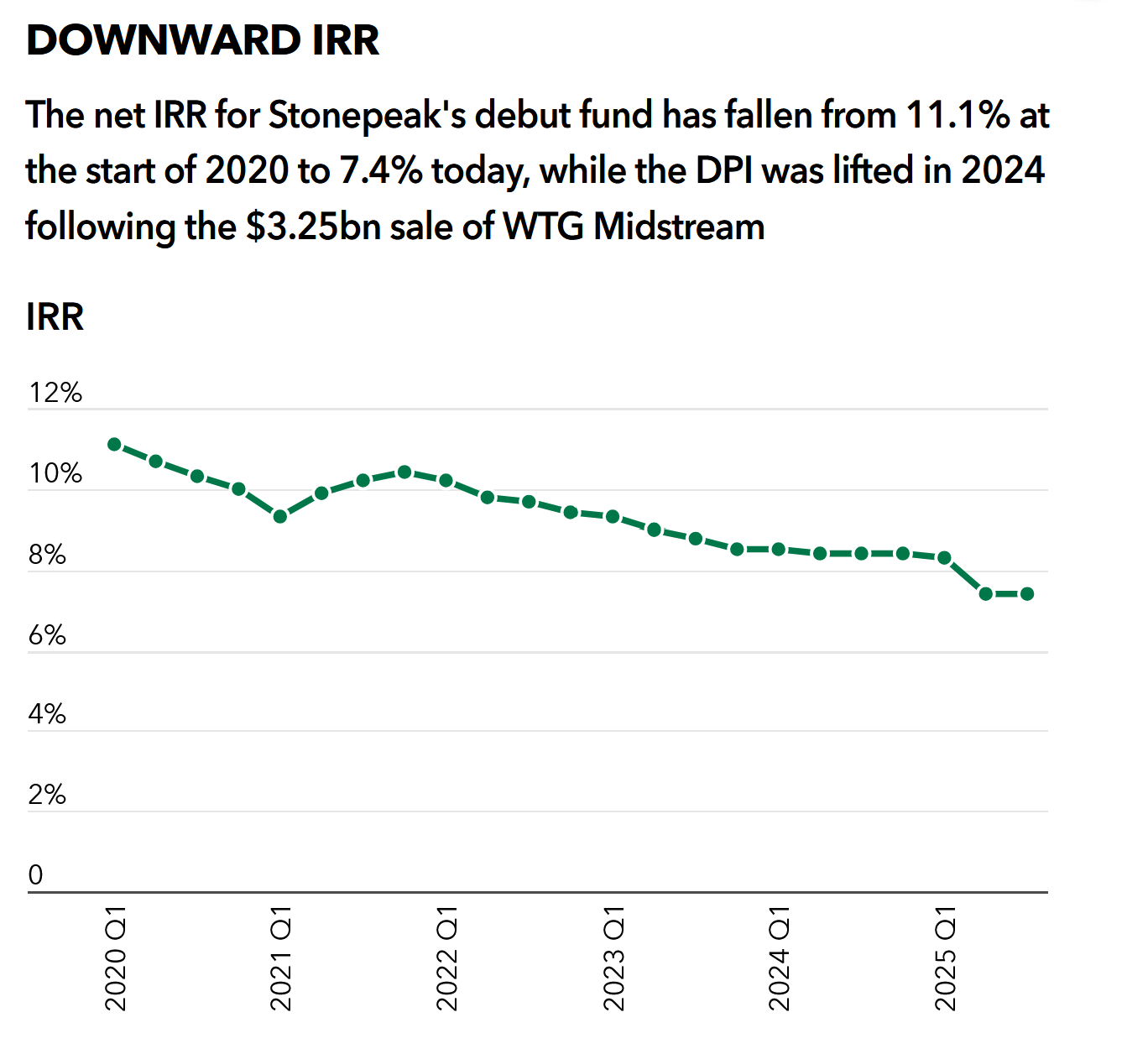

What is also really interesting is that graph that shows how calculated IRRs have developed in the last years from the perspective of investors in this fund:

Until 2020, i.e. for the first 7-8 years everything looked fine. But what happened then ? And why is this relevant ?

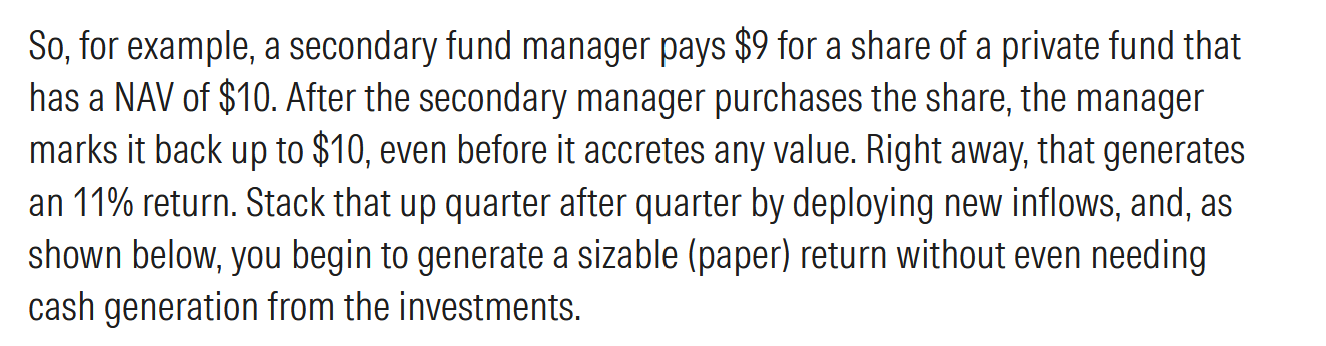

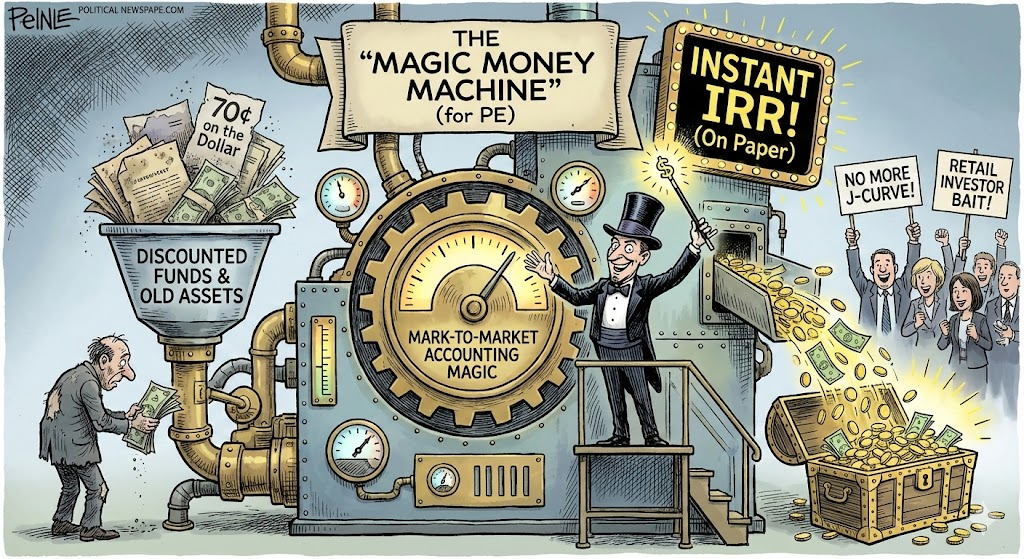

I guess it’s now time to tell you a little bit about a “dirty secret” of the Private Equity (and Private Infrastructure) world.

Whenever a new firm gets created and launches an initial fund, it takes a long time until investors can see actual results. On average, in the infrastructure space, investment are sold maybe 6-10 years after they have been bought.

However, Asset Managers don’t want to wait until then to raise a new fund. They want to raise funds more frequently in order to earn more fees. Normally the “fund raising” cycle is ~ 3-4 years.

Even professional investors invest mostly based on past performance, often just simply extrapolating those past numbers in the future.

So what do you do when you have no exits to show ? Of course, you just mark up your portfolio yourself based on some loosely defined metrics which often is coincidently very close to the target return. So just to say this again: In the beginning, almost all PE/Infrastructure funds are marking up their investments “at will” to show a decent performance, of course with the hope that later on, they will actually realize those returns or even more.

You then can present this (unrealized) return to investors and they happily invest into the next fund and the next etc.

In Stone Peak’s case they were quite busy and raised another 3 funds during the time when performance was looking still OK for the initital fund in 2020 as we can see here:

The funds got bigger and bigger, Fund III was ~7 bn and Fund IV 14 bn. And they are currently raising fund V with a target size of 15 bn,

Most of that money got raised with investors looking at the track record and saying: Fund I looks good at 11% p.a. (or maybe even more in the beginning) and I guess Stonepeak was telling them that this was marked “conservatively” (GPs always say that about unrealized values).

But it turned out to be wrong and clearly overvalued. And this is clearly embarrassing for Stonepeak.

If I were a potential Stonepeak investor doing Due Dilligence, I would ask: “How can I trust all the other performance numbers of your funds when the only one which is almost realised seems to have been significantly overvalued ?”

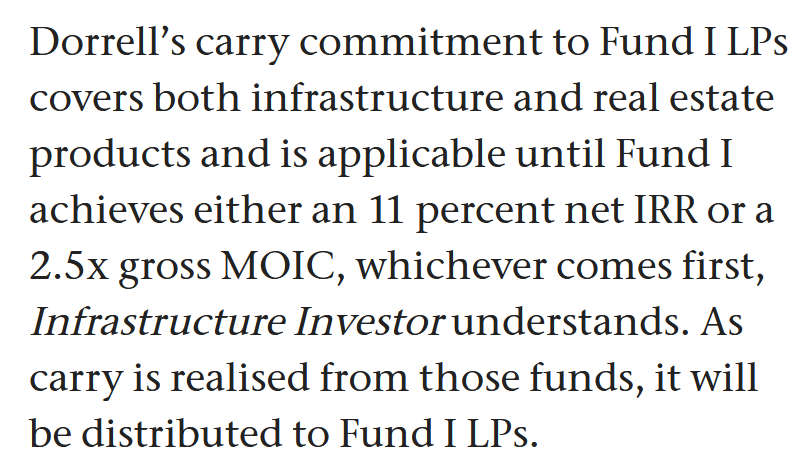

I guess that’s why Dorrell wants to make those investors “whole” with personal money:

As the first fund is significantly smaller than the follow up funds, this will not bankrupt him, but anyway, this is an industry first.

The industry relevance in my opinion is the following:

We can expect a lot more such cases where the initial, very positive performance will turn out not so positive at all or even funds may lose money (2019 to 2021 vintages for instance).

So far, this has always been the sole problem of the investor, never for the GP.

Michael Dorrell now created a high profile precedent that will be taken up with gusto by many disappointed investors.

The smart LPs will use the Stonepeak precedent to ask their GPs for the same “Commitment” to make good on their initial promise.

Otherwise they will not invest into a subsequent fund. Some GPs, especially the very big ones will resist, some will maybe just close up shop, but I guess a lot of GPs will get under a lot of pressure.

Overall, this might be a first step to change the relationship between GPs and LPs going forward. If you are an investor in any listed Alternative Asset manager, I think you should really pay attention to this. It could be that in the future, results might get even more volatile and in general lower if funds underperform.

Another relevant point is the following:

This case also puts a spotlight on how arbitrary especially early valuations are for these investments. Already last year, I heard rumors that auditors have begun to challenge valuations of PE funds as they see secondary transactions with large discounts.

I could also imagine that investors want better disclosure of unrealized return figures during Due Diligence and how those seemingly great early performance numbers got cooked up, or maybe not 😉

In any case, I am sure that there willl be a lot of interesting discussions already going on between disappointed investors and GPs, that’s for sure.

Timing wise, this comes at a pretty inconvenient time for most PE firms anyway. As this chart shows, the last year was not so good for the share price performance of the big shops:

Maybe we will see a turn-around at some point in the future, but for the moment I see more headwinds than tailwinds for the industry overall. If more GPs are forced to compensate investors, then valuations for those guys would need to come down significantly.