Trivago Update: From virtuous to vicuous circle in only 7 months ?

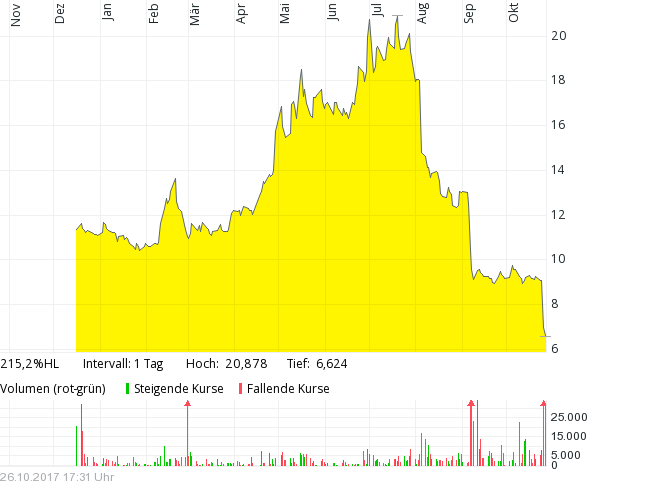

When I first reviewed Trivago in March this year, the company looked like an unstoppable growth machine, although much too expensive. Looking at the stock chart we can see that the stock almost doubled after my write-up but then lost 2/3 since its peak in July and now trades -40% against the IPO price 11 months ago:

So what happened ?

In July, Trivago came out confirming their earnings guidance 2017 with +50% in sales and increasing margins. In early September, after the stock had dropped already significantly, they came out with this warning:

Düsseldorf, Germany – September 6, 2017 – trivago N.V. (NASDAQ: TRVG), a leading global hotel search platform, today updated its annual guidance for the fiscal year 2017, based on its expectation that results for the third quarter and the remainder of the year will be softer than previously anticipated.

For the full fiscal year 2017, we now expect annual revenue growth to be around 40% and adjusted EBITDA* to be lower than in 2016 but to remain positive.

The changes to our full-year guidance are due primarily to the following two factors:

– Revenue per Qualified Referral (RPQR) related impacts:

– The anticipated negative impact on RPQR that we discussed on our second quarter 2017 earnings call has been more significant than previously expected.

– As a result of this impact, we have algorithmically pulled back our performance marketing activities more than previously anticipated, which has resulted in a further slowdown in traffic and revenue growth from those channels.

So to translate this into normal speech: We we had lower sales and then had less money to spend on advertising which in turn leads to lower sales.

Now 3rd quarter earnings came in 2 days ago. Again they are lowering guidance:

Starting towards the end of the third quarter 2017, we have seen increased testing activity on our marketplace by several large advertisers. This activity has been subsequently accompanied by changes in these advertisers’ bidding strategies and a corresponding adjustment of their cost-per-click bids on our marketplace. These developments have had a negative impact on our revenues and profitability. As a result, we have updated our guidance, and now expect total revenue to grow at a rate between 36% and 39% for 2017.

Things seem to deteriorate quite quickly and for some time. The times of rapid growth are over:

Looking to next year, we assume that these impacts will make it challenging for us to grow in the first six months of 2018 and expect to return to a positive growth trajectory in the second half of 2018. Against this background, we have seen a decline in the concentration of revenue generated by our largest advertisers during the first weeks of the fourth quarter of 2017.

So no growth in 2018 for the first 6 months and then maybe some growth later. With Trivago’s track record, this could even mean shrinking sales. So why did sales growth disappear so quickly ?

Already in September, Skift reported that online hotel giant Booking.com might pull back Metasearch spending:

The Priceline Group, which accounted for 43 percent of hotel-search site Trivago’s revenue in the first nine months of 2016 — might be pulling back on digital advertising in such hotel-metasearch platforms.

Trivago recently appears to have suffered a relative loss in advertising spend by Priceline Group-owned Booking.com, in particular.

Trivago’s share of Booking.com referral of users dropped about 23 percent across its various subdomains, according to Skift’s analysis of data from digital analytics firm SimilarWeb.

I didn’t read it at that time but the “backstory” looks interesting:

THE BACKSTORY

Earlier this month, Trivago lowered its forecast for revenue and profit for the second half of the year. Revenue dropped because of less ad spending coming from (an unnamed) one of its two main advertisers — Priceline or Expedia.

In early September, executives described the event as most likely being a one-off drop. Last winter they introduced a “relevance assessment” that had the effect of temporarily costing brands like Priceline-owned Booking.com more to get the same number of customer leads from Trivago until they could adapt to the change.

By this summer, that temporary period effectively ended for its two largest advertisers. Yet advertising spending did not rebound to the level projected based on spending patterns prior to the change.

Trivago’s recent move to prod its advertisers to spend money on user experience improvements may have irritated Priceline Group.

Priceline may have wanted to send a message to the rest of the metasearch industry not to take on moves that force Booking.com’s hand.

Trivago itself is definitely in a TV spend and branding battle with consumers in the U.S. and abroad, and new Priceline CEO Glenn Fogel may be asking himself, “Why underwrite your competitors?”

Now after the Q3 numbers Skift reported that also Expedia seems to have pulled back spending on Trivago:

Expedia’s fast-growing hotel search site Trivago may see its pace of growth stall as both Expedia and rival The Priceline Group have pulled back on spending per acquired customer. This is extraordinary given the fact that Trivago was one of Expedia’s growth engines and there was seemingly no end in sight.

This part finally brings it to the most important point:

With only two companies dominating its advertising auctions, when one downshifts its ad spending, the other doesn’t need to bid as high either — giving Trivago lower revenue and profit per customer referral. Advertisers submit cost-per-click bids in its auctions for each user click on an advertised rate for a hotel.

I think this clearly shows where the real power in online travel is at the moment: Priceline/Booking and Expedia. It looks like that the big guys now take Trivago more seriously as a competitor and start squeezing it.

Trivago’s business model has 2 clear weaknesses:

- The depend on only two companies for most of their revenues which is not good for an aggregator. Especially if they somehow agree to pay less.

- The virtuous circle more sales –> more advertising –> more sales can turn quickly into a vicious cycle less sales –> less money for advertising –> even less sales

Overall, the trivago business model doesn’t seem to create “sticky” clients which for instance Booking.com seems to do a lot better.

So is Trivago a “buy” now ?

I don’t think so. Fundamentally they need to show if their business model is really valid. There is clearly a risk that if they start shrinking and have less money to advertise, they will shrink faster and faster.

So for the time being, Trivago is off my watch list. Maybe in 9 months or so it might make sense to have another look.

Today on the FT: CMA launches investigation into hotel booking sites

Hier auf Deutsch:

“Trivago droht Sammelklage”

http://www.handelsblatt.com/unternehmen/mittelstand/britische-wettbewerbshueter-ermitteln-trivago-droht-sammelklage/20540430.html