Performance review 6M 2022 – Comment “The Siren’s Song of Fallen Angels and (very) low P/E stocks”

In the first 6 months of 2022, the Value & Opportunity portfolio lost -14,4% (including dividends, no taxes) against a loss of -20,2% for the Benchmark (Eurostoxx50 (25%), EuroStoxx small 200 (25%), DAX (30%), MDAX (20%), all TR indices).

Links to previous Performance reviews can be found on the Performance Page of the blog. Some other funds that I follow have performed as follows in the first 6M 2022:

Partners Fund TGV: -33,5%

Profitlich/Schmidlin: -18,1 %

Squad European Convictions -13,1%

Ennismore European Smaller Cos -2,5% (in EUR)

Frankfurter Aktienfonds für Stiftungen -14,1%

Greiff Special Situation -2,5%

Squad Aguja Special Situation -12,7%

Paladin One -17,0%

Performance review:

Overall, the portfolio was more or less in the middle of my peer group. Looking at the monthly returns, it is clear that June was one of the worst months in the 11 1/2 years of the blog in absolute terms:

| Perf BM | Perf. Portf. | Portf-BM | |

| Jan-22 | -3.7% | -4.2% | -0.6% |

| Feb-22 | -5.0% | -5.3% | -0.4% |

| Mar-22 | -0.2% | 3.4% | 3.6% |

| Apr-22 | -2.1% | -0.3% | 1.8% |

| May-22 | 0.5% | -0.4% | -0.9% |

| Jun-22 | -11.4% | -7.8% | 3.5% |

Looking back, only March 2020 was worse for the portfolio, whereas for the Benchmark, June and August 2011 were worse in addition to March 2020.

Within the portfolio, Naked Wines was clearly a disappointment, losing more than -50% in Q2. However also other high beta positions like VEF or Aker Horizon lost 30-40%. Even counter cyclical stocks like Admiral really suffered although I do not see any fundamental issues there.

My biggest new position, Nabaltec also performed poorly, despite posting much better results in Q1 as I had expected. The problem is here clearly a potential stop of Russian Gas deliveries, which for Nabaltec as an Energy intensive company might mean some trouble, as for other similar companies. Nevertheless, in the long-term, I am convinced that they will do well, especially as their US facilities suddenly become a lot more interesting and strategically relevant.

In relative terms I consider the first 6 months as pretty OK. My goal is not to achieve absolute returns which I think is not possible, but I try to outperform the benchmark on average by a few percentage points per year.

My portfolio has more Beta than in the past as I have allocated less into special situations which stabilize portfolios in such times. Unfortunately I do not have enough time to run a significant allocation towards special situations. They need much more “maintenance” than a normal “boring” long term position.

One quick comment here on the performance of the TGV Partners fund as well as on Rob Vinall’s performance (-40% this year): I think before judging the first 6 Month of 2022, it makes sense to look at the whole track record of each manager. Yes, there are a few guys, often FinTwit “celebrities” whose entire track record has been killed by early 2022. In the case of Rob and Mathias however it should be taken into account, that despite the horrible first 6 month, both have outperformed their benchmark significantly since inception. Both have also “cultivated” investors in a way that they hopefully don’t chase past performance but stick for the long time. On the other hand it must be clear that investing into a highly concentrated portfolio of companies that are supposed to be long term growers, higher volatility needs to be taken into account.

Transactions Q2:

In Q2, I added one new position to the portfolio, Solar A/S a small but interesting whole seller from Denmark that distributes among other things heat pumps and supplies for offshore works. I also added a little to Schaffner in the beginning of Q2. I also added to Nabaltec, only to reduce the position later, but overall I have more Nabaltec than in the beginning of the quarter.

I sold FBD, the remaining part of Zur Rose, Siemens Energy and also Orsted. I also took some profits on GTT (1/10 of the position). In addition (and not yet disclosed in the comments), I also sold my Netfonds position as I think that they might struggle for some time with current capital markets.

Cash is currently close to 15% which is on the high end of what I would be comfortable.

The current portfolio can be seen as always on the Portfolio page.

Comment: “The Siren’s song of Fallen Angels and (very) low P/E stocks”

In the current environment, after the popping of the “growth stock” bubble and with a looming recession, one can read many comments that either “this stock is really cheap now as it is -80/90/95 % down from it’s peak” or “you can’t go wrong with a P/E of 2 stock”.

The first case is usually referred to as a “Fallen Angel” stock, the second one as a “Low P/E bargain” and these situations are quite typical after a big bull run has ended.

“Fallen Angels”

The case for a “fallen Angel” is often like: If you bought Apple/Amazon/Microsoft after the Dot.com crash, you would have made 100/1000x or more. However the big problem is to actually identify the fallen Angels that rise again and, even more important, to have the patience to wait until things get better.

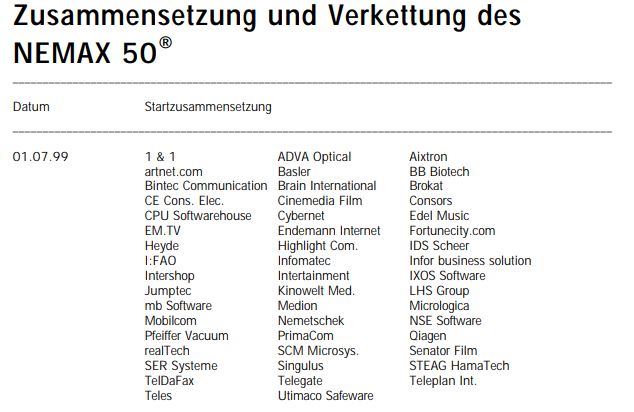

As an example, let’s look at the composition of the NEMAX50, a “German Nasdaq” index from 1999, just when the Dot.com bubble went into full swing:

Most of these 50 companies disappeared, some of them relatively quickly, some faded away over a longer term. Only a handful of them turned out to be “fallen Angels” that were rising again, among them 1&1, Pfeiffer Vacuum, Qiagen and Nemetschek.

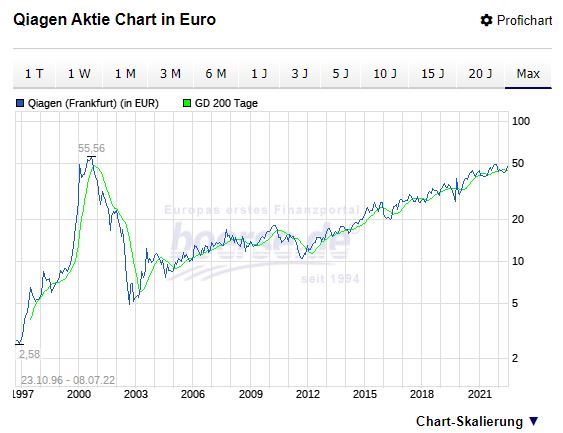

Let’s look for instance at Qiagen, clearly one of the companies who turned out to be long time winners:

Qiagen indeed lost around -90% from it’s peak in late 2000, but from the top (q3/q4 2000) to the absolute bottom it took around 2 years. However if you bought in for instance 1 year after the top was reached at around 20 EUR per share (-63% from the top) , it would have taken a cool 15 years to get to break even.

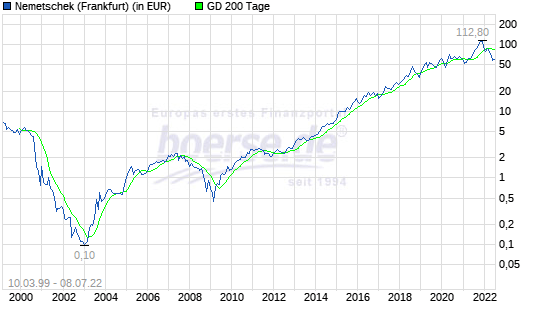

Another example is software company Nemetschek, one of the absolute top performers in the recent years:

Nemetschek IPOed in 1999 and lost ~98% until the end of 2003, only to then increase a 1000x (yes that’s right, a thousand bagger) until 2021.

Again, if you bought too early after the first drop at the end of 2001, you would have seen the stock drop more than -90% and you would have ultimately needed to hold the stock more than 10 years to get your money back.

Buying into Nemetschek in 2003 would have required “balls of steel”. The company had been shrinking for 3 years and just broke even after horrible losses the ears before.

So what is the lesson here for “fallen Angels” ?

- you really be very careful, which Fallen Angel you pick, because a lot of them will just disappear

- Timing is not easy: Getting in too early might really hurt

- Patience is required. Most of these stocks will not do a “V shaped recovery” but more like a pretty long “U”.

(Ultra) low P/E stocks

As mentioned above, the current turbulence have created quite a number of very low P/E stocks. I want two mention just two examples here: Salzgitter AG, the German steel maker trades at 1,4x P/E (yes P/E not P/S) and the US Insurance company Jackson Financial trades at 1,1 trailing P/E.

A lot of investors think that the risk of a bad outcome must be very low because it only requires a few years “to earn your money back” or so.

In my experience, very few “ultra low P/E” opportunities turn into great long term investment opportunities. In order to trade at such a low P/E, a company must have either existential problems and/or very dire profit outlooks. For Salzgitter, in my opinion the problems are very clear: Both, high energy costs and the overall Decarbonization efforts will lead to an incredible amount of investment required for the next 10-20 years.

The profits from last year will most likely be not repeated for the next years and all the cash that is earned will need to be reinvested at unknown Returns on capital invested. Even in the past, only a tiny fraction of the profits reached investors as this chart from TIKR shows that compares EPS and dividends per share:

Of course, in theory the share price of Salzgitter can do anything in the next weeks, months and years, but I do think that there is a high likelihood that Salzgitter will not be a big out-performer as shareholders won’t see any of these profits “in their pockets”. The P/E will most likely go up but mostly to to smaller profits.

Another interesting example is Jackson Financial, a recent spin-off from Prudential (US) that trades at an absurd low P/E. The excellent Verus Blog (in German) has written a pitch and concluded that the stock is so cheap that little can go wrong despite some uncertainties because of a large derivatives book and that maybe the “spin-off” situation has created that opportunity.

I do have a different opinion here. First, it is not only Jackson Financial that trades so cheap but also competitor Brighthouse Financial, which itself is a similar spin-off from Metlife and which is a long term David Einhorn favorite.

Verus Capital is a really good blog, but I do think that he never has had any in detail experience with some of the peculiarities of the US life insurance market. Both Jackson and Brighthouse have issued policies that are much more very complicated financial products than life insurance policies. The actual complexity of these companies is not the derivative book but the insurance liabilities which are almost impossible to analyse and contain lots of pretty significant “short option” exposure.

One big risk for instance is that in a typical US annuity, customers can often take out their capital with little or no penalties after some years. Especially now in a rising interest rate environment, those business models will be under a huge pressure

Another problem is that these companies have almost no “real” capital. looking at Jackson’s latest quarterly record we can see that shareholders Equity is around 9,6 bn USD that needs to support a balance sheet of 352 bn USD, an equity ratio of only 2,7%. On top of that, we find on the asset side ~14 bn USD position called “deferred acquisition cost”. This is in essence “Hot air” as this is a capitalized cost position that needs to be amortized over the life of the policies. Life insurance accounting allows to capitalize acquisition costs which in most other business models is not possible.

So “tangible” equity for Jackson is actually negative. In addition, as accounting of financial companies is very flexible where one shows profits, one should always look at “comprehensive income” because this tells a much better picture than net income as Financial can often hide losses below the net income line.

Jackson Financial has actually generated 2 bn in net income in Q1 but has hidden 2,7 bn losses “bellow the line”, resulting in a negative Comprehensive income of 700 mn in Q1. So economically, they are loss making.

Insurance regulation in the US is very easy to arbitrage, so Jackson seems to be still able to buy back shares and pay dividends, but this could end very soon if regulators wake up.

Of course, as in Salzgitter’s case, the share price can do anything over the next days, weeks, months and even years, but I do see a relatively high probability that they run into existential problems soon. I think it is quite dangerous to invest into shares like Jackson without being aware how potentially precarious their situation really is, just because they are cheap.

So what are the lessons for (very) low P/E stocks form my perspective ? I would mention those three:

- There is always (yes always !!) a fundamental reason and/or existential risk why they are so cheap

- In order to make an informed investment decision, you must be aware of these risks and have a different opinion that should be based on facts that support this different opinion

- If you only invest because they are cheap, then on average you will get hurt bug time

Re Admiral: Sabre slumped today, due to higher CR driven by claims inflation, peers Admiral, DirectLine also down. If I remember correctly admiral mostly sells insurance through platforms (Vergleichsportale) and makes heavy use of reinsurance, right?

yes, Admiral is a direct insurance company, reinsuring a significant part of its business.

Thank you for your comments on Jackson. I would be happy if you could answer some of the questions arising as consequence of these comments:

– You write that Jacksons annuities “contain lots of pretty significant “short option” exposure”. And later: “customers can often take out their capital with little or no penalties after some years” – do you have any evidence of that? My Interpretation was that the surrender fees for early withdrawals (from 8,5% at the beginning – descending with life time of annuity) covers the potential losses?

– Why to you think, that “now in a rising interest rate environment, those business models will be under a huge pressure”? In my understanding the majority of annuities is based on separate accounts (230 bn of the 350 bn Balance Sheet size). Of course there could (for existing contracts) be tendencies to withdraw capital (as in any investment fund), but the penalties (surrender fee, and tax disadvantages) would be an argument to cut exposure to the markets not via the annuitiy but with withdrawals from other fund assets? And for new clients the effect should be clearly positive – Jackson will be able to offer more attractive new contracts?

– Why do you take 352 bn as the denomiater in calculating the equity ratio. 231 bn of these 350 bn are double counted as separate account assets and liabilities on both sides of the balance sheet. These are (in my interpretation) not assets and liabilities of Jackson but of the clients. So the realistic equity ratio should be 8,3%?

– You questioned the capitalisation of acquisition costs (14 bn). In my understanding this is best practice in the insurance industry? Allianz for example holds a huge 25 bn of (capitalized) deferred acquisition cost (DAC) on its balance sheet (and I consider Allianz a very solid company). Concerning the “Quality” of assets there are in my understanding very restrict regulations for qualifying such assets for “Risk bearing Capital”. Under statutory accounting rules for Jackson these DAC have for example to be amortised over 7 years (in accordance to the surrender charges). So one could (simplified) say that in statutory capital only this part of the DAC is counted that is covered by surrender fees due in this moment. Do you see this differently?

– You write that “tangible” equity for Jackson is actually negative. My understand here is, that under statutory accounting (which is the relevant perspective concerning cash distributions) there is about 5 bn in “risk bearing capital”(Source: Capital markets day documents) (not 9,6 according to the balance sheet). You are right – the future ability to pay dividends and make buybacks lays in staturory accounting. And if regulation would require a higher ratio (or asset that do qualifiy now do no longer qualify as risk-bearing) this would reduce Jacksons abilities to reedeem capital. Do you have any evidende that these rules will be stricter? And what would be a possible reason for that? Do you think that the financial stability under current rules is not guaranteed=

– You write that “Jackson Financial has actually generated 2 bn in net income in Q1 but has hidden 2,7 bn losses “bellow the line”, resulting in a negative Comprehensive income of 700 mn in Q1. So economically, they are loss making.” Here I think that you did misunderstand the results. They did not “economically” make 2 bn in income (which would be almost the whole market capitalisation in one quarter!). But economically they also did not make a loss. They did “economically” earn (just) 354 million. This is the result if one takes into consideration all effects of changes in assets and liabilities (be it realised or not realised). As the realisation rules within GAAP-accounting are different for Hedges and Assets there are quite huge discrepancies for “formal-GAAP” and “economically/adjusted” results.

The last point is for sure not very “nice” for an investor, as he/she has to trust the management. And I agree in your assessment that management has lots of possibilities to “hide” good and bad results for quite some time. But this is true for all insurance investments. In liability insurance for example an actuary can produce very different IBNRs (insured but not incurred reserve). If this would be a “non-investible”-criteria all insurance companies would have to be excluded from an investors universe.

Thank you for the good discussion.

Helmut

Thanks for your qualified comments. I’ll try to answer as good as possible in a first try:

– yes, there are withdrawal penalties that decline with age of the policy. But you should not forget that competitors often offer “sign on bonuses” that directly compensate for the penalties at the competitor. But you also need to asume that those who surrender are those with older policies with lower penalties. Form the outside it is really not possible to assess if the surrender penalties cover losses. If there are only a few surrenders, than this is normally not a big issue as existing liquidity can be used to fund surrenders. However as soon as you have to sell assets that are potentially “under water” the picture might change dramatically.

– With higher interest rates, competitors can offer policies with better features (higher upside partipation, shorter ratchets etc.). As this is actually a capital market product you can assume that brokers actively try to swith customers into better products in order to earn a commission. As mentioned above, sign-on bonuses are very common. Even if Jackson manages to retain customers, they will need to offer significant incentives which might really hurt at some point in time.

– with regard to the acquisition cost: Of course this is part of GAAP but personally I think if you want to be conservative and especially if there might be a scenario with high redemptions you don’t want to rely on the assumptions behind that “non tangible” asset.

– Separate account assets: I have not deeply looked into how the accounting rules are here but my general “rule of thumb” is that if something is “on balance sheet”, there is some risk that you need to cover (be it operational, reputational, some kind of guarantee etc etc.). If it would be pure “assets under managment” it would be off balance sheet. Separate account does not mean that there is no risk to the company.

Add on: This is from the 10-K. (see below)

“We issue variable contracts through our separate accounts for which investment income and investment gains and losses accrue directly to, and investment risk is borne by, the contract holder. Certain of these contracts include contract provisions by which we contractually guarantee to the contract holder either a) return of no less than total deposits made to the account adjusted for any partial withdrawals, b) total deposits made to the account adjusted for any partial withdrawals plus a minimum return, or c) the highest account value on a specified anniversary date adjusted for any withdrawals following the contract anniversary. These guarantees include benefits that are payable upon the depletion of funds (GMWB), in the event of death (GMDB), at annuitization (GMIB), or at the end of a specified period (GMAB). Substantially all of our GMIB benefits are reinsured. GMIB benefits and GMAB benefits were discontinued in 2009 and 2011, respectively. For additional information regarding our account value by optional guarantee benefit, see “Business–Our Segments–Retail Annuities–Variable Annuities.”

So there are clearly guarantees (“Put options”) written on these “Separate account” and that needs to be borne by the Equity of the company. Ignoring these separate accounts in an analysis in my opinion would be a big mistake. From what I know, especially the older policies are quite “problematic” and the put options are valuable.

– US regulation: US Insurance regulation is quite anitquated and in my opinion not fit to reflect complex products like variable annuities. In Solvency II for instance, you completely ignore DAC and calculate “embedded value” instead which at least reflects the actual value of the book slightly better than historical acquisition cost. US regulation will most likely only change if one or more players get into existiential problems. The valuations of the pure plays might indicate that the day of reckoning is coming rather sooner or later

– result: my rule of thumb again here is for a financial company to use Comprehensive Income as the best proxy for economic income. Of course Management sees that differently because they cannot influence this as much as their own made up numbers and would have problems justifying their bonuses. I have written about that topic quite often on the blog. In most cases for financial institutions, you could see the problems coming long before in the CI .

– Insurance in general: Yes, Insurance companies are really hard to understand and a company with a large IBNR is clearly a “Black box” and requires a lost of trust in Managment which is rarely justified. Therefore I only invest in “short tail” businesses as a principle. But even in the P&C space it will be interesting to see how they manage with rising inflation. For long tail business, this could turn out to be very bad as well.

The biggest issue however in my opinion is that most of these products are relatvely new and there is absolute no historical basis how these products and policy holders will behave in a volatile environment with increasing interest rates. The Solvency of these companies depends on assumptions how policy holders will behave and there is a big risk that those assumptions could maybe be too positive.

I think the share price reflects this. Myself, I don’t see a chance to understand this Black Box in a way to understand if there is a mispricing or if smarter investors can judge the situation better then I can.

However, the fact that quite sophisticated insurers like Metlife and Prudential want to get rid of this, is one hint that this will not be easy and also the fact that both players trade very “cheaply” indicates that it is not a Jackson specific topic.

Maybe it will be a great investment, but I would not be able to build to the required long term conviction.

I hope that perspective helps a little bit to explain why I am just very sceptical.

Incurred But Not Reported !!!!

One important input factor here deciding on how valuable (costly) these embedded options are to JXN is the ‘rational’ executioning of the customers’ options.

In Germany, it was observable that customers tended to act much more rational with reagrd to their Bausparverträge then could have previously thought, but online edjucation regarding a hugely popular product was one factor and the (we) Germany are ‘Weltmeister’ if interest saving products are concerned.

For my master thesis i looked into more complex annuities and the Q how rational execution will be remained an open question with a big impact.

I think the more complex the product, the bigger the sales organisation and the more unedjucated (avg. US cust. even worse than in Germany?) the options holder is, the farther away from optimal…

Pls keep the high quality discussion going.

I stopped looking into BHF/JXN* early but might take another try (after first reading the verus post)…

Best, s4v

(* https://searching4value.wordpress.com/2021/12/07/quicky-on-brighthouse-financial-bhf-us-jackson-financial-jxn-us-abandoned/) re-reading it i still find it remarkable how the GS rating can result in a 14% pop.

Thanks for the comment. Waiting for Helmut to tell me what I have bern missing 😉

Thank you for your valuable comments. It looks as there are several issues:

1) Risk from withdrawals: In my view one has to distinguish between company specific “problems” and industry issues. You argue, that competitors-behavior (bonuses) could lead to losses for Jackson and that more attractive products (because of the new interest environment) could lure customers away. I do not see this as one way street as the economic environment is the same for Jackson as for all competitors. I consider (or considered) the risk that the whole industry might not be able to offer an attractive product as much more relevant. I know the German life insurance industry quite well and they had (and have) the problem, that their product is “dead” as the interest environment (combined with the costs) made it impossible to design good products. With rising rates this risk is much lower now and the chances for market growth is much higher than in the past.

the other question is: What happens in case of a withdrawal economically for Jackson? I have to admit that I do not know the product specific features in the US-Market.

But according to my understanding of the variable annuity products (which are the main category for Jackson) the guarantee is not designed by “pots” of safe asset components (which is the case for German live products – In the German market the assets have to produce enough to cover the guarantee). Instead, the required guarantees are secured by a corresponding hedging process and the assets are seen as a sperate pillar. The special feature is that, by separating investment and guarantee generation, the products are designed in such a way that the “return after guarantee fees”, i.e. the “efficiency” of the product, is higher than with products that generate the guarantee through and with the investment itself. My understanding is, that the company will pay back just the accumulated assets and all guarantees would be ended for the client in case of a withdrawal. Jackson would therefore not have a loss on its assets (irrelevant in what market situation) instead would just have to stop the hedging for this contract (therefore it is important that all hedging losses and gains are rated with current market values). The possible loss would of course be the capitalized acquisition costs – but regarding this I argued that this loss should be covered by the surrender fees.

2) US regulation/Statutory accounts: I have some experience in risk-management systems in the German market (preparation for Solvency II ) – but I have to admit, that I lack the equivalent knowledge for the US. But the general methodology is quite easy. Calculate the amount of risk you have and compare that to the risk-bearing capital you have. The question is how these two numbers are calculated. The assessment of risk is for sure the more complicated part (and in my view tail risks are not adequately reflected in German regulation rules as well). But things get better over time as there is more experience with the regulators and the insurance companies. I agree that an investor has to have trust here that the hedges in place really work and the calculated capital realistic. But the part you are referring to is the determination of the risk bearing capital. For me the US statutory regulation seems quite conservative to me. The nominal Equity of 9,6 bn is recognized only with 5,3 bn (mainly as DAC has to be amortized over 7 years and deferred tax is not regarded as an asset). Where do you see possible future problems? That less capital will be recognized as risk bearing (so that the relevant capital will go from 5,3 bn to say 4,0 bn? Or that the rules for assessing the risk will cause a higher number? Today the calculated risk according to the rules is about 1 bn (ACL) – If this this would rise by say 50% the solvency level would shrink from over 500% to about 350% (which would be low and dividends would not be possible).

3) relevant result: You argue that for a financial company Comprehensive Income as the best proxy for economic income. I agree that this is true in the long run. But short term this number does not reflect the true economic situation, as the realization of profits and losses for assets and hedges are not congruent under US-Gaap. But let us take this number for the last 3 years (1,1 bn, -0,2 bn, 2,1 bn) – the average is about 1 bn per year. Not too bad for a market capitalization of 2,3 bn.

I have to admit that Jackson is a more complicated investment case than I thought in the beginning. And as you said – investors are very reluctant not just with Jackson. But this reluctance does not necessarily mean, that Jackson have to be a bad investment case. If everyone is enthusiastic the risk is clearly on the wall. This is absolutely not the case for Jackson. And the pop in share price referenced “searching4value” caused by the rating upgrade is a good example. Trust is lacking (and the rating gives trust). Generally I feel more comfortable with an investment if everyone is skeptical. But an investor has to understand the risks of his companies … if he does want to invest and not to gamble. And that understanding is the problem here. Therefore I appreciate the good discussion which helps everyone to better understand possible pitfalls.

One more (crazy) thought, which I do not deem likely, but alos not impossible, and at some price JXN should be attractive! (We must be careful to not just assume what worked from the 2020 lows (ie BHF with low P/B) will work from a 2022 low)

WHAT IF: JXN was (almost) perfectly hedged for all embedded options sold assuming rational execution via customers. Now, vola is way up, making options much more valuable, but customers are far from execising optimally, thus JXN wins a lot!…?

Of course anything can happen. However it is in principle not possible to hedge all those options because the financial instruments to do so do not exist.

But of course, if many investors decide that the stock is worth more, then the share price will go up. The main risk here is that in a downside case, Jackson will need to raise capital quickly.

For me, A stock like Jackson is not an investment as I cannot see thorugh the black box. I see the risks but I cannot formulate a “counter thesis”.

In general, using the “Best case” as basis for an invetsment is not advisable.

Thanks for your qualified answers. This makes it really fun to argue.

1) Withdrawals etc.: You cannot compare German life insurance policies with US Annuities. Early redemptions for a German life insurers are ususally a significant part of the profit, due to a very intransparent “contract value” and quite low “Rückkaufswerte”.

In general, even variable annuities gurantee you the “Money back”, i.e. you get at least the money back that invetsors paid in. But many have “ratchets” build in that increase those guarantees over time.

The underlying assets are ususally a corporate bond portfolio and a “hedge book” that more or less tries to hedge the Equity risk. These proxy hedges were/are part of the problem, especially for old products. Newer products link the policies to an index, older policies allowed a selection of underlyings which made it almost impossible to hedge.

After a quick google search I found this document from AXA which explains some of the features and problems:

http://www.institutdesactuaires.com%2Fglobal%2Fgene%2Flink.php%3Fdoc_link%3D%2Fdocs%2F2017164734_2017-05-aymeric-kalife-erm-training-variable-annuities-2017.pdf%26fg%3D1&usg=AOvVaw0QBemOPRa6QIhVSdRfijTI

There are a couple of examples of how the guarantees are “rolled up” or “ratcheted up” independent of the account value.

So yes, there is also some “wiggle room” for US Insurers but it is definitely not the case that Insurers don’t have a downside case in the case of losses in the underlying portfolio.

In summary, you should not assume that this is some kind of Asset Management businesses although managment usually wants you to believe this. The guarantees have to be honored by the company, the policyholder assets are not “ring fenced”.

2) When you have read the AXA document that I linked to, you might start to understand what kind of risks such a complicated product includes, a lot of that has to do with the good old Greeks and is not or almost not covered by US regulatory rules. Solvency II is not that much better, but at least a little bit more economical, although the industry lobbied very hard to make Solevncy II as weak as possible, otherwise all Life insurance companies in Europe would have been insolvent.

I didn’t digg that deep into the company but US regulation allows also low quality reinsurance as well as stuff like surplus notes either to increase avaliable capital or reduce capital requirements. I have a very low opinion of US insurance regulation in general and they did everything in order to avoid somehow more transparent Solvency II standards.

In summary I would repeat that the business is a black box, even for experts. In my opinion there is also a significant risk that there is a lot of “toxic waste” in the portfolio, as especially the earlier VAs were more or less suicide products because the insurance coma

panies didn’t understand what they were doing.

The problem was that the actuaries who desgined these products didn’t fully understand financial markets and vice versa.

Of course, anything can happen to the share price in the short and the mid-term, but in the current environment there is also a significant possibility for a “sudden death”.

What a *rocket emojy* JXN has been. We have missed it.

But, such is often the case with your (our) style of analysis.

Indeed. Thank you for remindung me.😀

welcome, i have many more such stocks where i focused (too much!?) on the risks

Me too….

I suppose the question regarding Rob Vinalls portfolio is if you think his losses are transitory or permanent…I respect him a lot given his record but I do think his Carvana bet was way off and will result in some permanent loss of capital.It all goes to show how amazing was Warren Buffetts return of 21% over 40+ years…yet I would´nt rule out Rob yet

Why don’t you exclude separate account assets from Jackson’s balance sheet analysis? The ratio of equity to total capital then gives a completely different picture than the one you draw.

because these separate accounts are wrapped with guarantees and therefore not risk free for Jackson. Otherwise they would be off balance sheet.

“In the case of Rob and Mathias however it should be taken into account, that despite the horrible first 6 month, both have outperformed their benchmark significantly since inception. ” If one’s portfolio is mostly Nasdaq then the benchmark should be Nasdaq. For example, RV’s benchmark has absolutely nothing to do with his portfolio. It’s very similar to a leveraged loan fund using the 3 month treasury as a benchmark. I think you’re being too kind. Rob’s being very disingenuous at best. His benchmark of the DAX is a marketing tactic – and likely a dishonest one.

Interestingly I am not alone…

Not sure for how long you have been following Rob, but he indeed started out as a very Germany focused investor, that’s where the Benchmark originally comes from. But I also agree that the Nasdaq would be a better fitting Benchmark these days.

Maybe one additional comment with regard to “marketing tactics”: As far as I know, his fund is closed to new investors for quite some time.

Hello, thank you so much for your blog and congratulations on your performance… My portfolio was dragged down much more. Do you have an opinion on Stellantis? Low PE, high FCF yield, high dividend yield. Is it in the same category as Salzgitter?

Good luck for the future. Cheers

I have never deeply looked into Stellantis. What I do know is that the overall car industry will undergo a huge structural change in the near future, that tens of billions have to be invested and maybe not everyone will survive unharmed….

ok. Thanks for your reply. What do you think about fallen stocks that were already in your portfolio once. Einhell is such a candidate (that is in my portfolio). PE<8, order intake looks fine, growing etc. What do you reckon?

Hello MMI,

I would be pleased if you could specify shortly why you sold Netfonds. I attended virtual HV last month and found it rather convincing. (finfire sucessfully launched, , assumed further growth > 10%, slower growing costs …)

Thank you in advance,

Uscha

Uscha, mostly because I think their business is might be negatively effected by capital markets. I also didn’t like the VMR deal very much. With the drop in overall market levels and the relative stability of their share price, I do think they are fairly valued for the time being. But I could of course be completely wrong….

All things considered, good performance!

With regards to the FinTwit “celebrities”: in times like these many people find out that that most fund managers are more lucky than smart and their outperformance tends to revert back to the mean. When taking into account the much higher volatility, fees, luck and stress involved with finding\monitoring a really good fund manager, in most cases you were better off investing in a basket of diversified rebalanced ETFs.

Many thanks for sharing your thoughts and your investment decisions! I am always excited to read your posts! I am a bit surprised that you also sold your Orsted position, in my opinion they are still doing very well. Earning growths didn’t fully follow high energy prices yet, because they hedged part of their production. But over the next years they should be a long term winner from high energy/electricity prices. I would be very thankful if you could share some thoughts on this sell decision. Many thanks!

I have nothing against Orsted, but in the meantime I have bought more renewables positions (PNE, Energiekontor, ABO, 7C). So overall exposure has gone up and I think I do understand the smaller players better.

On a day like this, you look like a genius having sold Orsted. -24% 🙂 [no position]

There is a very thin line between genius and idiot in single stock investing indeed. And it’s quite easy to cross it to either side without doing a lot.