Ackermans & Van Haaren – Mini Berkshire from Belgium ?

Ackerman’s and Van Haaren is a diversified Belgian company which was on my research pile for quite some time. Bloomberg describes the company as follows:

Ackermans & van Haaren NV is an industrial holding company. The Company’s holdings are in the contracting-dredging environmental services, financial services, staffing services, and private equity investing.

![]()

Looking onto their participations overview on the (very informative) homepage, one can easily see that this is a quite diversified company. From oil palms in Asia (SIPEF) to old age homes, port service companies, real estate investments and an Indian cement company are among the 30 or more participations.

The largest investments are however a 78.75% Stakes in Delen Investments and Private Bank J. van Breda and a 50% stake in DEME, a marine engineering Group.

The DEME stake itself shows that Ackermans is rather an active holding company. This year they surprised everyone by striking a deal with Vinci and traded their 50% stake in DEME (valued at 550 mn EUR) with a 60% stake in CFE, the listed Belgian company which owns the other 50% of DEME.

The stock itself is not really cheap:

P/B ~ 1.3

P/E 2013 ~15

Market cap: 2.8 bn

The stock gained nicely in 2013 and is trading at an ATH:

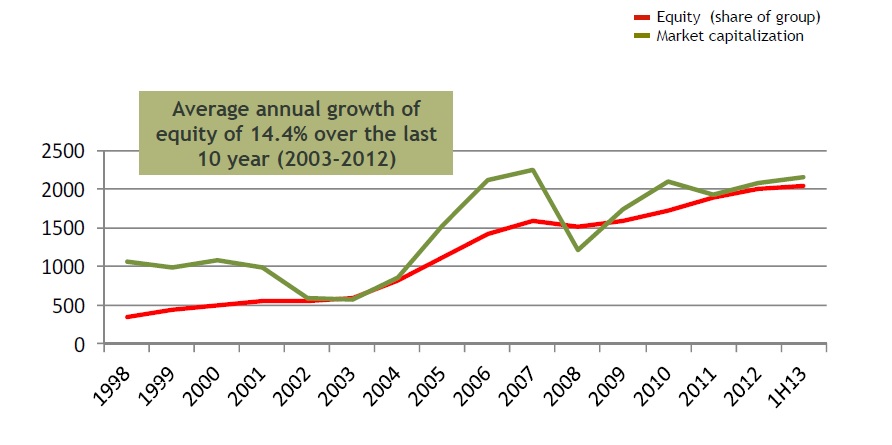

Why did I call them a potential “Mini Berkshire” in the beginning ? Well, that’s what they are showing in their latest Q3 presentation:

14.4% CAGR of book value is not bad over the last 10 years. Just for fun, I calculated Berkshires 10 Year CAGR from 2003-2012 based on the disclosure in the latest letter to shareholders:

| Berkshire | |

|---|---|

| 2003 | 21% |

| 2004 | 10.5% |

| 2005 | 6.4% |

| 2006 | 18.4% |

| 2007 | 11% |

| 2008 | -9.6% |

| 2009 | 19.8% |

| 2010 | 13% |

| 2011 | 4.6% |

| 2012 | 14.4% |

| 10 year CAGR | 10.60% |

So at least for the last 10 years, AvH has clearly outperformed Buffet by almost 4% p.a. which is really a lot.

Step 1: “Quick and Dirty” sum of parts

When I look at a company like AvH, i generally try to do a quick and dirty “sum of part” analysis first. AvH makes it quite simple by providing a net cash figure at holding level which is required as the consolidated accounts include non-recourse debt as well.

The only thing I was not sure was the fact that the holding segment borrowed money from the private equity part in an amount of 120 mn EUR. I decided to play it save and deduct it from the private equity NAV.

So this is the “quick and dirty” result:

| Value | Method | |

|---|---|---|

| DEME | 550 | Implicit valuation takeover |

| Van Laere | 26 | 0.75 book |

| rent-a-port | 5 | at book |

| Maatschappi | 20 | At book |

| Sipef | 130 | market cap 482 |

| Delen | 522 | 1.5 book |

| van Breda | 336 | 1.2 book |

| Extensa | 80 | 0.8 book |

| Leaseinvest | 108 | Traded |

| Financiere duval | 40 | at book |

| AnimaCare | 40 | 2x book |

| MAx Green | 70 | 10x Earnings |

| Telemanod | 30 | 10x Earnings |

| Sofinim | 255 | 75% of NAV minus cash to holding |

| Net cash holding | 148 | Q3 |

| Total | 2,361 |

The result of this exercise is higher than stated book equity of around 2.05 bn EUR, but on the other hand, significantly lower than the 2.8 bn market value.

If I haven’t made a big mistake, then even if some of the holdings like Delen are worth more than I assumed, AvH looks as it is trading at a premium. Although I think the company is a good one and can create value, I would not want to pay a premium, so one can stop at this point and move on.

Summar:

Ackermans & Van Haaren seems to be an interesting company with diverse holdings and a good culture and some very good and interesting businesses. The track record over the last 10 Years looks impressive and is better than Berkshire. Nevertheless, the stock looks overvalued from a sum of parts point of view, offering no margin of safety.

Hi V&O,

I wanted to bring Altamir SCA, the french equivalent company to your attention

The web-site for Altamir SCA is http://www.altamir-amboise.fr/

Regards

V

thanks, have never heard of them.

I’ve been interested in ACKB for a while and after your post I finally decided to take a look at it. While I agree with almost everything, it is not clear the valuation of DEME. If I understand it correctly, after the swap ACKB will own 60.4% of CFE, which today is valued at around €1.6 bn (price shot up from €43 in Sept to €63 today), so ACKB’s stake is worth around €1 bn, not €550 ml. CFE owns other participations in addition to DEME (obviusly, we have to deduct the cash ACKB will spend to increase its stake in CFE according to the plan, which remain a question mark as the price today is much higher than the offer price of €45).

Am I missing something?

Sorry, just realised that the €45 offer is for part of Vinci’s stake, not fot the public, so no issue in finalising it.

Thanks for the interesting read! Personally i like Hal Holding nv, a Dutch holding company with some interesting investments, both listed and privately owned. Not so different from Ackermans.

@Hans: GBL is an interesting company to research. Research leads to Pargesa (Swiss holding company), which leads to Power Financial Corp (Canadian Holding company). Makes you wonder which company is the best investment considering tax, dividends and currency risk. Nice puzzle 🙂

Funny, Hal Holding ist the major shareholder of Boskalis Westminster, one of the main competitors of DEME, the 50% subsidiary of Ackermans & Van Haaren.

You’re right. I do like Boskalis as a company. Think i’ll take a closer look at Ackermans and Hal and see which of the two makes the best investment.

Very interesting…traditionally Belgian holding companies trade at a discount to NAV…take GBL for example (managed by Albert Frere, the richest Belgian often hailed as the European Buffett). Current NAV is 86 EUR and share price is 67 EUR (http://en.gbl.be/financial/est_value/hebdomadair/default.asp). Have you ever looked at it?

Hi hans,

im also looking at GBL at the moment.

http://en.gbl.be/Images/9_4611.pdf#1

on site 7 they show their “sum of parts” calculation with -1,4 Mrd. in bonds and -0,9 Mrd. in Bank debt.

the Consolidated balance sheet (site 17) shows

Non-current liabilities of -4 Mrd. & Current liabilities of -1,4 Mrd.

if calculated with that numbers ther is a discount of about 2€/share left.

Hi,

yes, I looked at GBL and Pargesa, but i did not reallylike the underlying stocks. Maybe its time tolook at them again….

Agree with the quality of the business / management (e.g., just look at the track record and cost-income ratio of Delen) and the overall conclusion: not cheap enough (since last fall). Think your valuation of Delen is too low; they deserve a higher multiple than Van Lanschot (by the way I liked a lot your turnaround case for the latter ;-).

Interesting to note that (1) AvH’s shareholders include U.S. value investor Third Avenue, and (2) AvH’s dividend has increased steadily year after year.

Thanks for the comment. Just for the record: I valued Delen at twice the multiple than the current Van Lanschott multiple.

mmi

Agree with the quality of the company / management (e.g., just look at the track record and cost-income ratio of Delen) and with your overall conclusion: not cheap enough (since last fall). Think your valuation of Delen is indeed too low (they deserve a higher book multiple than Van Lanschot even though I like a lot your turnaround case for the latter ;-).

Interesting to note that: (1) AvH shareholders include U.S. based value investor Third Avenue; (2) the dividend has been increasing steadily over the past years.