Performance April 2013 & comment: “All time highs”

Performance April 2013:

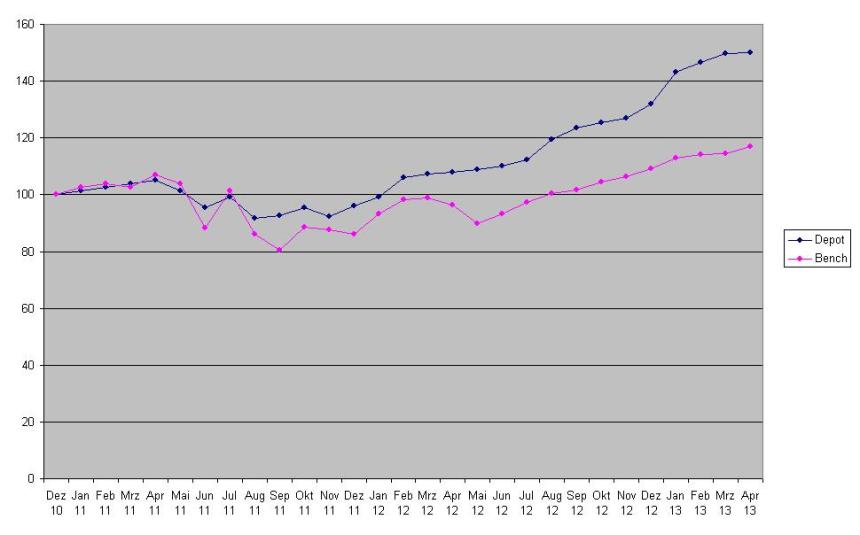

Performance for the month April was +0.5% against +2.1%, an underperformance of -1.6% vs. the Benchmark (50% Eurostoxx, 30% Dax, 20% Dax). YTD, the portfolio is up 14.0% against 4.9% for the Benchmark.

For some reason, the underperformance in April reassures me that my strategy is working. I would assume in “up months” a weaker performance than the benchmark, in down months a significant better relative performance. However, in the first 3 months of 2013, the portfolio strongly outperformed although we had seen 3 “up months” in a row and I ran at ~15% net cash in the portfolio. Despite the nice developement, one has to ask if there isn’t a lot of “hidden beta” in the portfolio.

However the current month shows that the stocks do have “their own life” versus the benchmark. For instance Tonnellerie, which acted like a high beta stock in the beginning of the year came down to earth with a -17,7% performance in April. As a reader asked me for it, here is the graphical performance since Inception:

Portfolio as of 30.04.2013:

| Name | Weight | Perf. Incl. Div |

|---|---|---|

| Hornbach Baumarkt | 3.8% | 2.8% |

| AS Creation Tapeten | 4.7% | 55.2% |

| Tonnellerie Frere Paris | 5.3% | 62.2% |

| Vetropack | 4.4% | 7.4% |

| Installux | 2.8% | 8.7% |

| Poujoulat | 0.9% | 6.4% |

| Dart Group | 4.1% | 124.0% |

| Cranswick | 5.4% | 26.6% |

| April SA | 3.3% | 4.2% |

| SOL Spa | 2.7% | 25.4% |

| Gronlandsbanken | 2.2% | 23.2% |

| G. Perrier | 3.0% | 4.8% |

| KAS Bank NV | 4.7% | 23.0% |

| BUZZI UNICEM SPA-RSP | 5.2% | 24.8% |

| SIAS | 5.4% | 48.6% |

| Bouygues | 2.6% | 10.2% |

| Drägerwerk Genüsse D | 10.1% | 193.0% |

| IVG Wandler | 4.1% | -17.7% |

| DEPFA LT2 2015 | 2.7% | 58.8% |

| HT1 Funding | 4.7% | 56.4% |

| EMAK SPA | 4.3% | 31.2% |

| Rhoen Klinikum | 2.2% | 8.4% |

| KPN shares | 0.6% | 0.2% |

| KPN rights | 0.4% | -1.0% |

| Short: Focus Media Group | -0.9% | -8.5% |

| Short: Prada | -1.0% | -13.7% |

| Short Kabel Deutschland | -1.0% | -5.0% |

| Short Lyxor Cac40 | -1.2% | -11.7% |

| Short Ishares FTSE MIB | -2.0% | -10.3% |

| Terminverkauf CHF EUR | 0.2% | 6.4% |

| Cash | 16.4% | |

| Value | 42.5% | |

| Opportunity | 47.0% | |

| Short+ Hedges | -5.9% | |

| Cash | 16.4% | |

| 100.0% |

Major changes were: Increase in Perrier to now 3%, sale of Total Produce and WMF pref shares, increase in IVG convertible plus 1% KPN as a new share. For my portfolio, this was a very active month.

Comment: All time highs

A lot of newspaper articles are concerned with the current “all time highs”, both in the DAX and the S&P 500 as well as the Dow Jones. Many people argue that level is of very high significance, either as an upper boundary or support.

In my opinion this is one of the most prominent cases of “Anchoring”, a well documented behavioural finance bias. Yes, the Dax already 2 times bounced back from the 8000 point level, in 2000 and 2007 as this chart clearly shows:

However if you look at the composition of the DAX in those years one can quickly see that the Dax is a very different animal now than in the past.

Those are the Top 5 stocks now:

| Weight | |

|---|---|

| BASF SE | 9.9% |

| Bayer AG | 9.8% |

| Siemens AG | 9.0% |

| SAP AG | 8.1% |

| Allianz SE | 7.6% |

Compare this to the top 5 a mere 5 years ago on December 2007:

| Weight | |

|---|---|

| E.ON SE | 10.1% |

| Siemens AG | 9.9% |

| Allianz SE | 8.4% |

| Daimler AG | 8.2% |

| BASF SE | 6.2% |

Yes, 3 stocks are still in the Top 5 (Allianz, BASF and Siemens) but 2 out of 5 are new and the weights are significantly different.

Even if we compare the top 5 based on their P/Es, we can see that even those shares which remained in the top 5 trade at quite different P/Es:

| PE 2007 | PE 2013 | |||

|---|---|---|---|---|

| E.ON SE | 15.6 | BASF SE | 14.6 | |

| Siemens AG | 26.3 | Bayer AG | 26.3 | |

| Allianz SE | 7.5 | Siemens AG | 14.1 | |

| Daimler AG | 23.3 | SAP AG | 25.4 | |

| BASF SE | 12.4 | Allianz SE | 10.4 |

So what does that mean ?

In my opinion, the current absolute level of the DAX compared to the past is totally irrelevant. Any investment decision on such an arbitrary basis is a clear “anchoring bias”. Investment decisions should be made irrespective of index levels. If you find a cheap stock buy it, when a stock is too expensive, sell it. It doesn’t matter where the Index is compared to its past.

Hi MMI, I really enjoy your blog even though I am just a beginner at all of this, so some of it goes over my head. I notice that EMAK has had a big surge since they announced 1Q results. Looking at the figures released, it seems that EPS increased compared to previous FY based on accounting tricks rather than increasing sales or decreasing costs. Should we be concerned about such a large increase in change in inventories for example? Would love to hear your opinion. Thanks.

Andrew, thanks for the comment.

Why exactly do you think they used accounting tricks ?

Receivables and inventory is actually lower than both, year end and 1st quarter 2012. I think the results are pretty good. Despite lower turn over, they seem to be succesful in cutting costs.

Net debt is down as well, cashflow is positive. So I don’t see your point here.

mmi

Receivables 31Dec12: 102,825 Receivables 31Mar13: 136,692

Inventory 31Dec12: 120,958 Inventory 31Mar13: 127,424

Both have increased in 1Q.

They also benefited from change in USD/EUR exchange rate, increase of 1,292k 1Q12 compared to 1Q13.

Also EMAK comment: “The result for the first quarter of 2012 was negatively impacted by two non-recurring items .. Adjusting the data for these effects, EBITDA in the first quarter of 2013 would have decreased by 8, 1% over the

same period.”

Am I looking at the wrong numbers? I did fail accounting at university. Twice. Passed it eventually.

#andrew,

you are correct, compared to year end inventory and receivables are higher.

Compared to March 2012, however, inventory and receivables are lower, in line with the slightly lower sales number.

If you look at EMAKs quarterly sales, you can easily see that it is a seasonal business. Lawn mowers, chainsaws etc. are being bought mostly in spring time. So it is quite normal that inventory rises in the first quarter as inventories have to be build up. Sales in the first 6 months of the year account for more than 60% of annual sales so investories are naturally higher if the production capacity does not change.

It is also correct, that Q1 EBITDA was lower due to one time effects, but again I don’t see an accounting trick here. On the other hand they claim that bad weather has delayed sales in Q1, so therefore Q2 should look better.

I think the market had expected much worse numbers than this and is now positively surprised. I am actually positively surprised as well, as some other Italian companies I am following, saw sales decreases by 20% or more.

FX: Yes, that is a positive effect, but again no accounting trick.

MMI

Ok, thanks very much!

no problem. I always appreciate tough questions from someone who actually reads financial statements 😉

By the way, I don’t think one needs an accounting exam to analyze stocks. Reading carefully like you are obviuously doing is much better !!!

A comment to alltime highs:

Most people forget that the DAX is a performance index (unlike the DowJones or S&P500). I didn’t look it up, but I’d assume that without dividends we would be min. 25% away from the 2000 high.

A look at “DAX Kursindex” confirms this: 2000 high was 6260, today 4400.

Plus there is inflation:

It should also drive stock prices even if marketshares etc. of companies simply stay flat or how would you see that?

Regards,

Woodpecker

While both price as well as performance indices are justifiable measures, it is indeed not very “clean” to compare different index methodologies (needless to mention that the Dow has also a different weighting methodology). Currently the DAX price index is about 30% and about 17% below its 2000 and 2007 highs, respectively.

My perception re inflation and its impact on stocks is mixed and from a rather broad market perspective less positive than often presented in the media (“equities as a quite good hedge against inflation”). More than “normal” rates of inflation will probably create increasing problems for many companies to pass input price hikes fully to customers i.e. such an environemnt will lead to lower margins and thus lower profits for many companies with no particular edge. Of course a moat company which faces a rather inelastic demand curve with few or no substitutes from competitors has much more pricing prower also in case of inflation.

Die Position, die man eigentlich mit Drägerwerk bezeichnen müsste 😀 … und dir real bei Verkauf richtig weh tun würde … Krass was die AGS so anrichten kann, wenn sich kleine Positionen verzigfachen

Nett, dass du schon die Performance von April 2014 kennst 😀 … Wie stehen die Kurse da so 😀

Mach doch mal spaßeshalber eine Nach-Abgeltungsteuer-Betrachtung. Deine Träger-Position würde den Depotwert dank AGS ja schon um die 2% senken 😀

Da die BM vor Steuer ist, macht hier auch nur ein Vorsteuer Vergleich Sinn. Den Nachsteuereffekt sehe ich in meinem eigenen Portfolio zur Genüge.

Was allerdings eine Träger-Position ist weiss ich nicht.