Rocket Internet Post Mortem, SpaceX (again) and the strange Google capital increase

Rocket Internet Post Mortem

Last week I mentioned in the comments on the blog and on Twix that I got some “bad vibes” and decided to liquidate my Rocket Internet position even before the planned SpaceX IPO next week.

There were overall 3 things that kind of spooked me and let me to take the profit (+30%) instead of waiting the one more week. Here are the 3 items:

- I mentioned initially, although it was not part of my investment thesis, that there might be a chance of a special dividend. Now it has become clear that there will be no special dividend. However, it also became clear that Rocket Internet intends to limit information flow to shareholders even more in the future which is clearly not positive

- SpaceX: Another news item that spooked me was that SpaceX is aggressively pitching via German brokers for German retail investors. German investors had never access to US IPOs before. Some might find this positive, I find that rather “surprising” and potentially a hint that demand is not high enough for Elon’s appetite.

- Another surprising event was the “surprise Capital increase” from Alphabet/Google. Interestingly, this represented the largest capital increase of all time at 85 bn USD but there was only very limited coverage about it in the financial news and mostly about Berkshire’s participation. But more on this later

Overall, I decided that the “easy money” was now made with Rocket internet and I was able to sell at around 25,80 EUR per share, netting a profit of 30% within 5 months, which is clearly one of my better “Special situations” investments.

I am not 100% sure that the share price increase was driven by SpaceX, maybe the rapid increase in the value of the Kalshi stake helped as well. I am not sure if there are a lot of other “plays” to benefit from KalshI’s incredible growth.

One could argue that I left some upside on the table here but the success of this investment is almost 100% depending for some time on someone else paying me more for the shares that I paid for, which is something I don’t feel too comfortable for a special situation investment.

Overall, I was clearly lucky with the timing on this one.

2. More SpaceX thoughts: Hyperliquid Perps and Damodaran

Since I wrote my update on Rocket Internet and SpaceX a few days ago, quite some things happened.

As mentioned above, we now know that Elon loves Germany so much that at the time of writing, German retail investors can now access this IPO via 8 or 10 different retail brokers.

Interestingly, SpaceX kind of already trades in a synthetic for as a “perpetual future” on a crypto exchange called Hyperliquid:

According to some sources, in order to compare apples to apples, one would need to discount the price by 10% to make it comparable to the actual SpaceX shares. That means on this “grey market”, a synthetic SpaceX share only trades at ~153 USD, above the 135 USD “sticker price” but inside the 135-162 USD bookbuilding range.

Although no one knows for sure if this has any relevance, it is at least a reference point and it seems to be traded quite liquid.

Another interesting source is the attempt of a valuation by Prof. Damodaran. What I like about Damodaran is that he at leasts tries to put values on these kind of situations and is very transparent with his assumptions. I know most tech bros laugh about these attempts but I think avery serious investor should read what Damodaran writes because there is always a lot to learn.

In a nutshell, Damodaran values SpaceX at about 100 USD per share. The ain changes to his initial, pre prospectus valuation is that he increased the margins for the Space and Starlink business, but significantly decreased the expected margins for the AI business.

“My biggest shift is in my estimated target margin is for the AI business, where the dynamics that are pushing gross margins down, i.e., increased competition and high costs of delivering AI services, will persist; my estimated operating margin drops from 45% to 25%. “

Damodaran is also smart enough to mention that in the first days after the IPO, valuation clearly doesn’t matter at all. But within the first 12 months or so, even for SpaceX, reality will need to be met somehow.

For me however the main take away is the significantly reduced margins for the AI business which leads me to the:

Surprising 85 bn USD Capital increase of Alphabet

Being a Corporate Finance/Treasury guy by training, the news that Alphabet is raising 85 bn USD via a capital increase really surprised me.

The “package” itself is quite complex. After announcing initially 80 bn USD in total proceeds, Alphabet ended up with ~85 bn.

According to the FT, this is the largest capital increase in the history of capital markets, the second largest was Petrobras in 2010 at around 70bn.

The financial press focused mainly on the 10 bn stake that Berkshire Hathaway took as part of the package. To be honest, this is a very small amount of money for Berkshire’s current size. It is also hard to really judge how good of an investor Greg Abel actually is.

The interesting thing about this capital increase is that so far, at least in the ~40 years that I follow stock markets, capital increases in size only occurred in the following situations:

- Primary share portion in an IPO

- Emergency capital raising in a crisis ( e.g. Banks in the GFC)

- Major M&A transaction where the acquiring company pays with new shares (Paramount)

In Google’s case, clearly none of the three situations applies. According to TIKR, Alphabet still has net cash despite ~100 bn in bonds outstanding. So in theory they could issue a lot more debt.

I heard the argument that Equity is “cheaper” than debt as the interest rate on a debt offering would be 5% whereas the “earnings yield” at the current 30x P/E is “only” 3,3%. However this does not reflect the tax shield from interest and especially not the fact that Alphabet’s earnings will most likely increase for the foreseeable future and that very soon that “earnings yield” for the issued shares will be much higher than the current 3,3%.

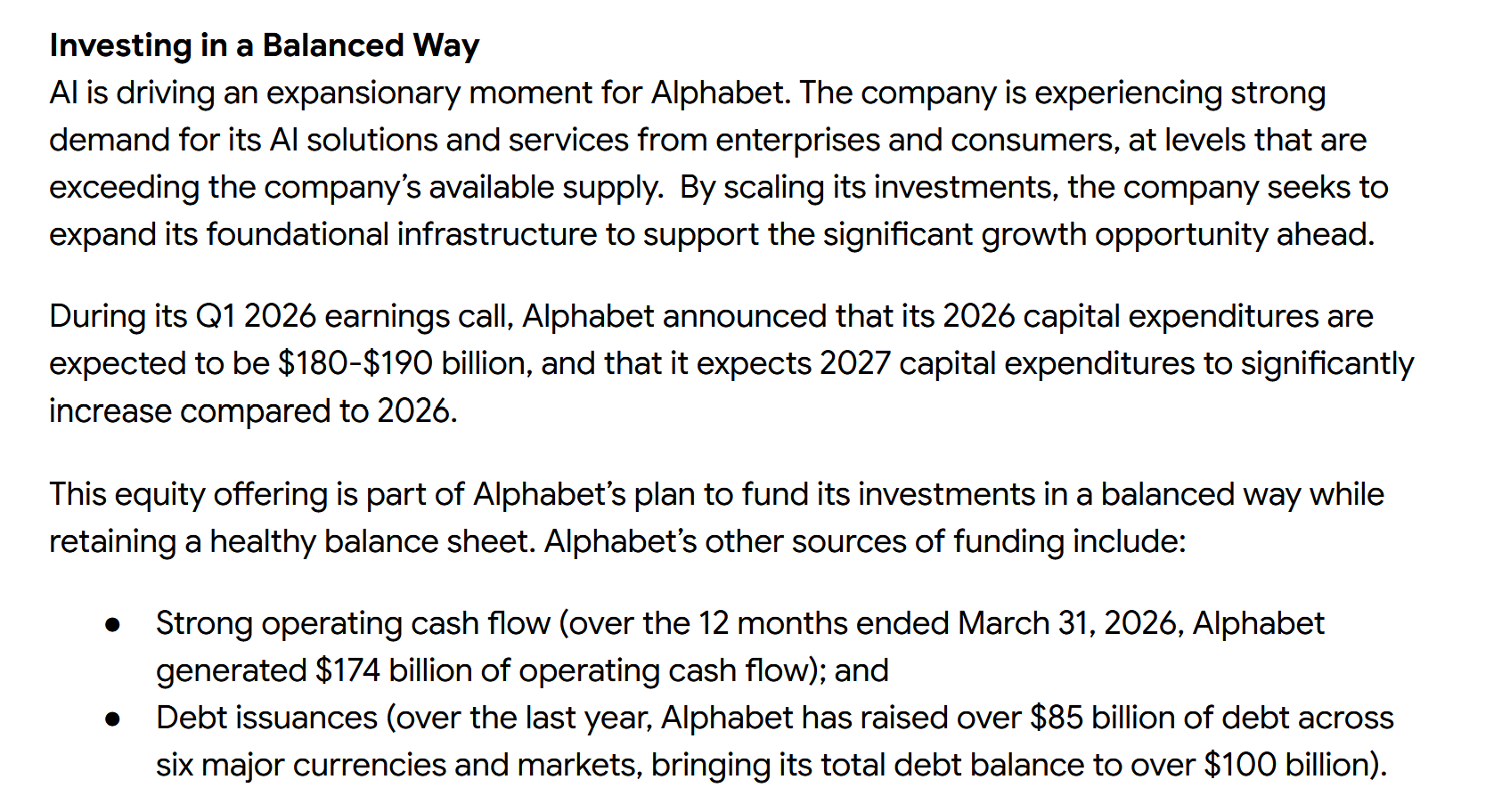

This is the main “justification” of Alphabet for the capital raise besides a 30 bn additional tax bill:

If you read this carefully, it is clear that they could still fund the 2026 Capex more or less with operating cashflow, but already in 2027, they plan to spend much more than that.

The really interesting thing is clearly: What are their plans beyond 2027 ? My best guess is that they plan with even larger investments that are not offset by operating cash flow.

But even so, why not wait until 2027 or so when they have a clearer point of view ? And I think here comes something into play which in my old Corporate Finance days was the golden rule of financing: “Raise when you can, not when you must”.

I think the Alphabet guys might have seen SpaceX’s announcement, they know that OpenAI filed for an IPO and that Anthropic will come to the capital markets as well.

As large as the listed capital markets are, there is only so much appetite for capital increases. Maybe they even fear a significant market correction which would require them to issue a much larger number of shares for the same amount of money.

Funnily enough, there were rumours that even Meta seems to think about raising large amounts of capital to fund their AI Capex programs.

One other factor that might also play a role here is that both, Private Credit and Private Equity which have been offering significant amounts of capital so far fight with redemptions themselves and are potentially overallocated to data centres already.

To me it is pretty unclear where all this is going. However one thing now is clearer to me:

The capital required to scale up this technology is larger than even the latest and best funded players like Google expected.

In my opinion, this means that it is very unlikely that we see 5 companies scaling this in parallel on their own (Alphabet, Meta, OpenAi, Anthropic & SpaceX). 1,2 or even 3 of those players might fold at some point in time or would need to collaborate really closely with someone like Microsoft or Apple to stay in the race. Or get help from the Orange guy in some sort.

Scrutinizing Data Centre Infrastructure orderbooks

For ordinary investors this might also mean to better scrutinize order books of companies that are supposed to profit from a further AI build out and trade at high multiples themselves.

At the moment, it is enough if a company releases “AI data centre” contracts to justify sky high multiples. I guess going forward, maybe even sooner than later, one really needs to understand from which counterparts those contracts are. Because not all of them might be actually turn out to be valuable.

In any case, as someone who loves capital markets, this is a great time to be alive and witness what is going on at the moment.