All German Shares part 32 – Nr. 701-725

And another 25 (more or less) randomly selected German stocks. This time, only 3 stocks made it onto my preliminary watch list.

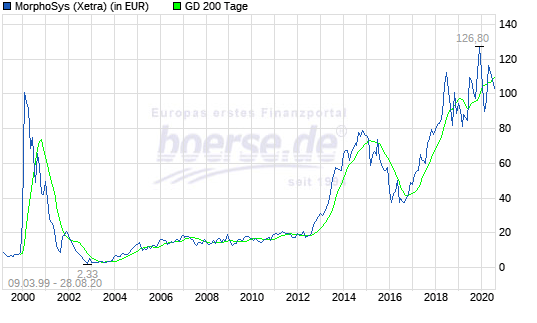

701. Morphosys AG

Morphosys is a 3.4 bn EUR biopharmaceutical company that belongs to the “old school” biotechs. Looking at the chart, it took them 2000 year to get back to the level where the first boom in the late 90s pushed them:

Morphosys does actually have revenues, something like 280 mn in the first 6M of 2020, but that seems to be due to a big one-off in Q1 as they have been successfully licensing one of their products to a US company. Q2 was already (again) negative. Morphosys would be a good starting point to learn more about the sector, but I am not sure if I have ever time for this. Nevertheless I’ll put them on “watch”.

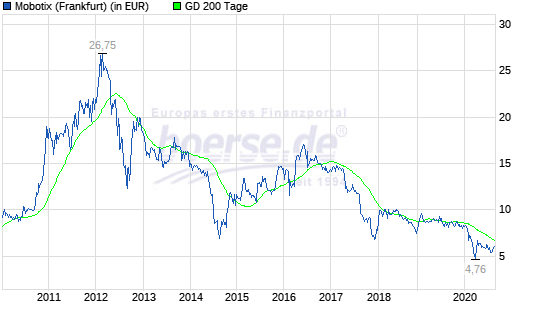

702. Mobotix AG

Mobotix is a 84 mn EUR specialist in video surveilance technology. The stock was “hot” some years ago, but is since then on a long decline:

Morphosys does actually have revenues, something like 280 mn in the first 6M of 2020, but that seems to be due to a big one-off in Q1 as they have been successfully licensing one of their products to a US company. Q2 was already (again) negative. Morphosys would be a good starting point to learn more about the sector, but I am not sure if I have ever time for this. Nevertheless I’ll put them on “watch”.

702. Mobotix AG

Mobotix is a 84 mn EUR specialist in video surveilance technology. The stock was “hot” some years ago, but is since then on a long decline:

A quick look into the latest 6M report shows that sales are declining and the company capitalized costs to stabilze returns. Without htis they would be already loss making pre Covid. Nothing to see, “pass”.

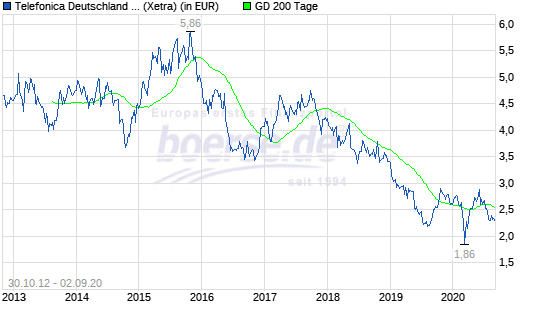

703. Telefonica Deutschland AG

Telefonica Deutschland is the stock listed German subsidiary of Telefonica (69% ownership) with a markt cap of 7 bn EUR. The company runs the third German mobile network under the brand O2 and is famous for having the worst quality.

The stock has seen clearly better days:

A quick look into the latest 6M report shows that sales are declining and the company capitalized costs to stabilze returns. Without htis they would be already loss making pre Covid. Nothing to see, “pass”.

703. Telefonica Deutschland AG

Telefonica Deutschland is the stock listed German subsidiary of Telefonica (69% ownership) with a markt cap of 7 bn EUR. The company runs the third German mobile network under the brand O2 and is famous for having the worst quality.

The stock has seen clearly better days:

The company pays relatively high dividends to its mothership in Spain, Topline has been more or less flat, GAAP results are negative due to depreciation. Debt has been increasing in 2020 as they seem to have issues actually earning their dividend payment. I don’t see anything that really interests me, therefore “pass”.

704. Capsensixx AG

Capsensixx is a 42 mn EUR market cap company that is part of the PEH Wertpapier Group which owns 81% of the company. Capsenixx owns 50,01% of Axxion, Axxion, a “private label” fund boutique itself seems to be stagnating/shrinking. After minorities, earnings fro shareholders are limited. The share price doubled from its low in April, but I do not understand why. “Pass”.

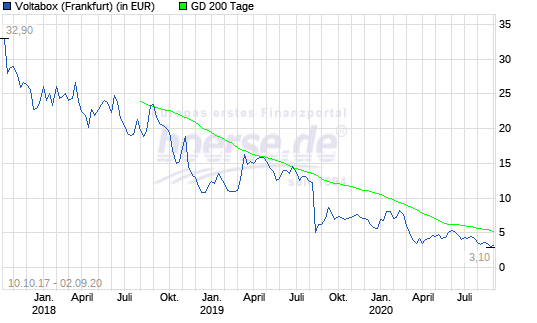

705. Voltabox AG

Voltabox, a 53 mn EUR market cap company, should be in theory a red hot stock: They are manufacturing batteries for special purpose vehicles. The stock price however since its IPO in late 2017 knows only one direction: down

The company pays relatively high dividends to its mothership in Spain, Topline has been more or less flat, GAAP results are negative due to depreciation. Debt has been increasing in 2020 as they seem to have issues actually earning their dividend payment. I don’t see anything that really interests me, therefore “pass”.

704. Capsensixx AG

Capsensixx is a 42 mn EUR market cap company that is part of the PEH Wertpapier Group which owns 81% of the company. Capsenixx owns 50,01% of Axxion, Axxion, a “private label” fund boutique itself seems to be stagnating/shrinking. After minorities, earnings fro shareholders are limited. The share price doubled from its low in April, but I do not understand why. “Pass”.

705. Voltabox AG

Voltabox, a 53 mn EUR market cap company, should be in theory a red hot stock: They are manufacturing batteries for special purpose vehicles. The stock price however since its IPO in late 2017 knows only one direction: down

The company seems to have struggled before Covid-19 but seems to use this as an excuse now to justify a huge write down. “Pass”.

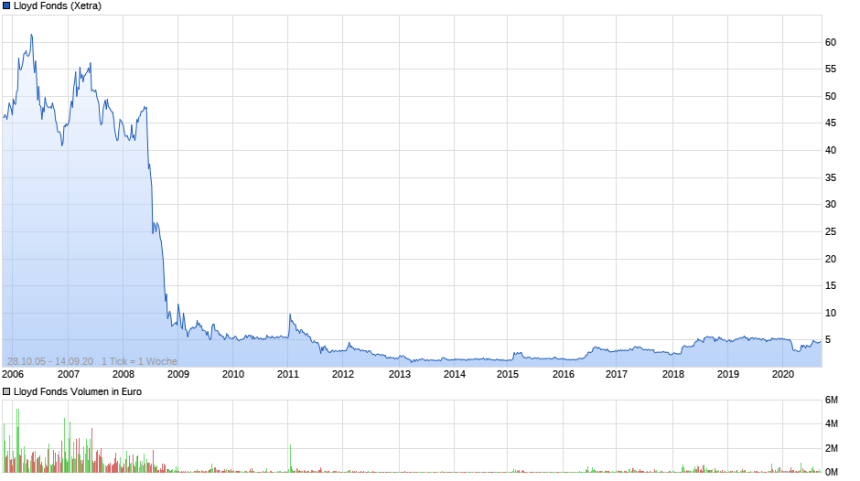

706. Lloyd Fonds AG

Lloyd Fonds is a 62 mn EUR market cap asset manager that was every successful until the GFC with selling participations in ships. As we can see in the chart, the GFC almost killed the company and it only came back very slowly:

The company seems to have struggled before Covid-19 but seems to use this as an excuse now to justify a huge write down. “Pass”.

706. Lloyd Fonds AG

Lloyd Fonds is a 62 mn EUR market cap asset manager that was every successful until the GFC with selling participations in ships. As we can see in the chart, the GFC almost killed the company and it only came back very slowly:

As the company didn’t disclose some risks in its prospectuses, the company was sued by investors over the last several years and the courts said that the company needs to compensate investors at least in one case. The company now seems to reinvent itself as a kind of “private client wealth manager”. Top line has been growing in 2020 but that seems to be driven by an acquisition. The company showed a loss in the first 6M and their still seems to be a significant risk of further compensation payments. “Pass”.

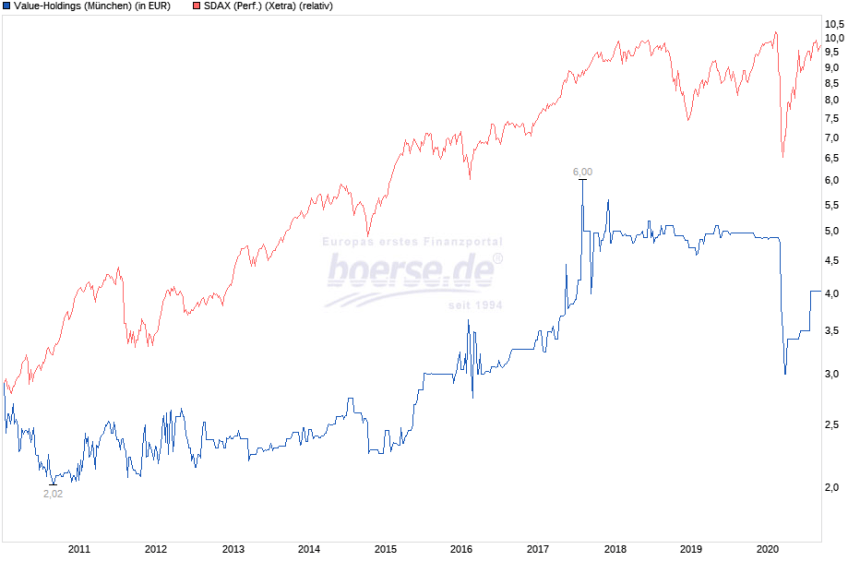

707. Value Holdings AG

Value Holdings AG is a 7,5 mn EUR market cap company that according to its homepage is both an Asset Manager and a holding company for listed stock investments. The company is mostly doing “old school” value investments in German small caps. The performance of the stock compared to the SDAX is however very weak as we can see in the chart;

As the company didn’t disclose some risks in its prospectuses, the company was sued by investors over the last several years and the courts said that the company needs to compensate investors at least in one case. The company now seems to reinvent itself as a kind of “private client wealth manager”. Top line has been growing in 2020 but that seems to be driven by an acquisition. The company showed a loss in the first 6M and their still seems to be a significant risk of further compensation payments. “Pass”.

707. Value Holdings AG

Value Holdings AG is a 7,5 mn EUR market cap company that according to its homepage is both an Asset Manager and a holding company for listed stock investments. The company is mostly doing “old school” value investments in German small caps. The performance of the stock compared to the SDAX is however very weak as we can see in the chart;

Nothing to see here, “pass”.

708. InCity Immobilien AG

InCity is a 89 mn EUR market cap real estate company with a relatively unclear foucs. The company is loss making and I couldn’t see anything there that interests me. “pass”.

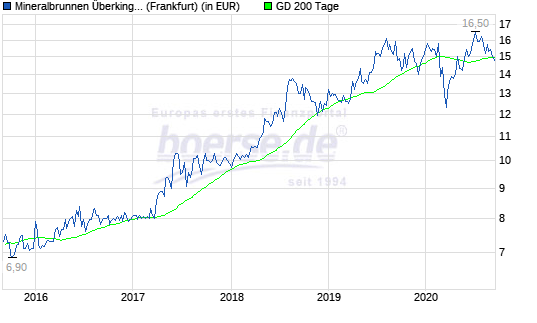

709. Mineralbrunnen Überkingen-Teinach AG

Mineralbrunnen Überkingen is a 121 mn EUR market cap beverage company that sells mostly sparkling mineral water. The company has a mixed past but it seems that until 2020, they made good progress over the last few years. The first 6M 2020 saw top line decreasing by -20%, which means that they seem to rely on restaurants and bars to a certain amount. Interestingly, the share price of the more liquid pref shares is pretty much back to pre covid-19 levels:

Nothing to see here, “pass”.

708. InCity Immobilien AG

InCity is a 89 mn EUR market cap real estate company with a relatively unclear foucs. The company is loss making and I couldn’t see anything there that interests me. “pass”.

709. Mineralbrunnen Überkingen-Teinach AG

Mineralbrunnen Überkingen is a 121 mn EUR market cap beverage company that sells mostly sparkling mineral water. The company has a mixed past but it seems that until 2020, they made good progress over the last few years. The first 6M 2020 saw top line decreasing by -20%, which means that they seem to rely on restaurants and bars to a certain amount. Interestingly, the share price of the more liquid pref shares is pretty much back to pre covid-19 levels:

The company has a 70% majority owner with unknown plans, but I found the stock interesting, so it will go on “watch”.

710. Securize IT Solution AG

Securize is a 2,2 mn EUR market cap company that just changed its name and wants to become a “Cloud powerhouse”. “Pass”.

711. Investunity AG

Investunity is a 0,7 mn EUR market cap shell company somehow associated with Dt. Balaton. “Pass”.

712. UET United Electronic Technology AG (ehemals CFC Industriebeteiligungen AG)

UET is a 13 mn EUR market cap company that own a few Telco related businesses. Reporting is super slow (no half year report yet as of Mid Spetmeber) and numbers are unimpressive. “Pass”.

713. Tonkens Agrar AG

Tonkens is a 7 mn EUR market cap agricultural stock, The stock looks cheap, however one can see a long downtrend, the company employs significant debt and results are volatile. “pass”.

714. Jost AG

Jost AG (not related to Jost Werke AG) is a 3 mn EUR market cap company that somehow is active in the tax advisory area. The stock price has been doing nothing for the last 10 years and there doesn’t see anything remarkable that this wil change. “pass”.

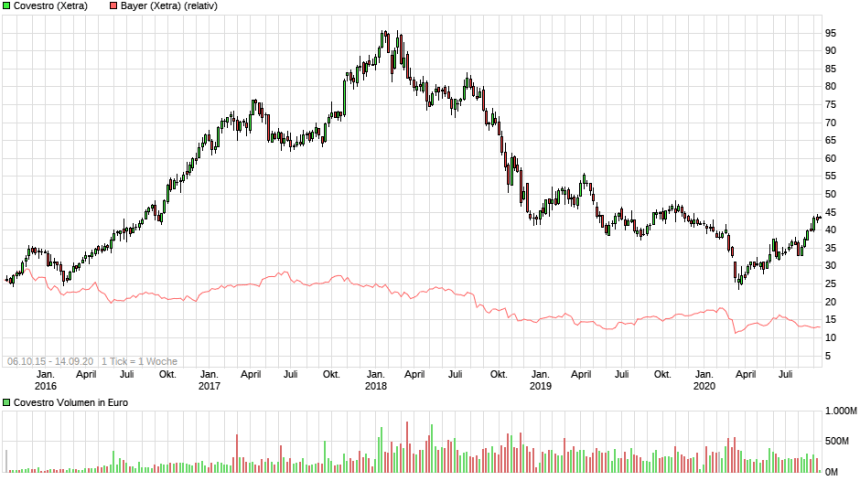

715. Covestro AG

Covestro AG is a 8 bn EUR chemicals company which is a spin out/IPO from its old parent Bayer AG which owns a remaining stake of ~7%.

Ironically, since its spin-out, Coverstr has done a lot better than “mothership” Bayer, despite the fact that the stock only trades at around 50% of its peak in 2018:

The company has a 70% majority owner with unknown plans, but I found the stock interesting, so it will go on “watch”.

710. Securize IT Solution AG

Securize is a 2,2 mn EUR market cap company that just changed its name and wants to become a “Cloud powerhouse”. “Pass”.

711. Investunity AG

Investunity is a 0,7 mn EUR market cap shell company somehow associated with Dt. Balaton. “Pass”.

712. UET United Electronic Technology AG (ehemals CFC Industriebeteiligungen AG)

UET is a 13 mn EUR market cap company that own a few Telco related businesses. Reporting is super slow (no half year report yet as of Mid Spetmeber) and numbers are unimpressive. “Pass”.

713. Tonkens Agrar AG

Tonkens is a 7 mn EUR market cap agricultural stock, The stock looks cheap, however one can see a long downtrend, the company employs significant debt and results are volatile. “pass”.

714. Jost AG

Jost AG (not related to Jost Werke AG) is a 3 mn EUR market cap company that somehow is active in the tax advisory area. The stock price has been doing nothing for the last 10 years and there doesn’t see anything remarkable that this wil change. “pass”.

715. Covestro AG

Covestro AG is a 8 bn EUR chemicals company which is a spin out/IPO from its old parent Bayer AG which owns a remaining stake of ~7%.

Ironically, since its spin-out, Coverstr has done a lot better than “mothership” Bayer, despite the fact that the stock only trades at around 50% of its peak in 2018:

The stock has recovered the Covid-19 crash already. I do not know a lot about their business but it seems to be volatile and somehow related to the oil price. 2019 was a difficult year, with profit down -70% yoy.

Cyclical stocks should usually be bought when their P/E is high, so now might not be a bad time to do so, but for me it is a “pass”.

716. Teles AG

Teles AG is a 5 mn EUR “Dot.com area” star that has not achieved anything since then. The company is majority owned and operationally not doing well. In 2019 they created significant profits from some related party financing actions. All in all nothing to see, “pass”.

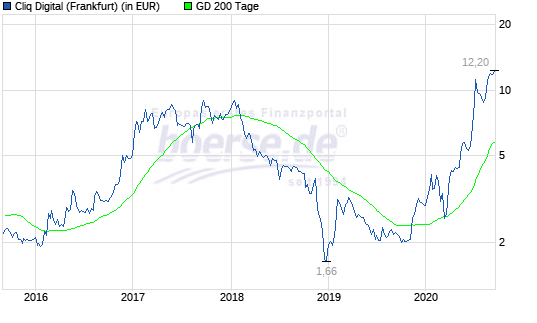

717. Cliq Digital AG

Cliq Digital is a 76 mn EUR market cap company that has seen its share price sky rocketing since the Covid-19 crisis:

The stock has recovered the Covid-19 crash already. I do not know a lot about their business but it seems to be volatile and somehow related to the oil price. 2019 was a difficult year, with profit down -70% yoy.

Cyclical stocks should usually be bought when their P/E is high, so now might not be a bad time to do so, but for me it is a “pass”.

716. Teles AG

Teles AG is a 5 mn EUR “Dot.com area” star that has not achieved anything since then. The company is majority owned and operationally not doing well. In 2019 they created significant profits from some related party financing actions. All in all nothing to see, “pass”.

717. Cliq Digital AG

Cliq Digital is a 76 mn EUR market cap company that has seen its share price sky rocketing since the Covid-19 crisis:

From what I understand, the company offers some second rate streaming offers (Movies, sports, music) which it sells predominantly to mobile users. For some strange reasons they are especially successful in North America, where slaes in the first 6M 2020 went up 6x yoy. What I find even more strange is the fact that they don’t use the net income after minorities for the EPS calculation but some other random number which is twice as high. All in all i find the company quite strange and I also don’t like the look of the management board (sorry, I still use my “face detector). “Pass”.

718. Heroes AG

A 7,5 mn EUR market cap stock with frequent name changes. Currently some kind of Sports right digital something company. “pass”.

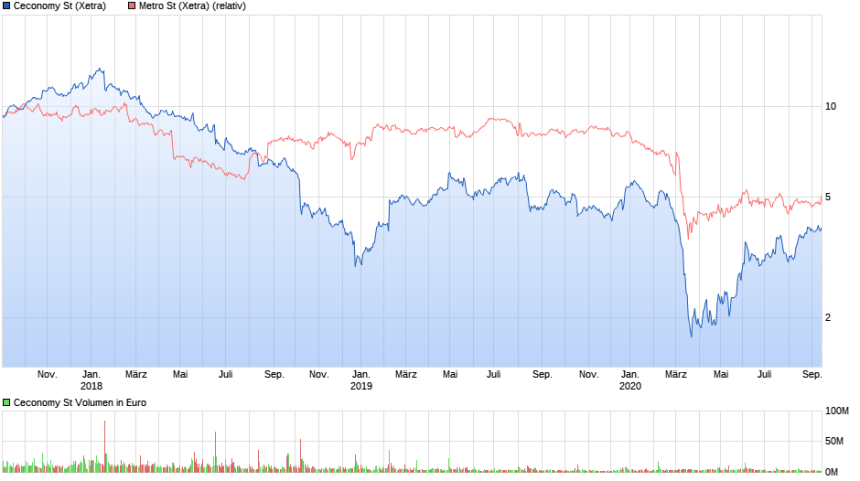

719. Ceconomy AG

Ceconomy is a 1,4 bn EUR market cap company that was spun-off from Metro in 2017. Initially I thought that Ceconomy (Media Markt and Saturn) was the bad part before realizing that there are no really good parts.

The company is a electronics retailer who is struggling among other things with Amazon and a unfortunate shareholder structure, which gives the family of the founder a blocking minority.

The Covid-19 induced boom of buying stuff for the home office helped them a little bit, doubling the stock price form their low:

From what I understand, the company offers some second rate streaming offers (Movies, sports, music) which it sells predominantly to mobile users. For some strange reasons they are especially successful in North America, where slaes in the first 6M 2020 went up 6x yoy. What I find even more strange is the fact that they don’t use the net income after minorities for the EPS calculation but some other random number which is twice as high. All in all i find the company quite strange and I also don’t like the look of the management board (sorry, I still use my “face detector). “Pass”.

718. Heroes AG

A 7,5 mn EUR market cap stock with frequent name changes. Currently some kind of Sports right digital something company. “pass”.

719. Ceconomy AG

Ceconomy is a 1,4 bn EUR market cap company that was spun-off from Metro in 2017. Initially I thought that Ceconomy (Media Markt and Saturn) was the bad part before realizing that there are no really good parts.

The company is a electronics retailer who is struggling among other things with Amazon and a unfortunate shareholder structure, which gives the family of the founder a blocking minority.

The Covid-19 induced boom of buying stuff for the home office helped them a little bit, doubling the stock price form their low:

Nevrtheless, their legacy store network with a lot of large mall sores will hurt them for some time and it will really be ahrd to turn this company around. Nothing to see for me, “Pass”.

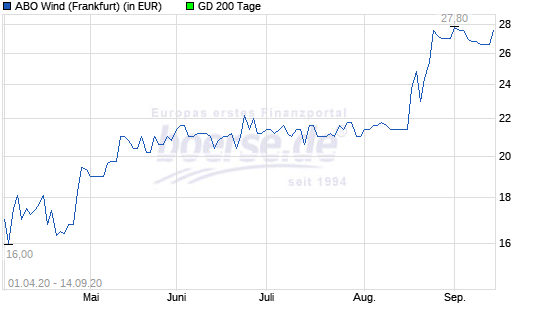

720. ABO Wind AG

ABO WInd is a 225 mn EUR renewable energy / wind farm company that listed in March 2020, just when Covid-19 really kicked in. As we can see in the chart, Covid-19 did not hurt the stock:

Nevrtheless, their legacy store network with a lot of large mall sores will hurt them for some time and it will really be ahrd to turn this company around. Nothing to see for me, “Pass”.

720. ABO Wind AG

ABO WInd is a 225 mn EUR renewable energy / wind farm company that listed in March 2020, just when Covid-19 really kicked in. As we can see in the chart, Covid-19 did not hurt the stock:

The founders still hold >50%, 10% of the capital is held by utility Mainova. ABO plans, develops and sells wind- and solar mostly in Europe. For the first 6 months, ABO could grow nicley and expects around 11 mn in profits for 2020, resulting in a PE of ~20. Perosnally, I do not like these kind of project companies that much. However, as the sector as such is interesting, I put them onto the “watch” list.

721. RM Rheiner Management AG

Rheiner is a repurposed company shell taht used to be a bankrupt textile company but is now a 7 mn EUR market cap investment company, specializing in squeeze out speculations within the German stock market. The company is part of the “Scherzer family”. For me, this is not really interesting, therefore “pass”.

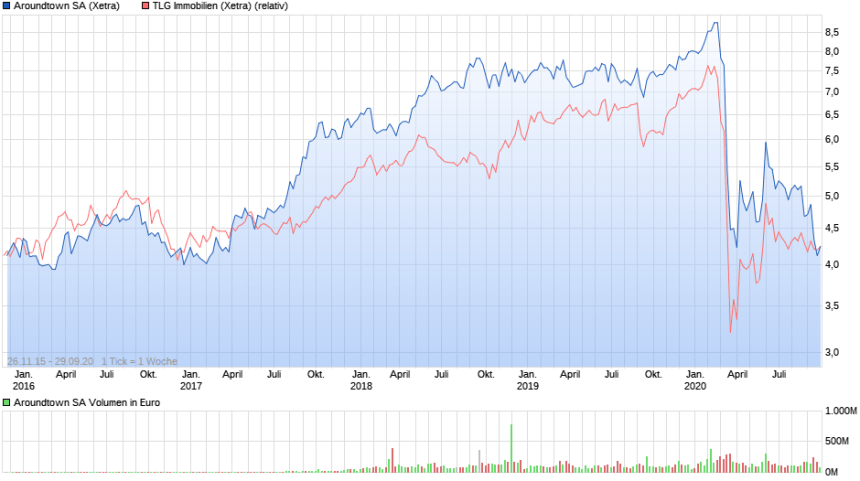

722. TLG Immobilien AG

TLG is a 2 bn market cap real estate company that has been taken over by competitor Aroundtown. Both stocks have been hammered due to Covid-19 as we can see in the chart.

The founders still hold >50%, 10% of the capital is held by utility Mainova. ABO plans, develops and sells wind- and solar mostly in Europe. For the first 6 months, ABO could grow nicley and expects around 11 mn in profits for 2020, resulting in a PE of ~20. Perosnally, I do not like these kind of project companies that much. However, as the sector as such is interesting, I put them onto the “watch” list.

721. RM Rheiner Management AG

Rheiner is a repurposed company shell taht used to be a bankrupt textile company but is now a 7 mn EUR market cap investment company, specializing in squeeze out speculations within the German stock market. The company is part of the “Scherzer family”. For me, this is not really interesting, therefore “pass”.

722. TLG Immobilien AG

TLG is a 2 bn market cap real estate company that has been taken over by competitor Aroundtown. Both stocks have been hammered due to Covid-19 as we can see in the chart.

With the portfolio consisting out of Office, retail and Hotel objects, the drop in value is not so surprising. Not sure if this is now an opportunity. As I never liked real estate companies, I’ll “pass”.

723. Hornbach Holding AG

Hornbach Holding is the 1.6 bn EUR market cap listed HoldCo of Hornbach Baumarkt that I covered some weeks ago (Nr. 591) plus a wholesale distribution business and some more real estate. To be honest, I totally underestimated how far the “covid-19 home improvement boom” would move the stock, it is now double the value before the crisis:

With the portfolio consisting out of Office, retail and Hotel objects, the drop in value is not so surprising. Not sure if this is now an opportunity. As I never liked real estate companies, I’ll “pass”.

723. Hornbach Holding AG

Hornbach Holding is the 1.6 bn EUR market cap listed HoldCo of Hornbach Baumarkt that I covered some weeks ago (Nr. 591) plus a wholesale distribution business and some more real estate. To be honest, I totally underestimated how far the “covid-19 home improvement boom” would move the stock, it is now double the value before the crisis:

I still think that Hornbach and the other big box home improvement stores have structural issues and that the current share price is to high, therefore I’ll also pass on the Holding.

724. Solar-Fabrik Aktiengesellschaft für Produktion und Vertrieb von solartechnischen Produkten

Bankrupt 0.3 mn market cap shell company. “Pass”.

725. Hensoldt AG

Hensoldt is a 1.3 bn EUR market cap company that just went public in September 2020. The previous owner KKR still owns 60% after the IPO, where 3/4 of the placement went to the company. The company specializes in sensors for security and defense purposes.

The IPO was not a success, the shares were placed at the lower end and of the book builing range at 12 EUR and dropped after a day. The company has a big order back log, but even adjusted EBIT margins are only 5%. Es expected with a PE backed company, intangibles are significant and the company carries around 1 bn of debt.

Nothing to see here, “pass”.

I still think that Hornbach and the other big box home improvement stores have structural issues and that the current share price is to high, therefore I’ll also pass on the Holding.

724. Solar-Fabrik Aktiengesellschaft für Produktion und Vertrieb von solartechnischen Produkten

Bankrupt 0.3 mn market cap shell company. “Pass”.

725. Hensoldt AG

Hensoldt is a 1.3 bn EUR market cap company that just went public in September 2020. The previous owner KKR still owns 60% after the IPO, where 3/4 of the placement went to the company. The company specializes in sensors for security and defense purposes.

The IPO was not a success, the shares were placed at the lower end and of the book builing range at 12 EUR and dropped after a day. The company has a big order back log, but even adjusted EBIT margins are only 5%. Es expected with a PE backed company, intangibles are significant and the company carries around 1 bn of debt.

Nothing to see here, “pass”.

Morphosys does actually have revenues, something like 280 mn in the first 6M of 2020, but that seems to be due to a big one-off in Q1 as they have been successfully licensing one of their products to a US company. Q2 was already (again) negative. Morphosys would be a good starting point to learn more about the sector, but I am not sure if I have ever time for this. Nevertheless I’ll put them on “watch”.

702. Mobotix AG

Mobotix is a 84 mn EUR specialist in video surveilance technology. The stock was “hot” some years ago, but is since then on a long decline:

A quick look into the latest 6M report shows that sales are declining and the company capitalized costs to stabilze returns. Without htis they would be already loss making pre Covid. Nothing to see, “pass”.

703. Telefonica Deutschland AG

Telefonica Deutschland is the stock listed German subsidiary of Telefonica (69% ownership) with a markt cap of 7 bn EUR. The company runs the third German mobile network under the brand O2 and is famous for having the worst quality.

The stock has seen clearly better days:

The company pays relatively high dividends to its mothership in Spain, Topline has been more or less flat, GAAP results are negative due to depreciation. Debt has been increasing in 2020 as they seem to have issues actually earning their dividend payment. I don’t see anything that really interests me, therefore “pass”.

704. Capsensixx AG

Capsensixx is a 42 mn EUR market cap company that is part of the PEH Wertpapier Group which owns 81% of the company. Capsenixx owns 50,01% of Axxion, Axxion, a “private label” fund boutique itself seems to be stagnating/shrinking. After minorities, earnings fro shareholders are limited. The share price doubled from its low in April, but I do not understand why. “Pass”.

705. Voltabox AG

Voltabox, a 53 mn EUR market cap company, should be in theory a red hot stock: They are manufacturing batteries for special purpose vehicles. The stock price however since its IPO in late 2017 knows only one direction: down

The company seems to have struggled before Covid-19 but seems to use this as an excuse now to justify a huge write down. “Pass”.

706. Lloyd Fonds AG

Lloyd Fonds is a 62 mn EUR market cap asset manager that was every successful until the GFC with selling participations in ships. As we can see in the chart, the GFC almost killed the company and it only came back very slowly:

As the company didn’t disclose some risks in its prospectuses, the company was sued by investors over the last several years and the courts said that the company needs to compensate investors at least in one case. The company now seems to reinvent itself as a kind of “private client wealth manager”. Top line has been growing in 2020 but that seems to be driven by an acquisition. The company showed a loss in the first 6M and their still seems to be a significant risk of further compensation payments. “Pass”.

707. Value Holdings AG

Value Holdings AG is a 7,5 mn EUR market cap company that according to its homepage is both an Asset Manager and a holding company for listed stock investments. The company is mostly doing “old school” value investments in German small caps. The performance of the stock compared to the SDAX is however very weak as we can see in the chart;

Nothing to see here, “pass”.

708. InCity Immobilien AG

InCity is a 89 mn EUR market cap real estate company with a relatively unclear foucs. The company is loss making and I couldn’t see anything there that interests me. “pass”.

709. Mineralbrunnen Überkingen-Teinach AG

Mineralbrunnen Überkingen is a 121 mn EUR market cap beverage company that sells mostly sparkling mineral water. The company has a mixed past but it seems that until 2020, they made good progress over the last few years. The first 6M 2020 saw top line decreasing by -20%, which means that they seem to rely on restaurants and bars to a certain amount. Interestingly, the share price of the more liquid pref shares is pretty much back to pre covid-19 levels:

The company has a 70% majority owner with unknown plans, but I found the stock interesting, so it will go on “watch”.

710. Securize IT Solution AG

Securize is a 2,2 mn EUR market cap company that just changed its name and wants to become a “Cloud powerhouse”. “Pass”.

711. Investunity AG

Investunity is a 0,7 mn EUR market cap shell company somehow associated with Dt. Balaton. “Pass”.

712. UET United Electronic Technology AG (ehemals CFC Industriebeteiligungen AG)

UET is a 13 mn EUR market cap company that own a few Telco related businesses. Reporting is super slow (no half year report yet as of Mid Spetmeber) and numbers are unimpressive. “Pass”.

713. Tonkens Agrar AG

Tonkens is a 7 mn EUR market cap agricultural stock, The stock looks cheap, however one can see a long downtrend, the company employs significant debt and results are volatile. “pass”.

714. Jost AG

Jost AG (not related to Jost Werke AG) is a 3 mn EUR market cap company that somehow is active in the tax advisory area. The stock price has been doing nothing for the last 10 years and there doesn’t see anything remarkable that this wil change. “pass”.

715. Covestro AG

Covestro AG is a 8 bn EUR chemicals company which is a spin out/IPO from its old parent Bayer AG which owns a remaining stake of ~7%.

Ironically, since its spin-out, Coverstr has done a lot better than “mothership” Bayer, despite the fact that the stock only trades at around 50% of its peak in 2018:

The stock has recovered the Covid-19 crash already. I do not know a lot about their business but it seems to be volatile and somehow related to the oil price. 2019 was a difficult year, with profit down -70% yoy.

Cyclical stocks should usually be bought when their P/E is high, so now might not be a bad time to do so, but for me it is a “pass”.

716. Teles AG

Teles AG is a 5 mn EUR “Dot.com area” star that has not achieved anything since then. The company is majority owned and operationally not doing well. In 2019 they created significant profits from some related party financing actions. All in all nothing to see, “pass”.

717. Cliq Digital AG

Cliq Digital is a 76 mn EUR market cap company that has seen its share price sky rocketing since the Covid-19 crisis:

From what I understand, the company offers some second rate streaming offers (Movies, sports, music) which it sells predominantly to mobile users. For some strange reasons they are especially successful in North America, where slaes in the first 6M 2020 went up 6x yoy. What I find even more strange is the fact that they don’t use the net income after minorities for the EPS calculation but some other random number which is twice as high. All in all i find the company quite strange and I also don’t like the look of the management board (sorry, I still use my “face detector). “Pass”.

718. Heroes AG

A 7,5 mn EUR market cap stock with frequent name changes. Currently some kind of Sports right digital something company. “pass”.

719. Ceconomy AG

Ceconomy is a 1,4 bn EUR market cap company that was spun-off from Metro in 2017. Initially I thought that Ceconomy (Media Markt and Saturn) was the bad part before realizing that there are no really good parts.

The company is a electronics retailer who is struggling among other things with Amazon and a unfortunate shareholder structure, which gives the family of the founder a blocking minority.

The Covid-19 induced boom of buying stuff for the home office helped them a little bit, doubling the stock price form their low:

Nevrtheless, their legacy store network with a lot of large mall sores will hurt them for some time and it will really be ahrd to turn this company around. Nothing to see for me, “Pass”.

720. ABO Wind AG

ABO WInd is a 225 mn EUR renewable energy / wind farm company that listed in March 2020, just when Covid-19 really kicked in. As we can see in the chart, Covid-19 did not hurt the stock:

The founders still hold >50%, 10% of the capital is held by utility Mainova. ABO plans, develops and sells wind- and solar mostly in Europe. For the first 6 months, ABO could grow nicley and expects around 11 mn in profits for 2020, resulting in a PE of ~20. Perosnally, I do not like these kind of project companies that much. However, as the sector as such is interesting, I put them onto the “watch” list.

721. RM Rheiner Management AG

Rheiner is a repurposed company shell taht used to be a bankrupt textile company but is now a 7 mn EUR market cap investment company, specializing in squeeze out speculations within the German stock market. The company is part of the “Scherzer family”. For me, this is not really interesting, therefore “pass”.

722. TLG Immobilien AG

TLG is a 2 bn market cap real estate company that has been taken over by competitor Aroundtown. Both stocks have been hammered due to Covid-19 as we can see in the chart.

With the portfolio consisting out of Office, retail and Hotel objects, the drop in value is not so surprising. Not sure if this is now an opportunity. As I never liked real estate companies, I’ll “pass”.

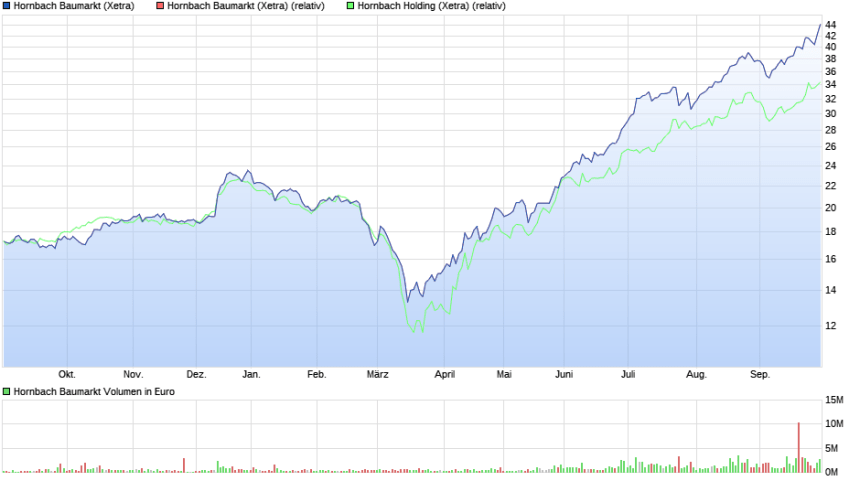

723. Hornbach Holding AG

Hornbach Holding is the 1.6 bn EUR market cap listed HoldCo of Hornbach Baumarkt that I covered some weeks ago (Nr. 591) plus a wholesale distribution business and some more real estate. To be honest, I totally underestimated how far the “covid-19 home improvement boom” would move the stock, it is now double the value before the crisis:

I still think that Hornbach and the other big box home improvement stores have structural issues and that the current share price is to high, therefore I’ll also pass on the Holding.

724. Solar-Fabrik Aktiengesellschaft für Produktion und Vertrieb von solartechnischen Produkten

Bankrupt 0.3 mn market cap shell company. “Pass”.

725. Hensoldt AG

Hensoldt is a 1.3 bn EUR market cap company that just went public in September 2020. The previous owner KKR still owns 60% after the IPO, where 3/4 of the placement went to the company. The company specializes in sensors for security and defense purposes.

The IPO was not a success, the shares were placed at the lower end and of the book builing range at 12 EUR and dropped after a day. The company has a big order back log, but even adjusted EBIT margins are only 5%. Es expected with a PE backed company, intangibles are significant and the company carries around 1 bn of debt.

Nothing to see here, “pass”.

Thank you for your interesting writing. It is not in this part of your german list, but may i ask you for your opinion to ProSieben? I am not able to calculate it, but the Internet companies they own are not priced in or are they?

#721 RM Rheiner Management: Scherzer is on my to do list and might be more interesting. It is trading at a discount to NAV and considerable assets (Nachbesserungsrechte) are not even included in NAV calculations, though possible tax liabilities are also excluded.

Could you explain that?

What I find even more strange is the fact that they don’t use the net income after minorities for the EPS calculation but some other random number which is twice as high.

They take profit after min. / number of shares… This company (cliq) is strange in many ways bec. nobody can explain where and why they earn money 🙂 but this point seems to be ok for me.

Great stuff as always.

I recall last time you asked for tips on possible follow-ups. I suggest (if this fits your sphere of competence):

– Swedish stocks

– Swiss stocks

The former is full of great (mostly overpriced) small and mid caps with some potential hidden champions, the latter is very rarely reported apart from the usual suspects above 10bn CHF.

Thanks for the great works!