IVG – JPM Research on property values

A friendly reader forwarded me a current equity research report from JPM about IVG.

Not surprisingly, they estimate the value of the share as zero:

Our EVA based European

Valuation Model implies zero value for IVG ordinary equity as a going concern, while a DCF driven revaluation implies zero equity value on the existing balance sheet. We therefore lower our Mar-14 EVM based price target from €2.22 to €0.01, and await the announcement of restructuring plans over summer 2013.

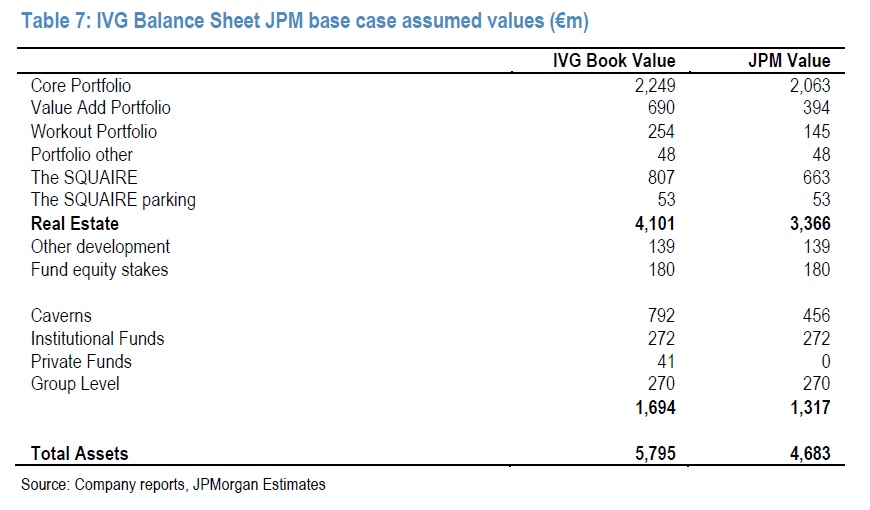

Although one might wonder, why they had a 2.22 EUR price target before. Much more interesting is that they actaully come up with an asset value for the IVG portfolio which looks as follows:

Although they use slightly different adjustements, thei asset value is very similar to what I calculated a couple of weeks ago:

| 2011 | Adj. Val | 2012 | Adj.Val | Comment | |

|---|---|---|---|---|---|

| Intangibles | 251 | 0 | 253 | 0 | 100% write off |

| Inv. Property | 3,964 | 3,398 | 3,654 | 2,920 | scaled to 7% yield |

| PPE | 157 | 118 | 190 | 143 | 25% discount |

| Financial Assets | 189 | 142 | 174 | 131 | 25% discount |

| equity part | 95 | 71 | 84 | 63 | 25% discount |

| DTA | 404 | 0 | 336 | 0 | 100% write off |

| Receivables | 60 | 45 | 25% discount | ||

| Inventory | 1,025 | 513 | 996 | 498 | 50% discount |

| Receivables | 179 | 134 | 190 | 143 | 25% discount |

| Cash | 238 | 238 | 142 | 142 | 0% discount |

| AFS | 341 | 256 | 58 | 44 | 25% discount |

| Asset Management | 275 | 318 | 1.5% of AUM | ||

| Marekt value caverns | 163 | 140 | 50% of disclosed adj. | ||

| Total | 6,903 | 5,351 | 4,540 |

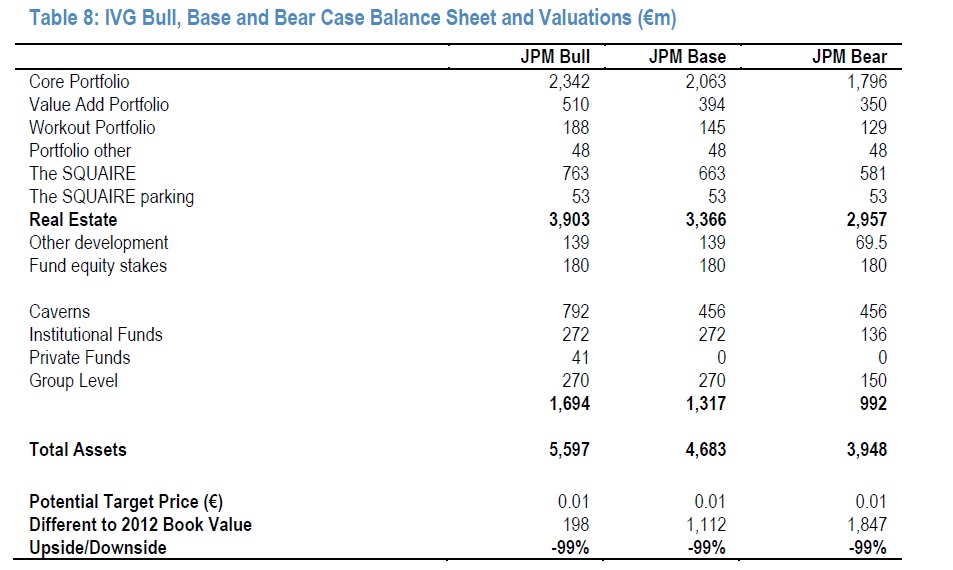

Additionally, they calculate “Bull” and “bear case” scenarios:

The bear case scenario clearly would not leave a lot for convertible holders.This clearly shows the risk of the implicit “leverage” of the secured loans via the convertible.

Summary:

Although the JPM research looks a little bit superficial especially with regard to the liability structure, it is definitely worth to look at in order to get a better feeling for the underlying property values.

Their base case would imply even “full recovery” for the convertible and hybrid, although I think they haven’t modeled the liability structure correctly.

In general, their asset valuation does not look to different from mine,so for the time being I don’t see a reason to sell the convertible at current levels. Also there seems to be no reason to approve any debt for equity swaps.

However both, equity and hybrid capital seem to be clearly out of the money in most scenarios if one takes into account the full liabaility structure.

Hi mmi,

IVG is a very interesting situation and entertaining too, when you read the w:o message boards. I am trying to watch and learn. Now regarding the convertible I have some questions

1) Going concern scenario:

a)How likely is it in your view that they keep as a going concern in 2014 (ie are able to refinance the convertible)

b) At what value will IVG refinance the convertible

c) How are they going to do it (sell propoerty, give equity …)

3) Bankruptcy

a) How much will be the recovery value

b) How long does to realize the recovery value

c) Is the IRR worth it?

Thanks and all the best

max

Hi Max,

very good questions. I am planning a post on that soon….

mmi

Maybe amused is th wrong word. But again, IVG is not bankrupt yet. So any valuation has to include the proability of a going concern scenario or any other scenario.

The “rock bottom” valuation is only one scenario.

If you want to avoid any upside, yes, then focus on it. However if one wants to calculate a “fair value”, the liquidation value has to be included with a certain probability only.

The taxman (and the IMF) is always senior and the Pensionssicherungsverein will only bail out any pension in case of ‘Insolvenzabweisung mangels Masse’ (which is hopefully not the case we we are talking about). The latest valuation of the derivatives position is nothing I would count on. Expect that the counterparties (investment banks) will have asked for a collateral beforehand.

Let’s hope that these loan buyers are smart enough and there will be something left which will rank pari passu what can be distributed in a possible winddown of the real estate portfolio and that fire sales can be avoided.

It is very important to find a rock bottom valuation here, since it is very likely that the company will try to highlight the risk of an insolvency and talk the convertible holders into a debt-to-equity-swap, a write-down in connection with a debtor warrant.or something similar

You could for example read through this document for taxes http://www.meilicke-hoffmann.de/assets/pdf/publikationen/Dr_Thomas_Heidel/4_1_4_6.pdf

and for pensions here on page 27:

Click to access Gutachten_deutsch_final.pdf

I find it kind of amusing within the IVG discussions that many people have very strong opinion but don’t really bother to check the facts.

This is not about rock bottom but about probabilites and expected pay offs.

As I mentioned before; I’m not a Liquidation specialist and I’ve to admit that I have misinterpreted an article on the pension issue I found online. But there is no reason to be amused when you talk about checking facts. The tax ‘document’ you’re referring to is based on the ‘Konkursordnung’ which has been replaced by the ‘Insolvenzordnung’ some while ago. Reading through this ‘opinion’, even then it seemed to depend on the timing and the nature of the individual tax liability. When I talk about rock bottom I obviously refer to the downside risk whích is the Minimum expected pay out.

no, I don’t think that other liabilities have priority if there are no explicit collateral agreements.

Addionally, the uncovered part of the bank loans would be pari passu to the convertible as well and thus increases the recovery.

Without knowing what ‘other liabilities’ exactly comprise, I would expect taxes, pensions and derivatives to be senior to the convertible (approx. 200 mill).

Yes, you’re right I forgot… It’s in particular true if we assume that the vulture funds have a sound understanding of the underlying asset values of these loans(which is a reasonable assumption).

Why should they be senior to the convertible ? They only could be senior if certain assets would have been pledged as collateral.

This is the reason why for instance there is a “Pensionssicherungsverein” to bail out the pensions in such cases.

Your recovery calculation makes sense – good work! What I’m not really sure about is the pecking order among the ‘other liabilities’. In your calculation you assume a pro rata distribution across all liabilities (including the convertible). Although I’m not a liquidation specialist my best guess would be that taxes, pensions, derivatives and probably most other liabilities would be senior to the convertible. Stripping out these positions would bring the recovery down to 64%!?