Again some thoughts on Banks (Low interest rates, ECB and yes, Deutsche Bank again) – Part 1

First things first: Deutsche Bank

I had a post in February last year why investing in something like Deutsche bank is maybe not a good idea. But still, as I said in February this year, I don’t think Deutsche Bank will be the next Lehman Brothers.

However the internal Memo from John Cryan is clearly not a good sign. Not the text of the memo, but the fact that he had to send out one (again). Similar to Dick Fuld back then, Cryan blames “speculators” for the stock price drop. Interestingly he didn’t say “short sellers”. Maybe this has to do with the fact that Deutsche Bank itself has around 106 different disclosed short positions on stocks according to the Bloomberg function SPOS.

The big difference to Lehman in my opinion is liquidity.and the general market environment. As a universal bank they have much better access to (guaranteed) deposits and overall the market still looks relatively stable.

So one could ask: After losing -50%, is Deutsche Bank now a good (Value) investment ? I honestly don’t know. For me, a value investment is an investment I can actually value with a “Margin of safety”.

For Deutsche Bank, I think that there are just too many moving targets in order to come up with a meaningful valuation. So yes, it could be a good gamble (especially if Erdogan bids for Deutsche) buys but in my opinion it is not a “value investment”especially for more concentrated portfolios. There is always the risk that you get diluted massively at some point in time. If you run a diversified “Graham style “portfolio of cigar buts it might be worth a punt, as the margin of safety then comes at a portfolio level through diversification. In general and I will come to that later, many current developments make life very hard for Universal banks in the EUR zone in general.

For some fun and how it was in the good old times, the video of Dick Fuld in 2008, at least John Cryan was not recorded to do something similar:

More general thoughts on banking: Low/No interest

Banks clearly do have issues with a low-interest rate environment. Low interest rates as such are not the biggest problem. I think two factors are more important:

1) Steepness of the interest rate curve

2) Credit spreads

1) Steepness of the interest rate curve

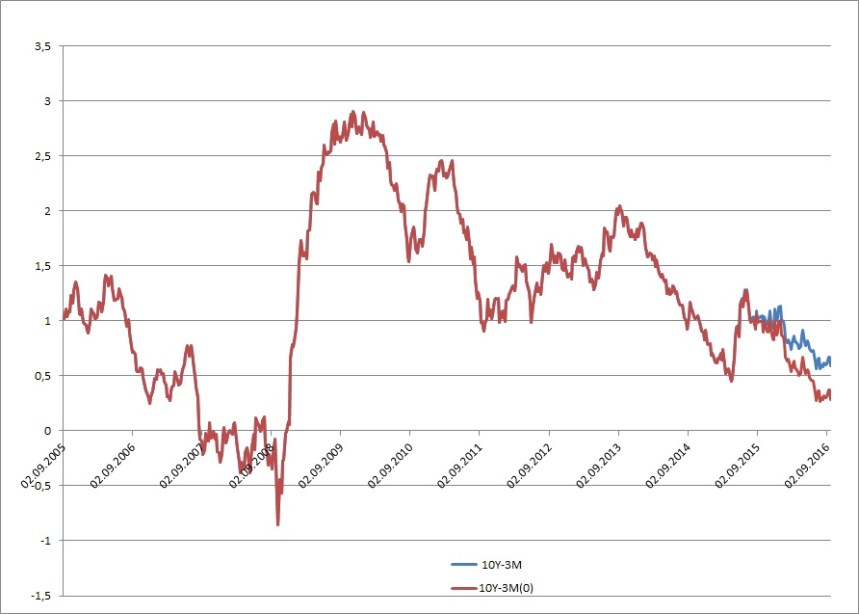

A well-managed bank does to a certain extent not care too much about the absolute level of interest rates. The major part of the “Juice” or “net interest income” actually comes from the difference between short-term deposits to long-term maturities as in principle normal banks borrow short and lend long (and do some hedging to off set the interest rate risk). I have made a quick chart which shows the interest rate difference between the 10Y Swap and the 3M Euribor as a proxy for the steepness:

The graph is actually two lines which only diverge at the end. The blue one is the “gross spread between the 10Y Swap and the 3M Euribor, the red one actually caps the 3M Euribor at 0%. This cap is relevant as for now, only very few banks have implemented negative rates for deposits and most floating rate contracts floor the base rate at zero. What we can see is that the interest rate differential is now at an extremely low point, almost similar to the level seen around the big financial crisis in 2007.

This means that for any new business, there is little to earn with maturity transformation and the old business will roll down pretty quickly.

2. Credit Spreads

The second part of the “net interest income” at banks is the credit spread they can charge on top of their own funding costs assuming similar maturities. In general, credit spreads do have some relationship to nominal rates. A 1% spread on a 10% base rate can be implemented much more easily than a 1% Spread on top of a 1% nominal interest rate, but usually this also applies to funding cost. It is now wonder that banks in high interest rate countries are much more profitable than in ultra low-interest rate countries

However, especially for European banks, there is a second (ugly) factor in play: ECB corporate bond buying.

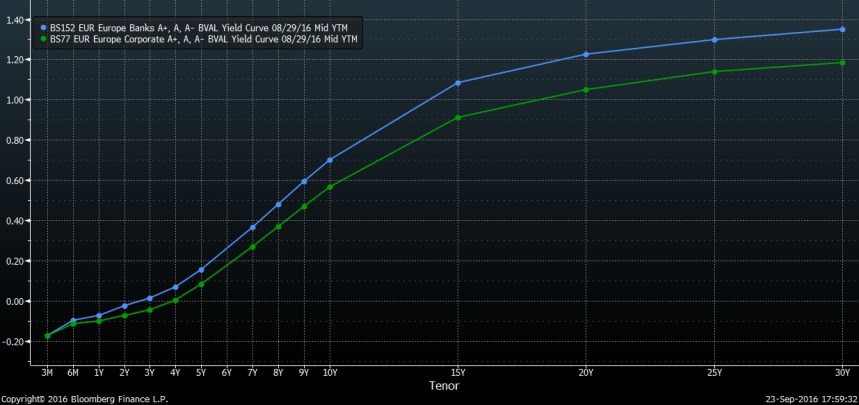

I have attached a chart which shows that there is clearly a problem:

The green line is the yield curve for single A EUR Corporate bonds, the blue line is that for single A banks. We can see that corporates get money cheaper from investors than banks, assuming the same credit quality. One can speculate why this is the case, but the fact that the ECB buys any corporate investment grade bond they can get, but do not buy any banking bonds might be the best explanation.

This is a problem, because that means that for many corporates it is clearly a no brainer to “cut out the middleman” and issue directly. Additionally, as bond spreads are usually the benchmark for any private loan transactions, this clearly lowers the spread for unlisted transactions further.

The disappearance of corporate bonds due to ECB buybacks creates another problem despite lower spreads: Those people (asset managers, insurance companies, pension funds) who used to buy corporate bonds need to buy something else. And it seems to be that the solution is to go into direct competition with banks for lending. This is from a recent Bloomberg article:

Insurers are now responsible for 11.6 percent of the loans in the global private debt market, which includes direct lending, according to data provider Preqin. Firms boosted mortgage funding by 50 percent to $430 billion in the last decade, according to the Federal Reserve.

Plus we have all the peer-to-peer companies which come from the other side (retail loans). Personally; i don’t see them as the major threat but who knows ?

The result of this is pretty easy to see. In the first 6 months of 2016 for instance, the net interest income went down -11% at Commerzbank and-8% at Deutsche Bank. Deutsche Bank looks better but taking into account that they have increased their balance sheet size by 10% and Commerzbank’s has been stable I would argue that same for same, Deutsche Bank did worse.

One should also remember that the full effect is not yet fully reflected as the “good” old business is slowly rolling down and only partially replaced by low margin new business. One could guess how much of the old book rolls down every year. My guess would be between 10-20% p.a. “replacement rate”, which would mean that based on current rates we will see dropping net interest income at least for another 3-4 years minimum.

Trading & Commission income

Back in the good old times, bank had two more structural profit streams: Trading for the own account and charging commissions on selling investment funds and insurance policies (mostly life insurance) or placing bonds for corporates.

Commissions do have a strong relationship to expected yields. You can more easily charge 5% for a mutual bond funds if interest rates are at 5% than when they are negative. There is a strong trend to low-cost index ETF which eats into the commission income. Also fees for placing bonds are going down quickly as well as sales and commissions for selling insurance.

Again, looking at the Two German banks, net fee&commision income went down -9,5% at Commerzbank and -13,5% at Deutsche,so even worse than net interest income.

In Germany, many banks try to charge fees for accounts now, but with a long history of zero cost accounts and new online competition, this is not easy.

Other issues Capital requirements (Basel IV)

Many “Normal” non-bank companies use the current low-interest rates to leverage up and buy back shares in order to boost per share income. For banks, this is much harder as regulators are still of the opinion that banks need more capital.

Just to review how the different “Basel” releases developed:

Under Basel I, banks needed to set aside capital based on very simple rules like 0% for OECD sovereigns (including Greece at that time !!!) or 8% for corporates.

Basel II the allowed banks to develop their own “internal” models. They could set their own rules for setting aside “risk based capital” (mostly based on ratings) and could assume diversification effects which in the model took away much of the risk. Implemented in the mid 2000s (2004-2006), this allowed banks to greatly increase and “leverage” their balance sheet and created the now infamous “AAA CDOs” bubble.

Basel III, the current release, did not change a lot but mostly increased capital requirements and set additional rules what accounts as capital. It alos reintroduced a cap on allowed leverage for banks.

Basel IV now seems to be a big step back if I understand correctly. The intend is to move back to some standard model, which for most banks, will increase capital requirements further as their current “Internal” model of course are tuned to show the absolute best outcome. I think the extent is not clear but it won’t be pretty.

Double whammy for European banks and only one way out: Cost cutting

So we have seen that the ECB actions make banks less profitable and that in parallel they need to raise capital. This is not a good combination and maybe the reason why the EU is strongly lobbying against Basel IV rules.

Other than normal industries, M&A consolidation is not really an option as the banks are already big enough. No one wants two big European banks to merge in order to create an uncontrollable monster.

So all that is left for banks is cost cutting. Commerzbank has just announced this week that they want to cut their 50 thousand workforce by almost 20%. This is quite necessary as their cost base was more or less unchanged which doesn’t look good if you lose revenue by 10% p.a. or more.

Personally, I do think there is a lot of cost to cut. Average salaries in banks are still significantly higher than anywhere else. But the question remains if the banks can do this quickly enough before they run out of capital.

The only good news: Lower defaults

The only thing which goes in favour for the banks is the fact that if you don’t have to pay interest on a loan, it is a lot less likely to default. So this part of the cost base goes down as well in principle. Interestingly, Commerzbank could reduce their cost for bad loans by almost -20% whereas at Deutsche, this cost increase significantly in 2016.

In any case this effect is very small compared to the revenues as the level of losses is already at an extreme low-level.

Summary:

To a certain extent, the situation that European banks are in currently is not unsimilar to Oil companies. Everyone in the oil sector is suffering from low oil prices. Nominal interest rates have a very similar effect on financial companies and especially banks like oil prices for oil companies.

Low interest rates (and flat yield curves) make it much harder to squeeze out margins. On top of that, banks have fewer opportunities than oil companies to merge or use low stock prices for value enhancing buy backs and the ECB seems to actively promote cutting banks out of the loan markets.

The P&L of the big European bank might not even fully reflect this as the good business from a few years ago is only rolling down slowly.

On top of that, a new round of increasing capital requirements is on the horizon.

Although I do not see a Lehman moment in European banking (liquidity is not a problem, the banks are rather too liquid), I don’t see the big banks as a fundamentally compelling investment opportunity.

Of course there is always the chance to gamble on short-term rebounds, but as a long-term value investor I would be very cautious especially for the big players, no matter how cheap they look based on P/B ratios.

In part 2 of this series I will have a look at how this impacts my view on my own banking investments (Handelsbanken, Lloyds, Pfandbriefbank, Citizens’s, Van Lanschot)

ICYM, Damodaran has evaluated DB stock and is a buyer at current levels:

http://aswathdamodaran.blogspot.hu/2016/10/deutsche-bank-greek-tragedy-at-german.html

Troubled banks are very difficult to evaluate, due to the balance sheet leverage. Small changes in assumptions about non-performing assets can lead to dramatic upside or downside in the stock.

Nice write up.

However, why do you think bank’s NIM is directly linked in its upper limit to a gov. long term bond yield (in this case 10 years)?

I think that the only part of banks’ lending book which is affected by the gov. long term bond yield is the one which contains securitized loans that are traded in the secondary market. That is due to the competition for investor’s money.

What’re your thoughts re. the above?

Michael

Excellent post. Indeed, with their bond buying, the ECB is now in direct competition with the banks

Great write-up, thanks. One remark:

“Although I do not see a Lehman moment in European banking (liquidity is not a problem, the banks are rather too liquid)”

I agree with you on liquidity, but as far as I can see, confidence in the business/banking system is very important. I don’t know if a confidence loss could trigger something like a Lehman moment/bank run/whatever, but this is definitely something to watch out for, especially with DB right now.

Tom

Great insights. Pity (particularly some french) banks seem among the only stocks giving a reasonable yield…

Well we will look somewhere else

Die Vermögensverwaltung und dws der deutschen müssten doch einiges an sicheren Einnahmen bringen und was wert sein. Der rest muss halt verkleinert,liquidiert und irgendwann wieder profitabel werden? Der laden gehört evtl aufgespalten?

Thank you for your great summary!

Kann es sein, dass gerade auch Lebensversicherungen in zukunft ein problem bekommen. Evtl hat ja zb eine allianz bis jetzt so gute zahlen geliefert wegen der kursgewinne bei anleihen. Nur die kurse der anleihen können ja nicht in den himmel wachsen. Ich würde sagen die kursgewinne bei anleihen haben den Gipfel erreicht.

Ja, das kann sehr gut sein.

This is a great summary. I think one way to play Deutsche is through something like this:DE000A0E5JD4

Buying shares can be bad as the bottom line performance and earning power is weak. It is better to bet on that they will not go belly up and some time it will be normalized

http://www.wsj.com/articles/the-ghost-of-lehman-brothers-haunts-deutsche-bank-1475193863