Annual Performance Review 2013

Performance:

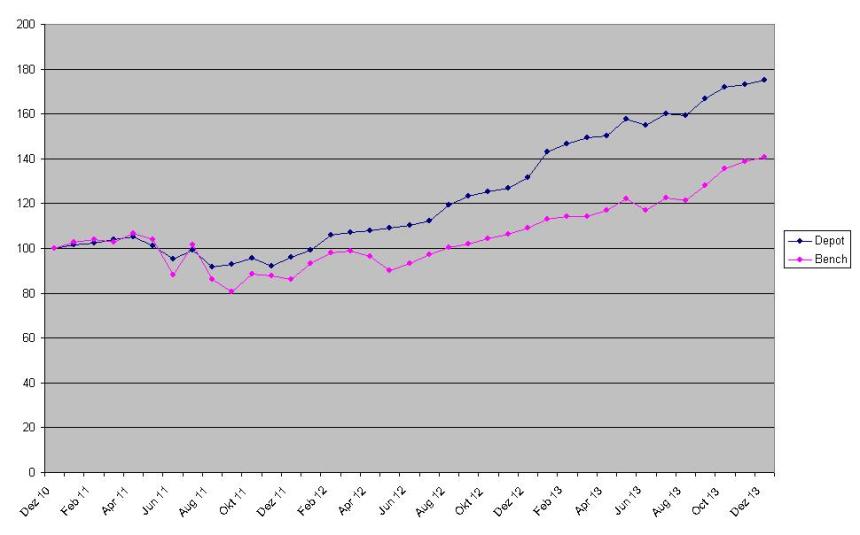

Performance for the month December was +1.2% vs. +1.3% for the benchmark, an underperfomrance of -0.1%. For the year, this resulted in +32.8% vs. +29.0% for the Benchmark (50% Eurstoxx 50, 30% Dax, 20% MDAX), an outperfomance of +3.8%.

Since inception (1.1.2011), the score is now +75.0% for the portfolio (20.5% p.a.) vs. 40.7% (10.4% p.a.) for the Benchmark.

Here is the detailed table:

| Bench | Portfolio | Perf BM | Perf. Portf. | Portf-BM | |

|---|---|---|---|---|---|

| 2010 | 6,394 | 100 | |||

| 2011 | 5,510 | 95.95 | -13.8% | -4.1% | 9.8% |

| 2012 | 6,973 | 131.81 | 26.6% | 37.4% | 10.8% |

| Jan 13 | 7,227 | 143.10 | 3.6% | 8.6% | 4.9% |

| Feb 13 | 7,302 | 146.64 | 1.0% | 2.5% | 1.4% |

| Mrz 13 | 7,315 | 149.59 | 0.2% | 2.0% | 1.8% |

| Apr 13 | 7,469 | 150.27 | 2.1% | 0.5% | -1.6% |

| Mai 13 | 7,808 | 157.67 | 4.5% | 4.9% | 0.4% |

| Jun 13 | 7,468 | 155.12 | -4.3% | -1.6% | 2.7% |

| Jul 13 | 7,845 | 160.00 | 5.0% | 3.1% | -1.9% |

| Aug 13 | 7,758 | 159.10 | -1.1% | -0.6% | 0.5% |

| Sep 13 | 8,194 | 166.85 | 5.6% | 4.9% | -0.7% |

| Okt 13 | 8,676 | 172.04 | 5.9% | 3.1% | -2.8% |

| Nov 13 | 8,878 | 172.93 | 2.3% | 0.5% | -1.8% |

| Dez 13 | 8,993 | 175.04 | 1.3% | 1.2% | -0.1% |

| YTD 13 | 8,993 | 175.04 | 29.0% | 32.8% | 3.8% |

| Since inception | 8,993 | 175.04 | 40.7% | 75.0% | 34.4% |

| p.a. | 20.5% | 10.4% |

As a special service, the graphical developement since inception:

If I would need to advertise the strategy, I would maybe mention the Sharpe ratio for the portfolio which is an unbelievable 1.74 against 0.66 for the benchmark.

Portfolio Year end

| Name | Weight | Perf. Incl. Div |

|---|---|---|

| CORE VALUE | ||

| Hornbach Baumarkt | 4.0% | 15.8% |

| Miko | 3.5% | 9.5% |

| Tonnellerie Frere Paris | 6.3% | 123.4% |

| Vetropack | 3.6% | 7.0% |

| Installux | 2.9% | 38.2% |

| Poujoulat | 0.9% | 34.1% |

| Cranswick | 5.3% | 47.3% |

| April SA | 3.4% | 27.8% |

| SOL Spa | 2.6% | 43.4% |

| Gronlandsbanken | 2.0% | 30.2% |

| G. Perrier | 4.0% | 67.1% |

| IGE & XAO | 2.4% | 36.8% |

| Thermador | 2.7% | 16.7% |

| Trilogiq | 2.4% | 13.1% |

| Van Lanschot | 2.7% | 8.5% |

| TGS Nopec | 2.5% | 2.8% |

| OPPORTUNITY | ||

| KAS Bank NV | 4.6% | 45.0% |

| SIAS | 4.9% | 73.9% |

| Drägerwerk Genüsse D | 7.8% | 171.4% |

| DEPFA LT2 2015 | 2.5% | 72.4% |

| HT1 Funding | 4.2% | 61.9% |

| EMAK SPA | 2.5% | 80.8% |

| Rhoen Klinikum | 4.9% | 25.4% |

| MAN AG | 2.5% | 0.3% |

| Celesio | 1.3% | 0.9% |

| Celesio 2018 | 1.4% | 0.1% |

| Cash | 12.0% | |

| Core Value | 51.4% | |

| Opportunity | 36.6% | |

| Short+ Hedges | 0.0% | |

| Cash | 12.0% | |

| 100.0% |

Performance comment 2013:

2013 was a very positive year in absolute terms for the portfolio as well as again (and the 3rd year in a row) against the benchmark. This is remarkable as I ran on average a cash balance of around 15-20% over the year.

If I were in the professional investment business, I could “sell” this the following way: Look how incredible my stock picking skills are. Even with 20% cash I managed to outperform the benchmark by a good margin. However, I only run my own money, so I can be honest to myself. I often preached that stock market timing is not my strength and that I deeply believe that only a very few people on earth can do this profitably over a longer period of time.

The reason for holding so much cash is mostly, that I sold out stocks that were too expensive in my opinion and I didn’t find enough (or quickly enough) opportunities to invest in. Yes, some stocks got bought out (EGIS), some situations worsened and I took the losses (IVG). But in general, I could have also redeployed the capital into my existing stocks. Especially so considering that I had a lot of new ideas where I only went in with a 50% position.

I think one reason that I didn’t do this was that I was too, implicitly trying to time the market. Even for me, the constant news coverage of the soon to happen crash seem to have taken its toll. For the future, I think it might make sense to implement some kind of maximum cash rule in order to avoid this kind of implicit behavioural biases. I guess I will implement a max of 15% cash with automatically reinvestments in existing positions if the amount gets higher.

The 3 year performance track record looks now very good, but 3 years is a much too short period of time to determine if a strategy really works.

One commenter more than once said that I had simply luck because I had 2-3 good ideas since I started the blog and that it will be much harder in the future.

This is absolutely correct !! When I started in 2010, this was still the first year after the big crash in 2008/2009. Many securities were not efficiently priced and it was quite easy to make money, both in normal shares and special situations like Hybrid bonds. Then again, 2012 offered a great opportunity to buy cheaply into PIIGS shares subsequently French shares. Although I missed some spectacular opportunities (Reply, etc) I still came out well.

On top of that, I was measuring myself to a large extent against large caps but invested mostly in small to mid caps. I do not limit myself to small caps but again, following the financial crisis, especially in the small cap field under valuations seemed to have disappeared more slowly than elsewhere. The MDAX alone for instance would have been much closer to the portfolio with a 62.6% performance over those 3 years. As I have written earlier, I will increase the benchmark weight of small and mid caps going forward.

So in principle, 3-4 ideas (Hybrid bonds, PIIGS and French shares, small caps) were responsible for the outperformance over the last 3 years. Going forward, it will be much harder. At the moment, I do not have any “big ideas” which might yield several new good ideas. PIIGS are mostly fully valued as well as most French stocks and Hybrid bonds. From today’s perspective not a lot of things look cheap and promising.

But both, in the beginning of 2012 and 2013 I was basically in the same situation. Over the last 3 years I tried to expand my Circle of Competence and so far this has yielded new ideas on an ongoing basis. So to a certain extent I am optimistic that there will be new ideas, but it is of course not guaranteed. I actually do expect to underperform for a certain amount of time in the near future.

Outlook 2014

Finally, a few words on 2014. I am not a fan of projections with regard to stock market levels etc, they should be viewed as pure entertainment only. Nevertheless I think there are a couple of fundamental issues that one should watch in order to be prepared for certain potential impacts.

I personally will focus (among others) on the following developments

Long term interest rates

No matter what commentators will say, if one believes that the value of any stock is equal to the discounted future cash flows, higher long-term interest rates will automatically lead to lower intrinsic values of stocks and most other financial assets. If this translates automatically into lower stock prices in the short-term is another question,

European banking union

In my opinion, if this is executed well, this could be an interesting situation going forward for European financial stocks

Renewable energy regulation

The misguided German renewable energy policy caused a lot of troubles for many German and European utilities. It will be interesting to see if the new Government will make any changes. If yes, then one should look at utilities again.

Overall, I think it would be highly optimistic to expect double digit stock market returns over the next 3-5 years, but again, there is no way to tell if we will see another 20% plus year in 2014. There is also a significant probability that markets become more volatile.

Finally, good luck and happy investing to all readers for 2014 !!!

Mich würde interessieren, welchen Performance Anteil deine jeweiligen Unterstrategien hatten – also Value only und Opportunity only.

Ich glaube, dass Sie genug großartige Ideen hatten. Ich denke, dass Sie Ihre Portfolio Diversifizierungsregeln lockern sollten. Meiner Meinung nach, ist es einfach nicht möglich 20 bis 30 großartige Investment Ideen zu finden. So hätten Sie Ihren Cash wunderbar durch Erhöhung der bestehenden Positionen investieren können. Es kann auch mal wieder die Zeit kommen, wenn es Sinn macht, eine sehr hohe Cash Position zu haben. Viel Erfolg für 2014.

congrats! great performance