All German Shares PArt 34 – Nr. 751-775

At first some good (or bad) news: By going through the German stock markets once again, I detected that my initial list was already outdated and that I missed quite some new IPOs and listings, so there will be (at least) one more post with German shares after this one before I then can wrap up the series into a condensed watch list.

This time, the 25 (to a certain extent) randomly selected (and US election free) stocks resulted in seven stocks that might be in principal worth watching and/or follow up.

751. L-KONZEPT Holding AG

L-Konzept is a 2.7 mn EUR market cap real estate company that has little business and small but consistent losses. “pass”.

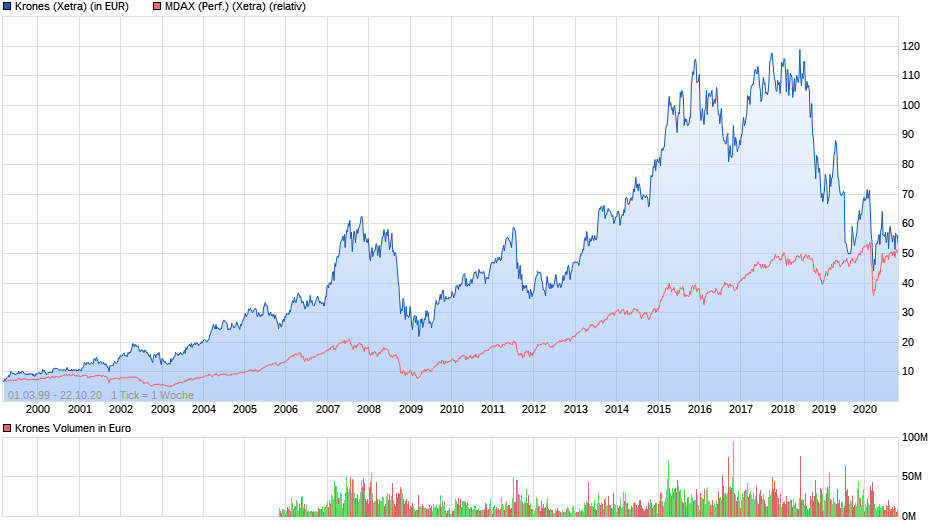

752. Krones AG

Krones, a 1.7 bn market cap company is often considered one of the typical “hidden champions”, being the world leader in manufacturing bottling machinery for the beverage industry. With Covid-19, the whole beverage industry is clearly negatively effected which in turn might make business more difficult for Krones. However if we look at the stock chart, we can see that the stock already peaked in 2018:

2017 was the last year where both, top line and bottom line grew in Tandem by high single digit %. In 2018 already, profitability declined and in 2019 Kornes was barely profitable due to significant restructuring charges. 2020 of course was difficult. Top line was down -10% in the first 6 months and order intake almost -30%. Now the big question is: Will Krones become as profitable again as they were in the past and if yes, when ? To my understanding, part of the drop in 2018/2019 was the fact that certain product lines (esp. PET plastic bottling) that was very profitable ran into issues duet to environmental considerations. Krones, as a typical family majority owned company runs with little debt. In any case, Krones is clearly a company that merits digging deeper. “Watch”.

2017 was the last year where both, top line and bottom line grew in Tandem by high single digit %. In 2018 already, profitability declined and in 2019 Kornes was barely profitable due to significant restructuring charges. 2020 of course was difficult. Top line was down -10% in the first 6 months and order intake almost -30%. Now the big question is: Will Krones become as profitable again as they were in the past and if yes, when ? To my understanding, part of the drop in 2018/2019 was the fact that certain product lines (esp. PET plastic bottling) that was very profitable ran into issues duet to environmental considerations. Krones, as a typical family majority owned company runs with little debt. In any case, Krones is clearly a company that merits digging deeper. “Watch”.

753. KHD Humboldt Wedag Vermögensverwaltung AG

KHD Vermögensverwaltung is a 3,8 mn EUR market cap company whose sole purpose seems to be to lend money to its “sister” company KHD which in turn is Chinese controlled. “Pass”.

754. Compleo Charging Solutions AG

Compleo is a very recent IPO focusing on the very hot sector EV charging stations. The company was IPOed at 49 EUR per share but dropped directly afterwards. The company is (of course) still loss making, for the 169 mn market cap, investors get around 30 mn EUR trailing annual revenues and 2 mn losses. Although the sector is interesting, the involvement of a certain Mr. Elgeti makes this un-investable for me. “Pass”.

755. Senvion SE

Senvion is a 2 mn EUR bankrupt wind energy company. “pass”.

756. Knorr Bremse AG

Knorr Bremse is a 16,5 bn EUR market cap company that went public in 2018 and still is majority owned by self-made billionaire Heinz Herrmann Thiele. Thiele is still quite active at 79 years, among others he recently bought >10% of Lufthansa. Despite selling twice significant stakes and firing CEOs quite often, the Knorr Bremse stock has done very well:  The company is a global market leader in breaking systems, mostly for trucks and trains. The business is very profitable, however the stock trades close to 30xPE for 2019. I guess it could be interesting at a (much) lower price point. Therefore I’ll put them on “Watch”.

The company is a global market leader in breaking systems, mostly for trucks and trains. The business is very profitable, however the stock trades close to 30xPE for 2019. I guess it could be interesting at a (much) lower price point. Therefore I’ll put them on “Watch”.

757. Curevac AG

Curevac is a “super hot” Bio Tech company that was successfully IPOed at the Nasdaq in August. From an IPO price of 16 USD/share, the shares went up to around 77 USD before stabilizing at a shre price of currently 50 USD, resulting in a market cap of ~7,4 bn EUR. Why is it so hot ? Curevac is developing a vaccine against Covid-19 and seems to be one of the more promising candidates. CureVac is developing the vaccine based on the so called mRNA technology which is different to traditional vaccines. Instead of using somehow defunct viruses, the mRNA technology only requires small RNA samples to be used which in theory should be a lot better especially for older patients. The technology could also be used for other vaccines. The company has some revenues but I guess these are research grants as the most developed projects according to the IPO prospectus were in stage 1 clinical trials. For all of us I hope that they are successful with their Covid-19 vaccine, but for me the risk/return profile of such a stock is just too hard to handicap. “Pass”.

758. Schuler AG

Schuler AG is a supplier to the automobile industry with a market cap of 566 mn EUR. Schule is majority owned by Austrian company Andritz which took over the majority already in 2012. This could be something for Squeeze out specialists, however for me this is too difficult. Therefore “pass”.

759. Kur- und Verkehrsbetriebe Aktiengesellschaft Oberstdorf

This 15 mn EUR market cap company runs several ski lifts and recreational facilities around the German mountain town Oberstdorf. The company had a pretty decent stock performance recently, most likely driven to the “vacation in Germany” boom during Covid-19.

The stock however is super illiquid and majority owned by the municipality. Would be a nice “Hobby stock”, but for my purpose a “pass”.

760. Koenig & Bauer AG

Germany was once the home of the three biggest manufacturers of large scale prinitng machines and Koneig & Bauer is one of them besides Heideldruck and now bankrupt MAN Roland. Koenig und Bauer, with a 295 mn market cap, did somehow better than the other two, but still was a lousy investment over the past 20 years:  In between there was quite some volatility. The stock increased for instance from +10 EUR per share in 2015 to around 55 EUR in 2019 before dropping back to 20 EUR this year. The company managed to triple profits in 2016 from 2015, then roughly keeping that level in 2017 and 2018 before profits dropped to 35 mn EUR in 2019. The first &M 2020 looked pretty ugly with a significant loss of -44 mn EUR. K&B was always quite conservatively financed which prevents any existential risks but I do not see any reason why the company should be long term attractive. The problems started already in 2019 and Covid-19 just made them worse. “Pass”.

In between there was quite some volatility. The stock increased for instance from +10 EUR per share in 2015 to around 55 EUR in 2019 before dropping back to 20 EUR this year. The company managed to triple profits in 2016 from 2015, then roughly keeping that level in 2017 and 2018 before profits dropped to 35 mn EUR in 2019. The first &M 2020 looked pretty ugly with a significant loss of -44 mn EUR. K&B was always quite conservatively financed which prevents any existential risks but I do not see any reason why the company should be long term attractive. The problems started already in 2019 and Covid-19 just made them worse. “Pass”.

761. KSB AG

KSB is a 383 mn EUR market cap company that is majority owned by the founding family and is one of the leading manufacturers of large pumping systems for instance for utilities or the oil and gas industry.

The company profited significantly from the oil and gas and natural resources boom in the mid 2000s as we can see in the long term stock chart:

Since then however, the stock is on a long way down without any clear indicator for a reversal. In the first 6M 2020, sales declined by -8%, profits however declined by -2/3, indicating a large block of fixed costs. The company has a large pension deficit and although it looks cheap on many metrics, I’ll “pass”.

762. Pacifico Renewables Yield AG

Pacifioc Renewables is one of the latest additions to the German stock market. The company had been listed in November 2019 and buys and operates renewable solar and wind parks in Europe. The company purchases these projects from ” Sister” company. Both companies (the listed one by 75%) are owned by “Pelion Green Alpha”, a vehicle owned by Alexander Samwer, one of the three brothers who founded Rocket Internet.

So instead of E-Commerce, Alexander now seems to think that renewable energy is the “Hotter” sector. Interesting.

From what I know, Alexander has a better reputation than his brother Oliver, nevertheless the set-up with the non-consolidated feeder vehicle creates significant conflicts of interest. “Pass”.

763. KST Beteiligungs AG (ehemals KST Wertpapierhandelsgesellschaft AG)

KST is a 6,75 mn EUR market cap holding company with little activity. “pass”.

764. Serviceware AG

Serviceware is a 136 mn ER market cap enterprise software company that went public in 2018 at a price of 24 EUR per share. Looking at the chart we can see that anyone who bought at the IPO might not be very happy:

Part of the issue seems to be that the company showed a loss in FY 2018/2019 although growth was pretty OK at ++20% yoy. Growth slowed in the first 9m 2019/2020 but was still +10% yoy, however it is not clear if all of this is organic.

On the plus side, the company seems to be transitioning even faster into a SaaS model from a traditional License/service set up and they are solid from a financial point of view, on the other hand the show very low margins for a software business and negative cash flow. Nevertheless, in principle this could be worth to “watch”.

765. Kulmbacher Brauerei AG

Kulmbacher is a 207 mn EUR market cap company, that in contrast to many similar stocks is still a very active brewery. The company at first sight is surprisingly profitable.

The stock made a big jump in early 2018 but stagnated since then, although 2019 seems to have been a very good year:

Interestingly, the first 6M 2020 were more or less flat vs. 2019, which is quite a surprise. It looks like that they have little exposure to bars and restaurants. If I would need to invest in a German brewery Kulmbacher would be my first choice, As I don’t have to, I’ll “pass”.

766. SM Wirtschaftsberatungs Aktiengesellschaft

SM is a 25 mn market cap holding company that mainly invests into real estate. I didn’t see anything that is very interesting so “pass”.

767. Biontech AG

Biontech went public on the Nasdaq in October 2019 and was struggling in the beginning. The company specializes in antibody treatments initially against cancer. However when Covid-19 hit, the company reacted super fast and is now has one of the most promising vaccines in its pipeline together with US giant Pfizer.

Interestingly, other than German competitor Curevac, BioNtech didn’t receive money from the GErman Governement. However the company is backed by the Billionaire twins Strüngemann, who made a fortune selling their Pharma company Hexal to Novartis.

I do highly appreciate how BionTech has moved so fast in developing the vaccine, but for me it is not a company that I underatnd, therfore “pass”.

768. KWS Saat AG

KWS is a 2.1 bn EUR market cap company that is active in agricultural seeds. The company clearly is one of the “hidden Champions” with a long history of growth as we can see in the chart, although there has been some stagnation for the last years:

The business as such has decent margins (13% EBIT margin) and KWS is clearly one of the leading players in their field. In the recent FY 2019/2020, top line growth was good, however EPS shrank due to conservative accounting for an acquisition in vegetable seeds.

The company is majority family owned (~70%). Overall this is clearly a very interesting company and, at the right price a potentially interesting investment. “Watch”.

769. Siemens Energy AG

Siemens Energy is a relatively young addition to the German stock market. The 13.7 bn EUR market cap company was spun off from Siemens in September 2020. The stock traded initially at 22 EUR/share bur lost around -15% since then.

The spin-off comprises the traditional gas turbine business but also the stake in the Siemens-Gamesa Wind Turbine JV that is listed separately. This stake is actually worth 11.3 bn ER (0,67*16.5). The company also owns other “extra assets” such as a 24% stake in Siemens India worth 1 bn EUR. The company also claims to have 2 bn in cash, so the traditional business is “for free”. On the other hand, according to the most recent reports, this business has been loss making.

Nevertheless, I’ll put the stock on “watch” as a potential interesting spin-off situation.

770. Lechwerke AG

Lechwerke is a 3.4 bn ER market cap regional utility, majority owned (90%) by E.On. Comparing the chart with E.oN shows that regional utilities seem to be good and steady businesses as long as you don’t try to do stupid stuff:

The company is relatively conservatively financed and has been able to create reliable earnings over the years, however with little growth. The share price increase in the last few years seems to have been driven mostly by a multiple expansion.

These the company trades at >30x trailing earnings. With a dividend yield of ~3% it could be interesting for some very conservative investors, but for me it is a “pass”.

771. 4basebio AG

4basebio is a 91 mn EUR market cap gene therapy / BioTech company. The company does minimal sales (500k in 6M 2020) after selling its main business. The interesting part is however that the company has 85 mn EUR in “hard” cash and another 15 mn in a trust account, so effectively the stock is a cash box.

However this has attracted Dt. Balaton via Sparta, who made a 2 EUR per share offer in September, but only received a few percent so that they currently own ~33%.

On top of this, 4basebio seems to prepare a spin-off of the remaining operating business in December.

Despite the involvement of Dt. Balaton, this might be worth a second look as special situation. “Watch.”

772. Akasol AG

Akasol is a 295 mn EUR market cap company that was IPOed in June 2018. The company is active in a super-hot area: battery technology for Trucks, Busses etc.

The company has grown by ~100% in 2019 but was still making loss on an EBITDA basis. However in 6M 2020, growth disappeared and BIT margin was -28,1% of sales.

They claim to have an order book of 2 bn ER, but sales in 6M have been less than 20 mn EUR. The stock however didn’t suffer that much:

On the plus side, the separate family business of the CEO still seems to be the dominating shareholder. Nevertheless this doesn’t sound like such a great business fundamentally, so I’ll “pass”.

773. aifinyo AG

aifinyo AG is a 84 mn EUR market cap company that offers financial services to small businesses. They offer all kind of services from factoring, leasing and other financing offerings on a “digital” basis. The company seems to have listed in 2019 (or 2018 ?) but the stock price recently suffered:

I guess investors would have expected sales to go up as small business need financing, but somehow they were very negatively effected by Covid-19.

On the plus side, the founders still own significant stakes in the company, on the minus side, the founder is a former banker and these kind of “start-ups” rarely succeed. For the time being, I’ll “pass”.

773. Aladdin Healthcare Technology

Alladin is a 11 mn EUR market cap AI Healthcare technology company with a lot of professors on its company presentation that seems to be the reincarnation of “Aladdin Blockchain”. The company has no revenues and the “German” MD seems to do this as a side gig from his UK home. “pass”.

774. Beno Holding AG

Beno is a recently listed, 19 mn EUR market cap company that invests in “industrial” real estate. Not my cup of teas, “pass”.

775. Brockhaus Capital Management AG

This is a 309 mn EUR market cap company I had never heard about before. They seem to invest in “Technology companies” . The company IPOed in July 2020 at 32 EUR per share, raising more than 100 mn EUR. For the 309 mn ER, investors get 23 mn 6M sales and around 2 mn EBITDA. I am not sure why exactly this stock is valued as it is, although the stock now trades below the IPO price.

Maybe the management is so excellent, but I will stay away. “pass”.

You have put a lot of work into this review and in the interests of making it more accessible would it be possible to create a link on the banner above to say “German Shares” as there seems no structured way to interrogate it. I say this as I remember coming across a comment you made on one of my shareholdings and yet when I search the company name I cannot locate it and I am left with trawling through the different months.

BTW love your site.

KWS Saat is no AG anymore, but has been changed into a KGaA.

Ok, thanks. As I mentioned, the list is quite old…..

Regarding Compleo Charging: The certain Mr Elgeti is the same as with the two German REITs?

Have you noticed the super-wide spread between the KSB VZ and KSB ST since COVID-19 (-30%)? It before traded in sync for years… Very strange, it might be interesting to follow whats going on there.

KSB has a dominating major shareholder that is said to hold ~84% of voting rights.

By the way: If Germany decides to move back into carbon free nuclear power, KSB would be an interesting play IMO. I have it on my watch-list.

Sadly, KSB payed private expenses for the family. Otherwise might have been an interesting company. But in this case, the trust in the management /family is very low now!

Yes, I forgot to mention this. See for instance here:

https://www.presseportal.de/pm/7169/3694474