All Danish Shares part 11 – Nr. 101-110

In volatile times like these, I actually enjoy from time to time to take a “stoic” brake and work through a list of companies. In order to reach my target of finishing Denmark this year, I also need to hurry up a little bit (still more than 70 stocks to go…). Please find another 10 randomly selected Danish stock with one new candidate to “watch”.

101. EAC Invest

EAC Invest is actually a stock I had looked at almost exactly 9 years ago when the company was called “East Asiatic Company”. Back then, their main business was a meat business in Venezuela and a Autralian focused relocation company for miners. Looking at the share price development, it was a good decision to move on despite back then the stock looked ultra cheap:

One of my major learning of this analysis was that one really needs to be careful in interpreting earnings in a high inflation environment. They are almost always highly overstated due to the fact that amortizations do not reflect the actual cost of replacing equipment.

These days, the company has a market cap of 15 mn EUR, seems to have sold all operating businesses and just owns a few remaining participations, among others in a Thai Acrylic company and some Chinese developer if I understood this correctly. Nothing to see here, “pass”.

102. Trifork Holding

Trifork is a 640 mn EUR market cap IT service company headquartered in Switzerland that was IPOed in 2021. Compared to other Danish Software IPOs in the recent pass, the stock did relatively well and trades close to its IPO price of 150 DKK per share.

The company is growing nicely but has only gross margins of around 25%, indicating that they don’t have a lot of value creation capabilities. It is hard to find out from their website what they are actually doing but is seems to be mostly organizing conferences and reselling software. At 23xEV/EBIT, the valuation looks quite steep for a IT service company. “pass”.

103. Skjern Bank

As the name indicates, yet another regional bank with a 144 mn EUR market cap. This one looks extremely cheap at 6x P/E, however according to their annual report, they seem to be somehow short on capital and they run a significant open FX position which leads to overall P&L volatility. “Pass”.

104. Nord.Investment

Nord is a tiny, 10 mn EUR market cap IPO from 2021 that seems to be active as a sort of robo advisor. At the end of 2021, they had ~ 300 mn EUR under Management and 5K clients. 2021 revenues were 0,6 mn EUR and the company made losses of 2 mn EUR. Initially, they wanted to double business in 2022, but not surprisingly, they had to lower their estimates in May. As a kind of innovative feature, they seem to offer to digitally consolidate Pension plans for customers. From what I know, Denmark has a very sophisticated pension scheme and this is something I haven’t seen before.

The share price looks really ugly:

Nevertheless, I will try to “watch” this as I do like the Robo Advisor business model when it is well executed, although the company clearly went public much too early.

105. DecideAct

DecideAct is another 2021 IPO with a market cap of ~8 mn EUR. The company runs a platform for “strategic management decisions”, which according to their website should have the same TAM as CRM.

The P&L in the 2021 report actually doesn’t have a revenue line which might indicate that this company should not have been IPOed. Funnily enough, the company claims that they had 0% churn in 2021, which is quite easy to achieve if you don’t have any sales. That’s my kind of humor, “Pass”.

106. Aalborg Boldspilklub A/S

Aalborg seems to be the listed company that owns the Aalborg Football team. The market cap of 5 mn EUR maybe reflects the second to last position in the Danish league. “Pass”.

107. Per Aarsleff Holding A/S

Aarsleff is a Danish Construction company that has a market cap of 483 mn EUR. Interestingly they seem to be active in ” infrastructure, climate change adaptation, environment, energy, construction, and collaboration”.

At first sight, the company looks both, very cheap (PE of 6,6) as well as having grown top line for 9 out of the last 10 years and 4x in net income over the same period of time.

The chart shows quite constructive performance from 2014 to 2021 before going down as many other stocks in 2022:

As a typical construction company, margins are thin (11-12% gross margins). The current year looks good from top line, but bottom line is suffering and cashflow is negative as significant working capital had to be build up.

Overall, despite looking cheap, I am not sure if I want to own a low margin construction company going into a recession, therefore I’ll “pass”.

108. Spar Nord Bank

Spar Nord Bank is one of the many regional Danish Banks with a market cap of 1,4 bn EUR. The bank is active in Northern Jutland and looks cheap at 9x earnings. ROE is also quite good at 10-12%. However,as I am not interested that much in regional Danish banks, I’ll “pass”.

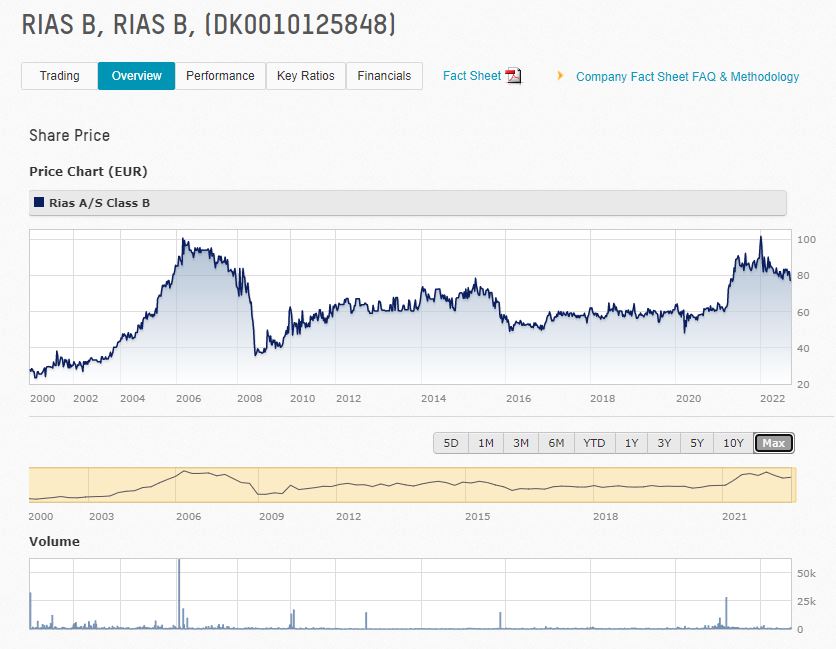

109. Rias A/S

RIAS is a small, 15 mn EUR market cap company that distributes plastic parts to the construction and industrial sector in Scandinavia. At 9x earnings and 7xEV/EBIT the company looks quite cheap. The company had a very good year in 2021. As for Solar, business has been doing well until mid year with an upward revision on earnings.

According to TIKR, interestingly 47% of the shares are held by Thyssenkrupp. Looking at the chart, the company failed to create much value over the last 20 years:

Overall, it looks like a little bit a similar story to Solar, however for my taste the market cap is too low and the stock is extremely illiquid. “Pass”.

110. Carlsberg A/S

Carlsberg is a world famous brewery group that is valued at around 18,2 bn EUR. At 16,7x earnings and 13x EV/EBIT, the stock is clearly not cheap in relative terms. A look at the share price shows that it is a more defensive, slow growing company:

Carlsberg has significant exposure to Asia and Central and Eastern Europe and pulled out of Russia early. 2022 so far looks quite good, with decent organic growth. The cash cow is clearly Asia which has margins >20%.

ROEs are 20%+, EBIT margins are at 15-16% and have been increasing nicely over the last few years. Carlsberg is clearly a very interesting “high quality” business. Breweries face their own set of problems from the Energy cirsis as they are energy intensive. In addition they need CO2 and rely on having enough glass bottles. However a large player like Carlsberg should be able to manage this.

Although I do not like their main brands that much (Tuborg, Carlsberg, 1664), I’ll put the stock on “watch”.

If you are looking at Carlsberg, you should take a look at Heineken holdings. It is trading at a discount to Carlsberg – 13x 2023 EPS estimates and 11.6x 2024 EPS estimates.

With a much pooer ROE the discount at Heineken seems fully justified, maybe even not large enough!?