Performance review 9M 2022 – Comment: “David Einhorn, Bumsbuden & Short selling”

In the first 9 months of 2022, the Value & Opportunity portfolio lost -15,8% (including dividends, no taxes) against a loss of -27,0% for the Benchmark (Eurostoxx50 (25%), EuroStoxx small 200 (25%), DAX (30%), MDAX (20%), all TR indices).

Links to previous Performance reviews can be found on the Performance Page of the blog. Some other funds that I follow have performed as follows in the first 9M 2022:

Partners Fund TGV: -42,6%

Profitlich/Schmidlin: -20,6%

Squad European Convictions -20,4%

Ennismore European Smaller Cos ––6,6% (in EUR)

Frankfurter Aktienfonds für Stiftungen -12,2%

Greiff Special Situation -5,0%

Squad Aguja Special Situation -21,2%

Paladin One -21,4%

Performance review:

Overall, the portfolio was again more or less in the middle of my peer group. Looking at the monthly returns, it clearly shows that the rebound in July until Mid August was short lived and that August and September turned out to be big down months again, after the disastrous June:

| Perf BM | Perf. Portf. | Portf-BM | |

| Jan-22 | -3.7% | -4.2% | -0.6% |

| Feb-22 | -5.0% | -5.3% | -0.4% |

| Mar-22 | -0.2% | 3.4% | 3.6% |

| Apr-22 | -2.1% | -0.3% | 1.8% |

| May-22 | 0.5% | -0.4% | -0.9% |

| Jun-22 | -11.4% | -8.1% | 3.3% |

| Jul-22 | 6.5% | 5.7% | -0.8% |

| Aug-22 | -6.0% | 0.4% | 6.4% |

| Sep-22 | -8.6% | -7.2% | 1.4% |

In relative terms, I consider the first 9 months as pretty OK. My goal is not to achieve absolute returns which I think is not possible, but I try to outperform the benchmark on average by a few percentage points per year.

In absolute terms, 2022 seems to shape up to be the worst year in the 12 year history of the blog. The worst so far has been 2018 with -15% for the benchmark and -11% for the portfolio. Personally, I have experienced much worse draw downs, especially in 2001-2003 when the DAX for instance lost almost 75% from High to bottom. It seems that many investors today have either forgotten about those times or never experienced them. Hard draw downs are part of the game. That’s why it is called a “risk premium”.

Another learning experience for many investors is the fact that cheap stocks can get a lot cheaper and stay cheap for a long time. A good example is Solar A/S from Denmark, a stock I bought on 9x trailing P/E in May. The company increased its guidance for 2022 but still the stock lost -26% (including a dividend) and now trades at around 6x 2022 P/E. Maybe this resolves itself quickly ? Who knows, but one should better prepare for those lower valuations to persist especially in the small cap area.

Transactions Q3:

The current portfolio can be seen as always on the Portfolio page.

The third quarter was quite active. I exited the Renewables basket with the exception of ABO Wind, by selling 7C, PNE and Energiekontor. I found them fairly valued and was a little bit cautious with regard to the looming “excess profit” tax. I also reduced Nabaltec slightly. I also closed the chapter on Naked Wines and sold 1/10 of the Meier Tobler position in order to manage position size.

With Exmar and 3U, two special situations were initiated. In addition I purchased an initial “Insulation” basket consisting of 7 energy efficiency stocks. However this was clearly not optimal timing. 5 of these 7 stocks got hid badly by the sudden housing slow down and saw losses of -13% to -35% over a few weeks.

Cash is at around 10% of the portfolio, average holding period around 3,5 years and the 10 largest investments make up around 55% of the portfolio.

Comment:

David Einhorn

Just when I wrote this post, I listened to a recent interview of David Einhorn here. Long term readers know that I have a certain “history” with Einhorn. I looked at a couple of his investments in the past but didn’t understand most of them. In one instance, Einhorn even commented on the blog at one instance.

I still have a high opinion of his abilities but I am really disappointed how he claims that passive investing is responsible for what he perceives as the “death of value investing”. I was especially struck by this quote:

It used to be we could buy something at a reasonably low multiple, whatever we thought that was. Think that the company would do somewhat better, benefit from it being somewhat better and realize that other investors would see what we saw six months later, a year later, and would rerate the shares.

So you could buy something 11 times earnings and maybe they would earn 10% more but you get another three points on the multiple and you make 50 percent over two or three years.

Of course there is nothing wrong with such a “system”, but essentially he is/was playing a rather short term system that relied on other investors being less smart than him and catching up within a relatively short period of time.

Claiming that value investing is dead because his specific strategy doesn’t work anymore is in my opinion a clear sign of trying to blame others for one’s own mistakes. To give Einhorn some credit, his 2022 performance seems to be OK, although the listed stock Greenlight Re has gone nowhere.

Bumsbuden & Short selling

Almost exactly one year ago, writing the 9M Performance review 2021, I had the feeling that the days of easy tech money was over. This is what I wrote back then:

The big question is : How long will this “flywheel” keep going ? I have no idea but my feeling is that we see already at least some sanity with the obviously stupid or overvalued “non-tech” tech companies feeling some gravity in their share price. Auto1, the German Used Car dealer masquerading as a Tech company for instance lost significantly against its IPO price and almost -50% from the top despite their continuous effort of marketing themselves as the “Carvana of Europe”. Or Lilium, the Frank Thelen backed “Electric Airplane Taxi” start-up that mostly has some fancy prototypes has lost -20% against the initial SPAC price.

My feeling is that the easy days of naive tech investing are over. I do believe that there are still many areas where a lot of break through innovation is happening and companies can grow fast and become very profitable, but from the current “tech darlings” many will not live up to their promises.

In the short term it seems that the Covid tailwinds for many mediocre digital business seem to be gone, such as the very recent news of German Software company Teamviewer or UK based E-Commerce darling ASOS. Many companies claim that supply chain disruptions are the main culprits but I do think that the problems go deeper.

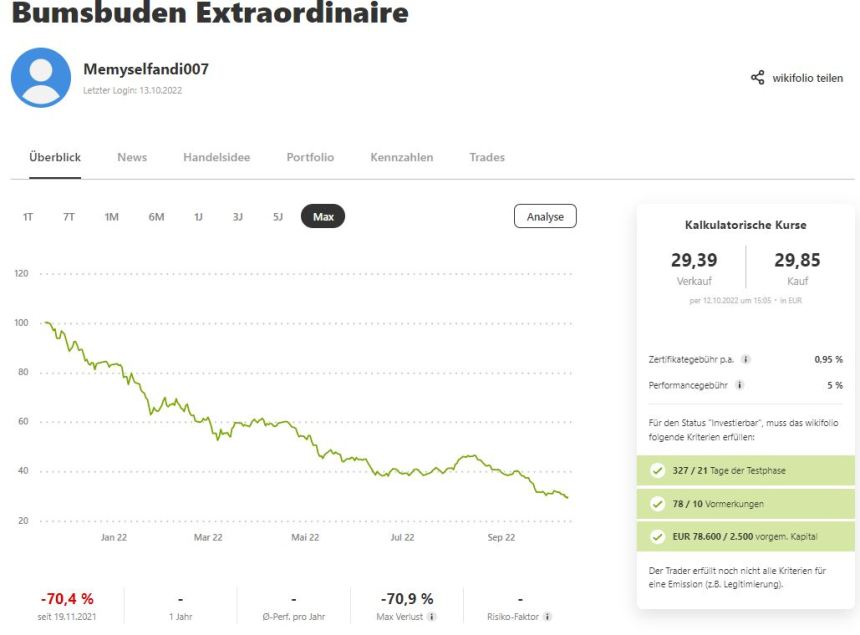

Those who follow my Twitter feed might know that soon after that post, I created a public watchlist (Wikifolio) in order to show, how quickly one could burn money by choosing the worst “naive tech” stocks only in Germany.

The result so far is spectacular: This portfolio was only positive on the very first day and since then lost more than -70% at the time of writing. The whole exercise was like “shooting fish in a barrel”:

Now of course the question is: Why didn’t I short these stocks in reality ? I would have made a lot of money. As my long term readers know, I stopped shorting in 2013 after a mixed record.

The problem is that if I had continued to short over all these years, I would most likely have lost a lot of money in between as stocks went from extremely overvalued to totally ridiculously overvalued over the last 4-5 years until fall last year.

As Gamestop and other meme stocks have shown, for individual stocks there is basically no limit on how overvalued they could become. I have recently watched the Gamestop documentary on Netflix and it is amazing how religious these meme stock investors have become.

Overall, I also find it difficult to pursue both strategies at the same tame, i.e. looking for good short candidates as well as trying to identify long term winners. The Wikifolio was something I did with minimal effort by just applying my general “red flag” approach and virtually buying those stocks with very obvious red flags, mostly based on the “operators” behind the stocks.

For me, the verification of “red flags” in order to filter out problematic investments early is also the main benefit of investing time into these kind of companies. For my successful “Bumsbuden” Wikifolio the following red flags worked best:

- known shady investors/promoters being involved (Northern Data, Auto1, Compleo Charging, Naga)

- more or less criminal track records of Management (Naga Group, Cliq)

- stupid and/or over-hyped business models (Auto1, Veganz, Social Chain)

- mostly promotional character of the stock (Naga)

Overall it was a funny and really helpful experiment but I will continue to focus on long only investing. This is hard enough.

Pingback: Efficiency overview 9M 2022 – Remark: “David Einhorn, Bumsbuden & Quick promoting” - Get Invest USA

Personally find your reaction to this shitfest of a year really admirable and humbling.

I’m -22% YTD (could have been worse), more or less matching my benchmark (SPY). Learned a lot. It’s not fun, but it’s not the end of the world.

Congratulations on the outperformace. Personally, I prefer long only strategies. Sometimes it is difficult to find the right time to sell.

Most of the sh*cos of your short basket don’t even have borrow (some never had). That’s the issue with shorting small/midcaps in Europe, it doesn’t work.