The “All Swiss Shares” Series Part 1 – Nr. 1-10

Introduction

After the great fun of doing the “All German shares” Series in 2019/2020, It is time to start the new “All Swiss Shares” series in 2021. According to the Swiss Stock Exchange, there are currently 220 Swiss based listed companies, so the series will be a little bit shorter. The reason for choosing Switzerland is that I actually own already two Swiss based companies (Richemont, Zur Rose) and that I think there is an interesting mixture of companies in Switzerland, several of which I have covered over the last 10 years.

Again, mostly for my own entertainment, I will use a random approach in looking at the companies.

One difference to the German series is that I’ll try to better define what I am looking for. In principle, my portfolio comprises three different styles/buckets:

- “Long term holdings” – Stocks where I think there is good long term potential. For this group, I require high quality with regard to the business model, leadership and balance sheet

- “Value Trades” – Stocks where I think for some specific reasons there is a significant undervaluation that will materialize in a period of up to 3 years. This could be a “sum-of-part” situation, a spin-off, activist involvement or another situation where I think that I can identify the reason for the undervaluation and where I have a different view. Due to the shorter time horizon, the requirements for “quality” are a little bit lower.

- “Special situations” – in my definition, special situations are based on corporate actions (M&A, Squeeze out etc.) where the potential outcomes are clear and the main task is to assess probabilities and an expected value.

So now let’s jump into the first 10 stocks. Surprisingly, I found already 4 stocks worth “watching” out of the first batch.

- BVZ Holding AG

BVZ Holing is a 170 mn CHF market cap company that seems to be active in local rail transportation, real estate and also touristic mountain cable cars, among them the world famous “Glacier Express” and the “Gornergrat” cable car at the world famous Matterhorn.

Covid-19 clearly had a big impact, the net result in 2020 declined from 20 mn in 2019 to -7 mn in 2020. The company owns a significant real estate portfolio but also employs some debt and seems to have ordered a lot of new equipment.

Looking at the stock price we can see that the stock hasn’t recovered that much sicne the beginning of the pandemic:

Maybe this has to do with the fact that a significant part of the Swiss tourism seems to depend on rich Asians who can and want to afford Swiss prices. I just checked and a return trip onto the Gornergrat from Zermatt costs a juicy 80 CHF per person. This (German language) analysis shows that the growth in recent years until 2019 was clearly driven by Chinese visitors.

I think for the time being it is open when especially Chinese tourist will be back, maybe next year but certainly not this year. On the plus side, the company clearly has unique assets.

For investors with more time to dig into the assets, BVZ might be interesting, for me it is a “pass” as I don’t really look for asset plays and this would require too much time.

2. Carlo Gavazzi AG

Gavazzi is a ~150 mn CHF market cap manufacturer of electric and electronic components and sensors for a variety of uses among them industrial automation and buildings. What is interesting at first glance is the fact that Gavazzi has a strong net cash position (~45 mn CHF) and actually increased profit in the Covid-19 year with stable top line.

On the other hand, the company didn’t show any growth in the last 4-5 years and return on capital and margins are relatively low. Therefore I’ll “pass”.

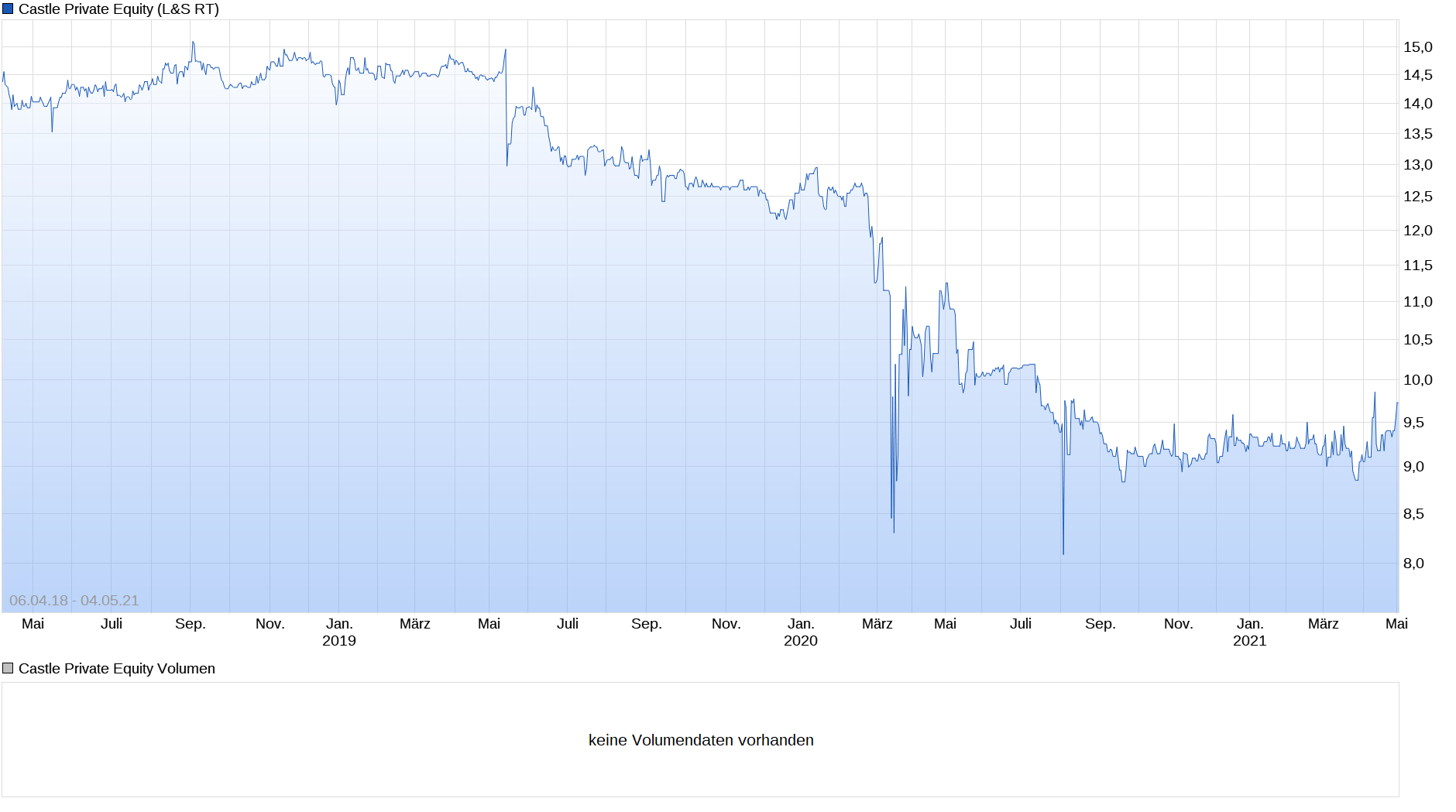

3. Castle Private Equity AG

Castle is a 110 mn CHF market cap listed investment company that invests into Private Equity (not Castles…). The underlying portfolio is a mixture of buy-out and venture capital with a very global distribution. The largest country exposure seems to be India. The most recent NAV released is at around 15 CHF which would mean that at the current 11 CHF per share, the stock trades at a significant discount to NAV.

Looking at the stock chart one can see that Castle didn’t recover from the “Corona crash”:

According to the annual report, Castle seem to be in “harvesting” mode, i.e. they do not make any new investments but pay out whatever is distributed from the underlying funds (via distributions/share buy backs). Around 35 mn USD cash is held by the company. The performance of the portfolio seems to have been quite disappointing, with low single digit returns over the past few years which clearly is below any PE/VC benchmarks.

As I am nor really a specialist in liquidation situation, I’ll “pass”.

4. Schweiter Technologies AG

Schweiter is a 2,2 bn CHF market cap company that produces a variety of composite panels. According to their IR presentation, M&A is part of the growth strategy, having acquired 18 companies in the last 20 years. The long term stock chart looks “constructive” with a clear value creation over the long term:

The company seems to have had little impact of Covid-19 with stable sales in 2020 and increasing margins. EBITDA margins in 2020 were 15%, EBIT margins still above 10%. The company is conservatively financed (net cash).

One of the areas where they are active is supplying material for blades of wind mills which sounds interesting. Based on 2020 profit, Schweiter trades at 20x trailing earnings. The largest shareholders seem to be the Frey family, who also were big shareholders in Zur Rose but sold much too early.

Based on this very first assessment, Schweiter Technologies is a candidate to “watch” as a potential long term play.

5. Starrag Group AG

Starrag is a 144 mn CHF market cap manufacurer of steel working machinery. The company got hit hard by Covid-19 with significant reductions in sales (-30%) and orders (-50%). The company seems to have struggled before with ROE in the low single digits and declining sales and earnings, the stock has been moving sideways for the last 15 years.

Nothing to see here for me, “pass”.

6. Romande Energie Group SA

Romande is a 1.4 bn CHF regional utility. Interestingly, 2020 was a very good year for them, almost doubling their profit to more than 80 mn CHF. According to the investor presentation they are very active in renewable energy and are expanding into France.

Romande also ownes ~10% on a look through basis in Alpiq, another Swiss utility that seems to have turned into profit from a deep loss in 2019.

Technically, the stock looks cheap with a Book vlaue above the current market value, on the other hand, the stock has been trading sideways for the last 10 years.

As an electric utility that owns both generation and networks, the future with an increasing degree of electrification could be interesting. Therefore I’ll put Romande on “watch” as a potential “value trade”.

7. Swiss Prime Site AG

Swiss Prime Site is a 6,8 bn traded real estate fund. According to the 2020 results presentation, the stock trades near the NAV. They seem to have a diversified Swiss property portfolio, however as I am not a big fan of listed real estate in general, I’ll “pass” without any deeper research.

8. U-Blox AG

U-Blox is a 435 mn CHF “fabless” semiconductor company which means that they do not produce chips themselves but only design them. They are specialized on designing chips for global positioning and seem to focus a lot on IoT and Industry 4.0. 2020 was not a good year for them, however Management seems to be optimistic for 2021. According to their projections (5-15% revenue increase, 9-15% EBIT margin), the stock would trade at around 10xEV/EBIT for 2021

On the negative side, revenues seem to have peaked in 2017 and were on the way down already since 2017 which explains the stock performance in the last few years:

Although I am not an expert on semiconductors, I think the stock is worth to “watch” as a potential “value trade”.

9. Energiedienst AG

Energiedienst is 1.13 bn market cap Hydropower utility that I owned and covered several times during the last 10 years. I bought it at 29,5 CHFs in 2014 and sold it at CHF 30,50 in 2015. Looking at the stock chart we can see that only very recently Energiedienst manage to come back to the level when I sold them in 2015:

This might have to do with an increasing electricity price as Hydropower is mostly a “pure play” bet on electricity prices and Energiedienst, mostly located on the German border is directly influenced by German electricity prices:

Like for Romande, 2020 was a pretty good year for Energiedienst. As I do like “Green” electricity producers and networks, I will put them back on the “watch” list as a potential “value trade”.

10. Berner Kantonalbank AG

Berner Kantonalbank is a 2 bn CHF market cap regional bank, majority owned by the local district Bern. The bank seems to be a very conservatively run bank with little observable volatility and a decent dividend yield of ~4% which is very high especially in Switzerland.

ROE is at around 5%, the stock has been moving sideways for a long time. As I am not such a big fan of bank stocks and dividends are not really relevant for me, I’ll “pass”.

To be continued…

A funny stock here will be SNB ! Besides those funny stocks, little/no CH company truly fits TerrySmith’s criteria (Geberit and maybe Partners, and Nestle in the past)

Oh ! I forgot: maybe Givaudan (wonderful company with BillGates the largest shareholder), Sika or Schindler (Fundsmith has Kone) and some Luxury brands as Richemont (Fundsmith has LVMH)…

Great project! I hope you get a lot out of it and have some fun along the way.

At U-Blox you have to watch out for the egregious cost capitalization. In my view their EBIT number is worthless. The last few years they were a fundamental short seller’s “gift that kept on giving.”

Ok, thanks for that hint. So they are a “weak” watch list candidate and that might explain the “cheap” valuation.

Super great topic!!! One might add to Energiedienst their special dividend payout situation. If I remember right, it is paid according to German tax rules and not Swiss ones. So you do not have to reclaim it from the Swiss tax authorities. Sounds strange, but I think it was something like this.

For me hbm healthcare is the star of the Swiss exchange for many years. In addition: partners group, sika and Lonza.

Great posts, these. Modern day version of going through the Moody’s manual. I find it to be an underrated but indispensable source of idea generation. Many thanks.