Performance Review 2011-2020 – Lessons learned, Outlook 2030

After the 2020 Performance review a few days ago, this time a more “in depth” look into the 10 year performance of the portfolio. For the record: The Performance page of the blog is now fully updated 😉

As this has become a very long post, these are the main sections:

- Numbers & Stats for the Portfolio (plus Benchmark discussion)

- Flop 15 & Top 15 positions

- 2011-2020 Macro events

- Style /Process /System

- Main lessons learned

- Outlook 2021-2030

1. Numbers & Statistics

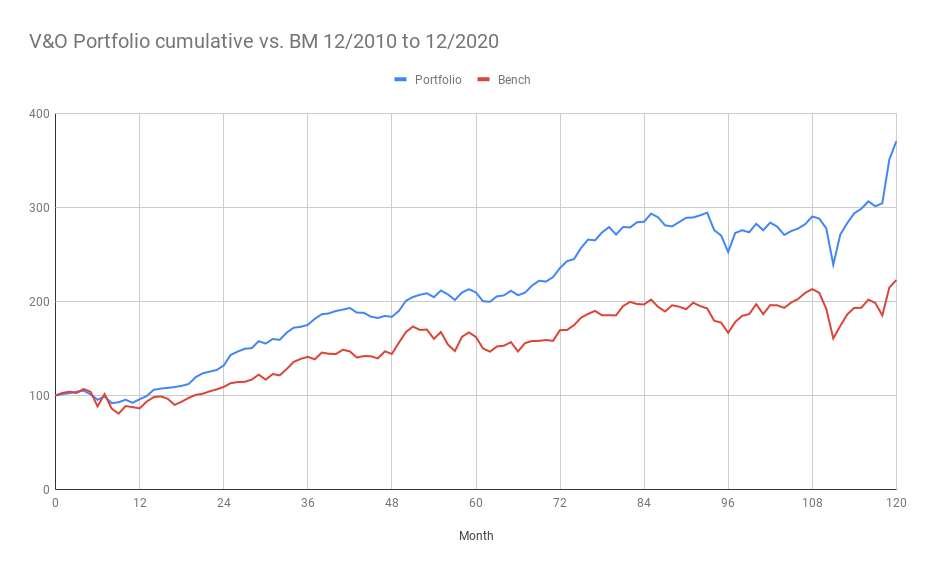

The hard numbers: Over the 10 years from 12/31/2010 to 12/31/2020, the portfolio gained +270,3% against +122,7% against the Benchmark (Eurostoxx50(25%), Eurostoxx small 200 (25%), DAX (30%), MDAX (20%), all performance indices including Dividends).. In CAGR numbers this translates into 14,0% p.a. for the portfolio vs. 8,3% p.a. for the Benchmark. As a graph this looks as follows:

A widely used concept to check with how much risk the performance was achieved is the Sharpe Ratio that compares performance with volatility. Although not perfect, it is sometimes useful. This is how it looks over 10 years, using monthly returns, both for the BM and the portfolio:

| Sharpe 10Y | |

| Perf BM | 0.8% |

| Stdev BM | 5.08% |

| Sharpe BM | 0.54 |

| Perf Portfolio | 1.2% |

| Stdev Portf | 3.6% |

| Sharpe Portf. | 1.12 |

A Sharpe Ratio above 1 is considered to be “good”. In any case it clearly shows that the portfolio is less volatile than the Benchmark and that the performance is not just the result of a “high Beta” positions.

The annual returns look as follows:

| Bench | Portfolio | Perf BM | Perf. Portf. | Portf-BM | |

| 2010 | 6,394 | $100.00 | |||

| 2011 | 5,510 | $95.95 | -13.8% | -4.1% | 9.8% |

| 2012 | 6,973 | $131.81 | 26.6% | 37.4% | 10.8% |

| 2013 | 9,017 | $175.04 | 29.3% | 32.8% | 3.5% |

| 2014 | 9,214 | $183.60 | 2.2% | 4.9% | 2.7% |

| 2015 | 10,363 | $209.53 | 12.5% | 14.1% | 1.7% |

| 2016 | 10,835 | $235.56 | 4.6% | 12.4% | 7.9% |

| 2017 | 12,582 | $284.72 | 16.1% | 20.9% | 4.7% |

| 2018 | 10,651 | $252.63 | -15.3% | -11.3% | 4.1% |

| 2019 | 13,620 | $290.30 | 27.9% | 15.0% | -12.9% |

| 2020 | 14,238 | $370.31 | 4.5% | 27.6% | 23.0% |

| J | |||||

|

Since inception

|

$370.31 | 122.7% | 270.3% | 147.6% | |

|

CAGR 2019

|

8.3% | 14.0% | 5.7% |

Both, the portfolio and the BM had only 2 negative years out of 10 which indicates that it was a decade with very nice opportunities.

Nevertheless, even the relatively weak European markets (lacking the Tech exposure of US markets) achieved a respectable 8,3% CAGR in these 10 years which is a good reminder that macro events often have only short term impacts.

Some words on the Benchmark

Over the years I received some comments that I am low balling the Benchmark because i don’t use US indices. Low-balling Benchmarks is indeed a problem in the fund industry, especially if there are performance fees involved that are calculated relative to Benchmarks.

However one of the rules of fund in performance measurement and attribution is, that the Benchmark should reflect the targeted investable universe for each specific mandate. For reasons that I will discuss later, I never had any significant US stock positions in the portfolio. My attempts to invest globally (Australia, Russia, Turkey) mostly ended with very mixed results. At year end, only 0,9% of my portfolio was in a US stock (Southwest). The rest of my portfolio is European and will stay so for the foreseeable future. Therefore I do think my Benchmark, a combination of German and European Benchmarks, is appropriate.

For completeness, I made a quick comparison of some Benchmarks over the 10 year time period which shows that my benchmark contains a few very well performing indices such as the MDAX who performed (in EUR) equal to the S&P 500:

| S&P 500 | S&P 500 € | MSCI World | MSCI World € | DAX | MDAX | |

| 2010 | 1,140 | 853 | 1,280 | 958 | 6,914 | 10,128 |

| 2020 | 3,218 | 2,634 | 2,690 | 2,202 | 13,718 | 30,796 |

| Total | 182.3% | 208.7% | 110.1% | 129.8% | 98.4% | 204.1% |

| CAGR | 10.9% | 11.9% | 7.7% | 8.7% | 7.1% | 11.8% |

Looking back 5 years

Five years ago, I did a 5 year performance review.

What I found interesting is that back then the out-performance with 5,8% p.a. was at exactly the same level as after 10 years, whereas the Sharpe ratio was better at around 1,53. I think this is the effect of having a little more growth tilt in the portfolio than I had back then. My portfolio now is maybe less idiosyncratic as it was back in 2015.

This is what I wrote back then on my expectations for 2016-2020:

Outlook & Strategy 2016-2020

I think the probability is high that the next 5 years will be not as good as the last five years, both in absolute terms as well as in relative terms for my portfolio. “Value” in the areas of my core competency (boring European small caps) has become extremely rare. Maybe my shift to larger cap companies and Emerging market related stocks will work out, maybe not. On the other hand, if someone would have asked me five years ago if I would more than double the portfolio within 5 years I would have clearly said “no way”.

As my readers know, I don’t make predictions about future stock prices. I do think that there is some value out there but mostly in areas where I am not an expert. So one of my tasks will be to learn more in areas where I only have very superficial knowledge such as Emerging markets, commodities and energy.

Will there be a big crash at the stock market in the next 5 years ? I don’t know and I wouldn’t bet on it. Market timing for me is something which clearly doesn’t add value and spending too much time on macro economic issues is also not time well spent.

So for me the strategy will remain the same as for the past 5 years: Analyze company by company, buy if they are cheap, sell when they become to expensive. Maybe the companies that I analyze wil become a little bit more exotic.

My “slow investing” philosophy so far has clearly not directly improved my returns but my nerves. So I will stick to the maximum of 1 transaction per month. The only thing I might change is that I will maybe allow myself to exchange one position per month. Otherwise I will have some indirect market timing if I sell first, then go in cash and invest again with a 1 month time lag.

My expectation for lower returns turned out to be true: My portfolio “only” made 12,1% p.a. from 2016 to 2020 compared to 14,9% p.a. for the first 5 years. However, the relative out-performance stayed the same despite the “freak accident” years 2019 and 2020. However Large Caps and Emerging markets did not contribute very much to performance.

I did learn more about Emerging Markets, commodities and energy that helped me to avoid these areas. Unfortunately I started relatively late to learn about Software & Technology.

2. Position stats & 15 all time Winners & Losers:

In addition to the 27 current positions, I have 134 unique positions that have been bought and sold during the last 10 years, resulting overall in 161 positions that were at some point in the portfolio or an avg of 16 new positions per annum.

Hall of shame – all time Flop 15

This is an update to this 2018 post

| Name | Loss in % | Year of first investment |

Year fully sold

|

|

| 1 | Metro Bank | -59.43% | 2020 | 2020 |

| 2 | Short: Kabel Deutschland | -53.17% | 2011 | 2013 |

| 3 | Cars.com | -43.80% | 2017 | 2019 |

| 4 | Silver CHef | -39.58% | 2016 | 2018 |

| 5 | Sistema | -39.35% | 2014 | 2014 |

| 6 | Bijou Brigitte | -37.18% | 2010 | 2011 |

| 7 | Metro AG | -26.36% | 2017 | 2018 |

| 8 | TGS Nopec | -34.24% | 2013 | 2020 |

| 9 | Apogee Enterprises | -32.31% | 2011 | 2011 |

| 10 | Noble | -29.00% | 2011 | 2011 |

| 11 | KSB | -24.17% | 2011 | 2011 |

| 12 | Fortum | -23.86% | 2011 | 2012 |

| 13 | Portugal Telecom | -23.75% | 2013 | 2014 |

| 14 | Einhell VZ | -20.67% | 2010 | 2011 |

| 15 | Medtronic | -18.93% | 2010 | 2011 |

Looking at the list, my main takeaway is that I should avoid investments with “Metro” in the name and that there is a over-proportional percentage of Non-European stocks in the losers list.

Hall of Fame – all time Top 15

| Name | Total Gain in % | Year of first investment |

Year fully sold

|

|

| 1 | Bouvet ASA | 589.90% | 2013 | |

| 2 | G. Perrier | 345.50% | 2013 | |

| 3 | Zur Rose | 241.40% | 2019 | |

| 4 | Dart Group | 232.96% | 2012 | 2013 |

| 5 | IGE & XAO SA | 227.54% | 2013 | 2018 |

| 6 | Draeger Part. | 198.60% | 2011 | 2020 |

| 7 | Installux | 178.50% | 2012 | |

| 8 | TFF Group | 132.40% | 2010 | |

| 9 | SIAS SpA | 129.63% | 2012 | 2014 |

| 10 | HT1 Funding | 127.29% | 2010 | 2016 |

| 11 | Thermador | 111.32% | 2014 | |

| 12 | AIRE KgAA | 108.55% | 2010 | 2012 |

| 13 | Brenntag | 107.21% | 2020 | 2020 |

| 14 | Admiral | 103.20% | 2014 | |

| 15 | DEGI International | 102.36% | 2010 | 2011 |

Some observations:

- Every single “top performer” is a European investment

- the 2010-2013 vintages were clearly good. I think this has to do that for some time after the GFC and during the Euro Crisis, quality securities were miss-priced in a wide area and I managed to find a few.

- Most out-performers were clearly GARP stocks that I managed to buy cheaply back then. A smaller part were Special situations that resulted from the GFC dislocation

- I managed better over the years to hold on big winners. Very early on, I sold some good stocks to early (Dart, Cranswick, IGE ….)

- So far I didn’t manage to get a 10-bagger. Bouvet is my best shot at that (non important) goal

- However roughly 10% of all stocks that went into my portfolio became doubles or better. That’s a pretty Ok “hit ratio” in my opinion

- Technology is pretty much absent from the list (only IGE & XAO, Bouvet and maybe Zur Rose have some tech aspects). That was clearly an omission from my side not understanding for instance software business models better

3. 2011-2020 Macro review

Just to remember a few main topics over the 10 years have been in financial markets (and I maybe forgot a few)

- In 2011, stocks were out of fashion because of the “lost decade”, mainly caused by the Great Financial crisis (GFC). 2011 started with a double digit BM loss

- Euro crisis with Greek Quasi-default 2011 and big draw downs and high volatility (in 2011 there were two months with a BM loss of ~-15%)

- High Frequency Trading went mainstream (Flash Boys 2014, Flash crash 2010)

- Trump being elected as POTUS in 2016 and trying to steal the election in 2020 after losing narrowly

- Unexpected result of Brexit vote 2016

- The most admired company of the 2000s, General Electric implodes and loses more than -90% of its market cap

- Interest rates went negative in many countries, now extending to retail bank deposits

- Trade war US vs. China

- 2020 Pandemic

- Highly volatile oil prices with first time ever negative prices in 2020

- A German DAX Company went bankrupt (Wirecard)

- Software (and its producers) ate the world

In my opinion the two biggest overall drivers of the performance from 2011 to 2020 were not these Macro Events but clearly the decrease in (real) interest rates and the breakthrough of many technologies. We should not forget that the Iphone was only invented in 2007/2008. End of 2010, when I began the blog, only around 70 mn Iphones had been sold in total compared to around 1.800 million (!!!) at the end of 2020. Through smart phones, a new huge global industry materialized basically out of nothing and creating one of the biggest profit pools in human history and, along the way, killing a lot of other business models. Similar breakthrough shave been made in Biotech (think of mRNA Vaccines among others) and renewable energy. These two big shifts created a significant value creation int he tech sector and an even greater stock price appreciation.

4. Style / Process /System 2011-2020

Depending on how one would see it, my approach evolved/drifted from a quantitative /Deep Value starting point, via a period of more systematic” investing to my current more “quality GARP” based approach.

Looking at the initial “mission statement” it is clear that this was very much “Graham influenced” with pretty conservative, balance sheet related hurdle rates based on backward looking metrics with a small quality overlay. My research always started with a quantitative screener and I would not look at companies that didn’t fit the criteria. For some time I even experimented with the “Magix Sixes”, an approach that filters out really cheap companies but I didn’t feel confortable investing into very cheap (and weak) companies. And I discovered early enough that a lot of the “super cheap” companies like for instance German listed Chinese companies had systematic fraud issues.

I think the big difference between now and 10 years ago was that 10 years ago, the market was still “shocked” by the GFC and the subsequent Euro crisis offered relatively high quality stocks at low valuations. So back then that approach still allowed me/us to include some quality stocks into the portfolio but also a couple of “cigar butts”.

In 2012/2013 I tried to capture quality better via a new “system” that I called the BOSS score. Initially that helped me to find some interesting low priced stocks that turned out to be nice quality GARP stocks like Bouvet or Gerard Perrier. However over time I recognized the following: First, maintaining the database to calculate my returns took a lot of time and second, the quality of the companies I found declined pretty rapidly.

These days a Graham approach can still work for some but one needs the right approach and be comfortable with difficult turn around situation and/or bad balance sheets or intransparent Governance.

For a long time I was also very skeptical vs. US stocks because I didn’t like intangibles and didn’t really understand the role that “soft capital” is playing these days and that a balance sheet is only a starting point for an analysis. Plus, I didn’t understand that due to the large size and homogeneity of the US market, successful US small caps have a much longer runway before they need to do a riskier international expansion than their European peers.

In 2015 I added for the first time an Investment fund to the portfolio, TGV Partners. TGV Partners is run by my former collaborator and investing into his fund was clearly a huge benefit. Not only that he outperformed my portfolio but also I learned a lot from his approach to more growth driven investments.

In 2020 I added with Active Ownership another fund that hopefully allows me to learn much more

One big topic for me was clearly the fact that the Financial Industry, which I consider the sector that I know best was pretty much a no-go area despite some very specific opportunities in the beginning of the decade. Fortunately I learned this rather sooner than later and avoided getting stuck in too much exposure into financials.

Overall I would consider myself now rather “GARP” type of investor with a “Special situation” hobby. Or to put it into other words: These days I’ll try to find out if a company is undervalued compared to what it earns in 3-5 years in contrast to analyzing if a company is cheap compared to its 10 year trailing average of earnings or any relatively arbitrary historic accounting number like Price to Book.

Actually I do not use any screeners at all these days. I think reading high quality news sources and a good network of fellow minded investors are a much better starting point for finding interesting stocks than a screener.

One of my biggest open issues is that there is relatively little correlation between what I think is a “high conviction investment” and the ultimate success of that position. Maybe that has to do with my 20/80 approach. As a result, It makes sense for me in general to start smaller and then add into a position when it is actually working well. This is psychologically not easy for me but seems to be the best compromise. On the flip side, I avoided big mistakes, Even my worst investments only lost me around 1-2% of portfolio value.

Another weakness of mine is that sometimes I pass on investment because I like to have “original ideas” and I do not like just to copy ideas from others. Sometimes a good copy works better. But creating original ideas is more fun.

One of my main to dos going forward is to better document my current actual process & system to have a basis from where I can improve.

5. A few main lessons learned from these 10 years:

- Everyone needs to find his/her own investment style/process/system that fits his/her personality. Reading every book about Warren Buffett unfortunately doesn’t turn anyone into Warren Buffett

- However, Style, processes and systems should be regularly reviewed and adapted to match underlying changes

- There is no “Magic formula” that works all the time. Stock markets are dynamic and adapt, so must investors

- Finding good stocks is less than half of the game. Being able to hold the really good ones is even more important

- Check your portfolio on a regular basis for systematic exposures that are not obvious (oil price, Travel related etc.)

- Try to increase your circle of competence but don’t be too stubborn if it doesn’t work

- Try to limit “information intake” to high quality sources

- Don’t try to create a religion out of an investment approach

- People are important, both in management of the company but also in the governance and among shareholders

- Fundamental research and market timing don’t work well together. Over the long run I do not know any stock picker who has added consistent value by market timing

- Short selling requires a very different skill set and approach than long fundamental investing. very few investors are really good on both sides

- Don’t think too much about missed opportunities. There will always be new opportunities.

- Don’t blame anyone else for your mistakes. Be honest to yourself. This is the only way to improve.

- Just showing up is the hidden superpower for any individual investor. Make sure you are in it for the long term. As Chuck Schwab says: “It is not timing the market” that is important but “time in the market”.

- Structure your approach to have fun. Having fun is the best incentive to remain engaged for a very long time. Once it becomes a chore, you should completely rethink your approach

- Individual investors cannot compete in speed with professionals, however patience is a very good way to achieve superior results over a long time

- Write a journal. Write down your “plan” for every investment and check from time to time how the investment is doing vs. plan.

6. Outlook 2021-2030

Similar to my 5 year outlook from early 2016, a few Predictions for the next 10 years:

I expect nominal returns over the next 10 years in general to be lower than the past 10 years. I believe that long term equity returns are a combination of the risk free rate and an equity premium. In December 2010, the 10 year German Bund was at around 2,9% p.a. and German indices realized a 10 year equity premium of something between 4,2% equity premium (Dax) to ~8% for the MDAX.

The current starting point for the 10 year Bund is -0,6%, which to me indicates that average returns might be 3-4% p.a. lower. Even if my relative performance stay the same, reaching double digit returns over the next decade will be not easy.

This time I also predict that there will be at least one major crash in the next 10 years, maybe even more. I do think that there is even the possibility of a longer bear market and that buying the dips will stop working for some time. Maybe not as long as in the 1970s but maybe 3 to 4 years. However I have no idea when that could happen.

In the next 1-2 years the big question ist if and how the World economy emerges from the pandemic and what impact an eventual wae of defaults will have. There is a good case for a strong recovery but in the end no one knows what is going to happen.

In principle , my “system” will stay the same: Try to find well run companies with solid balance sheets and good future prospects at a reasonable price. Let winners run, sell losers quickly if they performa much worse than I predicted. Avoid structurally impaired sectors/businesses. Try to learn as much as I can and stay away from market timing.

Very nice article! In my view the key to long term success is doing enough research to really understand your investing strategy, when it will work and when it will not. I’ve been on mission to document the performance of various stocks screens (fundamental and not) so for I’m up to over 60 and counting! Send me requests and I’ll take them on!

Also congrats from my side and thanks for the blog.

But … that posting once more proves your apostasy. ;).

Especially point 5.2 and 5.3 show that you lost your religion (and 5.8, of course) – or you never really had it. It just resembles the old sentence “This time is different”.

Thanks for the comment. To be honest, “this time is different” is one of the dumbest arguments you can bring to the table in long term investing. My counterargument would be “Every time is somehow different”. Otherwise market timers would be the richest investors and I don’t know that many long term successful market timers.

Dear MMI,

congratulations on your performance. Thank you for keeping up the blog and the high-quality content. I appreciate the links to other authors.

You are not alone with your opinion that future returns in the stock market will (probably) be lower than in the last ten years (and lower than some might anticipate). Maybe this article might be interesting for you regarding that context: https://www.hussmanfunds.com/comment/mc201201/ …To sum it up, his conclusion is: “Speculation has now driven our estimate of prospective 12-year S&P 500 total returns to -3.6%”, we’ll see how it goes. Have you considered holding some more cash? And holding cash not to time the market, but because fundamentals do not look too bright?! Do you expect the European market to perform better than the US market?

When talking about bright fundamentals: Have you ever looked at Lang&Schwarz? They have a great run, but other than Tesla, I see it fundamentally based: the 2020 EPS will be around 12€. And when looking at the trade numbers at the beginning of 2021 the future seems to be better than the present. L&S is the doing the trades for TradeRepublic. TradeRepublic is now starting in France and will be released in other European countries soon… I am keen on your opinion on the company.

Cheers, Michael

Even if the articel seems compelling. I wouldnt use/share Hussmans outlook because he is known to be very bearish for at least the last decade and his performance & AuM were really not good.

https://www.csmonitor.com/Business/The-Reformed-Broker/2011/0112/Mutual-fund-manager-apologizes-kind-of

Thank you very much for your insights. I did not know his very bearish opinion that he does not seem to change. Do you have better sources that try to predict the long term returns of equities (either US or Europe)?

Hi Miachael, I stopped reading anything from Hussmann like 8 years ago. Allow me one comment: There are no “better” sources for predictions. No one knows what the returns over the next 10 years will be.

Very interesting and congratulations for your consistent out performance. One take away is that in order to achieve good performance consistently is the ability to adapt. Do you think you would consider more quantitative factors, if the economics change in a way that old style value becomes more fruitful? Or do you want to explore and deepen your qualitative skills?

If you mean a pure P/something driven approach to picking stocks: I think you will keep getting mostly “Cigar butts” when looking at “cheap” stocks for many years to come. But you never know, the next crisis could be around the corner.

I am very happy to found that blog some months ago. My guess is, when pandemic is over the next big task will be to avoid a big inflation risk . This is usually not good for shares. On the other side, house prizes run up far, Gold is on record highs, not to mention the cryptos. . I do not see any reasonable investments than shares of good companies.

So keep up the good work, i will follow your journey an hope to read much more of your success and developement.

Congrats, dear MMI, for the outstanding and consistent performance. One remark maybe: If you expect equity yields to be lower in the next 10 years, you should be super bullish for the stock market IMO, at least in the short term. Why? According to Deutsche, the Dax trades at 16x 2021 earnings at the moment. Don’t know if that makes any sense but if yes, this translates into an earnings yield of 6.3%. For the yield to actually drop to 4%, the P/E needs to go up to 25x. Accordingly, the DAX needs to rise by more than 50% for that yield to become real, assuming zero growth. So either stock prices must go up strongly or earnings need to go down significantly forever for yields to drop by 2 percentage points.

Personally, I don’t expect equity yields to drop in general by a wide margin. (Actively) investing into stocks is a cumbersome business and comes with unpleasant surprises and high market volatility at times. Most people don’t fancy that. So I assume there will always be opportunities to buy stocks on the cheap side, not least because of all the “dumb” money that went into index investing. So I think there will always be opportunities in the future and I bet, you will find the one or the other. Looking forward to it!

Enrico,

not sure if I fully follow your argument. First, I find it interesting that Deutsche seems to already know what 2021 earnings will be for all DAX companies (Dax 30 ? Dax 40 ?).Second: why should the “earnings yield” drop to 4%?

Another remark. The market PE of an index can actually go up via another mechanism: Earnings go down. A couple of the DAX companies do have real structural issues. Of course the sell side never projects lower earnings.

But anyway, I have no crystal ball, so any prediction is great. The point that I wanted to make is that the general tailwind of falling interest rates that we had since the late 80ties is going away.

Hi MMI, i have been a reader of your blog for almost 10 years and it did inspire and educate me significantly. One question i have for you is what portfolio management software do you use? I have tried my own excel sheet, but once you add different currencies and when you start adding/selling positions it quickly became quite complicated and error prone. Now i am using my banks portal but am not really happy as it omits things as dividends from the overall return and once positions are sold the gain/loss disappears completely. Anyhow, if you have any recommendations on that point that would be great. Thank you.

Hi, I don’t use any software but an excel sheet. it is clearly more work but also flexible enough for my purpose.

Hi T, have a look at the tool Portfolio Performance (https://www.portfolio-performance.info/en/). It offers many or all features you are looking for.

What a decade it has been! I think you show through your post how much you developed as an investor through this bull market and very impressed with your returns given that it has for sure not been value investors decade. Thank you for all the great posts and thoughts over these years. I really enjoyed your all German stocks series you should do a follow-up on that where you take your watch-list and zoom down on 2-3 of the most interesting stocks.

Thanks. Some narrowing down is reflexted though in my portfolio ….

Congrats for your wonderful blog!

I have a question regarding “7. Try to limit “information intake” to high quality sources” and your point; “I think reading high quality news sources and a good network of fellow minded investors are a much better starting point for finding interesting stocks than a screener.”

What are your 5 or 10 most important “news sources” (regarding the amount of time you spend reading them)?

Thanks!

lear99,, I guess that would justify a separate post.

I pay for FT (electronic) and Economist (Paper & Electronic). I stopped paying for the WSJ as it is too much US focused and allocate a significant amount of reading time on these 2.

Excellent review, as expected! crisp on the actual (performance) numbers, more qualitatively content/review

Good point. I should have written: “Let winners run if fundamentals develop positively”….

Nice job throughout these years, and continuing to actively blog about it all this time. I hope to be able to continue reading about your journey in investing in the next decade as well! 🙂

Congratulations! Strong metrics and more important to me: your investments actually are consistent with the narrative you create – too many investors, especially pros, talk a story and then do something else…

On your outlook:

“Let winners run” has obviously been rewarded in the last decade, but historically it is not as good a strategy. The obvious cross check is to decompose the return for fundamentals (E or B or CF), multiple expansion and yield. Fully aware this would have hampered returns recently but anyhow…

Good luck for the next decade!