All Swiss Shares series Part 2 – Nr. 11-20

And the next batch of randomly chosen Swiss stocks, however this time I only identified one potential “watch list” candidate.

I do have to say that I enjoy this kind of research a lot. After looking now at 20 stocks so far I have to say that reporting quality is generally a lot better than for German companies, independent from the size of the company.

11. Varia US Proporties

Varia is a listed property company that only invests in US real estate with a market cap of ~380 mn CHF. They seem to own a diversified portfolio of resdidential units. The company seems to be a “yield vehicle”, with relatively large distributions but little increase in NAV. As I am not a fan of listed real estate in any case, I’ll “pass”.

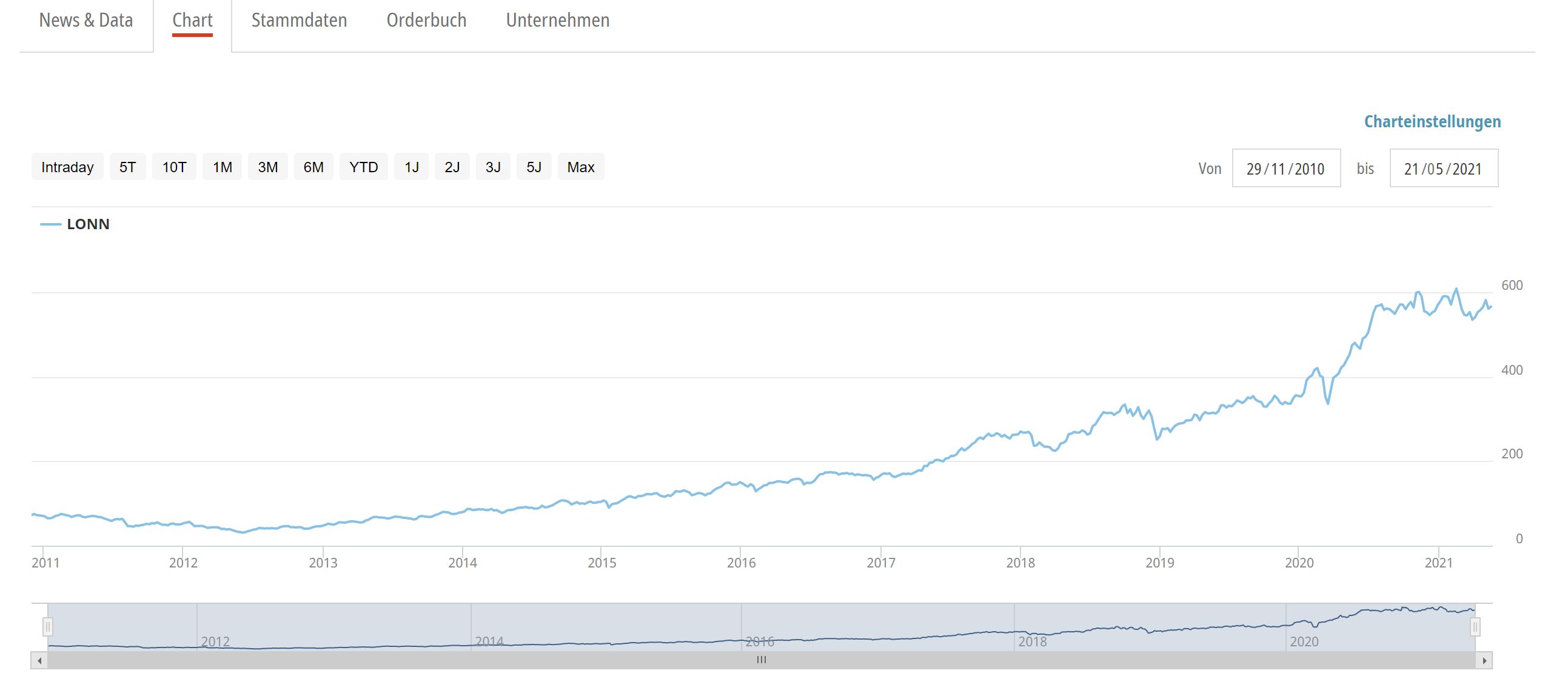

12. Lonza Group

Lonza is a 42,3 bn CHF “large cap” chemical and pharmaceuticals Group. What makes the company interesting is the fact that over the last 10 years, the share price has risen by around 10x:

In 2020, the company achieved sales of ~4,5 bn CHF with an EBITDA margin of around 31%. So the stock is definitely not cheap. Lonza seems to manufacture special ingredients for other companies, for instance Moderna.

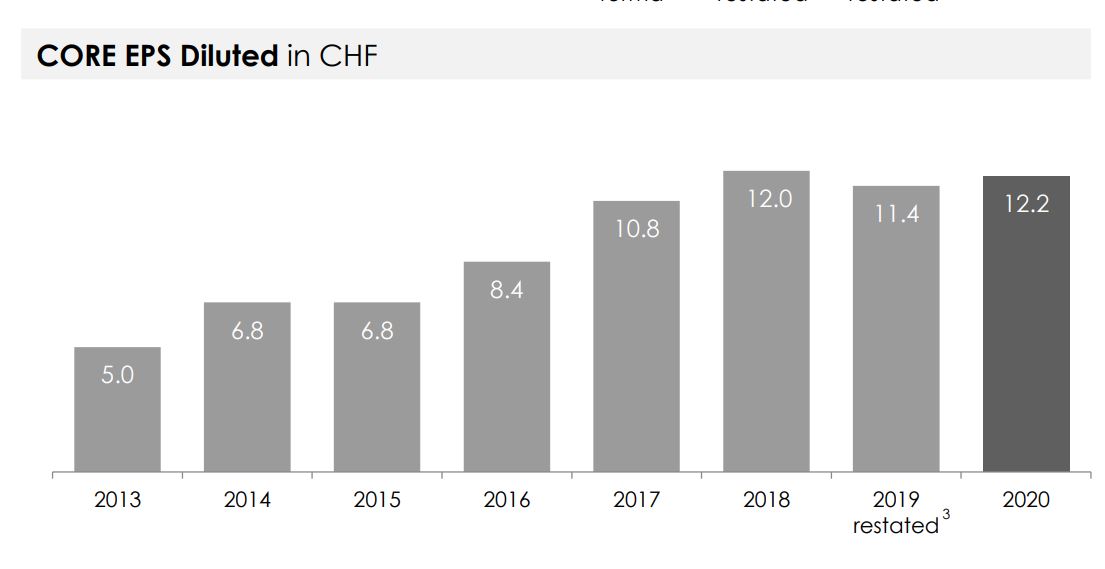

Interestingly, this 10 fold increase has been achieved by relatively moderately increasing EPS over the last 10 years:

According to their 2020 prwsentation, they plan to grow double digit until 2023. Nevertheless, with a trailing P/E of around 60 or around 47 in 2023 the company looks fully valued.In addition I do not know that much about the sector. Maybe they have created unparalleled intellectual property but I guess I will not be able to asess this, therfore I’ll “pass”.

13. CPH Chemie + Papier Holding AG

CPH is a 370 mn CHF market cap company that is active in chemicals, paper and packaging. Paper is the largest division and seems to be struggling. Chemicals seem to do ok, packaging however seems to be the “crown jewel” with rising sales and high BEITDA margins (>20%).

On the plus side, the company is debt free and quite cheap (below book value, . I found an interesting German language post about the company which stresses that they are a “sustainable” player in the paper market.

The long term chart looks not too nice which most likely is the result of the structural issues in the paper market:

At a very first glance, I do like the fact that there sems to be a “hidden gem” in this otherwise very boring company.

The company is majority family owned and seems to be not very well known. I’ll put them on my “watch” list.

14. Banque Profil de Gestion

This bank is a small, 32 mn CHF market cap wealth manager. When I started to read the annual report was quite surprised: The Chairman states that the bank is too small and that they need to merge in order to obtain the required scale. They seem to pay a special dividend and then merge with another bank. I have not fully understand when that happens but I am also not too interested into digging deeper, therefore I’ll “pass”.

15. Lindt & Sprüngli AG

Lindt is a company that doesn’t need a lot of explanation. With 21,3 bn CHF market cap, the company is one of the larger Swiss company. With a stock price of around 91.000 CHF ist is also one of the most “expensive” stocks in Europe. I guess Lindt will not be traded that often on platforms like Trade Republic…

In 2020, the company had ~4,5 bn in sales (-6% in CHF yoy) . The years before, Lindt managed to grow mid single digits each year. EBIT declined ~-30% yoy, net incpome by almost -40%. It seems that a significant part of Lindt’s business depends on physical retail (own shops, airports) which is not compensated via online sales.

The share price, apart from a short dip in March 2020 is completely unimpressed of the 2020 numbers:

Based on 2019 earnings, the stock trades at a P/E of around 45x which is clearly more than I would be prepared to pay. However investors seem to be very convinced that Lindt will recover quickly and move back to single digit growth. Even at the depth of the Covid-Crisis the stock didn’t trade below 35x 2019 P/E. Unfortunately a “pass” for me.

16. Crealogix AG

Crealogix AG is a 165 mn CHF market cap software company that offers solutions for banking and wealth management. According to the half year report, the company had 6m sales of around 50 mn CHF and managed to grow by 8%. As many other software companies, Crealogix tries to move to a SaaS model, with currently around 25% of sales that are already SaaS based. Overall recurring revenue share is ~50%.

On the plus side, the company has no debt. Unfortunately, the company is not very profitable with around 1 mn EBITDA for the first 6M 2020/2021.

According to the report, they expense all R&D, but still the share of salary expense indicates that their software seems to be quite client specific.

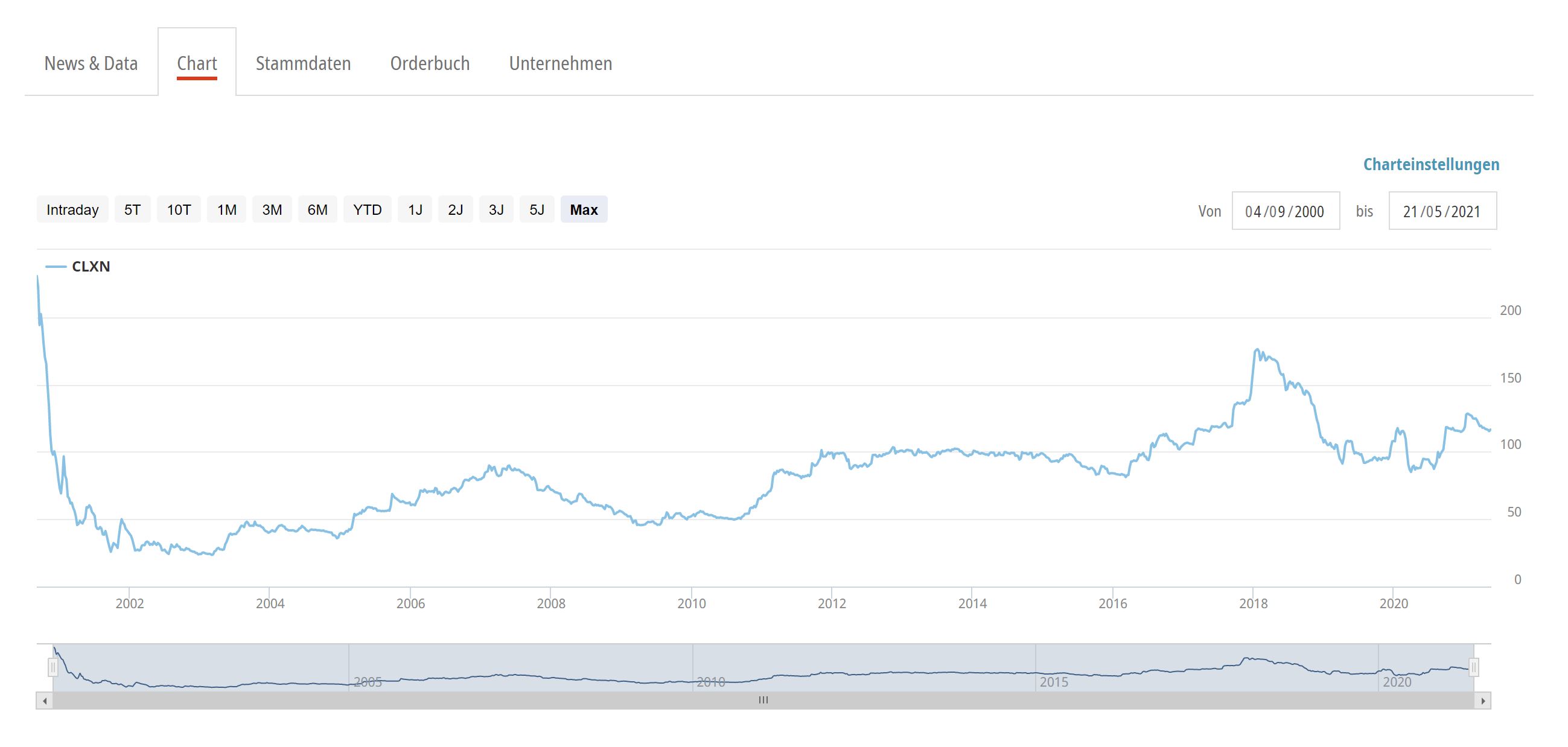

The long term chart shows that they never reached their IPO price from 2000:

An article from 2014 shows that back then they were already trying to transform themselves into a more profitable “platform” company but that didn’t work that well. To be honest, I do not know what should be different this time.

Although the SaaS story could be interesting, I’ll “pass” nevertheless.

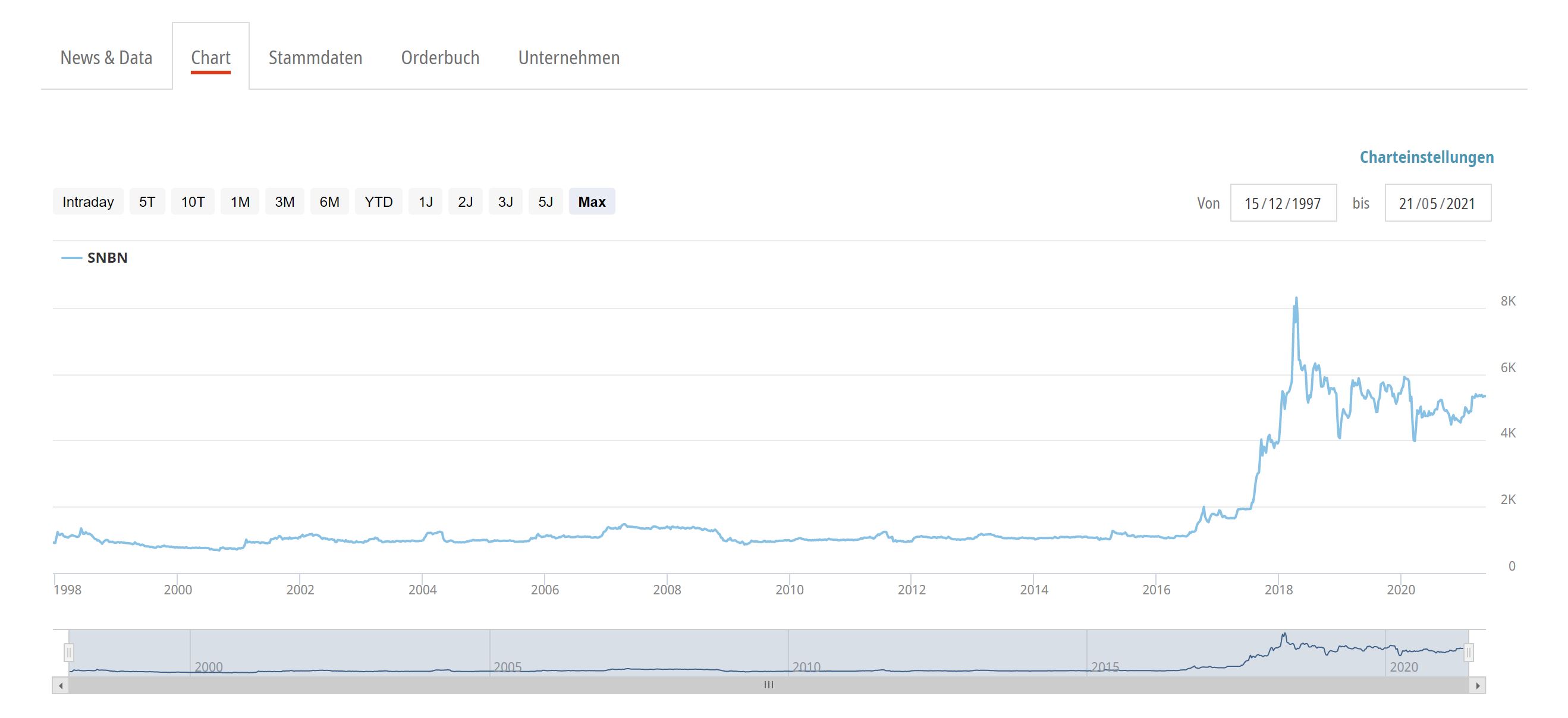

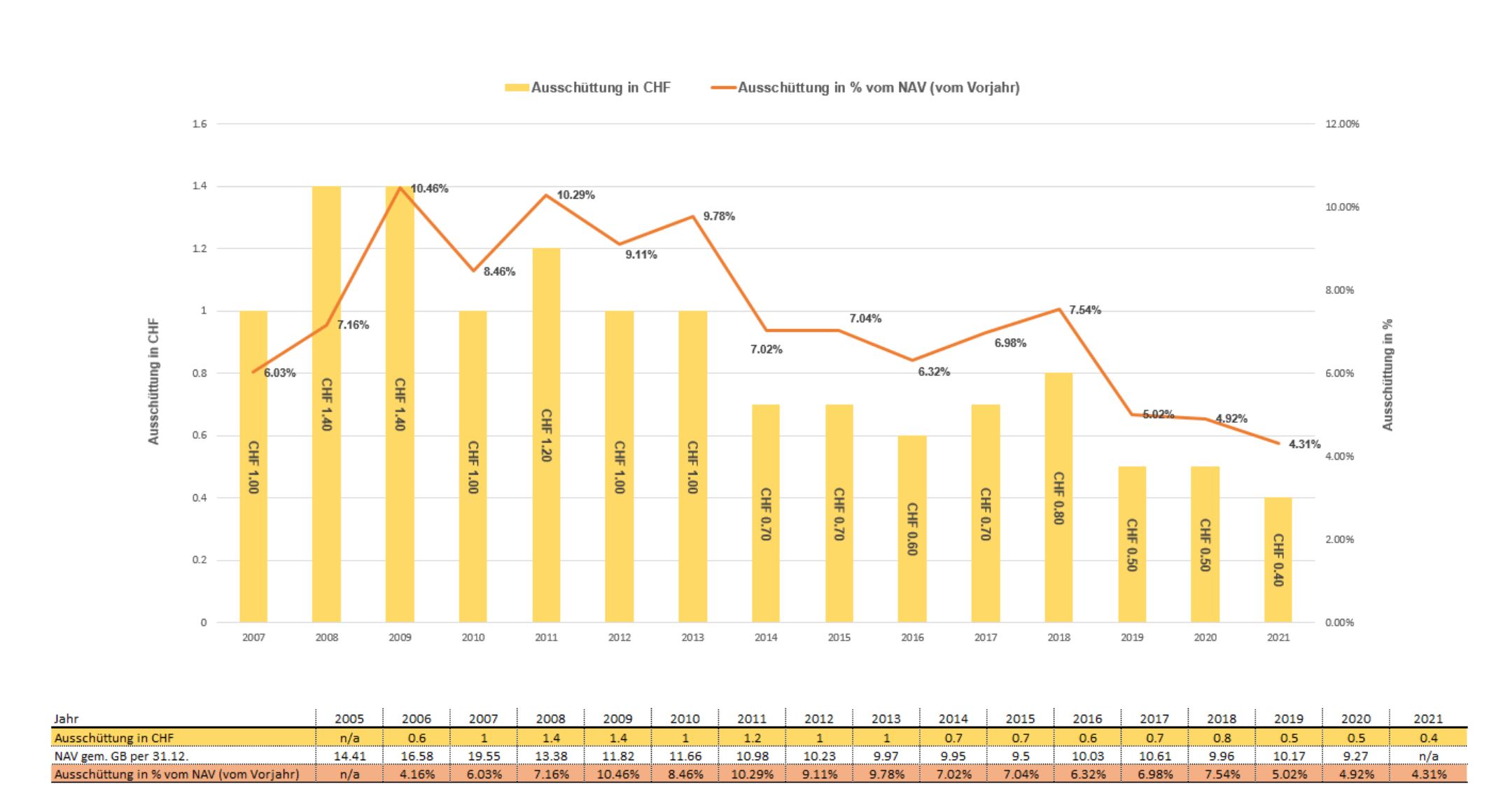

17. Schweizerische Nationalbank

The Swiss National Bank is actually as the name says the Swiss central bank. Funnily enough it is not the only publicly listed central banks, the belgian central bank is listed as well as I have covered it in a 2012 blog article.

The SNB stock is not really a stock as shareholders have no voting rights and no rights on the profit of the company. It is rather a perpetual bond with a 15 CHF guaranteed dividend.

Since I wrote the post, the stock went up by more than 5x as we can see in the chart, especially starting in 2018:

I never really followed up why the stock went up so much especially in 2018, maybe some investor believe that they might be entiteled to more than the 15 CHF dividend. Although the low interest rates certainly have driven part of the price increase.

As these days everything can be valued at stratospheric levels, I’ll happily “pass” as I do not want to be long a perpetual bond with a 0,2% yield in CHF.

18. Nebag AG

Nebag is a 90 mn CHF market cap company that itself invests into small Swiss companies, most of them listed. They publish daily NAVs which is a big plus and explains why the company trades relatively closely to NAV. They do have some quite concentrated positions in smaller Swiss companies.

They also distribute significant dividends, on average around 5% p.a. of NAV. However, there has been very little capital appreciation in the last years as this chart from their web site shows:

I think the company is worth to follow in order to learn more about Swiss small caps, but as an investment I will clearly “pass”.

19. Jungfraubahn Holding

Jungfraubahn, which translates into “Virgin Canle Car” is a 833 mn CHF market cap is another listed cable car company that runs cable cars on mountains in Switzerland, including the famous “Jungfrau” peak. 2020 was not a very good year for them, but in prior years they also showed decent increases in activity.

The share price has recovered nicely from both, a March 2020 and a November 2020 low:

On the plus side, the company seems to have little debt and is quite profitable, having achieved ~100 mn in EBITDA in 2019 on sales of roughly 220 mn CHF. However, similar to BETT, I do not feel really comfortable in evaluating these kind of businesses as there is clearly also a very important “real estate” factor to consider. If I would not have a day job and time to spen, I would love digging deeper into such a company.

Despite the fact that I like the mountains and skiing a lot, I’ll “pass” on Jungfraubahn.

20. Bank Linth AG

Bank Linth is a 495 mn CHF local bank that I had never heard of before. The bank is majority owned by the Central Bank of Liechtenstein. At first glance, the bank looks solid but not very exciting. They trade close to book value and earn around 5% ROE with little observable volatility. Top line has been shrinking for some time but due to very low write-offs, the bank could keep their profitability.

From the outside, this looks more like a utility than a bank. Nevertheless, a “pass” for me.

Interesting to see how different a course the Belgian National Bank share price has taken compared to the Swiss National Bank.

CPH will merge with it’s biggest shareholder Uetikon. CPH has fared bad this year if you look at the share price.https://finance.yahoo.com/quote/CPHN.SW?p=CPHN.SW&.tsrc=fin-srch

Interesting to me is the pharmaceutical blister company within CPH’s packaging division (the hidden gem) P/E < 8

Switzerland is the place in Europe with the largest density of “Finance-employees” (Luxembourg gas no real stock market). Hence and without surprise it will be very difficult to find any opportunities here, beyond those I mentioned.

Well, let’s see. I won’t give up that easily. And It is fun.

And in German I would say the following: “Der Weg ist das Ziel”….

Well… some people are in closed loops… :-s

thx for another great series…. Bought a starter position in CPH, like the way they are moving the company and what is not to like about the balance sheet.

Even within the paper division, the recent price increases have to help and as i understand it, they are using a lot of recycled paper as a commodity.

One to tuck away and buy bits more in dips if they keep performing. Also the current timing and share price historically low