Re-underwriting Sixt AG: Family owned & run long term compounder with a great US growth story at a “bonkers bargain” price

DISCLAIMER: This is not investment advice. The Author is known for making lots of mistakes in his write-ups and will frontrun you whenever possible. DO YOUR OWN RESEARCH !!!!

As always in my longer write-up, this post only contains selected sections of the write-up- A full pdf is embedded below.

- Management Summary

Sixt AG, a family-owned and -run Car rental company from Munich, has been compounding profits and shareholder returns at a double digit CAGR for the last 20 years. Following Covid, they accelerated their organic growth in the US which now represents ⅓ of their business and is growing rapidly at 20% plus p.a..

As most of their competitors (Hertz, AVIS, Europcar) are overleveraged, they will continue to take market share from them in the coming years. The recent (temporary) issues with residual (EV) car values depressed valuation multiples so that Sixt trades at a very low P/E for 2025 (~8 times for the Prefs, 11x for the common) for what I consider a high quality company resulting in an attractive risk return profile.

- Background

Sixt is a company I owned several times in my investment career, unfortunately never long enough. During the initial Covid panic, I bought a “half” position as a part of a wider Covid basket” without any deep fundamental research at that time. Initially, this turned out to be a brilliant investment and almost tripled until the end of 2021, however since then, the stock struggled.

When the Pref Shares hit 50 EUR I tweeted that I couldn’t believe how cheap the stock is.

Following that Tweet, I thought it’s a good time to dive a little bit more into the rental car industry and see if I should “re-underwrite” Sixt or not.

3. Sixt History & some KPIs

3.1. Company history

Sixt was founded in 1912 and so technically is the oldest of the large car rental companies. However, only with Erich Sixt, who became CEO in 1969, Sixt started to expand significantly. Sixt went public in 1986 and opened the first US Branch in 2011. In 2021, Erich Sixt after 42 years finally passed to lead over to his two sons who now run Sixt as Co-CEOs in the 4th generation.

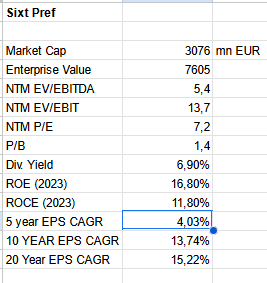

3.2. Some KPIs

We can see that over 10 and 20 years (based on 2023), Sixt has been a great compounder. Only over the last 5 years (EPS 2018 adjusted for DriveNow one off gain), EPS growth slowed. But one has to remember that this time period includes a beginning recession (2019), Covid, interest rate increases etc.

It’s also worth mentioning that all that growth was achieved organically. To my knowledge, Sixt never acquired another company.

Full PDF:

10. Why is the stock cheap ?

As always, when a stock is cheap, the question is: Are there any perfectly good reasons for the stock being so cheap ?

Despite the general weakness in European small and midcaps, these factors might play a role:

- A common theme I hear is that the rental car business is a shitty one. I think this is mainly due to the fact that the problems of AVIS, Hertz and Europcar are very public, but the success of Enterprise is not. On a P/E basis, both Hertz and Avis have traded at similar multiples (but with a lot more debt). As Enterprise is not publicly traded, some analysts might look at Sixt and decide that it is even “expensive” compared to Hertz and Avis.

- Falling residual values for cars have impacted Sixt in 2024. Initially, an EBT of 400-520 mn had been forecasted. After Q1, where they had to book a loss because of unexpected depreciation, they had to cut the guidance again with the Q2 results in May to 350-450 mn EUR. In Q2 once again they again reduced the outlook to 340-390 mn EUR. So investors might be afraid that Q3 might contain more negative surprises.

- Investors might still not fully trust the two sons to continue what Erich has achieved over more than 40 years. I have to admit that I am also not 100% convinced. Only time will tell.

- Sixt is clearly also exposed to the overall economic situation. A deepening recession in Europe might soften the demand, both for vacation rentals and business customers. Or customers might trade down from Sixt’s premium offer to a cheaper competitor.

11. Summary & conclusion

The initial question that I asked myself before writing this post was: Should I re-underwrite Sixt despite the quite disappointing performance over the past months ?

Thea answer after this exercise for me is clearly YES.

Sixt is a stock that offers an interesting growth story, a strong track record for a very low valuation which in my opinion creates a very attractive risk-return profile on a mid-term time horizon.

There are clearly some risks, as mentioned my main concern is how the sons will perform once Erich is not around anymore.

In any case, I decided not only to “re-underwrite” the stock but to increase my exposure by buying an additional 1% of the portfolio of Common shares.

I might add further, both to the Prefs and the Commons in the future if no negative surprises happen. The date for the release of Q3 earnings is November 11th.

Great German language Podcast with legendary Erich Sixt:

Hi MMI,

How do you feel about the growing amount of debt, especially in the face of higher rates and lower % of the fleet with buyback agreement ?

Regarding the brothers, I hear it is not easy to work for them but equally it seems they “live and breath” this business. Market seems to attach a lot of importance to Erich still being present. When the latter passes the market may offer another opportunity to increase the position in my eyes. On the cultural aspect I also remember after the stellar 2021 they paid out a bonus to ALL employees which I liked…

+

I am not to worried about debt. Sixt is at leat 50% a financial company. According to the IR presentation, the European fleet now has reached the old level of buyback agreements.

Is your „face detector“ still used to evaluate companies and their management? 😀

Both sons wouldn´t pass it for me. But Sixt looks really solid nonetheless.

Have you taken a look at L.D.C. SA in recent times? You have covered the stock in the past but never invested in it (as far as I can remember). The stock looks rather cheap but somehow never gets covered by anyone I follow. Given the fact that L.D.C. is a rather defensive stock, I think its worth a look. What do you think?

Is your „face detector“ still used to evaluate companies and their management? 😀

Both sons wouldn´t pass it for me. But Sixt looks really solid nonetheless.

Have you taken a look at L.D.C. SA in recent times? You have covered the stock in the past but never invested in it (as far as I can remember). The stock looks rather cheap but somehow never gets covered by anyone I follow. Given the fact that L.D.C. is a rather defensive stock, I think its worth a look. What do you think?

Are you sure about the entrepreneurial culture at Sixt?

Have a look at eg. https://www.wiwo.de/my/unternehmen/auto/abwanderungswelle-bei-sixt-es-beiden-recht-zu-machen-ist-eine-unloesbare-aufgabe/29619152.html (and also other similar texts…)

Manager würden angehalten, ihren Mitarbeitern gegen das Schienbein zu treten, „damit sie schneller laufen“, so ein Insider. Diesen Stil pflegen die Sixt-Brüder offenbar selbst mit ihren Führungskräften sowie externen Projektmanagern. In seinem ersten persönlichen Gespräch mit Alexander Sixt sei er komplett abgewatscht worden, wie er es noch nie erlebt habe, berichtet einer. Manager würden nicht selten im Beisein anderer Führungskräfte persönlich runtergemacht. So sei im Konzern eine Kultur des Duckmäusertums entstanden, sagen diverse Exmanager. Statt die Eigenverantwortung von Managern und Mitarbeitern zu stärken, betreibe vor allem Alexander Mikromanagement, degradiere Führungskräfte zu ausführenden Organen.

I know about that article. But my own conversations with Sixt employees have not confirmed the claims in the article.

Thanks.

Do you know why Sixt in Europe could achieve such a high proportion of ‚risk free‘ vehicles while it seems that with US business practice it is far lower? Are US automotive manufacturers less willing to do that compared to German/European ones? It seems to be the most natural way to derisk the business and the US car rental ‚Platzhirsch‘ companies are large enough companies to have the pricing power if they want to go for it. But they don’t seem to do it, Sixt also tries in the US.

I really would like to understand this point.

My understanding is that the US market just works differently. However, I do think that the pain might soon be over.

I love premium companies. sure, you can save a couple of yo-yos and wait in line plus ride shitty cars. For many, hard working people this is not worth it – especially in the US. The down-turn in demand in automotive industry (have you seen premium OEMs quarterly reports) will strengthen their position. Glad you underwrite your investment 🙂

I agree with everything you wrote, but you missed one potentially crucial negative: What happens to car rental demand in a world of self-driving Teslas, Ubers and Waymos?

Clicking through to the pdf, I now see you have it covered:

“As FSD seems to be always some years away anyway, I think car rentals should be safe for the next 5-10 years and might even benefit.”

If they are safe only for the next 5 years, a PE over 5 is far too high.

As just a service provider for a fleet of Waymos, they won’t generate earnings enough to justify today’s market cap. FSD cars will be able to drive to the pickup point you desire at a time you specify – you no longer need a car rental at home nor in vacation as long as there are enough FSD cars in circulation. FSD does not need to be ubiquitous for Sixt shares to decline. Proof of concept will be enough and the multiple gets hit immediately.

Well, we will need to see how many FSD cars will be in circulation in your favorite holiday destination in 5 years time, how long the waiting times will be and how hight the cost etc. To my knowledge, a Waymo car currently costs around 200K to buy. Not sure if that is then cheaper as a rental car.

A rental car in my opinion serves a different purpose than for instance a taxi and the “proof of concetp” is already heir, at least for sunny California with its wide streets.

We will see, but I am betting that in 5 years time there will not be 200 mn Waymo cars all over the world at each tourist destination.

One final point: This reminds me a little bit about the guy who wanted to short Progressive Insurance 5 years ago because of FSD and because there will be no need for ca Insurance anymore. Progressive is more than 3X since then.

where is that short report to be found? Did (s)he really conclude no car insurance would be needed in the case of FSD?

Maybe one asditional point Someone will need to won and maintain this fleet of cars if that happens. It will not be Tesla nor Google nor Uber.

I suppose this will be like radiologists and AI.

Worth a read: “The “Godfather of AI” Predicted I Wouldn’t Have a Job. He Was Wrong.

Nobel Prize winner Geoffrey Hinton said that machine learning would outperform radiologists within five years. That was eight years ago. Now, thanks in part to doomers, we’re facing a historic labor shortage.”

https://newrepublic.com/article/187203/ai-radiology-geoffrey-hinton-nobel-prediction

I always wonder what kind of moat Sixt has. When I book a rental car, I always take the cheapest offer and that has never been Sixt. And I don’t think other customers are more loyal. But there is one advantage to being a shareholder: Sixt rental cars are available at a reduced shareholder price (-20% 🙂

You have abviously not bothered to read the write-up. I have expected exactly such a comment.

The short answer is: If you are the guy only looking for the cheapest option, you are not the target group of Sixt.

The longer answer is that the “moat” of Sixt is a combination of Financial flexibility and operational excellence, similar to Enterprise, the profitable market leade rin the US:

The market of “cheapest car rental” is very crowded. Most car rentals aim for the same kind of customer.

Bad for the margins.

The market of “premium car rentals” is quite empty. Sixt can easily start there and make its offers for this niche customers with good margins. Perfect USP, good starting point for growth.

The market of “home city markets” was empty until Enterprise came. It is their USP and it was their starting point for an great growth.

roughly 3/4 prefs (old position), 1/4 Common (new)

What is your common to prefs ownership mix I wonder?