Since 1.1.2011 the Total Return is +181% or 7,3% p.a. Not great but also not a total Desaster either. Until year end 2023, the numbers were +650% and 16,8% p.a.

Nabaltec: You mentioned that the energy prices in Germany are a concern. My understanding from the annual report is that they get their steam heat from a adjacent waste disposal plant. They also mention that their energy cost is locked in until end 2024. Given the steam heat supply from the waste disposal plant, wouldn’t energy pricing be less of a concern here ? (Unless the price they pay for the steam is somehow linked to natural gas prices in Germany)

as always, sincere thanks for the update and the constant research! I also see that it goes on again pleasantly at TGV. I assume, that they also have sold Naked Wines in the meantime. Such a pity about this originally promising business model in the wine business.

Onvista hat mich informiert, dass Admiral die Dividende zum Teil als Barzahlung und zum Teil als Wertpapierzahlung (optional) ermöglicht.

Kannst du aus der Erfahrung einschätzen, ob sich die Dividende in Wertpapierform lohnen wird oder muss man dazu zunächst den Reinvestierungskurs, der von Admiral festgelegt wird, abwarten.

Thanks for your blog and the insights. I wonder why you did sell Aker Horizons given the steep discount compared to the price when you initially mentioned the position in your Energie Transition Basket. Did your assumptions change in this regard?

What are your thoughts on Admiral? I had been waiting at the sideline before the current slump which from My search is mainly down to a “peer” reporting slow momentum. Fun it hard to identify any fundamental problems…

Hey, i have a question regarding conviction vs. portfolio weight. Some of your positions which you see as long term holds (e.g. ACT, VEF) have substantially lower weights than some of your mere “hold” positions (e.g. TFF, Naked Wines). Why is that? Regards Mathias

How do you look at VEF AB since the last investment round of Creditas. It seems like Q3 was 4.5 NAV and 5.6 share price. and now more 4.6 share price and NAV around 5.6.

a question regarding Bouvet. Although a consolidation is not that surprising after this long lasting surge, the modest development compared to the market trend recently is striking. Do you ascribe this trend to particular news (change in CFO)? If there are no structural concerns the stock seems not that expensive at a leading P/E of 24, given the intact growth and the good margins…

do be honest, I try not to speculate on why a stock is doing what it does. Fundamentally, I will keep Bouvet as long as things are looking Ok, which they do.

Moin, vielen Dank für diese Seite. Was halten Sie von Silvano Fashion Group (Estland) und Grigeo (Litauen)? Erstere haben Probleme mit Wechselkursverlusten (Russland), letztere mit einem Abwasserskandal. Aber mit Blick auf den Free Cash Flow und das Geschäftsmodell an sich halte ich beide für deutlich unterbewertet.

Ihre Kommentare/Portfolio sind extrem fundiert – ich freue mich, wenn Sie Ihre Einschätzung teilen. Vielen Dank.

Naja, beide haben verständliches Geschäftsmodell und seit Jahren starken FCF, aber KGV 6. Ich dachte, Sie suchen auch nach solchen Wert…wenn nicht von Interesse, sorry, will Sie nicht langweilen.

Nun ja, ich hatte erhofft Sie erklären mir kurz das Geschäftsmodell oder hängen zumindest einen Link an. Sonst muss ich mir das erst mühsam raussuchen. Meine “to do” liste ist über 100 Unternehmen lang, dann muss ich effizient sein.

Hi,

the stocks that are in my portfolio are the stocks that I hold in my personal account. Some of them are there, for now, more than 10 years. Once a year I do short summaries of my positions, the posts are called “My xx stocks for 20xx”. You might want to look at the last one to see which positions I am very comfortable with and which positions are shakier.

In general, I do not recommend any shares as I do not provide investment advice. Please consider what I write as my personal diary. of a long-term investment journey. So just looking at the portfolio page without reading the corresponding posts is something I do not recommend. You rarely will find a “Hot tipp” on this site.

German Startups Group Aktie = is basically an insider enrichment scheme with loosely bought secondaries from C-Level management – it is even worse than investing into a publicly listed VC/PE Holding vehicle (e.g. Rocket Internet), I would not go anywhere near it

Not sure if you actually read the underlying post. I would agree with your statement 1 or 2 years ago but my investment case is that things have changed and maybe not everyone has realized it 😉

Hello thank´s for that article. Reading the article and some reports of the company, I´m on your side redarding the undervaluation. Especially the company did verry well since you wrote the article. The realized price for Exozet was significant higher than you expected and the companies portfolio fits very well in the Corona-digitalization-hype we´re seeing in the valuations at the moment. So maybe they can make some more profitable exits in the next months at high price-levels.

They also further reduced their high interest debt, which makes a lot sense in my opinion.

Reading a few articles about auctions (mainly art) makes me think, that Auctiontech (biggest part of the portfolio) will benefit a lot from the developement of the last months, in total the portfolio looks like it could perform well in this cercumstances.

Thanks for sharing the portfilo and efforts behind the scenes.

Sorry, I am newbee on these and couldn’t find the clear meanings of „Perf. Incl. Div“ and „Holding period“ between commnent as well.

Performance including dividend – from which date is the calculation?

Holding period – Start and end datetime?

Hi MMI, a question regarding your stock INSTALLUX. Have you already checked the last half-year report of INSTALLUX? They booked “Actifs liés aux droits d’utilisation” to their balance sheet with an amount of 18.6 Mio. EUR. Do you know the reason? Thank you in advance

First of all, I love your blog! That said, I’ve got a question 🙂

Looking at your portfolio i’m wondering why you invest mostly in Europe. Don’t you see opportunities elsewhere in the world?

Your benchmark is also European. Your investment philosophy doesn’t explicitely exclude investments outside of Europe. Did you ever write a post about this choice or is it simply a ‘home bias’?

I invest elsewhere as well (Expedia, Cars. com etc.) but as I live in Europe and will spend all my money in Europe I think it is OK to use this as Benchmark. And yes, there is clearly some home bias at work. But if you read my blog you will see I tried for intsance Australia (Silver Chef) and learned some hard lessons investting far away…..

You wrote that you exited SilverChef in Sept. [memyselfandi007 14.Sep.2017 11h41] … but curiously it is still listed in your portfolio as of 31.12.2017… Is this a Phantom Invesmtent ? 😉

If you read the comments carefully you will recognize that on 14. Sep 2017 I said the following:

For the record: I sold the additional Silver Chef shares that I bought 2 weeks again. Why ? Well, I missed one specific issue when I looked at the numbers: Overdue receivables increased significantly, but provisoning against defaults did not increase in the same amount. Management seems to have explanations for this, but I am not 100% convinced.

I think its clear that I only sold the shares that I had baough ADDITIONALLY 2 weeks earlier.

Of course, sorry… 😉 SES is trading a low PE and PB ratio with a div yield of around 8%. They have a pretty nice EBITDA margin of >70% and a operating profit margin of about 44%. The market is growing at a steady pace and seems to have significant entrance barriers…

In my oppinion SES could be a value trap because of over-capacity in the satellite industry. It seems cheap, but gets cheaper and cheaper. It seems that there are too many satellites and that over time the cost of launching a new satellite (micro satellites) with greater and better functions is lower.

Hey, what do you think about the current price and takeover offer for the french company Tessi ? You’ve been talking about it few years back. I think it’s an interesting situation because its balance sheet looks solid.

Not that you’re looking for more investment ideas, but one that may be of interest is CBR (US). After decades of empire building they are engaging in a slow motion liquidation–to be determined whether it’s partial or total–and based on today’s SEC filings looks like they have received several offers which will at least let them pay off their debt, and may represent a mild bidding war for some of their assets (no way to know for sure until they settle on a transaction). Trades at very low (~normalized) multiples due to middling operations and self-inflicted wounds, and they will likely have another goodwill impairment after the test they initiated in Q4 2016. This will probably all play out in 1H17, and quite possibly in the next month or so.

I don’t see any liquidation value in CBR. Certainly not to Grahams standards. Their property consists of intellectual rights that obviously are worthless if they are ceasing operations. With only discounting their intangibles, the business is worth $0.30 per share as it stands. Currently they’re trading in excess of that. In any event, that’s for the information. It was worth looking into.

I think this depends on the individual style of investing. I guess you are not a regular reader. Because then you would know that I am rather a “7 Iron” investor and prefer to leave my Driver in the bag for the time being…..

Yes, there is a simple reason: I try to slow myself down with regard to transaction frequency. So I decided it is enough to update every quarter along my “quarterly report”

Have you had a look at Joy Global?

They are a manufacturer of mining equipment with a (until now) fairly strong balance sheet (cf. Caterpillar).

Clearly, they are hit extremely hard by the coal price drop.

Coal consumption goes down in the USA and is generally under pressure in developed countries because of concerns about CO2 emissions. The consumption in China has stalled but is still growing in India.

There is literally blood in the streets and BHP etc. are not lowering production.

I guess Joy Global will never see the old highs again, but even if the coal price stabilises on a fairly low level and they manage to survive this might be a good investment.

Do you think mining companies and related investments are not a good investment anyway (strange business model)?

No, never looked at it. I don’t know that much about mining companies. With regard to coal, I think that anything coal related could turn out to be a value trap. Natural gas in my opinion is more interesting as it is the cleaner form of energy. But again, I am not an expert.

Ich bin bei der HYPOPORT AG seit vielen Jahren dabei. Und dies, wie ich ohne Übertreibung sagen kann, sehr erfolgreich. Was hältst Du von diesem Wert, der in zwei Wochen in den SDAX aufgenommen werden wird und dessen fairen Wert ich aktuell konservativ auf 80 bis 120 EUR (also zwischen plus 0 und plus 50 % auf Stand heute) schätze.

dann erstmal herzlichen Glückwunsch. Die Tatsache dass eine Aktie stark gestiegen ist und in einen Index kommt spricht m.E. aber nicht unbedingt dafür dass es ein Value Investment ist. Ohne Hypoport zu kennen vermute ich mal, dass es eher was für einen anderen Investmentstil ist (Momentum etc.).

At current prices (9 €/share RWE) I think is worth to have a look at the German utilities.

It is obvious the political risk but precisely because of this they are showing an extreme deep discount vs. fair value.

Some of the valuation exercises using SOP show incredible discounts even taking into consideration further deterioration on the nuclear decommissioning provisions.

It reminds me kind of panic mood (much alike Goldman during the Lehman crisis)…

despite panic, I still don’t touch German utilities. As I have written extensively, there are so many problems that there is a large risk that they turn out as typicalvalue traps. You might trade them succesfully but long term the upside is very limited. If you are interested in th sector, “collateral dmages” like Verbund might be the better chance.

mmi

Thank you for your response.

I would love to read your points about the German utilities (any specific article that you recommend me)?. Remember that sometimes the value is found into the darkest pool of irrationality…:-). I will not argue about the quality of the management (that is obvious) but value stands ostensibly above price nowadays.

With EV/EBITDA at current 4.3xEV/EBITDA I will look into RWE…Moreover bond markets doesn’t seem to reflect the so feared increase of the nuclear provisions (I do attach bond vs. equity): https://pbs.twimg.com/media/CPl7GzbVEAAxaoi.png:large

Last but not least, at current prices provisions for nuclear would have to amount to 17 bn€ for RWE (currently 10,4 bn€) to justify its 10 €/share…when minister Gabriel recognizes that such a level of funding for dismantling is an irresponsible speculation exercise.

EV/EBITDA without adjustments is highly misleading. There is not only the nuclear issue but also a big ension problem and the fact that the core businessis svrewed up.

RWE is a badly run company in a bad sector. Clearly you can try to time a rebound, but midto long term German utilities do not have a lot of upside unless we get a surprise ice age within the next few years,..

mmi

p.s.: i am not sure how deep you are int German politics but Mr. Gabriel’s potential voters ar not really RWE or E.On shareholders…..

You are right. A normalized ratio would result in 7.6xEBITDA pretty much in line with the sector. A “facial” ratio would result in a misleading 4.3x

I was referring more to the special situation surrounding the stock (higher EPS by substituting provisions by debt, Constitutional Court ruling, capacity payments scheme in Europe, etc).

Politics are always a nightmare! Thank you, as usual, for your thoughts.

Take care.

The stock has dropped 25% over the last two months on no obvious company specific catalyst (Greece sentiment and hasn’t recovered with the rest of the market). As you know they won the mondadori case and as a result, they have a lot of cash and near cash items on their balance sheet.

Classic holdco – sum of theparts situation – very simple holdings – what is the appropriate discount ? right now think it is trading at >30% discount to NAV and cash and near cash items on their balance sheet at the holdco represent 50% of market cap. They are returning cash to shareholders primarily through a share buyback programme (tax advantages versus dividend). The programme lasts 18 months from April 2015 and they are buying 25% of daily volume (some Italian regulatory limitations on how much they can buy back per day linked to daily traded volume).

I think it is relatively low risk (given the nature of their balance sheet and margin of safety), 20% near term upside as the buyback programme takes out shareholders that want to get out and I think their opco performance will be reasonable and the assets on the balance sheet away from the two listed entities that are well covered (education group, NPL portfolio, hf/pe investments) have good track record and some upside.

What about Bilfinger? It seems to have all the prerequisites for joining the portfolio. New proven CEO, minimal debt, good business (with the sole exception of energy, where a turnaround -or sale- is needed).

It would be great to have your opinion on this stock.

Take care.

I have been following your website for a long time. Given that you are German, maybe you can help me.

I found a cheap share with low liquidity, trading on the Frankfurt market, although I have never bought any shares on this market, usually I buy on the Xetra market.

Can you tell me Why some stocks are on this stock market (Frankfurt) instead of Xetra, and if there are any disadvantages to trade on the Frankfurt market instead of Xetra?

To my knowledge, super-iiliquid stocks like Creaton are not found on Xetra, maybe it is too much effort. Overall I don’t think it is a disadvantage. The “normal exchange” for instance is open antil 8 pm, Xetra closes at 5:30 pm.

I think that German companies can delist from stock exchange without a “fare” compensation/price.

Don’t you think this is a problem for super-illiquid stocks?

Yes, that’s correct. I have covered this topic frequently and this is one of the reasons why I don’t own more German small caps. But this is not related to Xetra.

A newcomer to your site. Interested in your portfolio allocation to Tonnellerie Francois Freres. I know the business (as a wine importer not an investor). How long have you held the stock? What is its beta?

It is the market leader in its sector in Burgundy, its home patch. Strong elsewhere but of course facing price competition from other big outfits such as Seguin-Moreau, a Bordeaux firm.

I note that the Francois Freres T/O splits two thirds wine barrels, one third barrels for spirits. I know the wine end, not the spirits sector. I’d say that many non-French wine producers specializing in Pinot Noir and Chardonnay will probably want the Burgundy connection and gravitate towards this supplier. So I think the demand will stay strong (China coming onstream as a major wine producer).

Our experience in Burgundy is that coopers (the normal word for barrel makers) can dictate prices. Customers end up accepting price rises. Some customers look East for cheaper oak forests but the firm has that covered with its Hungarian operation.

All in all, a solid-looking sector and a well-run family firm. Probably quite prudent regarding debt. I’m not sure that growth will be rapid from here forward as the dynamics of the industry are quite stodgy. (Two or three years to dry oak before it is ready for use!)

I see the stock is up at 76 Eur. OK but not a bargain. I’m looking to deploy a small amount of UK cash to take advantage of the exchange rate and buy somthing in euroland. Was looking more at Germany – especially at Siemens – and really enjoyed your piece on the Dax and returns since 1992.

thanks for your insights. For TFF, I think there is always the chance that they could consolidate further like they did With Radoux. But of course this is not guaranteed.

Siemens: this is one of the German stocks I would not want to own long term….It might look relatively cheap but it is so spectacularily badly run that it is almost comical.

Thanks for the health warning on Siemens. Not really a serious interest on my part. But I would want to apply the ‘chowder rule’ whatever the stock. Namely, impressive safety (balance sheet fortress) and 5 year CAGR + current dividend yield > 12.

Nestle is one of my core holdings. Regarding Germany I’d really like to find a boring, hard-working mid cap still with a strong family presence but many of these are private companies, unlike in UK/US.

Regarding the French cooper there is great scope for consolidation inside that sector in Burgundy but few businesses of enough size to make a material difference to performance. Perhaps it will be the other way round. Foreign firm acquiring Francois Freres? How much stock is controlled by the family?

regarding TFF: 70% of the shares are owned by the family, so very little chance for a take over ….

German hard-working mid caps: Sorry to say but I guess you are 3 years too late for that idea. All that is left are struggling companies unless. If you want a well run German mid cap, be prepared to pay 30x P/E or more.

Sorry to bring a weird question but did you have the chance to have a look to mining co. such as Vale, BHP, Arcelor or Rio Tinto? It is a long shot but it seems that a bounce back is about to happen and according to historical levels it should be a significant one.

I do respect your opinion, so I’d like to know if you had a thought on this. Thank you as usual. Take care.

Dear Dave,

unfortunately, I have never looked at mining companies. They looked cheap for some time but i generally do not understand their business model fully. At the moment I am trying to get a grip on oil companies which is pretty hard. In general they are very cyclical and the cycles seem to be long and deep…..

Beim ersten Angebot kann ich mir nicht vorstellen, dass ich einen Ergänzungsanspruch aus einem nicht verbrieften Genussschein haben kann. Das ist bei mir der Fall, denn ich habe Genussscheine im Laufe der Zeit verkauft.

Beim zweiten Angebot stört mich die Sperrfrist, die auch nur von der Deutschen Balaton aufgehoben werden kann und von mir gewährt werden muss.

Allgemein kann ich nicht beurteilen, ob das Gericht evtl. Nachbesserungen aus den Klagen der Balaton oder Sparta auch den nicht klagenden Genussscheininhabern zusprechen könnte.

Ich habe es mir ehrlich gesagt nicht genau angeschaut. Damals war ich der Meinung dass die Entschädigung ökonomisch OK war. Ich glaube ich spare mir den Stress.

Bei den sehr niedrigen Bewertungen könnte man m.E. bei SBERBANK einen spekulativen Einstieg schon erwägen. Grund: Verschärft sich die Ukraine-Krise erheblich, dann haben wir wahrscheinlich ein ganz anderes Problem an den Aktienmärkten bis zu einer “Kernschmelze” wie 03/2003 bei stark steigenden Goldpreisen. Verbessert sich die Situation, dann dürften die Kurse schneller steigen als an allen Märkten. Die Frage ist ja nicht nur ob das ein gutes Investment wäre, sondern ein besseres.

Sberbank verdient jetzt erst einmal u.a. wegen des fallenden Rubel weniger. Die Rückstellungen sind gestiegen. Anscheinend haben sie auch ukrainische Schuldner. Das fundamentale Russlandgeschäft wächst aber. Ich habe zu aktuellen Kursen eine erste Position aufgebaut, jedoch auch nur 1%. Wenn die russische Wirtschaft sich schlecht entwickelt, kommt es zu mehr Insolvenzen und Sberbank wird getroffen, auch ohne direkte Sanktionen gegen russische Banken, welche noch drastischer wären.

I just would like to had that I asked for an opinion at http://www.oddballstocks.com/ (a website that I follow appreciate too), and I had feedback too.

I am a value investor and I have been following your blog.

I would like to congratulate you for your analysis they have been very helpful

I invested in a company that semms to be bargain, although I would like to have your opinion.

AUSTRALIAN VINTAGE LTD (AVG)

The company produces and exports bulk and bottled wine, and is the second largest vineyard owner and manager in Australia

P/E forward: 6;

p/B: 30% (a net-net stock);

Although the margins, ROE, RIC are very low and the demand for wine has been decresing in important markets, like china.

I made the investment considering the amasing multiples (p/b, p/e) but the margins are not a great indicator.

Can you give me your opinion?

Danke für die Einschätzung zu den Genussscheinen der Drägerwerke. Wissen Sie, ob ein Zwangstausch in 10 Vorzugsaktien einen Verkauf mit Abgeltungssteuer darstellen würde. Denn dann müsste man wohl noch einen Abschlag für die Steuer berücksichtigen.

Vielen Dank für Ihren Blog. Super Arbeit, danke für die guten Ideen.

Im Feb. 2011 hatte Sie einen fairen Wert für die Drägerwerk Genussscheine in Höhe von 145-180 Euro berechnet. Wie sehen Sie die Situation heute? Welchen Wert erachten Sie heute als fair?

Hi,

“Perf. Incl. Div” is the same as annualized rate of return, including dividends?

I have the same doubt as John. The above table is not clear about your performance as a whole. It seams you are hiding your performance …

I was going to ask the same question. Found your results. The results are good – why don’t you make them front and center?

I really love all the great information you post and the amazing debates after your articles. As an amateur value investor having access to this kind of information is invaluable.

danke für den Kommentar. Gazprom ist mir persönlich zu komplex. Ich kann so ein Unternehmen nicht beurteilen, zudem fehlt mir das Vertrauen in Eigentumsrechte bei Russischen Aktien. Von daher habe ich hier keine Meinung.

Vielen Dank für die rasche Rückmeldung. Finden sie generell, dass sich Value Investing und Emerging Markets aufgrund der von Ihnen angesprochenen Unsicherheiten ausschließen?

Generell ausschliessen möcht ich eigentlich nichts, aber ich finde es in der Tat schwierig direkt in EM Aktien zu investieren. Viel besser finde ich es über eine etablierte Firma indirekt zu investieren. AS Creation mit Ihrem Russland JV ist da ein gutes Beispiel.

Sehr interessant, weiter so. Auch tolle idee wegen der Genusscheine.

Bzgl OMV wenn schon ein österreichisches Big-Cap, dann hätte ich eher die Österr. Post dazu gegeben, die Branche wird (wurde?) zwar vom Internet abgelöst, wird meiner Meinung nach aber unterbewertet. Der Trend wird etwas übertrieben vom Markt, pakete gibts weiterhin + ich geh die wette ein, dass schon längst fast nur solche affairen über post geschrieben werden, die auch großteils bleiben werden.

Post “Liefert” weiterhin gute Resultate ab und zahlt eine hohe, wachsende Dividende (c.a. 6.6%) zugegeben bei hoher ausschüttung (c.a. 75% vom Cashflow). Sehr gutes Management.

Btw, wegen allen diesen Stocks, Ist hier jemand Österreicher (bin selbst auch schuldig 😀 )?

Ösi Post kommt in meinem Modell nicht ganz so gut weg. Kostet 3 fach Buch und produziert gerade mal die Kapitalkosten. Das ist in “meiner Welt” eine klare Überbewertung.

Ist für ein Value Investor wie Sie die DNick Holding interessant. Die Gesellschaft soll “delisted” werden und das stellt sich sehr nachteilig für die Kleinaktionäre dar. Ich denke jedoch, dass man bei einem Börsenwert von ca. 43 Mio. Euro in Zukunft mindestens 20 Mio. Euro Cash als nicht betriebsnotwendiges Kapital ausschütten kann und das bei einem möglichen bereinigten JÜ in Höhe von 3,6 Mio. Euro (konservativ geschätzt). Leider kann ich die gerichtlichen Chancen gegen das Delisting nicht einschätzen. Haben Sie eine Meinung.

Dafür wird die TUI endlich den Frenzel los – das ist sicherlich zuträglich zum Unternehmenswert… Unglaublich einer der größten Geldvernichter-Manager die es in Deutschland gibt!

Was halten Sie von einem Short auf TUI. Die Gesamtergebnisrechnung zeigt einen Verlust von ca. 900 Mio. Euro per Q3. Die TUI AG hat noch Finanzschulden von über 2 Mrd. Euro. und keinen Zugriff auf den Cash der überwiegend in der 53 % Beteiligung der TUI Travel liegt. Auch die Ergebnissituation der TUI Travel ist sehr schlecht. Mit dem Abgang von Herrn Frenzel könnte sich die Refinanzierung als sehr schwierig erweisen. Da der Nachfolger ein Branchenfremder ist und sicherlich bei Vodafone keine schwierigen Unternehmensfinanzierungen zu stemmen hatte.

Glückwunsch zu Deinem Short bei Green Mountain !

Ich glaube der David Einhorn liest bei Dir heimlich mit und hat die Short Idee von Dir. Ich würde bei Ihm anrufen und nach einer Provision verlangen 🙂

a) werde ich versuchen

b) habe ich gemacht, wäre aber wohl auch sinnvoll in die Page einzufügen

c) ja, mein eigenes Portfolio sieht (abgesehen von der Größe) recht ähnlich aus.

Sehr gute Arbeit. Danke für die vielen Informationen und Einblicke!

Anmerkungen/Fragen:

a) Häufigere Aktualisierung wäre wünschenswert.

b) Gesamt-Performance-Messung wäre wünschenswert

c) Ist das ein Testportfolio oder gibt es das Portfolio wirklich?

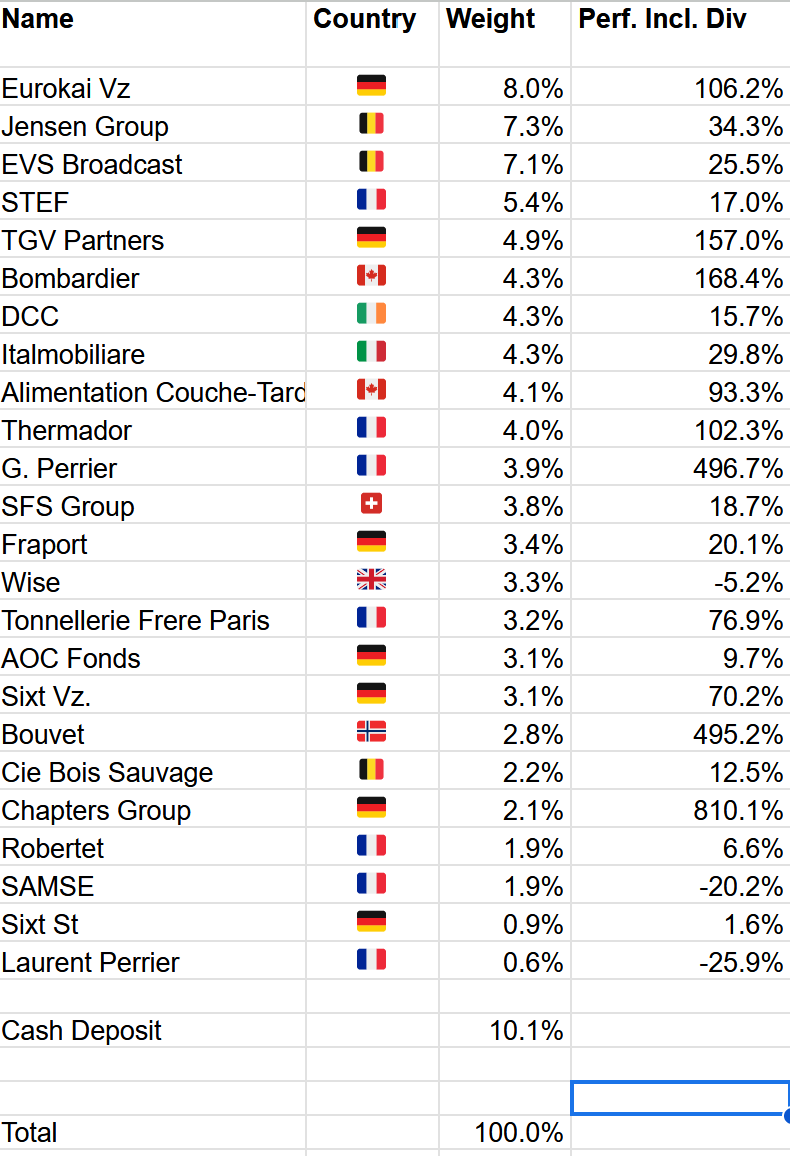

FYI I noticed some overlap between your portfolio and the one of Belgian holding company Quest for Growth:

Jensen Group 7,8% vs 5,9%

EVS 7,1% vs 5,3%

Thermador 4,0% vs 1,8%

Robertet 1,8% vs 2,9%

Quest for Growth trades at a 40+% discount to NAV, partly due to its significant PE exposure.

https://capricorn.be/en/channels/quest-for-growth/monthly-portfolio-overview

Thank you. If I remember correctly i Have seen Jensen in ne of Capricorn’s funds before I started to look deeper.

They now seem to want to focus on… VC

https://capricorn.be/en/channels/quest-for-growth/news_items/qfg-strategic-change-of-course-and-capital-reduction

That’s not good…

Wow, on TFF you roundtripped from a 5-bagger back to a doubler?

Since 1.1.2011 the Total Return is +181% or 7,3% p.a. Not great but also not a total Desaster either. Until year end 2023, the numbers were +650% and 16,8% p.a.

Hi, really good blog and interesting insights, is there any reason you only invest in Europe?

Hi! As Profitlich/Schmidlin is in your “peer group”: Did you ever have a closer look at Laboratorios Rovi (for a detailed description of their business model see PS’ latest quaterly report: https://profitlich-schmidlin.de/wp-content/uploads/2023/10/ProfitlichSchmidlin-Fonds-Q39-Bericht.pdf)? Briefly checked their numbers on TIKR, looks like a GARP candidate… Regards Mathias

nabeltec will have a difficult second year after a good first and a bad second quarter

if the market cap goes down another 40 million it will get interesting 🙂

seems their products aren’t really taking off in europe and they have no access to china

Nabaltec: You mentioned that the energy prices in Germany are a concern. My understanding from the annual report is that they get their steam heat from a adjacent waste disposal plant. They also mention that their energy cost is locked in until end 2024. Given the steam heat supply from the waste disposal plant, wouldn’t energy pricing be less of a concern here ? (Unless the price they pay for the steam is somehow linked to natural gas prices in Germany)

Was ist dein Szenario bei Biontech? Würdest du diese aktuell sogar aufstocken?

Nein, das ist erstmal eine “Erinnerungsposition” die ich laufen lasse.

What is the difference between “weight” and “percentage” collumn?

Just the title.

I propose another one with the title “share” and of course the same numbers again.

as always, sincere thanks for the update and the constant research! I also see that it goes on again pleasantly at TGV. I assume, that they also have sold Naked Wines in the meantime. Such a pity about this originally promising business model in the wine business.

It would be great if you kept a monthly update:)

Sorry, quarterly it is.. .

Looking forward to this quarter then 😉

Onvista hat mich informiert, dass Admiral die Dividende zum Teil als Barzahlung und zum Teil als Wertpapierzahlung (optional) ermöglicht.

Kannst du aus der Erfahrung einschätzen, ob sich die Dividende in Wertpapierform lohnen wird oder muss man dazu zunächst den Reinvestierungskurs, der von Admiral festgelegt wird, abwarten.

VG!

Hallo, habe nie reinvestiert, weiss auch nicht wie das mit der Vergeltungssteuer funktioniert.

Thanks for your blog and the insights. I wonder why you did sell Aker Horizons given the steep discount compared to the price when you initially mentioned the position in your Energie Transition Basket. Did your assumptions change in this regard?

I honestly got confused by all the reorgs they made. Need to look at them again. I also wanted to realize some losses from a tax perspective.

What are your thoughts on Admiral? I had been waiting at the sideline before the current slump which from My search is mainly down to a “peer” reporting slow momentum. Fun it hard to identify any fundamental problems…

Hey, i have a question regarding conviction vs. portfolio weight. Some of your positions which you see as long term holds (e.g. ACT, VEF) have substantially lower weights than some of your mere “hold” positions (e.g. TFF, Naked Wines). Why is that? Regards Mathias

In hte specific case, ACT and VEF would be positions where I would still add to the position.

Overall, I found out that my conviction and subsequent performance do not correlate that well 😉

Was ist denn mit Admiral heute passiert?

Dividendenabschlag ähhh nein, doch nicht. Einigen anlegern hat wohl der Ausblick nicht gefallen (2022 wird schlechter als 2021 und 2020)..

Inflation führt immer zu einem gewissen Zyklus insbes. in der Autoversicherung, Scheinen aber viele vergessen zu haben.

When did you sell Just Eat ?

According to my blog I started selling in June

and was done by the end of the quarter

Avg selling price ~75 EUR vs 91 EUR purchase price.

How do you look at VEF AB since the last investment round of Creditas. It seems like Q3 was 4.5 NAV and 5.6 share price. and now more 4.6 share price and NAV around 5.6.

Not much different. I am in there for the long term.

Hi MMI,

a question regarding Bouvet. Although a consolidation is not that surprising after this long lasting surge, the modest development compared to the market trend recently is striking. Do you ascribe this trend to particular news (change in CFO)? If there are no structural concerns the stock seems not that expensive at a leading P/E of 24, given the intact growth and the good margins…

Mathias

Hi,

do be honest, I try not to speculate on why a stock is doing what it does. Fundamentally, I will keep Bouvet as long as things are looking Ok, which they do.

mmi

Moin, vielen Dank für diese Seite. Was halten Sie von Silvano Fashion Group (Estland) und Grigeo (Litauen)? Erstere haben Probleme mit Wechselkursverlusten (Russland), letztere mit einem Abwasserskandal. Aber mit Blick auf den Free Cash Flow und das Geschäftsmodell an sich halte ich beide für deutlich unterbewertet.

Ihre Kommentare/Portfolio sind extrem fundiert – ich freue mich, wenn Sie Ihre Einschätzung teilen. Vielen Dank.

Hallo,

ich kenne beide Unternehmen nicht. Warum sollte ich mir das näher anschauen ?

MMI

Naja, beide haben verständliches Geschäftsmodell und seit Jahren starken FCF, aber KGV 6. Ich dachte, Sie suchen auch nach solchen Wert…wenn nicht von Interesse, sorry, will Sie nicht langweilen.

Nun ja, ich hatte erhofft Sie erklären mir kurz das Geschäftsmodell oder hängen zumindest einen Link an. Sonst muss ich mir das erst mühsam raussuchen. Meine “to do” liste ist über 100 Unternehmen lang, dann muss ich effizient sein.

Hello, thanks for your homepage. It is very nice.

Are all the stocks in your portfolio stocks that you are still recommending or which ones or how do we know?

Thanks and regards,.

Hi,

the stocks that are in my portfolio are the stocks that I hold in my personal account. Some of them are there, for now, more than 10 years. Once a year I do short summaries of my positions, the posts are called “My xx stocks for 20xx”. You might want to look at the last one to see which positions I am very comfortable with and which positions are shakier.

In general, I do not recommend any shares as I do not provide investment advice. Please consider what I write as my personal diary. of a long-term investment journey. So just looking at the portfolio page without reading the corresponding posts is something I do not recommend. You rarely will find a “Hot tipp” on this site.

Hope that helps,

MMI

German Startups Group Aktie = is basically an insider enrichment scheme with loosely bought secondaries from C-Level management – it is even worse than investing into a publicly listed VC/PE Holding vehicle (e.g. Rocket Internet), I would not go anywhere near it

Not sure if you actually read the underlying post. I would agree with your statement 1 or 2 years ago but my investment case is that things have changed and maybe not everyone has realized it 😉

We will see if I am right or wrong …..

Management Geschäftsführer – Christoph Gerlinger = what changed here?

or are you referring simply to the market cap of it’s listed assets aka there stake in DH?

Maybe you want to read the post ? IT’s all there and I don’t want to write it twice.

Edit: In case you have troubles with the search function, here is the link:

Hello thank´s for that article. Reading the article and some reports of the company, I´m on your side redarding the undervaluation. Especially the company did verry well since you wrote the article. The realized price for Exozet was significant higher than you expected and the companies portfolio fits very well in the Corona-digitalization-hype we´re seeing in the valuations at the moment. So maybe they can make some more profitable exits in the next months at high price-levels.

They also further reduced their high interest debt, which makes a lot sense in my opinion.

Reading a few articles about auctions (mainly art) makes me think, that Auctiontech (biggest part of the portfolio) will benefit a lot from the developement of the last months, in total the portfolio looks like it could perform well in this cercumstances.

Hi,

Thanks for sharing the portfilo and efforts behind the scenes.

Sorry, I am newbee on these and couldn’t find the clear meanings of „Perf. Incl. Div“ and „Holding period“ between commnent as well.

Performance including dividend – from which date is the calculation?

Holding period – Start and end datetime?

Thansk in advance.

Many thanks for the update

I’ve been following your blog silently for years, nice to see other investors describing their thought processes! Keep up the great work!

Hi MMI, a question regarding your stock INSTALLUX. Have you already checked the last half-year report of INSTALLUX? They booked “Actifs liés aux droits d’utilisation” to their balance sheet with an amount of 18.6 Mio. EUR. Do you know the reason? Thank you in advance

simple = IFRS 16

First of all, I love your blog! That said, I’ve got a question 🙂

Looking at your portfolio i’m wondering why you invest mostly in Europe. Don’t you see opportunities elsewhere in the world?

Your benchmark is also European. Your investment philosophy doesn’t explicitely exclude investments outside of Europe. Did you ever write a post about this choice or is it simply a ‘home bias’?

I invest elsewhere as well (Expedia, Cars. com etc.) but as I live in Europe and will spend all my money in Europe I think it is OK to use this as Benchmark. And yes, there is clearly some home bias at work. But if you read my blog you will see I tried for intsance Australia (Silver Chef) and learned some hard lessons investting far away…..

What do you think about Mayfield Childcare Limited (MFD.AX)

PE 7

Forward Dividend & Yield 8.97%

I haven’t looked at the stock. PE and Dividend yiled however indicate that there might be some problems….

You wrote that you exited SilverChef in Sept. [memyselfandi007 14.Sep.2017 11h41] … but curiously it is still listed in your portfolio as of 31.12.2017… Is this a Phantom Invesmtent ? 😉

If you read the comments carefully you will recognize that on 14. Sep 2017 I said the following:

For the record: I sold the additional Silver Chef shares that I bought 2 weeks again. Why ? Well, I missed one specific issue when I looked at the numbers: Overdue receivables increased significantly, but provisoning against defaults did not increase in the same amount. Management seems to have explanations for this, but I am not 100% convinced.

I think its clear that I only sold the shares that I had baough ADDITIONALLY 2 weeks earlier.

Hey, did you ever had a look on SES Global? A leading satellite operator from luxembourg… would like to hear about your first view/ impression.

No I did not look at it. Why should I ? Can you give me your first view/impressions first ?

Of course, sorry… 😉 SES is trading a low PE and PB ratio with a div yield of around 8%. They have a pretty nice EBITDA margin of >70% and a operating profit margin of about 44%. The market is growing at a steady pace and seems to have significant entrance barriers…

In my oppinion SES could be a value trap because of over-capacity in the satellite industry. It seems cheap, but gets cheaper and cheaper. It seems that there are too many satellites and that over time the cost of launching a new satellite (micro satellites) with greater and better functions is lower.

Hey, did you ever had a look on SES Global? A leading satellite operator from luxembourg…

Hi, How often do you reconsider on your current portfolio?

I was wondering if you’d consider Deutsche Pfand still being a buy or hold position.

Best

C

by coincidence there will be a post soon on this. It is a “sell” for me due to risk management reasons

Hey, what do you think about the current price and takeover offer for the french company Tessi ? You’ve been talking about it few years back. I think it’s an interesting situation because its balance sheet looks solid.

sorry, I have no qualified opinion on this. I never fully understood what they are doing.

Not that you’re looking for more investment ideas, but one that may be of interest is CBR (US). After decades of empire building they are engaging in a slow motion liquidation–to be determined whether it’s partial or total–and based on today’s SEC filings looks like they have received several offers which will at least let them pay off their debt, and may represent a mild bidding war for some of their assets (no way to know for sure until they settle on a transaction). Trades at very low (~normalized) multiples due to middling operations and self-inflicted wounds, and they will likely have another goodwill impairment after the test they initiated in Q4 2016. This will probably all play out in 1H17, and quite possibly in the next month or so.

I don’t see any liquidation value in CBR. Certainly not to Grahams standards. Their property consists of intellectual rights that obviously are worthless if they are ceasing operations. With only discounting their intangibles, the business is worth $0.30 per share as it stands. Currently they’re trading in excess of that. In any event, that’s for the information. It was worth looking into.

Fair point–no margin of safety for sure!

What tool do you use to track your paper portfolio return & performance statistics?

Excel spreadsheet

May I enquire which broker/ brokers you use? Great website, thanks for putting it out there!

I use consors. I also had a DAb account, but the 2 were merged. I am not sure if I will open one at another bank.

Much too diversified of a portfolio.

I think this depends on the individual style of investing. I guess you are not a regular reader. Because then you would know that I am rather a “7 Iron” investor and prefer to leave my Driver in the bag for the time being…..

Hello

I soule like to have your opinion on Cheniere (LNG). Already analyzed?

yes, just search the blog.

You have not to be updated the list for a while. How often do you intend to do so?

This is not updated for a while. Is there a reason, why you don’t update more often?

Yes, there is a simple reason: I try to slow myself down with regard to transaction frequency. So I decided it is enough to update every quarter along my “quarterly report”

Have you had a look at Joy Global?

They are a manufacturer of mining equipment with a (until now) fairly strong balance sheet (cf. Caterpillar).

Clearly, they are hit extremely hard by the coal price drop.

Coal consumption goes down in the USA and is generally under pressure in developed countries because of concerns about CO2 emissions. The consumption in China has stalled but is still growing in India.

There is literally blood in the streets and BHP etc. are not lowering production.

I guess Joy Global will never see the old highs again, but even if the coal price stabilises on a fairly low level and they manage to survive this might be a good investment.

Do you think mining companies and related investments are not a good investment anyway (strange business model)?

No, never looked at it. I don’t know that much about mining companies. With regard to coal, I think that anything coal related could turn out to be a value trap. Natural gas in my opinion is more interesting as it is the cleaner form of energy. But again, I am not an expert.

Just looked at it – I find Danieli cheaper and more robust

Ich bin bei der HYPOPORT AG seit vielen Jahren dabei. Und dies, wie ich ohne Übertreibung sagen kann, sehr erfolgreich. Was hältst Du von diesem Wert, der in zwei Wochen in den SDAX aufgenommen werden wird und dessen fairen Wert ich aktuell konservativ auf 80 bis 120 EUR (also zwischen plus 0 und plus 50 % auf Stand heute) schätze.

dann erstmal herzlichen Glückwunsch. Die Tatsache dass eine Aktie stark gestiegen ist und in einen Index kommt spricht m.E. aber nicht unbedingt dafür dass es ein Value Investment ist. Ohne Hypoport zu kennen vermute ich mal, dass es eher was für einen anderen Investmentstil ist (Momentum etc.).

Hey,

what do you think about PLATFORM SPECIALTY PROD.CORP

US72766Q1058

Biggest Investors Bill Ackman, Nicolas Berggruen, Permira, Cevian…

hmm, looks like a “Hedge Fund hotel on fire”. I have no idea about that stock to be honest.

At current prices (9 €/share RWE) I think is worth to have a look at the German utilities.

It is obvious the political risk but precisely because of this they are showing an extreme deep discount vs. fair value.

Some of the valuation exercises using SOP show incredible discounts even taking into consideration further deterioration on the nuclear decommissioning provisions.

It reminds me kind of panic mood (much alike Goldman during the Lehman crisis)…

hi Dave,

despite panic, I still don’t touch German utilities. As I have written extensively, there are so many problems that there is a large risk that they turn out as typicalvalue traps. You might trade them succesfully but long term the upside is very limited. If you are interested in th sector, “collateral dmages” like Verbund might be the better chance.

mmi

Thank you for your response.

I would love to read your points about the German utilities (any specific article that you recommend me)?. Remember that sometimes the value is found into the darkest pool of irrationality…:-). I will not argue about the quality of the management (that is obvious) but value stands ostensibly above price nowadays.

With EV/EBITDA at current 4.3xEV/EBITDA I will look into RWE…Moreover bond markets doesn’t seem to reflect the so feared increase of the nuclear provisions (I do attach bond vs. equity):

https://pbs.twimg.com/media/CPl7GzbVEAAxaoi.png:large

Last but not least, at current prices provisions for nuclear would have to amount to 17 bn€ for RWE (currently 10,4 bn€) to justify its 10 €/share…when minister Gabriel recognizes that such a level of funding for dismantling is an irresponsible speculation exercise.

Best,

Dave,

EV/EBITDA without adjustments is highly misleading. There is not only the nuclear issue but also a big ension problem and the fact that the core businessis svrewed up.

RWE is a badly run company in a bad sector. Clearly you can try to time a rebound, but midto long term German utilities do not have a lot of upside unless we get a surprise ice age within the next few years,..

mmi

p.s.: i am not sure how deep you are int German politics but Mr. Gabriel’s potential voters ar not really RWE or E.On shareholders…..

You are right. A normalized ratio would result in 7.6xEBITDA pretty much in line with the sector. A “facial” ratio would result in a misleading 4.3x

I was referring more to the special situation surrounding the stock (higher EPS by substituting provisions by debt, Constitutional Court ruling, capacity payments scheme in Europe, etc).

Politics are always a nightmare! Thank you, as usual, for your thoughts.

Take care.

Hallo, schon mal daran gedacht das portfolio bei Wikifolio einzurichten ?

Nein, ein Großteil der Werte wäre ohnehin nicht handelbar.

have you looked at cir spa recently – looks to be getting very interesting again

why is it getting interesting ?

The stock has dropped 25% over the last two months on no obvious company specific catalyst (Greece sentiment and hasn’t recovered with the rest of the market). As you know they won the mondadori case and as a result, they have a lot of cash and near cash items on their balance sheet.

Classic holdco – sum of theparts situation – very simple holdings – what is the appropriate discount ? right now think it is trading at >30% discount to NAV and cash and near cash items on their balance sheet at the holdco represent 50% of market cap. They are returning cash to shareholders primarily through a share buyback programme (tax advantages versus dividend). The programme lasts 18 months from April 2015 and they are buying 25% of daily volume (some Italian regulatory limitations on how much they can buy back per day linked to daily traded volume).

I think it is relatively low risk (given the nature of their balance sheet and margin of safety), 20% near term upside as the buyback programme takes out shareholders that want to get out and I think their opco performance will be reasonable and the assets on the balance sheet away from the two listed entities that are well covered (education group, NPL portfolio, hf/pe investments) have good track record and some upside.

What about Bilfinger? It seems to have all the prerequisites for joining the portfolio. New proven CEO, minimal debt, good business (with the sole exception of energy, where a turnaround -or sale- is needed).

It would be great to have your opinion on this stock.

Take care.

Dave, yes I will look at them again, unfortunately i do have other stuff in the pipeline before….

I have been following your website for a long time. Given that you are German, maybe you can help me.

I found a cheap share with low liquidity, trading on the Frankfurt market, although I have never bought any shares on this market, usually I buy on the Xetra market.

Can you tell me Why some stocks are on this stock market (Frankfurt) instead of Xetra, and if there are any disadvantages to trade on the Frankfurt market instead of Xetra?

it would be easier to answer the question if you would name the share…..

Creaton AG

Xetra at the end of the day is only a trading system, see this explanation:

http://www.boerse-frankfurt.de/de/wissen/marktplaetze/der+elektronische+boersenplatz+xetra

To my knowledge, super-iiliquid stocks like Creaton are not found on Xetra, maybe it is too much effort. Overall I don’t think it is a disadvantage. The “normal exchange” for instance is open antil 8 pm, Xetra closes at 5:30 pm.

mmi

I think that German companies can delist from stock exchange without a “fare” compensation/price.

Don’t you think this is a problem for super-illiquid stocks?

Yes, that’s correct. I have covered this topic frequently and this is one of the reasons why I don’t own more German small caps. But this is not related to Xetra.

A newcomer to your site. Interested in your portfolio allocation to Tonnellerie Francois Freres. I know the business (as a wine importer not an investor). How long have you held the stock? What is its beta?

Hello and welcome !!! I hodl the stock in the blog portfolio since the beginning (1.1.2011), privately a little bit longer.

May I ask for your view on the business & the company ?

It is the market leader in its sector in Burgundy, its home patch. Strong elsewhere but of course facing price competition from other big outfits such as Seguin-Moreau, a Bordeaux firm.

I note that the Francois Freres T/O splits two thirds wine barrels, one third barrels for spirits. I know the wine end, not the spirits sector. I’d say that many non-French wine producers specializing in Pinot Noir and Chardonnay will probably want the Burgundy connection and gravitate towards this supplier. So I think the demand will stay strong (China coming onstream as a major wine producer).

Our experience in Burgundy is that coopers (the normal word for barrel makers) can dictate prices. Customers end up accepting price rises. Some customers look East for cheaper oak forests but the firm has that covered with its Hungarian operation.

All in all, a solid-looking sector and a well-run family firm. Probably quite prudent regarding debt. I’m not sure that growth will be rapid from here forward as the dynamics of the industry are quite stodgy. (Two or three years to dry oak before it is ready for use!)

I see the stock is up at 76 Eur. OK but not a bargain. I’m looking to deploy a small amount of UK cash to take advantage of the exchange rate and buy somthing in euroland. Was looking more at Germany – especially at Siemens – and really enjoyed your piece on the Dax and returns since 1992.

thanks for your insights. For TFF, I think there is always the chance that they could consolidate further like they did With Radoux. But of course this is not guaranteed.

Siemens: this is one of the German stocks I would not want to own long term….It might look relatively cheap but it is so spectacularily badly run that it is almost comical.

Thanks for the health warning on Siemens. Not really a serious interest on my part. But I would want to apply the ‘chowder rule’ whatever the stock. Namely, impressive safety (balance sheet fortress) and 5 year CAGR + current dividend yield > 12.

Nestle is one of my core holdings. Regarding Germany I’d really like to find a boring, hard-working mid cap still with a strong family presence but many of these are private companies, unlike in UK/US.

Regarding the French cooper there is great scope for consolidation inside that sector in Burgundy but few businesses of enough size to make a material difference to performance. Perhaps it will be the other way round. Foreign firm acquiring Francois Freres? How much stock is controlled by the family?

#swissfranc,

regarding TFF: 70% of the shares are owned by the family, so very little chance for a take over ….

German hard-working mid caps: Sorry to say but I guess you are 3 years too late for that idea. All that is left are struggling companies unless. If you want a well run German mid cap, be prepared to pay 30x P/E or more.

mmi

Sorry to bring a weird question but did you have the chance to have a look to mining co. such as Vale, BHP, Arcelor or Rio Tinto? It is a long shot but it seems that a bounce back is about to happen and according to historical levels it should be a significant one.

I do respect your opinion, so I’d like to know if you had a thought on this. Thank you as usual. Take care.

Dear Dave,

unfortunately, I have never looked at mining companies. They looked cheap for some time but i generally do not understand their business model fully. At the moment I am trying to get a grip on oil companies which is pretty hard. In general they are very cyclical and the cycles seem to be long and deep…..

mmi

Beim ersten Angebot kann ich mir nicht vorstellen, dass ich einen Ergänzungsanspruch aus einem nicht verbrieften Genussschein haben kann. Das ist bei mir der Fall, denn ich habe Genussscheine im Laufe der Zeit verkauft.

Beim zweiten Angebot stört mich die Sperrfrist, die auch nur von der Deutschen Balaton aufgehoben werden kann und von mir gewährt werden muss.

Allgemein kann ich nicht beurteilen, ob das Gericht evtl. Nachbesserungen aus den Klagen der Balaton oder Sparta auch den nicht klagenden Genussscheininhabern zusprechen könnte.

Ich habe es mir ehrlich gesagt nicht genau angeschaut. Damals war ich der Meinung dass die Entschädigung ökonomisch OK war. Ich glaube ich spare mir den Stress.

Ich wäre Ihnen sehr dankbar für die Info, ob Sie die Angebote der Deutschen Balaton annehmen werden.

Starten wir mal so: Was Ist Ihre/Deine Meinung ?

Nehmen Sie das Angebot der Deutschen Balaton zum Erwerb der Ausgleichansprüche für Ihre Genussscheine der Firma Dräger an? Siehe Link:

http://www.deutsche-balaton.de/draeger-dezember-2014.html

Sollte man bei Sistema und Sberbank jetzt kaufen?

Wenn ich ehrlich bin: Keine Ahnung.

Bei den sehr niedrigen Bewertungen könnte man m.E. bei SBERBANK einen spekulativen Einstieg schon erwägen. Grund: Verschärft sich die Ukraine-Krise erheblich, dann haben wir wahrscheinlich ein ganz anderes Problem an den Aktienmärkten bis zu einer “Kernschmelze” wie 03/2003 bei stark steigenden Goldpreisen. Verbessert sich die Situation, dann dürften die Kurse schneller steigen als an allen Märkten. Die Frage ist ja nicht nur ob das ein gutes Investment wäre, sondern ein besseres.

Sberbank verdient jetzt erst einmal u.a. wegen des fallenden Rubel weniger. Die Rückstellungen sind gestiegen. Anscheinend haben sie auch ukrainische Schuldner. Das fundamentale Russlandgeschäft wächst aber. Ich habe zu aktuellen Kursen eine erste Position aufgebaut, jedoch auch nur 1%. Wenn die russische Wirtschaft sich schlecht entwickelt, kommt es zu mehr Insolvenzen und Sberbank wird getroffen, auch ohne direkte Sanktionen gegen russische Banken, welche noch drastischer wären.

Handeln Sie bei Sistema? Ist das heute eine Kaufgelegenheit?

hab schon verkauft…Begründung kommt noch.

And which broker is that?

Either Cortalconsors or DAB Bank. DB Bank is better for London orders.

Which online broker do you use to buy russian stocks?

my normal brokers as I buy either the UK GDRs or the German listed cerificates (also GDRs).

fyi

Koç Holding records 49 percent profit jump with real estate sale

http://www.hurriyetdailynews.com/koc-holding-records-49-percent-profit-jump-with-real-estate-sale.aspx?pageID=238&nid=70475&NewsCatID=345

I just would like to had that I asked for an opinion at http://www.oddballstocks.com/ (a website that I follow appreciate too), and I had feedback too.

Sorry, i am on vacation right now and not able to give qualified answers.

Hi there,

I am a value investor and I have been following your blog.

I would like to congratulate you for your analysis they have been very helpful

I invested in a company that semms to be bargain, although I would like to have your opinion.

AUSTRALIAN VINTAGE LTD (AVG)

The company produces and exports bulk and bottled wine, and is the second largest vineyard owner and manager in Australia

P/E forward: 6;

p/B: 30% (a net-net stock);

Although the margins, ROE, RIC are very low and the demand for wine has been decresing in important markets, like china.

I made the investment considering the amasing multiples (p/b, p/e) but the margins are not a great indicator.

Can you give me your opinion?

Laura

Danke für die Einschätzung zu den Genussscheinen der Drägerwerke. Wissen Sie, ob ein Zwangstausch in 10 Vorzugsaktien einen Verkauf mit Abgeltungssteuer darstellen würde. Denn dann müsste man wohl noch einen Abschlag für die Steuer berücksichtigen.

Es gibt m.E. keinen Zwnagstausch o.ä. Bei Steuerfragen bitte Steuerexperte fragen.

Vielen Dank für Ihren Blog. Super Arbeit, danke für die guten Ideen.

Im Feb. 2011 hatte Sie einen fairen Wert für die Drägerwerk Genussscheine in Höhe von 145-180 Euro berechnet. Wie sehen Sie die Situation heute? Welchen Wert erachten Sie heute als fair?

Der “intrinsische” Wert is relativ einfach: 10xVorzüge.

Für den fairen Wert sollte man meines Erachtens einen Unsicherheitsabschlag machen, der m.e. aber deutlich unter 50% liegt.

mmi

Hi,

“Perf. Incl. Div” is the same as annualized rate of return, including dividends?

I have the same doubt as John. The above table is not clear about your performance as a whole. It seams you are hiding your performance …

no, perfomance is perfomance since purchae date.

The above table is not meant to present performance as a whole. As the headline says it shows the current portfolio.

I am not “hiding” anything. If you look through the blog, I am actually disclosing performance on a monthly basis……

What is your annual rate of return in 2012, and 2013?

Chears

if possible ignoring cash

What was your anual rate of return in 2013/2012/2011?

If you search in the blog, you will find it 😉

I was going to ask the same question. Found your results. The results are good – why don’t you make them front and center?

I really love all the great information you post and the amazing debates after your articles. As an amateur value investor having access to this kind of information is invaluable.

Thanks

Hallo,

finde ihren Ansatz sehr interessant. Was halten sie in diesem Zusammenhang von Gazprom?

– Sehr niedrige Multiples

– Hohe Eigenkapitalquote

– Hohe Dividende

Zugegeben, die CG-Probleme sind evident, sollten aber im aktuellen Kurs mehr als eingepreist sein!?

hallo,

danke für den Kommentar. Gazprom ist mir persönlich zu komplex. Ich kann so ein Unternehmen nicht beurteilen, zudem fehlt mir das Vertrauen in Eigentumsrechte bei Russischen Aktien. Von daher habe ich hier keine Meinung.

mmi

Vielen Dank für die rasche Rückmeldung. Finden sie generell, dass sich Value Investing und Emerging Markets aufgrund der von Ihnen angesprochenen Unsicherheiten ausschließen?

Generell ausschliessen möcht ich eigentlich nichts, aber ich finde es in der Tat schwierig direkt in EM Aktien zu investieren. Viel besser finde ich es über eine etablierte Firma indirekt zu investieren. AS Creation mit Ihrem Russland JV ist da ein gutes Beispiel.

mmi

Gibt es einen Plan bzgl. des IVG Wandlers?

demnächt 😉

On what exchange do the Depfa Funding issues trade primarily? thanks

Frankfurt mostly.

Sehr interessant, weiter so. Auch tolle idee wegen der Genusscheine.

Bzgl OMV wenn schon ein österreichisches Big-Cap, dann hätte ich eher die Österr. Post dazu gegeben, die Branche wird (wurde?) zwar vom Internet abgelöst, wird meiner Meinung nach aber unterbewertet. Der Trend wird etwas übertrieben vom Markt, pakete gibts weiterhin + ich geh die wette ein, dass schon längst fast nur solche affairen über post geschrieben werden, die auch großteils bleiben werden.

Post “Liefert” weiterhin gute Resultate ab und zahlt eine hohe, wachsende Dividende (c.a. 6.6%) zugegeben bei hoher ausschüttung (c.a. 75% vom Cashflow). Sehr gutes Management.

Btw, wegen allen diesen Stocks, Ist hier jemand Österreicher (bin selbst auch schuldig 😀 )?

hallo,

danke für den comment.

Ösi Post kommt in meinem Modell nicht ganz so gut weg. Kostet 3 fach Buch und produziert gerade mal die Kapitalkosten. Das ist in “meiner Welt” eine klare Überbewertung.

Der Flughafen ist da interessanter.

mmi

hallo,

nein, DNick finde ich nicht so interessant. Ich hatte mir das vor einigen Monaten mal angeschaut.

MMI

Ist für ein Value Investor wie Sie die DNick Holding interessant. Die Gesellschaft soll “delisted” werden und das stellt sich sehr nachteilig für die Kleinaktionäre dar. Ich denke jedoch, dass man bei einem Börsenwert von ca. 43 Mio. Euro in Zukunft mindestens 20 Mio. Euro Cash als nicht betriebsnotwendiges Kapital ausschütten kann und das bei einem möglichen bereinigten JÜ in Höhe von 3,6 Mio. Euro (konservativ geschätzt). Leider kann ich die gerichtlichen Chancen gegen das Delisting nicht einschätzen. Haben Sie eine Meinung.

Hi,

You position in Mapfre is not present into your portfolio?

hi peter,

Portfolio is always end of last month. I bought Mapfre only in August, and unfortunately only 0.5% in the blog portfolio.

MMI

Dafür wird die TUI endlich den Frenzel los – das ist sicherlich zuträglich zum Unternehmenswert… Unglaublich einer der größten Geldvernichter-Manager die es in Deutschland gibt!

Was halten Sie von einem Short auf TUI. Die Gesamtergebnisrechnung zeigt einen Verlust von ca. 900 Mio. Euro per Q3. Die TUI AG hat noch Finanzschulden von über 2 Mrd. Euro. und keinen Zugriff auf den Cash der überwiegend in der 53 % Beteiligung der TUI Travel liegt. Auch die Ergebnissituation der TUI Travel ist sehr schlecht. Mit dem Abgang von Herrn Frenzel könnte sich die Refinanzierung als sehr schwierig erweisen. Da der Nachfolger ein Branchenfremder ist und sicherlich bei Vodafone keine schwierigen Unternehmensfinanzierungen zu stemmen hatte.

in der Tat ein Sch….laden. Irgendwie wursteln sich die immer durch, fragt sich in der Tat wie lange noch.

hallo cehri,

Ehre wem Ehre gebührt, die Green Mountain Ide kam von WhiteCollarFraud, einem Blog eines verurteilten Betrüger CFOs, Sam Antar.

Glückwunsch zu Deinem Short bei Green Mountain !

Ich glaube der David Einhorn liest bei Dir heimlich mit und hat die Short Idee von Dir. Ich würde bei Ihm anrufen und nach einer Provision verlangen 🙂

Zu dem Thema “own currency” empfehle ich die Ausführungen von Ray Dalio (Bridgewater)

http://www.bwater.com/home/research–press.aspx?agreed=681454

danke für den Link. die Sachen stehen schon länger auf meiner (sehr langen) research Liste

Hallo,

dein Musterdepot ist noch nicht aktualisiert, oder? Soweit mir bekannt ist, hast Du dich aus der Position von Autostrada getrennt.

Gruß

hallo,

ich aktualisere nur monatlich im Blog, für “”real time” fehlt mir leider die Zeit 😉

MMI

Sie haben eine sehr interessante Strategie. Ich finde Ihre Ideen sind sehr informativ. Weiter so.

moin dante,

danke für die Hinweise.

a) werde ich versuchen

b) habe ich gemacht, wäre aber wohl auch sinnvoll in die Page einzufügen

c) ja, mein eigenes Portfolio sieht (abgesehen von der Größe) recht ähnlich aus.

mmi

Sehr gute Arbeit. Danke für die vielen Informationen und Einblicke!

Anmerkungen/Fragen:

a) Häufigere Aktualisierung wäre wünschenswert.

b) Gesamt-Performance-Messung wäre wünschenswert

c) Ist das ein Testportfolio oder gibt es das Portfolio wirklich?

Pingback: Opportunistic Short: Green Mountain Coffee Roasters (GMCR)15 | valueandopportunity