All Danish Shares Part 12 – Nr. 111-120

And on we go with our journey through the danish share universe. This time we have one very strong candidate that already made it into the V&O portfolio recently. Enjoy !!!

111. Boozt AB

Boozt AB is a “Nordic technology company selling fashion, apparel, and beauty online”, currently valued at 342 mn EUR. The chart shows that,as other E-Commerce players, times are tough for E-Commerce:

Boozt has been actually already profitable, even on a GAAP basis in 2021. 2022 clearly looks worse than 2021 with lower EBIT margins and significant negative cash flow. I am not an expert with regard to fashion E-commerce, but I think it is an extremely difficult business and competition is really tough. “Pass”.

112. Newcap Holding

Newcap is a 3,5 mn EUR market cap nano cap, doing something with financials but having no revenues. “Pass”.

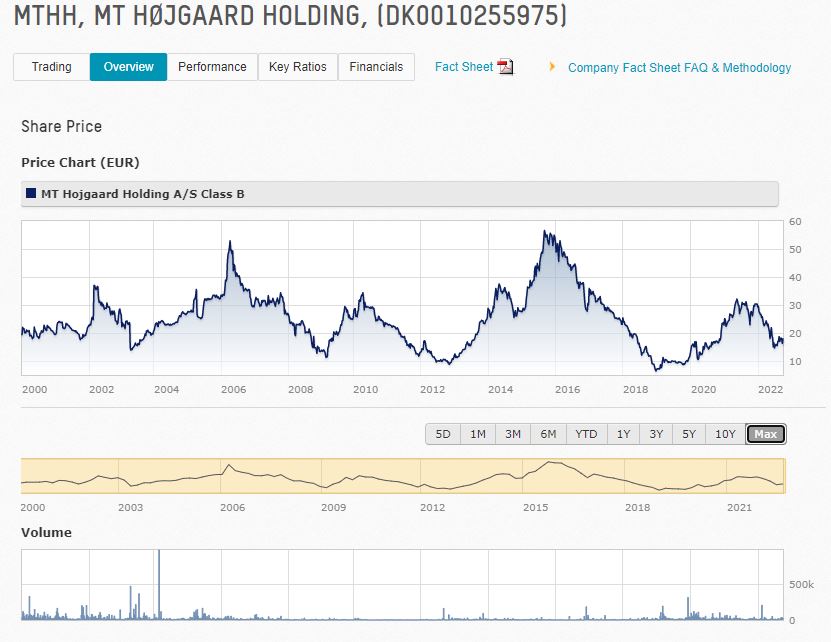

113. MT Hojgaard Holding

Hojgaard is a 140 mn EUR market cap construction compnay which has a long term chart that looks like a nice mointain range:

The company again looks cheap with around 6x P/E. However the company has extremely thin margins (7% gross). 6m 2022 looks still good from earnings but not so good from a cash flow perspective. Similar to Aarsleff, I would not comfortable owning a contrauction company going into a recession, therefore I’ll “pass”.

114. Agillic A/S

Agillic is a 26 mn EU market cap company doing something with AI. The company actually has revenues, around 4 mn EUR in the first 6M, but is loss making. They also seem to capitalize costs. One thing that I found remarkable that the reports features the very smartly dressed CEO several times, for instance here:

At the current burn rate, cash only lasts another 12 months and the CEO doesn’t look like that he is a penny pincher. “Pass”.

115. Ennogie Solar Group

Ennogie is a 89 mn EUR maket cap Rooftop Solar company that used an existing defunct vehicle formerly called “small Cap Danmark”. Although the investor information is only in Danish, this looks like a promotional stock. “Pass”.

116. Nexcom

Nexcom is a 4 mn EUR market cap nano cap software company that is of course using AI. “Pass”.

117. Seluxit A/S

Seluxit is a 6 mn nano cap software company that has little sales and is losing money. “Pass”.

118. Roblon A/S

Roblon is a 27 mn EUR small cap that “operates in business segments that are Industrial Fiber, which comprises development, production and sale of strength element solutions, fibre optic cable components to the fibre optic cable industry, and composites to offshore and other industries; and Engineering, which comprises development, production and sale of rope-making equipment, twisters and winders, and cable machinery”.

That sounds interesting and with a lot of Fiber cables being rolled out could be a good business. However, it isn’t as the company is loss making since 2019. 2022 looks good from the top line after the acquisition of a Czech company, but they still shows losses.

Maybe this could become a turn around at some point in time, but for me it is a “pass”.

119. Park Street A/S

Park Street is a 25 mn EUR market cap real estate company active mostly in Copenhagen. “Pass”.

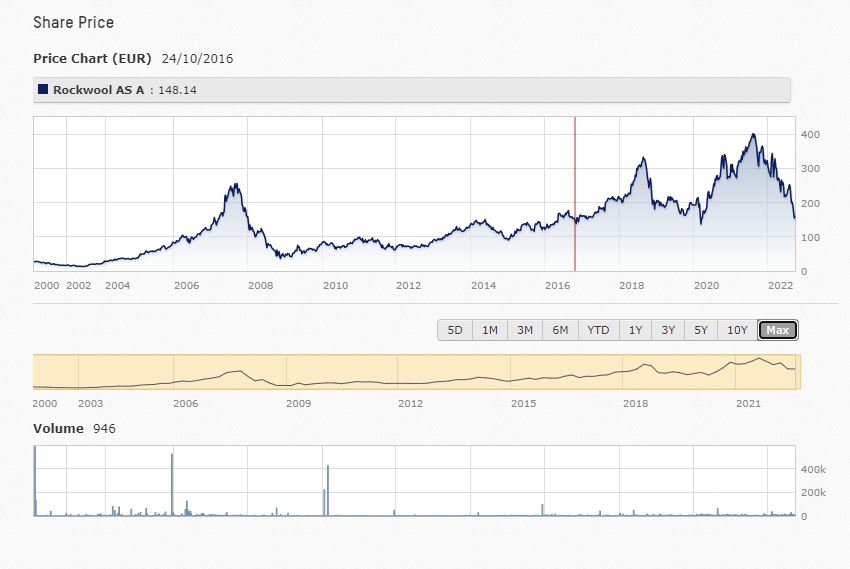

120. Rockwool A/S

Rockwool is a 1,7 bn EUR market cap company that offers insulation solutions based as the name indicates on Rockwool, a material that is produces basically by melting rocks.

A quick look at the chart shows a first peak pre GFC and then a nice increase for several years until 2021:

In the last 12 months or so, the share price more than halved, reflecting the worries about high energy prices and a drop in building activity.

Compared to plastics based insulation, Rockwool is more expensive, but is also more flame retardent and seems to show better characteristics with regards to room climate (humidity).

At a current valuation of 11x P/E and 8x EV/EBIT, the valuation is at the same level as after the GFC. Despite high top line growth, the bottom line has been suffering a little bit, but EBIT margins are still in the double digits. The big question is how hard they will be hit by the downturn in building activity and in contrast, if they can benefit from additional insulation activity.

The company has very little debt and really good reporting. As I have included Rockwool already in my “freedom insulation” basket, it is an obvious “watch”.