Performance review 9M 2019 – Comment: The “Death of Value Investing” revisited

In the first 9 months of 2019, the Value & Opportunity portfolio gained 8,8% (including dividends, no taxes) against 19.4% for the Benchmark (Eurostoxx50 (Perf.Ind) (25%), Eurostoxx small 200 (25%), DAX (30%), MDAX (20%)).

Links to previous Performance reviews can be found on the Performance Page of the blog.

Some other funds that I follow have performed as follows for 9M 2019:

Partners Fund TGV: -2.25%

Profitlich/Schmidlin: +9,1%

Squad European Convictions +9,8%

Ennismore European Smaller Cos +7.5% (in EUR)

Frankfurter Aktienfonds für Stiftungen 2,3%

Evermore Global Value +13,7% (USD)

Greiff Special Situation +2% (est)

Squad Aguja Special Situation +9,8%

Paladin ONE 6,61%

Q3 2019 transactions

Q3 was not so busy. The main transaction was the Osram special situation which I obviously exited too early but still brought a decent profit. At the end of the month, the Innogy tendered shares were paid out with only a tiny profit. The upside did not materialize as the E.On stock price development was too weak. 1 day after the quarter end, also the KAS bank special situation has been paid.

The current portfolio, as always can be seen on the portfolio page. The average holding period is at 3.9 years which is inside my 3-5 year target.

Performance review:

In Q2 I wrote that being behind the benchmark by -6% is not fun. Clearly. being behind the Benchmark now more than -10% is even less fun. It doesn’t help much that most of my “peer group” did similarily bad or even worse.

Part of the underperformance is clearly self inflicted. Cars.com, for instance, which disappointed again in July/August has cost me around 3% portfolio performance and with -60% since purchase clearly qualifies for my top 10 “Hall of shame”. Another factor is clearly the more cautious positioning of my portfolio with a relatively high allocation of cash and cash-like special situations. This turned out to be a pretty bad indirect timing call on the stock market.

Aditionally, my existing portfolio didn’t include any “real winners” in that market and good new ideas were few. When I look at the 1 year top performers in the German stock market for instance, very few of them would belong to my “active” investment universe. This could be bad luck or worse, maybe some fundamental issue in my stock selection process. A partial problem is clearly that what I consider my “core competeny” is the financial services industry and there almost all of the established players do have significant structural issues and I was not able to identify the winners such as the payment players.

Comment: The “death of Value Investing” revisited

Almost 6 1/2 year ago I wrote a post called “The Death of Value Investing”. The post was based on an article by the A16Z founders Andreessen and Horowitz. The final paragraphs summarize their view quite well:

With technology upending markets, remaining a value investor is a death sentence. In the case of RIM, the company thought that their scale was defensible and stopped innovating on the operating system, favoring battery life instead. Apple’s iPhone operating system and associated software was an order of magnitude better than RIM and attracted consumers. Interestingly enough, Apple is dangerously close to losing their own software battle to Google with mobile versions of Google Maps, Gmail and Google voice being far better than their iOS counterparts.

While there may still be opportunities for value investing, you need to be cautious of businesses that appear to be on a slow decline. With the rate of technology adoption accelerating, Internet being a way of life and software consuming the world, businesses who refuse to embrace or adapt don’t just slowly decline; they fall off a cliff and take their cash flows with them.

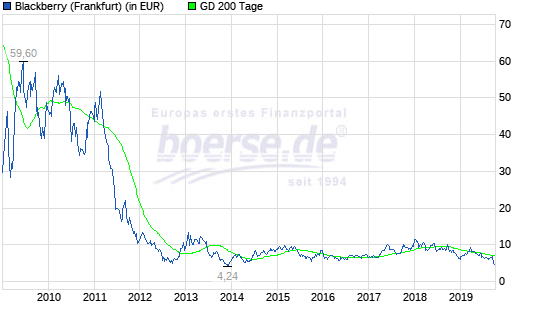

Looking at RIM/Blackberry we can clearly see that their RIM/Blackberry prediction turned out to be right (and Prem Watsa wrong, although some trading profits in between could be made)

My own conclusion was as follows:

To summarize it bluntly up to this point: If you think value investing is only about buying low P/E and/or low P/B or low P/FCF stocks, then you will most likely be in for a quite nasty surprise, especially if you invest in anything that is subject to the technological changes as described above. Many of the companies will drop off much more quickly than in the past and reversion to the mean will not happen.

Personally, it saved me from a lot of potentially bad investments. Not all of them but I managed to filter out many of the “cheap stocks” at an early stage because I always tested them against potential disruption.

One of the big issues I have with the “vakue investing is dead” topic is that value investing is often considered to be only cheap P/B (or P/E) stock investing. The US “Value indices” are mostly created on a Price to book ratio and when these stocks perfom badly, value investing as such is punished in the media.

I have mentioned this before: For me, “value Investing” is not buying “optically” cheap stocks but fundamentally cheap stocks.

Benjamin Graham’s “Intelligent Investor” is a very good book but especially investing beginners in my opinion draw the wrong conclusions. “Below book value” investing is a very easy concept because it allows you to quickly calculate a “discount” and who doesn’t like “dicsounts” ? It sounds like an “easy hack” to find undervalued shares but as we have seen now for almost a decade, it isn’t.

In my opinion, the reason for the underperformance of “low P/B” shares is relatively simple and the result of several strong fundamental changes happening at the same time such as:

- (mobile) internet

- permanently low interest rates

- Environment driven changes in energy policy / renewables

- Electric cars

- electronic payments

These strong changes effect almost any company, some more some less. The major implication of all this in my opinion stays the same:

The old “Value hacks” i.e. using P/B and P/E as selection criteria do not work very well in this environment. On the other hand, fundamentally cheap stocks do not necessary have to be optically cheap stock. Take Microsoft for instance. This is a stock which I considered for some time to invest in. This stock was fundemantelly extremely cheap for some time but optically still expensive, as the company for instance fully expenses R&D with the result that “book Value” is signifcantly understated. I never pulled the trigger but some very good “value investors” that I know invested and could reap the benefits of a fundamentally cheap stock.

To cut a long story short: I do believe that “statsistical Value investing” has become really difficult. However, sound “fundamental value invsting” is anything but dead but clearly much more difficult than just searchin “cheap” stocks with a screening tool.

“it’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price” After dabbling 10 years semi-professionally in the stock market I have come to agree with Munger (or Chris Mayer for that matter). Buy excellent companies at fair price and then let compounding do the work for you.

We should very much reflect how skilled we are in the game. It’s indeed painful to see oneself below the benchmark. The problem is when everyone else we play along is also below the benchmark. This should raise fundamental questions, and if we don’t face this issue we are making a big mistake of omission.

TRUE.

Spot On.

Wait, what?

Don’t be so frustrated MMI !

It could always go worse !!

Just see “your friends” of TGV partners fund (of which hopefully you don’t take any advice).

They really have a point to be frustrated.

Don’t be that harsh with TGV Partners Fund !!!

Don’t worry, they are doing fine as do I as investor.

Good Post. Myself I crashed with Schäffler: -55% ! 😦 !!

I would add that traditional Finance Business (and specially banks for now, maybe insurers next?) are exposed to lots of value destruction by tech, and big uncertainty (which even makes the picture worse by increasing risk premia and cost of capital).

Smart play would be not only identifying fundamental value creation, but also the simultaneous value destruction implied. This would provide a double edge (though at an increased risk). Voilà my innovative contribution ! 🙂