All Swiss Shares Part 13 – Nr. 121-130

Back to Switzerland with 10 “fresh” and randomly selected Swiss stocks. This time, 5 of the 10 stocks might be worth to watch after a first analysis, although I need to slim down my watch list to a more manageable number at some point in time. Enjoy !!

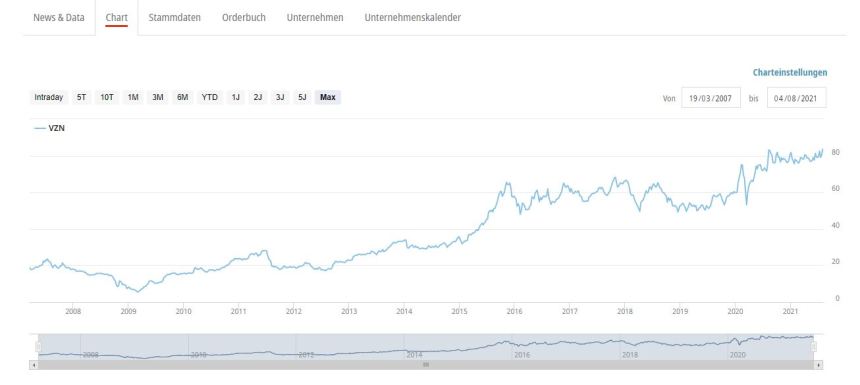

121. VZ Holding

VZ Holding is a 3,5 bn CHF market cap financial services company, that in contrast to most other Swíss financial companies seems to been able to create some long term value over the last years:

VZ is an Asset advisor/manager and there is a very decent write-up available from Verus Capital (in German).

The stock is valued at around 24x which is not too expensive for a growing Asset advisor / specialist AM. Although it really needs to be seen if and how they can scale the business outside of Switzerland.

This is clearly a candidate to “watch”.

122. Flughafen Zuerich AG

Flughafen Zuerich is, as the name indicates the operator of the Zurich airport and has a market cap of around 4,46 bn CHF. A look to the chart shows, that after a long bull run, the stock has been struggling already before Covid-19 hit in March 2020:

Around 40% of the shares are owned by the Kanton and the City of Zurich. In 2020, sales decreased by -50% and prift swung from +300 mn to -70 mn CHF.

Based on 2019 earnings, the stock would trade at 15x which would be cheap, however the big question is if and when business returns to normal for the whole aviation industry.

The company ramped up leverage significantly in 2020 by almost 900 mn CHF, however around 500 mn of this has been “parked” by year end as cash and deposits.

Overall, i am not convinced that Flughafen Zuerich would be the most attractive option in the tourism/aviation sector, therefore I’ll “pass”.

123. Basellandschaftliche Kantonalbank

This seems to be the little sister of Basler Kantonalbank (Nr. 110) with a market cap of 520 mn CHF. The stock chart is a “flat line” fro many years. No reason to spend time here, “pass”.

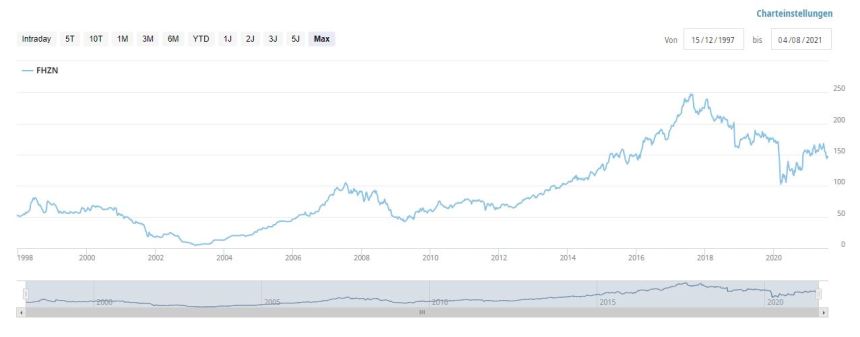

124. Logitech International SA

Logitech, a 17,1 bn CHF market cap manufacturer of computer peripherals is clearly one of the big winners of Covid-19 and the trend to Home office and Home schooling etc.

The stock chart shows the impressive run of Logitech from March 2020, increasing by around 3x:

Sales in Fiscal 2020/2021 almost doubled (I even ordered a Logitech Webcam myself), margins expanded and as a result net income more than doubled to 5,5 USD/per share. With a trailing PE of 20, Logitech doesn’t look expensive, but again the question here is how sustainable that boom will turn out to be. Personally, I am not planning to buy more equipment for the next years to come….

The first quarter of fiscal 2021/2022 again showed decent growth but the company itself guides rather cautiously for the current year.

Overall I am not sure if they will able to grow much in the coming years, therfeore I’ll “pass”.

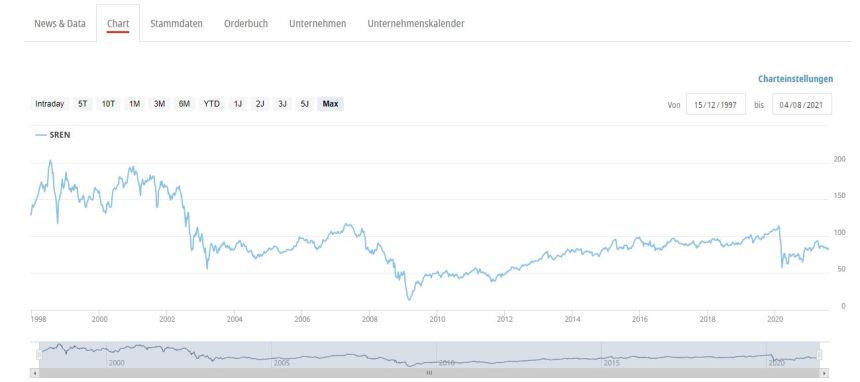

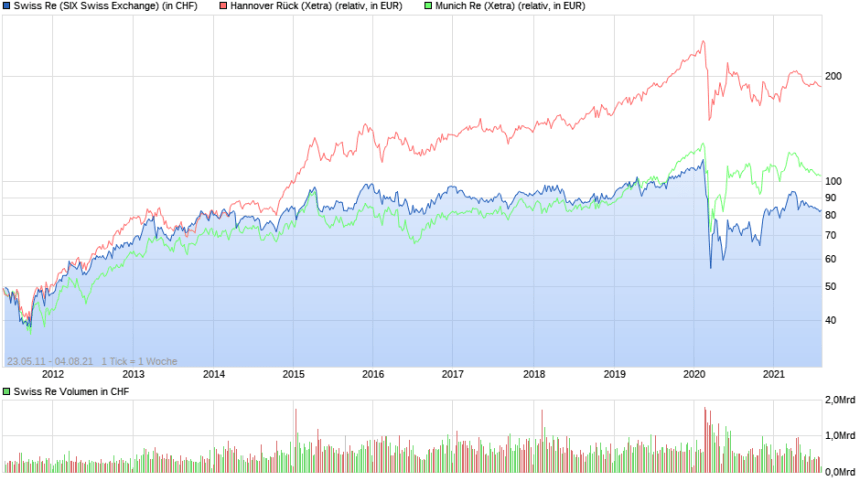

125. Swiss Re

Swiss Re is the worlds largest reinsurance company measured by premium and has a market cap of 26,3 bn CHF. The long term chart doesn’t look very encouraging:

Fundamentally, Reinsurers have to battle low interest rates which reduces the amount they can eanr on the float, less demand from increasingly diversified Insurance companies and “regular catastrophic events”, be it natural desasters or the pandemic. An increase in inflation with low interest rates is also nto a very good scenario for the porperty and casualty business line.

On the plus side, I consider Swiss Re to be one of the more innovative players.

In 2020, Swiss re booked a -800 mn Loss after a 900 mn loss after a 700 mn profit in 2019. Also in 2017 and 2018, Swiss Re only to managed 300 to 400 mn CHF per year. One has to go back to 2015 and 2016 to see net income that goes into the billions. Interestingly, investment income is not really to blame for these declines but rather a combination of higher claims and costs.

It is really difficult to say what the true “earnings power” of Swiss Re could be. Especially as the German competitors Munich Re and especially Hannover Re have been doing much better as this chart shows.

Nevertheless, I think it makes sense to put Swiss Re on “watch” to understand if there is some light at the end of the tunnel.

Nevertheless, I think it makes sense to put Swiss Re on “watch” to understand if there is some light at the end of the tunnel.

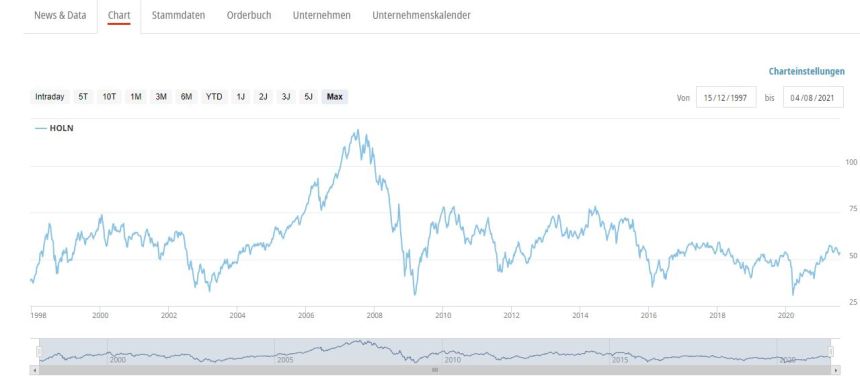

126. Holcim AG

Holcim AG, a 32,6 bn CHF market cap company, is the result of a merger between the French Lafarge Group and the Swiss Holcim Groupin 2015 which created the biggest global cement company. Looking at the stock chart, it looks like that they have bean “threading water” for the last 30 years:

Just a few months ago, they dropped the “Lafarge” part in the name which clearly shows which part of the merger of equals has gained dominance.

Despite lower sales in 2020, net income has been quite resilient. One of the most interesting aspects is clearly the fact that former SIKA CEO Jan Jenisch has become CEO of Holcim and tries to repeat the “SIKA playbook” at Holcim, giving subsidiaries more freedom and focusing on value add products.

One big future issue for Cement makers are clearly the significant CO2 emissions that are part of the chemical processes that produce cement. However it looks like that Holcim is the leading player here with the lowest CO2 footprint which could become a competitive advantage in the future.

Overall, this is clearly a stock to “watch”.

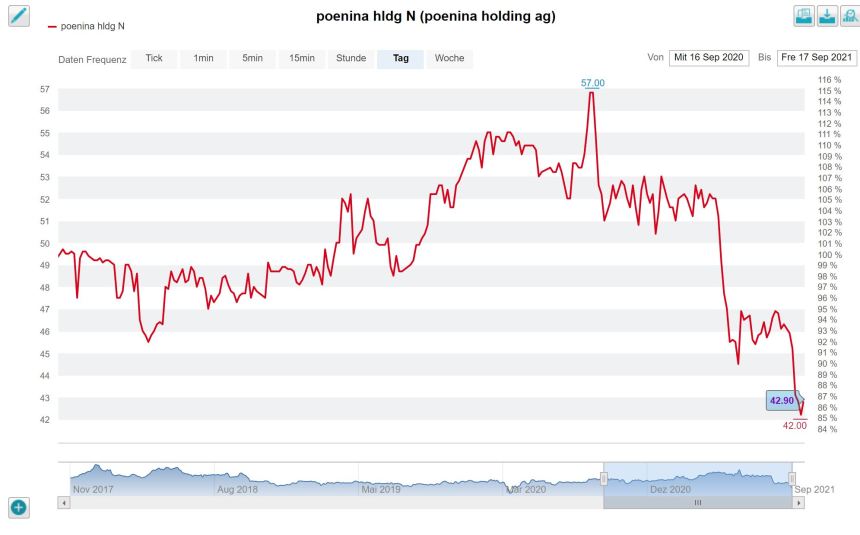

127. Poenina Holding AG

Poenina is a 250 mn CHF market cap company that is active in the building/construction sector. Just a few weeks ago, the long time CEO (and 20% shareholder) just has been kicked out as he seems to have been involved in a big scandal in Switzerland some 12 years ago.

This was clearly not helpful for the share price which reached an all time low just a t the time of writing:

In 2020, the company did surprisingly good, however the numbers are hard to interpret as the company merges with a competitor (Caleira AG) which triggered a capital increase. With an expected PE of 15, Poenina is one of the cheapest stocks in Switzerland, however the business is rather low margin and they seem to “roll up” the sector in Switzerland. EPS in 2019 was slower than in 2017 despite a significant increase in sales.

Looking at their main segment, Poenina might be a competitor for Meier Tobler especially in the areas of heating and cooling. Therefore I’ll put the them onto my “watch list”.

128. Bergbahnen Engelberg-Truebsee-Titlis AG

BETT is a 155 mn CHF market cap mountain cable car company that as its peers has seen better days due to Covid:

BETT is also somehow famous, because Rob Vinall has/had a position in the stock and is hosting his annual conference there. He outlined the thesis in his 2014 half year letter. Part of the business case were Chinese tourists who clearly are missing now, but might come back in the future. When you missed out on BETT back then, you can now buy at a slightly higher valuation than Rob bought it.

Although no one these days knows when and how long distance tourism will develop. In any case, I’ll put BETT onto my “Watch” list.

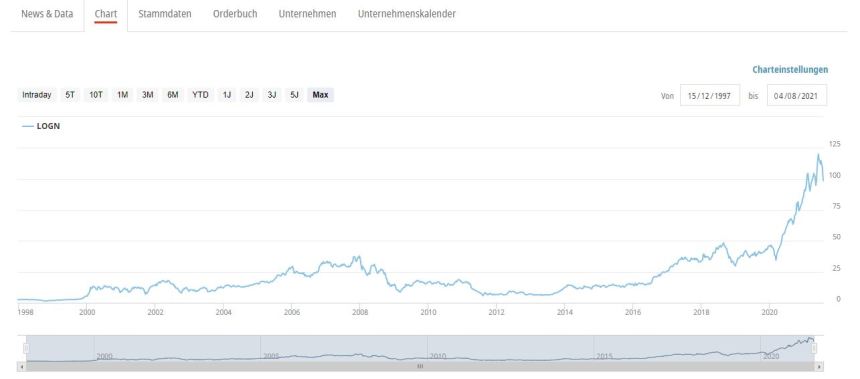

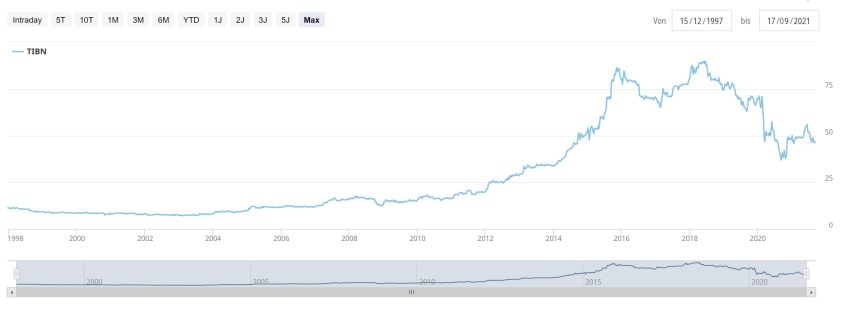

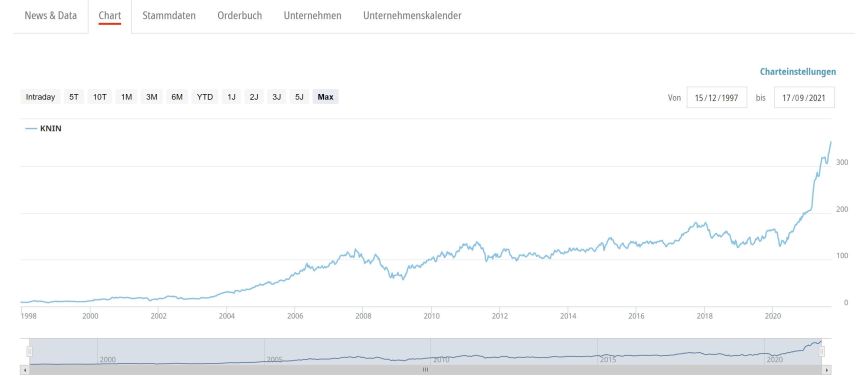

129. Kuehne & Nagel AG

Kuehne & Nagel is a 43 bn CHF market cap logistics company. I have to admit that although I have seen their trucks rolling over German “Autobahns” many times, I have never looked at the company. Billionaire Owner Klaus Michael Kuehne, who still owns ~54%, is one of the richest Germans and also infamous for sinking a lot of money into Hamburgs soccer club HSV without any or even negative effects.

What I find very interesting is the fact that the stock, after doing nothing for almost 15 years, more or less trippled since the beginning of the Covid crisis as we can see in the chart;

Indeed, Kühne was not negatively effected by Covid and earnings were relatively unchanged at around 800 mn CHF, however it is not clear to me why the stock now trades at 55x trailing PE which is a lot for a 4% net margin stock. My only explanation is that some investors consider this to be an infrastructure play which then would mean that investors consider the business as being not very risky.

For me, the stock looks not attractive at this valuation and I don’t understand enough of the business, therefore I’ll “pass”.

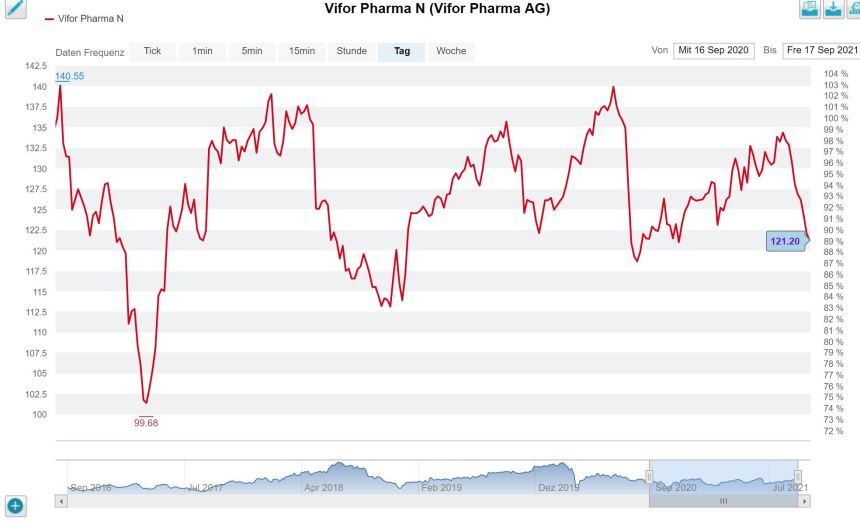

130. Vifor Pharma AG

Vifor is a 8 bn CHF market cap company that I have never heard of before. It seems to have been a spin-off from Galenica in 2017.

The stock is trading since then in a strangely narrow range as we can see in the chart:

The company seems to specialize on iron deficiencies and kidney / heart treatments. The Iron deficiency business seem to be nicely growing. The stock looks relatively cheap on an EV/EBITDA basis (13x for 2021), but there seem to be significant minority interests. Trailing P/E is at around 40x. “Pass”.

Very interesting (i.e., reinsurance comments). Reinsurance always seemed liked a tough business, given the competition, the low yields on balance sheet reserves and the large tail risks.

Also as an internal, just sharing my two cents. SwissRe has undeserved reputation from the very old days. Some good talent indeed, in a sea of mediocre very greedy people. Many of them banking on swissiness (like this would bring value, per se).

Corso was run down and obviously they replaced Galvani way too late. The crony gang of Kielholz, primarily served his interests, with outright nepotism: Chairman of BoD promoting his god-son to CEO. Yes, Mummenthaler is Kielholz’s god-son. “Conflict of interest”, we do not know this concept at SissyRe.

They should also get reckognised for burning 1bUSD on the ATLAS project. Bringing the company nowhere, except for big mgmt bonuses. Mediocre’s epiphany moment is described here https://insideparadeplatz.ch/2021/02/19/swiss-res-pleite-mit-projekt-atlas/

The best SwissRe creation in the last 15 years was a pure marketing idea: ‘protection gap’. They have been fooling investors by miss-estimating the real TAM and pretending that they could grow businesses to unrealistic market segments. Reality is that Primary Insurers are every year more diversified, requiring less reinsurance. Most internal innovation projects are RocketScience, with hardly any tangible benefit.

SwissRe’s ultimate aspiration is keeping statusquo. That’s why they brought in Ermotti, another old acquaintance of the cronny Swiss marketplace.

When a SwissRe shares yield > 5%, it because they have nothing else to offer.

As a Holcim insider just noting that Holcim spent handsomely in Lafarge, when Lafarge net value was zero (realistically it was negative). Their cement plants were a mess, no maintenance, poor quality, and on top of that serious reputational and legal issues.

Cement is an capital intensive industry, that destroys value when considering WACC vs RoE or RoCE.

Due to its intrinsic nature, cement business were only profitable in monopoly situations (where profit margins without competition). This was the case in the 1980-2007…. But after financial crisis, and anti monopoly governmental activity, cement business is over.

No surprise that Founding family Schmidheiny jumped off the boat years ago.

I really like this post series – concise and informative. How do you catch up so fast on the recent narratives of all those companies listed in foreign markets? Just reading annual reports/recent filings, skimming last news, or visiting local investing forums?

Cheers!

The most interesting post in months (for me).

Good to know. Sometimes you only get what you pay for 😉

Hi,

I really like this series of posts – fast and informative. How do you manage to catch up with the most recent ‘story’ of so many companies in various industries? Simply reading annual reports, doing some fast news checkups, or visiting local investing forums?

Cheers!

All of the above…… I start with the IR Website and then look around a little bit. Not 100% structured.

reg. Kuehne & Nagel AG (#129)

My guess is that investors believe in much higher margins due to all the supply chain issues currently