German Startups Group KGaA – Where Deep Value meets Venture Capital

Disclaimer: This is not investment advice. Please do your own research !!!

Management summary:

Despite many issues in the past, I do think that German Startups Group, a stock listed VC investment vehicle, represents an interesting “deep value” situation, where one can buy 1 EUR of underlying value for less than 50 cents. A lot of things have changed into the right direction and there is the chance for some (soft) catalysts in the relatively near future. On the other hand, the unusual corporate structure in combination with a small market cap (EUR 15mn) and relatively illiquid trading also clearly makes it a risky investment.

“Never say never”

Some of my readers will ask: What did make my opinion change on this ?

In a post about investing in publicly listed VC companies a year ago, I wrote the following about German Startup Group (GSG):

German Startup Group is a tiny listed VC company which invests as the name says in German start-ups. Looking at the performance since their IPO in 2015, we can see that they did even worse than Rocket:

My impression (without a very deep analysis) is that German Startups is not a value add VC but rather a “spray and pray” kind of investor. They invest more or less randomly across sectors. In their last interim report interestingly they announced a strategy shift from VC investor to a kind of VC asset manager /platform.

In principle, this sounds quite interesting, but I am not sure if they can actually pull this off. They already needed to issue debt earlier this year as they have very little liquidity and the investors clearly have doubts.

Very unusual structure for a public company

GSG has been set up as a public company, however with a special German structure called KGaA. A KGaA structure is a mixture of a private company with a dominating part (“Komplementär”) and public shares that have less rights (“Kommanditist”). The most unusual feature is however that they tried to “mirror” a typical management fee & Carry structure.

In GSG’s case, there is a 25% carry on whatever gets distributed to shareholders as profit plus a theoretical management fee of 2,5% that gets charged on TOTAL ASSETS of the company.

When I first read this 2 years ago I was thinking to myself: How stupid can a shareholder be to accept this, especially if the company buys majority stakes and then the management fee is charged on the consolidated asset. Plus, the 25% carry does not include a hurdle rate (6% to 8%) which is normally standard for most “Normal” VC funds (not for the top funds like Sequoia etc.).

Changes into the right direction:

However a few things have changed and a few things I have understood now better, also with the help of 2 posts from the CEO in a German stock forum:

- the 25% carry is a total value carry based on German GAAP including all costs for running the AG (and not a deal by deal carry as I thought before)

- The management fee has been reduced twice. In the 6M 2019 report they mention that at a stock price below 1,80 EUR, the management fee is further reduced.

- The salary of the CEO is netted from the management fee,, the company as such does not bear any other cost for the asset management

- the management fee pays the total team of the CEO (2 fixed employees, 2 part time) plus office etc.

All in all, things look better now but clearly not perfect from a shareholder point of view.

However some other positive things happened:

- they now report surprisingly transparent

- continued to sell minority investments, mostly at book value

- their majority participation Exozet seems to be doing well and they intend to sell as well

- the company uses the proceeds to pay back debt and buy back shares (capital allocation seems to become better)

- They are in the process of changing their business model into a asset manager, which if successful, could unlock a valuation change and is less capital intensive

- Some good investors have come on board (Frank Fischer) and the supervisory board has added some decent members

Valuation:

The valuation of GSG is a little bit tricky as they consolidate Exozet and have started other activities that are/will be consolidated. So my approach is as follows:

I will try to value GSG based on the book value of the equity (NAV) adjusted for

- the actual valuation of the minority VC investments

- adjustment of the consolidated 50,8% Exozet stake

- plus/minus any value attributable to the other activities that are not reflected “on balance”

- minus a structural discount

Minority VC investment valuation

Valuing a VC minority portfolio is not easy. GSG gives us the IFRS book value of the participations which include revaluation and resulted in a total value of 28,6 mn EUR in June 2019. The problem with these value is as follows:

- only during a funding round, prices can actually be observed

- but even these observed prices are often misleading (primary vs. secondary pricing) and volatile funding rounds

GSG also provides the information that the 15 actually disclosed investments account for 86% of the minority portfolio value and that the 8 “focus” investments alone are worth 76% oft the 26.5 mn EUR IFRS value. The rest is attributed to a number of small undisclosed investments.

In order to verify these values, I did the following: I looked what I could find quickly on Google about the existing portfolio companies and did a “quick and dirty” valuation based on very crude measures (money invested, sales, gut feeling) and then compared it with the stated values. Here are the results:

| Stake | Company value | Value mn EUR | Method | |

|---|---|---|---|---|

| ArmedAngels | 2.80% | 34 | 0.95 | 1 x Sales |

| Auctiontech | 23.40% | 20 | 4.68 | Series B valuation |

| Ceritech | 8.80% | 10 | 0.88 | Pre series A |

| Chrono24 | 1.20% | 400 | 4.80 | 0.5 GMV |

| Junique | 1.70% | 29 | 0.48 | 1xmoney |

| Mister Spex | 1.30% | 300 | 3.90 | 2.5x money |

| Remerge | 2.40% | 100 | 2.40 | Estimate |

| Simplesurance | 1.60% | 120 | 1.92 | Estimate |

| Sum “focus” | 20.02 | 73.59% | ||

| Customer Alliance | 1.90% | 40 | 0.76 | Estimate |

| Finiata | 1.70% | 10 | 0.17 | estimate |

| Fiagon | 2.20% | 27 | 0.60 | 4xMonay invested |

| Onefootball | 0.25% | 80 | 0.20 | 5xmoney, Adidas |

| Soundcloud | 0.15% | 250 | 0.38 | Emergency funding 2017 |

| Wunder | 0.40% | 80 | 0.32 | Assumed premoney |

| Thinksurance | 1.34% | 30 | 0.40 | Estimate, pre funding |

| Sum small | 2.83 | 10.39% | ||

| Sum Focus & small | 22.84 | 83.98% | ||

| Value 100% of assets | 27.2 |

My result is surprisingly close to what GSG has on its books. Of course each of the single investments can be valued very differently, but in aggregate my feeling is that the book value is a reasonable proxy for the true value.

The quality of the disclosed portfolio is surprisingly OK. Although there doesn’t seem to be a clear strategy, some of the assets (Mr. Spex, Chrono24, Wunder, Simplesurance) have a decent reputation.

Some more recent developments:

End of August they have sold one “focus” investment and one partially and got “mid single digit” mn EUR proceeds for this. Comparing it with the portfolio overview page, we can see that it was the remainder of Chrono 24 and some other stake that is not mentioned. SO ot seems that the 4.8 mn EUR that I assumed for Chrono 24 are quite realistic. Selling more than 20% of the portfolio more or less at book value, should in theory further support a much higher valuation of the stock as the risk now has been reduced.

Exozet Valuation and impact on NAV

Next is the question on how to treat the 50,8% participation of Exozet. Exozet, a digital agency, is fully consolidated into German Startups Group so there is no directly observable book value. The impact on the NAV can be however reverse engineered by the minority interest:

Minority interest per 30.6.2019 is 1.868 mn EUR, which represents (100%-50,77%)= 49.23%. Which in turn means that the stake is valued at 1.95 mn EUR within GSG’s shareholder equity position.

Interestingly I found some news that in 2018, German Startups were considering to sell the stake for around 2.5 mn EUR. However looking at 6M 2009 they report numbers as follows.

6M Sales 7.951 mn EUR (yoy +33%) and a “double digit” EBIT margin. The aggregated minoirty interest per 6M 2019 was +260K EUR. However German Startups for instance also run some of their other activities (Fund management) with minorities, so I gues the Exozet Net income might be higher.

So let’s assum Exozet makes a 10% EBIT margin, we would end up with an annualized EBIT of around 1.5 mn EUR. A company that grows at 30% would normally fetch a valuation of north of 8-10x EBIT, however to stay a little bit more on the conservative side I will use a valuation of 8xEBIT which gives us a company value of 12.8 mn EUR and a value of the stake of 6,5 mn EUR.

For a reference, stock listed Digital Agency Syzygy, who based on 9M numbers runs at an annualized revenue of around 64 mn EUR and an EBIT of 5,3 mn is valued at an EV of 90 mn (EV/EBIT 18) with almost no growth.

This leaves us with a positive adjustment of (6,5-1.95)= 4.55 mn EUR on the book value of equity for GSG which is quite significant (0,42 EUR per share)

Other business activities

In November 2017, GSG started a online platform to facilitate secondary transaction in shares of startups. According to the 6M 2019 reports, in total 3.5 mn EUR volume has been traded in these 20 months with a total fee income of 150k. Clearly this is no easy business, but I still would value this at the current stage with 1.5 mn EUR.

Additionally, GSG now tries to actually launch a VC fund. I haven’t seen any announcement yet that it actually happens, so therefore I would attribute zero value to this. There is also a crypto effort under way but to this I also attribute 0 value.

Tax loss carry forwards

In 2018, GSG had to reduce their tax loss carry forward by ~ 2mn EUR. This could be recovered if they generate taxable income in the future. Although capital gains are not taxable, their other activities could at some point generate taxable income. Therefore I would value them at ~50% ot 1 mn EUR

Bringing it altogether, here is the final valuation overview:

| GSG Valuation Summary: | ||

|---|---|---|

| EUR | per share | |

| Book value of equity | 28,689,000.00 | 2.64 |

| Adjustment for minority stakes | 0 | 0.00 |

| Adjustment Exozet | 4,563,398.51 | 0.42 |

| Adjustment other activities | 1,500,000.00 | 0.14 |

| Adjustment tax loss carry forw. | 975,000.00 | 0.09 |

| Total adjusted equity | 35,727,398.51 | 3.29 |

| Structural discount | -8,931,849.63 | -0.82 |

| Adjusted Book Value | 26,795,548.88 | 2.47 |

| Market cap GSG at 1.4 | 15,195,600.00 | 1.40 |

| In % of total adjusted Book value | 42.53% | |

| In % after discount | 56.71% | |

| Upside w/o discount | 135.12% | |

| Upside after discount | 76.34% |

So before applying any discount, according to my estimates the adjusted NAV of GSG is at 3,29 EUR per share or 24% higher than the stated book value or 135% of the current stock price. Applying a 25 % “structural” discount, we still end up with a nice potential upside of +76% to the current stock price. Of course all my assumptions could be wrong and these value can change quickly, but for the time being it looks like that GSG is dramatically undervalued.

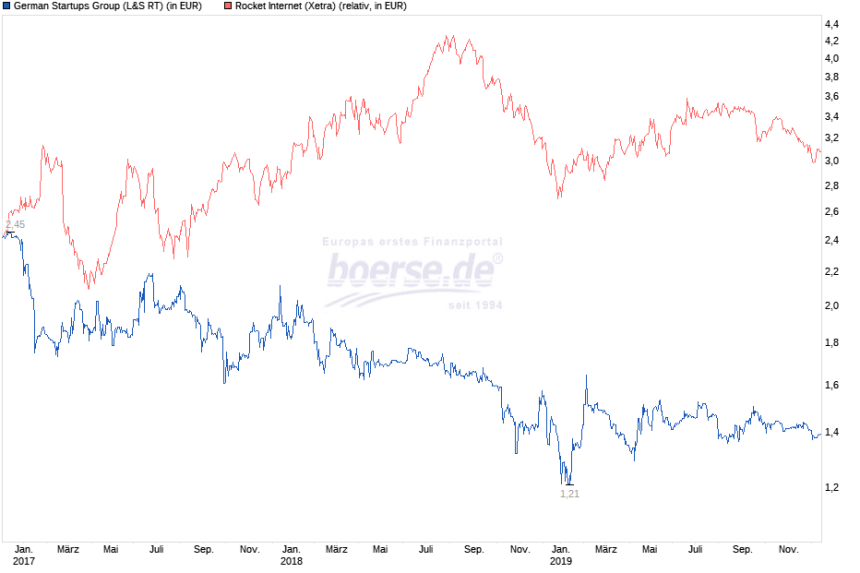

Why is the stock cheap ?

The stock chart since the IPO clearly shows that investors are not too happy on what had happened at GSG:

The stock nearly halfed whereas for instance Rocket internet did yquite Ok.

So as always, one should ask: Why is there such a big discount to “fair” value. I think there are a few reasons:

- the value of the company is not so easy to understand (combination of majority owned asset, unlisted stakes) despite a notable improvement of the reporting and communication

- The VC investment strategy as such was not really convincing (Spray and pray)

- The company has a pretty bad reputation and partially for the right reasons. The former co-MD who was mostly responsible for this has left the company and is now being sued. Among other things, he charged significant “kick backs” on stakes that GSG bought. GSG is suing him (and others) now which is well documented in the shareholder letters

- there is relatively little liquidity in the stock and the market cap is tiny.

- Investors do not like the KgaA / carry structure

So I do think that the main reason is that most (old) investors are most likely frustrated and have sold for more interesting new stocks and GSG has not been able to attract that many new interested investors.

Pro/con overview

As always a quick high level pro/con list:

+ deep discount to fair value

+ observable improvements in strategy, reporting and capital allocation

+ Potential catalysts (further sale of assets and share buybacks)

+ additional potential through new activities

+ good alignment with CEO incentives (at least until 1,80 EUR /share)

– unusual set up

– volatility of underlying assets

– “one man show”

Management:

A few words on managment. Initially, there were two MDs running the company. This is a picture from the IPO:

In the meantime, the guy on the left with the “interesting” hair cut left and only Christoph Gerlinger is the remaining MD. Christiph Gerlinger has a quite successful past. He founded one company that went public and got sold (Frogster Interactive) and was CEO of another company that went public (CDV Interactive). The last two reports explain in pretty “gory” details why Gerlinger is now suing his old Co-MD, among other things, the other guy paid himself private commissions when he bought stakes for GSG. Gerlinger seems to have a good network, although as mentioned above, his strategy is not always so clear.

Summary:

Overall, I have clearly changed my mind on GSG. Although it is not the “Perfect” stock, the combination of positive changes and deep discount convinced me to buy a 4% position for the portfolio at around 1,40 EUR/share for the “opportunistic” portion of my portfolio-

There are clearly significant risks, but I do think that the potential upside compensates for that with a margin.

What is going on with GAI? Why leave PE business 18 months into 4-5 year investment? GAI also held a direct position in the PE portfolio company, which I understand it sold, again 18 months into a 5-year investment period.

one more pivot 🙂

SGT German Private Equity – Strategic Focus on Artificial Intelligence

Renaming to ‘German AI Group’

https://sgt-germanpe.com/index.php/press-release-13-march-2023/

Bumsbude 😉

So little time, so much to do 😉

Today I full sold my position in German Startups Group. The trigger was this Adhoc news from today:

https://www.finanznachrichten.de/nachrichten-2020-07/50183540-dgap-adhoc-german-startups-group-gmbh-co-kgaa-german-startups-group-fusioniert-mit-sgt-capital-und-wird-zu-einem-boersennotierten-private-equity-a-016.htm

As far as I understood this, they want to pivot into a Private Equity manager with an unknown PE company based in Singapore, Cayman and Germany. I couldn’t find any actual names about this SGT capital company. As my initial case was expecting distributions to shareholders and not such a pivot, I sold out and say “thank you and good bye”.

Edit: Selling price was on avg. 1,71 EUR/Share. More details later this week.

Do you understand what is the equivalent value for the 50m shares they are getting? So what is SGT bringing to the table to justify receiving circa 85m EUR?

No. In theory it would be the track record of the team but as there is no information, no one knows.

Nice amount for a track record. Should be easy to be transparent on that prior investments and persons generating it.

I see the CEO is buying shares today at €1.78 and €1.79

Yep. but so far only with pocket money….

As I mentioned, for me, the initial investment case is over. Now it is a totally new case.

Surprisingly upbeat comment by German Startups today

http://www.german-startups.com/index.php/pressemitteilung-vom-24-april-2020/

“Nach Ansicht der Geschäftsführung wird die German Startups Group nicht durch die Covid19-Pandemie beeinträchtigt, weil diese nach heutiger Kenntnis keine wesentlichen positiven oder negativen Auswirkungen auf ihre für sie wesentlichen Beteiligungen hat und die Aktivseite der Bilanz ohnehin zu einem großen Teil aus liquiden Mitteln besteht.”

CEO is stil buying (small amounts) at 1,70 EUR

https://www.boerse.de/nachrichten/DGAP-DD-German-Startups-Group-GmbH-und-Co-KGaA-deutsch-/14396035

Another (small) Purchase of Christoph Gerlinger at 1,65 EUR/share

https://www.boerse.de/nachrichten/DGAP-DD-German-Startups-Group-GmbH-und-Co-KGaA-deutsch-/12357775

Oh MMI! Have just read this. So sorry you drank the VC coolaid. Your analysis which is normally very interesting (and I mostly agree with) here is just so so flawed. Let me tell you how VC value portfolios (and I know cause I’ve been one for the last 12 years). They stick a finger in the air, they wave it about and then put some numbers down which they think the auditor won’t argue with too hard. That’s it, and I mean really that’s it. So the concept of this being a value investment because it’s a discount to some random number book value is laughable – especially when the people waving the finger are those two characters in the photo. And this is before you factor in that all those investments that have „book value“ are mostly burning cash – therefore a massive factor in your valuation ought to be the willingness of the next fool along to come along and fund them – but this of course is completely ignored in the valuation „process“.

You have stuck some money on red and are now spinning the wheel – there’s nothing to say the ball won’t land on red. But the idea that betting on red was somehow better value than betting on black is nonsense. Sorry to be direct. Good luck regardless though – I genuinely don’t want to see you lose money.

Dear Pogonific,

thanks for the long comment. I agree to a certain extent on valuations but I disagree about a few things. Plus I don’t think that you have actually read the post all the way. Let me point out a few things that you most likely missed:

– the “book value” was only the starting point. I used my own valuation (which might of course be wrong) and ended up with a total value that is actually higher. However I made a 25% haircut in the end which still shows significant “margin of safety” at least for me

– the first real test of that book value happened actually one day after I released the post Their biggest asset Exozet was sold for cash and guess what: I had underestimated the value significantly. Instead of a 12,8 mn company valuation they exited at around 22 mn, resulting in 1 EUR cash per share which was responsible for pushing up the share price for ~20%

– with all the sales happened in the last month, net cash (debt already deducted) should now be at least 11 mn or around 2/3 of the market cap, so there is some donwside protection from a fundemantal point of view

– I assume that they will distribute some of that cash by buying back shares in 2020 which will decrease the risk further

Of course can I lose money with this one, but so far it looks like that there is actually some value and not only hot air as you indicate. And it is clearly not an invetsment that I intend to hold for the next 2 decades or so, that why this is more a special situation.

MMI

I don’t believe constructs like KGaA should be publicly traded. When ever I come across that I have two thoughts:

– I’m not welcome

– It is only a question of time when I’m going to be screwed out of money

My feelings towards Vorzüge are similar but it’s a more honest way of going about it. I am willing to make an exception if the voting shareholders have a long track record of showing responsible stewardship with respect to minority shareholders. Jungheinrich is a positive example and Schaeffler is a negative one, in my opinion.

There is no doubt that vehicles like that are useful and neccessary – in private markets.

Super Timing 🙂

Glückwunsch !

https://www.comdirect.de/inf/aktien/detail/news_detail.html?NEWS_CATEGORY=EWF&NEWS_HASH=e5d34f46e8ea7b84ca0aa22f5b7cdeb4fa8f216&OFFSET=0&SEARCH_VALUE=DE000A1MMEV4&ID_NEWS=928729577&ISIN=DE000A1MMEV4

Holy guacamoly !!!

Almost suspicious !!!!

X-D

I consider it an early Gift from Santa…

Nice one . Wenn done!

After checking the numbers 2 take aways from that news:

– the sales price for Exozet is much higher than I assumed

– on the flip side, the book value of Exozet also seems higher than I thought.

Still, in total, the transaction increases NAV by ~0,13 EUR per share against my estimate plus the risk is now clearly lower.

I increased my position by 1% at around 1,72 EUR/share.

Christoph Gerlinger seems to have bought some shares as well.

Where do you track the German insider transactions?

Interesting idea. Thanks for blogging in 2019. Appreciated.

Also, if I look in the H1 report (my German is not very good) there are 11.75m shares outstanding, as well as 0.23m treasury shares (with the footnote that 0.9m shares were bought back per 31 / 7 / 2019). Doesn’t that make the (outstanding) share count 10.854m? Or are you including treasury shares for a reason?

A comment on German Startup from Börsengeflüster (10/2019)

https://boersengefluester.de/german-startups-group-kleine-aktie-mit-grosem-discount/