Quick Updates: EVS Broadcast, Thermador, Eurokai and Sixt

The last few days are super busy with 8 (or more ?) of my companies reporting 2025 numbers. That’s why I do only the first 4 right now, the others (Jensen, SFS, Bois Sauvage and Italmobiliare) will follow soon.

EVS Broadcast 2025 preliminary results

EVS released preliminary numbers last Friday. At first sight, they were a little bit of a “mixed bag”. Revenue was up which is good for an “odd” year, EPS slightly down.

EVS explained that that they have invested into people to penetrate especially the US market. The second half of the year was really good, the first 6 months were weaker, mainly because of the “Tarif tantrum” from Uncle Donald.

The outlook for 2026 was quite good:

In the call, the CFO mentioned that for 2026 they don’t plan big additional investments into staff and that more M&A could be possible.

According to TIKR, analysts expect EPS of 3,36 for 2026. So far, the development is roughly within the initially expected case from 2024. Knowing EVS, there is also a good chance that they will revise 2026 numbers upwards during the year.

The 1,20 EUR dividend will compensate for waiting a little bit longer although Belgian withholding tax is not nice.

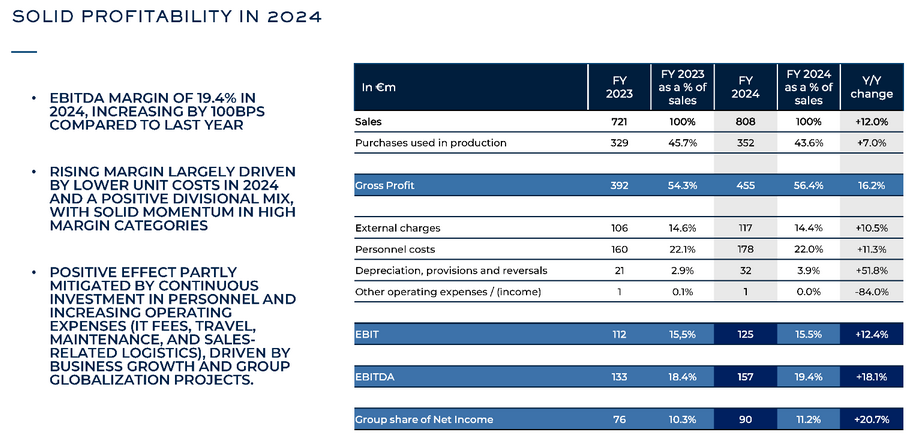

Thermador 2025 preliminary results

Thermador followed this week with 2025 results. As to be expected, sales were slightly negative y-oyy as construction and modernization is still weak in France:

What I find very surprising is how well the result kept up:

They managed to reduce working capital so they have a decent net cash position which should allow them again some M&A. And maybe, maybe the sector looks a little bit better in 2026. Analysts are quite positive. Thermador itself mentions a couple of Government programs which could be positive for them.

Thermador is a “hold” for me at the moment. Nothing to change here.

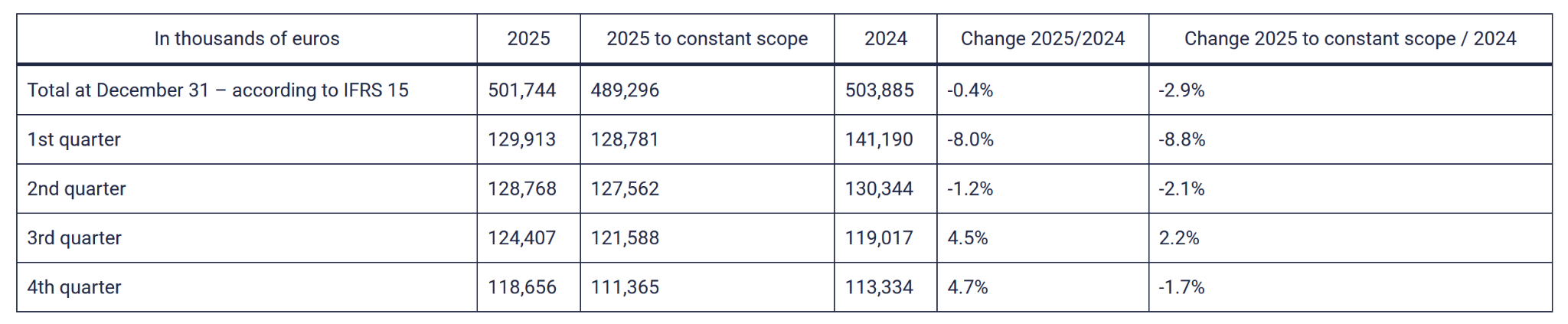

Eurokai preliminary results 20025

Eurokai also came out with an “Estimate” of the 2025 result. Typically for Eurokai, the result for 2025 will be significantly better than the revised estimates during the year.

They estimate now that 2025 Earnings will be above the 2024 earnings of 88 mn EUR (which included a 19 mn Non-cash positive one off).

Depending on what allocation the Golden share gets at Holdco level, this could result in an EPS of up to 6 EUR . Which means that despite the significant increase in the share price, Eurokai is still very cheap.

Investors should prepare once again for a very cautious outlook for 2026, although in my opinion, there are a lot of factors which indicate that 2026 could be once again better than 2025, even before any “juicy” one-off profits from partial sales to Container shippers.

The share price is now slowly approaching the historical ATHs from 2006/2007.

Eurokai is now by far my largest position but I leave that one untouched.

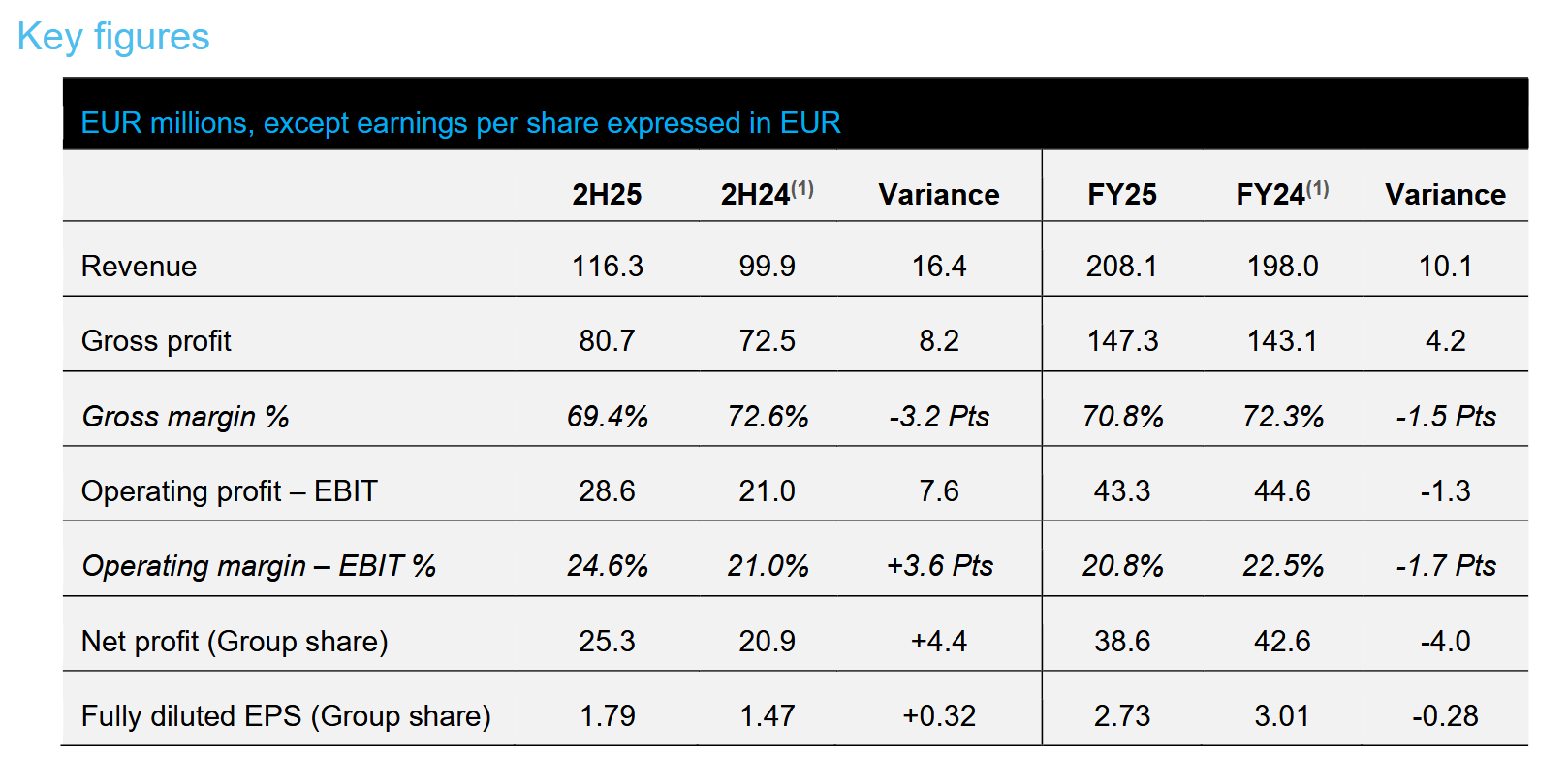

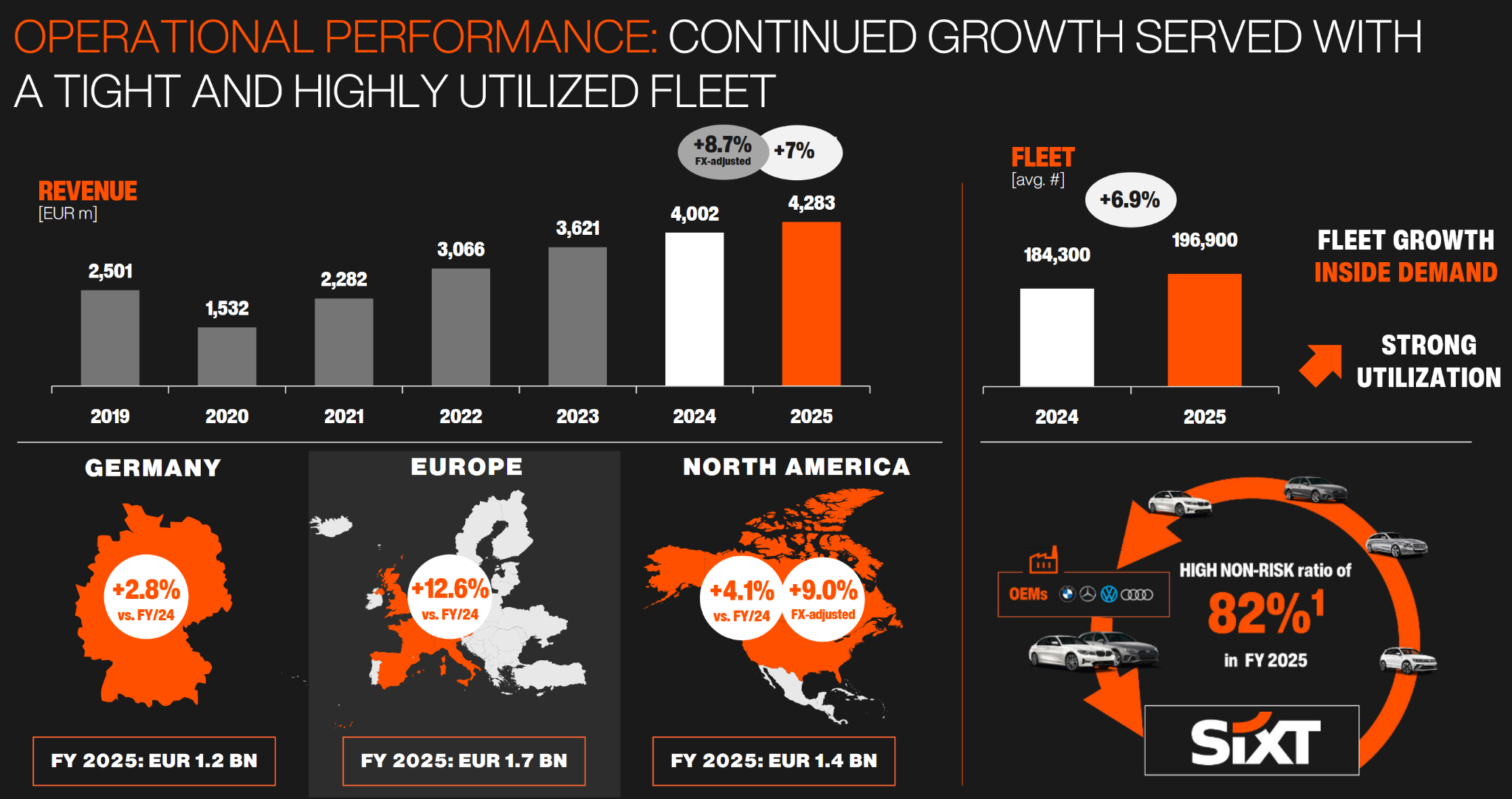

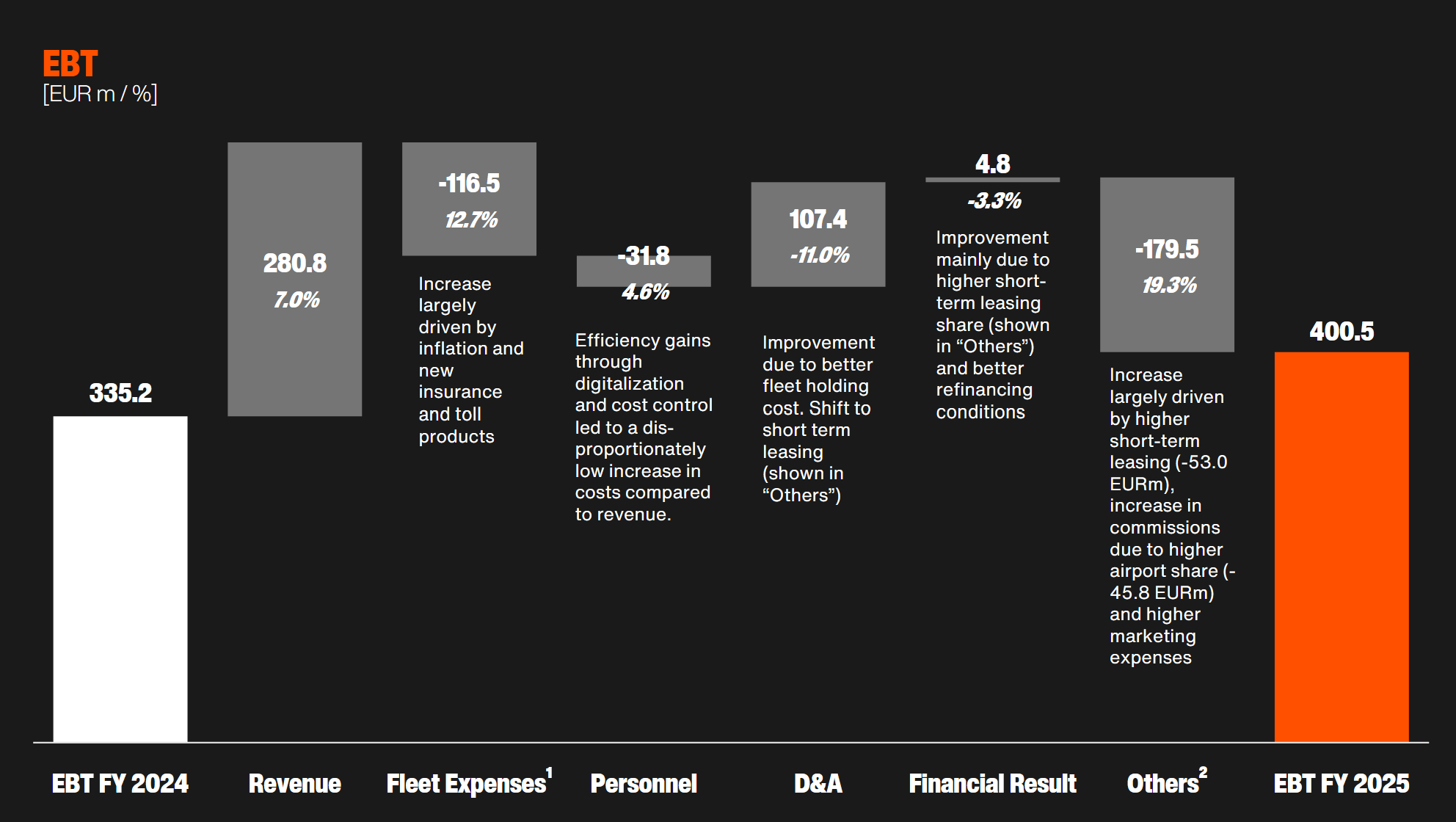

Sixt Preliminary results 2025

Sixt was the fourth company that week that released 2025 results. Although the results ended up to be a little bit below the forecast from Q3, it clearly seems that analysts have expected worse as Avis and Hertz both showed huge losses and declining revenues.

Sixt in contrast managed to grow also in the US:

And a significant increase in Profits:

What analysts seemed to have really liked was a quite optimistic outlook for 2026:

That seems to have surprised analysts and led to a “decoupling” of the share price from those of the weaker US competitors:

With a trailing P/E of 9 and a dividend yield of 5,8%, the pref shares are really “good value” in my opinion.

To be continued soon….