All German Shares part 16 (Nr. 301-325)

At the moment I can keep the weekly frequency for this series. This time, the random generator only included 2 stocks that in my opinion are worth “watching” but some of the stocks covered have interesting histories.

301. Lotto24 AG

Lotto24 is providing online access to Germany’s state lottery. With a market cap of 353 mn, investors get a run rate of 5mn Profit. The high market cap is mostly a result of a successful take-over event of Zeal Group, which now seems to own 93% of the shares. a “pass” for me.

302. WCM Beteiligungs- und Grundbesitz Aktiengesellschaft

WCM is a company with an interesting past. The vehicle of German Billionaire Karl Ehlerding was one of the high flyers of the Dotcom Boom and even tried to acquire Commerzbank. The company went bankrupt in 2006 but recently reemerged as a real estate company. WCM is now majority owned by another listed real estate company, TLG and currently has a market cap of 700 mn. As all the other real estate companies, this one is a “pass”.

303. HOMAG AG

HOMAG is a 618 mn market cap machinery company that specializes in machinery for wood processing (i.e. furniture industry, etc.). HOMAg is majority owned (64%) by also listed Duerr AG. Duerr has established a “Profit and Loss transfer agreement” with HOMAG which means that HOMAG shareholders are only entitled to a guaranteed dividendd dividend of 1,03 EUR per share. Economically, the share is therefore a bond.

I find it therefore super strange how the HOMAG share has moved over the last few years:

In theory, HOMAG would be an attractive position for a bond portfolio as a perpetual bond with a 2,5% yield, however as I am not in the bond business, I’ll “pass”.

304. Cash Medien AG

Cash Medien publishes a few investment magazines and has a market cap of 5.8 mn EUR. The company is shrinking as many print publishers. “Pass”

305. Fielmann AG

Fielmann is one of the stocks where I could always hit myself not to have invested despite being a loyal client for a long time. Fielmann with a market cap of ~6 bn is one of the typical family owned and run “hidden champions” dominating the German market for prescription glasses. Fielmann has been a great long term compounder, increasing over 10x over the last 15 years:

These days however, the company trades at an P/E of around 35 and grows only very little (Profit growth ~5%) which in my opinion does not leave a lot of upside for shareholders at current prices. As a quality stock it will however still go on my “watch” list.

306. Global Oil & Gas AG

Big name, little market cap: 1.2 mn. “pass”

307. Formycon AG

321 mn EUR market cap pharmaceutical company specializing in “biosimilars”. In the first 6 months of 2019, sales have gone down by ~-1/3 and the company has made a loss. Not sure what justifies the market cap, most likely a lot of hope. “pass”.

308. Ultrasonic AG

For some reasons still listed remainder of a Chinese fraud. “pass”.

309. Böwe Systec AG

Another listed bankrupt shell company. “Pass”.

310. H&R GmbH &Co KGaA

A 195 mn market cap chemical company which seems to be in a deep slump. The company trades at ~0.5 x book value, but has a bad reputation from a governance perspective. Maybe a deep value opportunity for specialists, but for me it is a “pass”.

311. Alba SE (ex Interseroh)

Alba is a Berlin based, 590 mn market cap company active in waste management and recycling. The stock is 93% majority owned by the holding of the Alba Group and has a “profit & loss transfer agreement” in place. This means a guaranteed gross dividend of ~4 EUR per year which at forst sight looks attractive. However the whole Alba Group has very shaky finances and this explains the relatively low share price of this sub. “Pass”.

312. PVA Tepla AG

PVA Tepla is a 338 mn EUR market cap technology company that delivers mainly equipment to the semiconductor industry. The company is currently enjoying significant growth (+40%) although order entry grows a lot less and Q3 is already flat yoy. The company seems to tarde at around 30-40x 2019 earnings and with EBIT margins of 9% I don’t really understand why. “Pass”.

313. Interstahl Handels AG

A 1.5 mn market cap company that changes its name frequently. “pass”.

314. Backbone Technology AG

Another name changing company with a 5 mn market cap and some “technology assets”. “Pass”.

315. Aktienbrauerei Kaufbeuren AG

23 mn market cap brewery from southern Bavaria. The brewery seems to be loss making, but the listed company only holds a 45% minority stake and is focusing on….Real Estate of course. From the outside, it doesn’t look that promising and is maybe mostly interesting for locals. “Pass”.

316. Paion AG

Another “Biopharmaceutical” company worth 160 mn EUR. The company is burning money since a long time. I have no idea if their pipeline is any good, so “Pass”.

317. Publity AG

One of the many companies riding the real estate wave in Germany. With a 540 mn EUR market cap already a significant player but with a very volatile development in the past months. For me, as in the other cases, a “pass”.

318. Janosch Film & Medien AG

Janosch is a 6 mn market cap media company that shows an incredible performance in the past years:

Over the last 10 years, the stock went up around 20x. Operationally, the company has indeed improved and on top of licensing the famous Janosch Children comics, the company seems to plan to open child care centers. For the time being, I’ll keep them on “watch”.

319. Munich Brand Hub AG

Munich Brands Hub is a 0.2 mn nano cap who does something with brands but not very successful. “pass”.

320. ABO Invest AG

ABO Invest is a 93 mn market cap company that itself invests into wind parks. The company is signifcantly leveraged (~90% LTV) and therefore a clear “pass” for me.

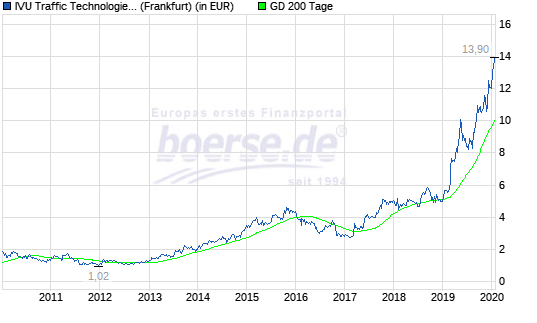

321. IVU Traffic AG

IVU Traffic is a 233 mn market cap software company that specializes as the name indicates on public transport solutions. As many software companies, the stock enjoyed a decent upwards move in the recent months:

Operationally it is not clear at first sight what exactly has driven this, as Q3 2019 looks a lot weeker than Q3 2018. The company estimates 9 mn EBIT for 2019 which means an EV/EBIT of >20 for a company that is depending on a few large projects. “pass”.

322. Deutsche Cannabis

A 5 mn market cap “PE company for Hemp products”. A little bit behind on the hype curve, “pass”.

323. Black Pearl Digital AG

A 1.2 mn nano cap with frequent name changes, now focusing on “Blockchain”. Pass.

324. Datron AG

Datron is a 46 mn EUR market cap machinery company, which has been IPOed in 2011 and is now trading at the same level as back then. The company i majority owned by the founding family and specializes in milling machines.

The first half year 2019 has been disappointing. Overall the company looks conservatively run but somehow vulnerable to macro issues. “pass”.

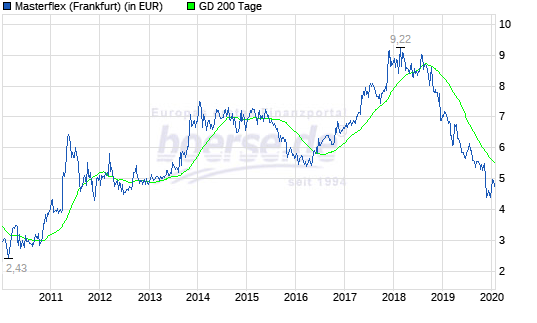

325. Masterflex SE

Masterflex is a 44mn EUR market cap company active in specialty plastics, more precisely plastic tubes/hoses for industrial use.

In 2019, Masterflex announced on 8.11. Q3 numbers and stated that they are “On track” to reach their goals, only to be followed by a profit warning 2 weeks later. The stock is already on a downtrend since the beginning of 2018:

Already in 2018, profitability declined and also in 2018 they came out with a late profit warning, so visibility seems to be an issue. “pass”.

Am Ende ist aber wie immer entscheidend was hinten raus kommt. Im Fall von IVU ist der Rohertrag schlicht der Umsatz, dass man die Hardware Umsätze auf die eigenen Bücher nimmt hat historische Gründe. Ich hätte es gelassen, weil es verwirrt Letztlich hat IVU 2019 über 60 Mil. Umsatz und 10 Mill. Ebit erzielt. Wächst organisch definitiv zweistellig und hat noch ein Großteil des Geschäftsmodell immanente Skalierungspotential vor sich. IVU hat als Marktführer in einem (Recht großen) Nischenmarkt einen großen Moat und dürfte mittelfristig Margen wie andere Nischensoftwaremarktführer erreichen. Gibt für mich jedenfalls keinen ersichtlichen Grund, warum dies nicht passieren sollte. Aber ich bin immer dankbar für kritischen Input!

I have received a very good comment on Formycon via Email which I hereby reporduce:

Formycon is basically a contract developer for generics, but the complex molecule type (produced using bacteria cultures rather than pure chemistry). They have a fairly low development risk, i.e. I expect that most products they develop will also make it to market, albeit sometimes after a lengthy approval process and modest cost overruns. The Strüngmann brothers have funded the first projects in exchange for basically 90% of product revenue. Formycon will try to expand its own economics by plugging its own 10% from early projects (and money from capital increases) into the next projects. The team is excellent, but shareholders buying at the current price have a much much worse deal than the Strüngmann brothers. They paid EUR 100m to get 90% of the upside on one product, maybe another EUR 100m for another. We pay EUR 270m at present for 10% of the upside. Product revenue could be fairly low given expected competition from heavyweights such as Samsung Pharma. Not a good deal at the current market cap. But worth keeping on watchlist around EUR 18 or thereabouts.

Sehr lesenswerte Serie – warum filtern Sie nicht Microcaps und bestimmte Industrien raus?

Danke. Einfach weil ich alle Aktien ohne Ausnhame einmal durchgehen will. Vielleicht ist ja doch die eine Perle bei den Nanocaps dabei ? Janosch ist z.B. nicht völlig uninteressant.

I have been following Masterflex for years now but had to give up.

Their business seems promising and should be reasonably profitable.

For some reason they always seem to be unlucky and have to postpone a bright future.

Even their optimistic guidance is a barely double digit EBIT-margin – which seems low.

By now I think there needs to be a new set of eyes steering that ship.

Die Einschätzung von IVU würde ich nochmal überdenken. Gegenwärtig die interessanteste Softwareaktie in Deutschland. Sind sind mit Abstand Marktführer bei Betriebssystemen für den europäischen Bahnverkehr, der selbst vor einer Digitalisierungswelle steht. Zudem ist es falsch, dass sie von Großprojekten abhängig sind. War noch nie der Fall. Sie sind organisch die letzten Jahre immer um 6-8% gewachsen. Das Ebit wird 2019 über 10 Mill EUR liegen und Dank Skalierung bis 2021 auf ca. 20 Mill. steigen. Ich persönlich kenne keine Softwareaktie mit einem EV/Ebit von unter 10 für 2021.

Warum liegt die Brutto-/EBIT-Marge bei nur 70% bzw. 6-7% in all den Jahren? Erscheint niedrig fuer ein Software Unternehmen. Danke

Hier muss man nur auf den Rohertrag schauen. Der spiegelt IVU Softwareleistung wieder. Der Rest ist Fremdhardware (Bordrechner usw) und stellt nur einen Durchlaufposten dar. Gemessen am Rohertrag kommt IVU in diesem Jahr auf eine Ebitmarge von 18%. Diese dürfte bis 2021 auf ca. 22% skalieren.

Bei einer EBIT Marge die auf den Rohertrag gerechnet wird, schauen plötzlich ganz schön viele Geschäftsmodelle attraktiv aus….