Updates: Energiedienst (CH0039651184) & Vossloh (DE0007667107) voluntary tender offer

Energiedienst

My first transaction this year was to sell my shares in Energiedienst.

Looking at the Swiss Francs chart, where Energiedienst has its primary listing, this looks like genius timing:

However in Euro, it looks pretty stupid:

In Euro, the shares jumped from around 25,20 EUR to around 27 EUR at the time of writing, a upmove of around 7% against a loss in Swiss Francs of around -10%.

So what happened ? Well in case you were not on a Moon mission last week you might have heard about that Swiss Franc “thing”. The Swiss Franc increased around 17% against the Euro within a very short time frame. What we can see above is relatively easy: The stock price in Swiss Franc fell, but not enough to off set the CHF/EUR movement. This is very strange, especially in the case of Energiedienst.

Energiedienst operates (based on sales) around 85% of its business in Germany and only 15% in Switzerland. So even if we assume that the business in Switzerland is not negatively affected, the increase in EUR should have been theoretically only 0,15*17%= 2,6% in EUR and not +7%.

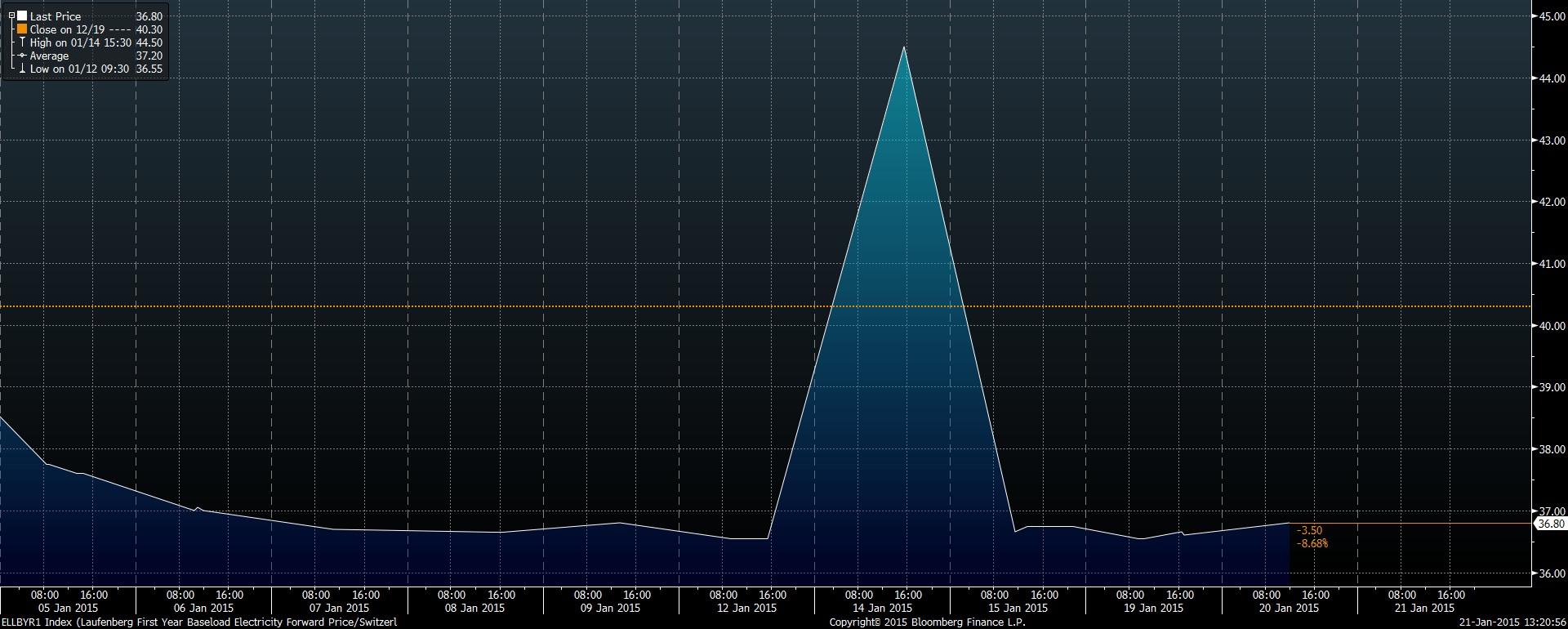

If we look at Swiss Power prices however, we see something interesting: With the exception of the one day, they directly adjusted in EUR terms as we can see here for instance in the Swiss 1 year forward electricity prices:

So in this case, electricity prices seem to be more efficient than stock prices, as there seems to be a very quick and liquid market to arbitrage away those currency differences quickly. Nevertheless I lost money by selling to early but in this case it was not my fault.

Vossloh

Back in September, I presented Vossloh as a potential fallen angel with activist involvement. This is what I wrote back then:

Based on today’s price of ~49 EUR this would mean a potential upside of 35-68%. However one should assume that this turn-around needs at least 3 years. For a turn around, I personally would require a higher return than for a normal “boring” value stock as there is clearly a risk that the turnaround does not work out as planned.

If I assume a target return of 20% p.a., i would need to be sure that the price of Vossloh is in 3 years at around 85 EUR. This is clearly at the very upper end of my target range. So I would either need to have more aggressive assumptions or I would need a lower entry price. As a value investor, I would not want to bet on growth or on a shorter time frame for the turn around, so the only alternative is to wait for a lower entry price.

Taking the midpoint of my range from above at 74, I would be a buyer at ~42 EUR per share but not before.

On November 7th, Vossloh actually hit the 42 EUR threshold but somehow I was not quick enough and passed to buy some shares. Since then the shares recovered nicely to around 54 EUR when yesterday, the following news hit the wires:

On 20 January 2015, KB Holding GmbH decided to make a voluntary public takeover offer to the shareholders of Vossloh Aktiengesellschaft, Vosslohstraße 4, 58791 Werdohl, Germany, for the acquisition of all ordinary bearer shares with no par value, each share representing a proportionate amount of EUR 2.84 in the share capital (the ‘Vossloh-Shares’).

KB Holding GmbH intends to offer the payment of a cash consideration per Vossloh-Share in the amount of the weighted average domestic stock exchange price during the last three months before the publication of this

announcement according to Sec. 10 para. 1 sent. 1 WpÜG pursuant to Sec. 5 para. 1 and 3 of the Regulation on the Content of the Offer Document, Consideration for Takeover Offers and Mandatory Offers and the Release from

the Obligation to Publish and Issue an Offer (WpÜG-Angebotsverordnung), as determined by the German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht, BaFin). This consideration is expected to be in a range between EUR 48 and 49 per Vossloh-Share and will be published immediately after being notified by BaFin.KB Holding GmbH currently holds 29.99 percent of the shares in Vossloh Aktiengesellschaft.

The stock managed to gain some more and closed at around 56 EUR per share:

So the first question is: Why does he offer 49 EUR per share if the shares are trading already at 55 EUR ?

This one is pretty easy: Thiele was already owning 29,99%. In Germany, once you cross 30%, you have to make a mandatory offer at the trailing 90 “VWAP” stock price. My guess is that Thiele clearly wants to take control, but maybe not now and not at 55 EUR. So he used the occasion to come out with this lowball offer, because this releases him from any further mandatory offers and he is not forced to take more shares than he actually wants.

After the offer has expired and Thiele has crossed 30%, he only needs to disclose purchase once he crosses 50% and even then he does not need to make a mandatory offer as the voluntary offer releases him from making any subsequent offers.

Is the stock still attractive at that level ?

Well, we know now that Thiele clearly wants to take control. But we also know that he is a very shrewed operator with little interest in minority share holders. He controls the management of the company already (he actually hired the new CEO) as he ist already the strongest shareholder.

For anyone who followed the blog and the German Corporate law discussion, the biggest issue is the following: Under current law, Thiele could decide (or his CEO) to delist from the stock exchange. This is now possible in Germany without even getting any kind of shareholder approval. This would force many funds out of the stock as normally unlisted stocks are not permitted under most fund regulations. Even for hardcore hold outs this would mean low or no transparency etc. etc.

I have seen a recent study (Solventis, “Endspiele”) that since the change in law (or the change in interpretation), on average stocks lost around -25% following the announcement of a delisting.

Overall, at the current price the risk/reward ratio is in my opinion neutral. There is some room left with regard to a fair value and mean reversion, on the other hand one should be careful with regard to any minority unfriendly actions from Thiele & Co.

As a learning experience, I should maybe watch my watchlist a little bit closer in order not to miss such opportunities as in November.

More than 4 years later, Vossloh is again (or still) at 42€, and Ennismore likes them as a kind of finished succesful reorganisation: http://www.ennismorefunds.com/documents/OEIC/Newsletters/2018/NL%20OEIC%20Apr%2018.pdf

What do you think?

Oops.

Less than 4 years, but more than 3 years later…

Hi, any secret in how you find these special situation type opportunities in Europe? For US I am using services of http://www.specialsituationinvestments.com, but for Europe.UK have not found anything. Cheers for info.

Hi MMI,

regarding Energiedienst: Almost nobody could see it coming and therefore I would not consider this a loss/failure. You stuck to your investing style and in my opinion did the right thing after your investment case didn’t work out. But I actually like the move of the swiss central bank. Maybe it’s a good chance to get some shares of nice swiss companies in the future (Novartis, Swatch, Geberit, Nestle). I’ll have to take a look at them soon.

I also think that everone has experienced missed opportunities in the past. I had some myself recently. E.g. I rememver setting a buy limit (“Abstauberlimit”) for Ross Stores last year at 45 €. Unfortunatly they only came down to 46 or so which I missed because of a longer vacation… The same goes for Gilead where I wanted to buy at 70 € at the end of the year… But in my opinion patience is one of the most important qualities an investor need to have. There are so many companies out there that good chances will present again and again…

Regards,

Markus