All Belgian Shares part 7 – Nr. 121-140

It’s Belgian Power Week on the blog this week with a second post in the “All Belgian Shares” series. From these 20, randomly selected shares, 7 made it onto the preliminary watch list, including some really interesting companies. Let’s go !!

121. Galapagos

Galapagos has nothing to do with the Islands in the Pacific but is a Biotech company that has spiked during Covid and lost -90% since then. They do have sales and even some earnings and according to TIKR, they have a negative EV of -1,8 bn.

Gilead owns 25% of the company. For some strange reason, the negative EV attracts me like a fly to the light bulb, so I’ll put them on “watch”.

122. IBA – Ion Beam Application

This 400 mn EUR market cap company according to Tikr “develops, manufactures, and supports medical devices and software solutions for cancer treatments in Belgium, the United States, and internationally”.

The company actually has sales and is waking out small profits here and then and has net cash.

According to their last investor presentation, the company has quite aggressive mid term targets. If they would hit that, the stock would be quite cheap:

This sounds quite interesting, especially as the have net cash and don’t seem to burn much cash. “Watch”.

123. Econocom Group SE

This 393 mn EUR market cap IT distributor is quite interesting, as it is very cheap and seems to buy back a significant amount of shares each year on top of a current 7% dividend yield.

On the other hand, they have significant net debt and the share price has done little for many years. Margins are razor thin, too.

Not my favorite kind of situation, but I still will put it on the preliminary “watch” list.

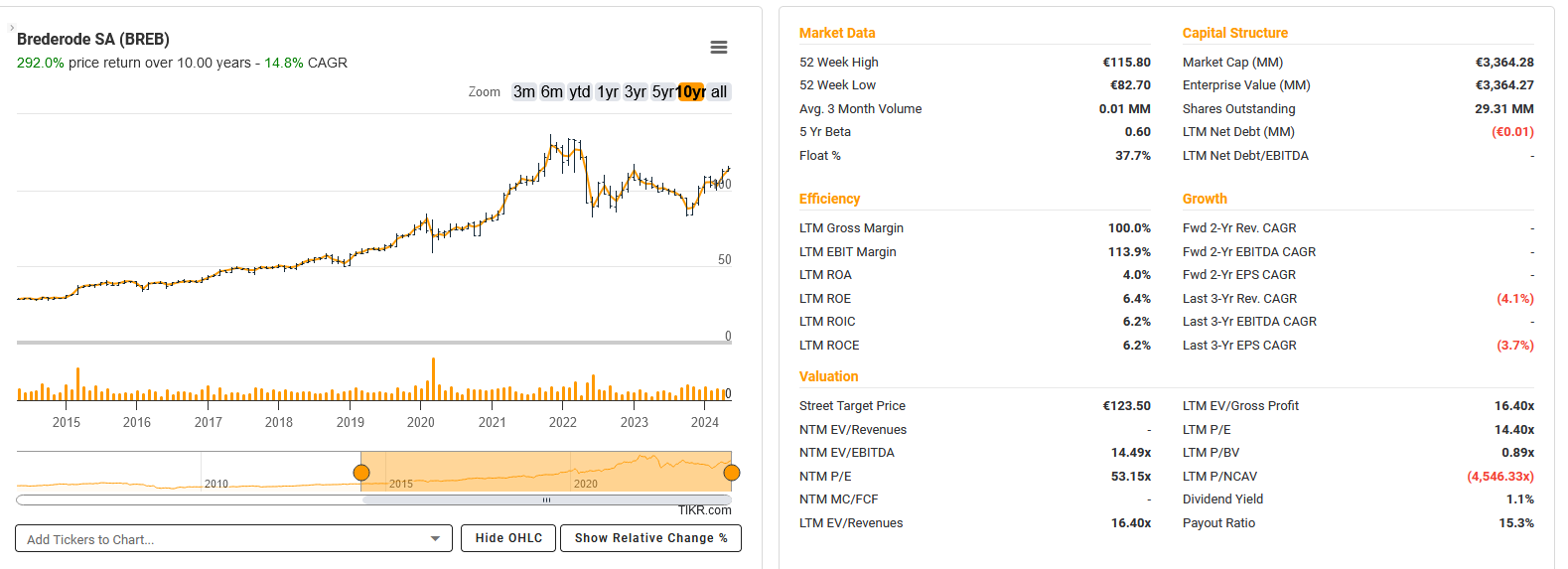

124. Brederode

Brederode is a 3,4 bn EUR market cap investment company that is formally headquartered in Luxembourg but to my knowledge is originally from Belgium.

Looking at the chart, long term value creation looks quite nice with around 15% CAGR over the past 10 years:

⅔ of their investments are in Private Equity, ⅓ in public securities. They have a quite detailed list of their private equity fund investments on their website which is quite unusual.

Their listed portfolio is something like a “large cap quality” portfolio. The NAV at year end was at around 128 EUR, so Brederode traded at a relatively narrow discount of -20%.

Personally, I would not invest here but I think it is an interesting example of a well managed investment company that manages to trade at a relatively narrow discount.

If someone is looking for PE exposure, this might be a better choice than the currently touted “PE for normal investors” offerings. “Pass”.

125. BOUFFIOULX-ST-NICOLAS (Le Patrimoine Immobilier)

This Expert market stock has traded last in 2023. According to Euronext “Bouffioulx-St-Nico is a real estate certificate issued by the company Le Patrimoine Immobilier. The activity of the company Le Patrimoine Immobilier consists in issuing certificates that gives the right to a quota of the distributions and determined property deals income.” As I am not interested in Real Estate, I’ll “pass”.

126. AGENCE MARITIME MINNE

This Expert Market stock seems to have never traded. “Pass”.

127. Banimmo

Banimmo is a 38 mn EUR market cap real estate company that has been flatlining for many years. It seems to be a subsidiary f a Life Insurance company. “Pass”.

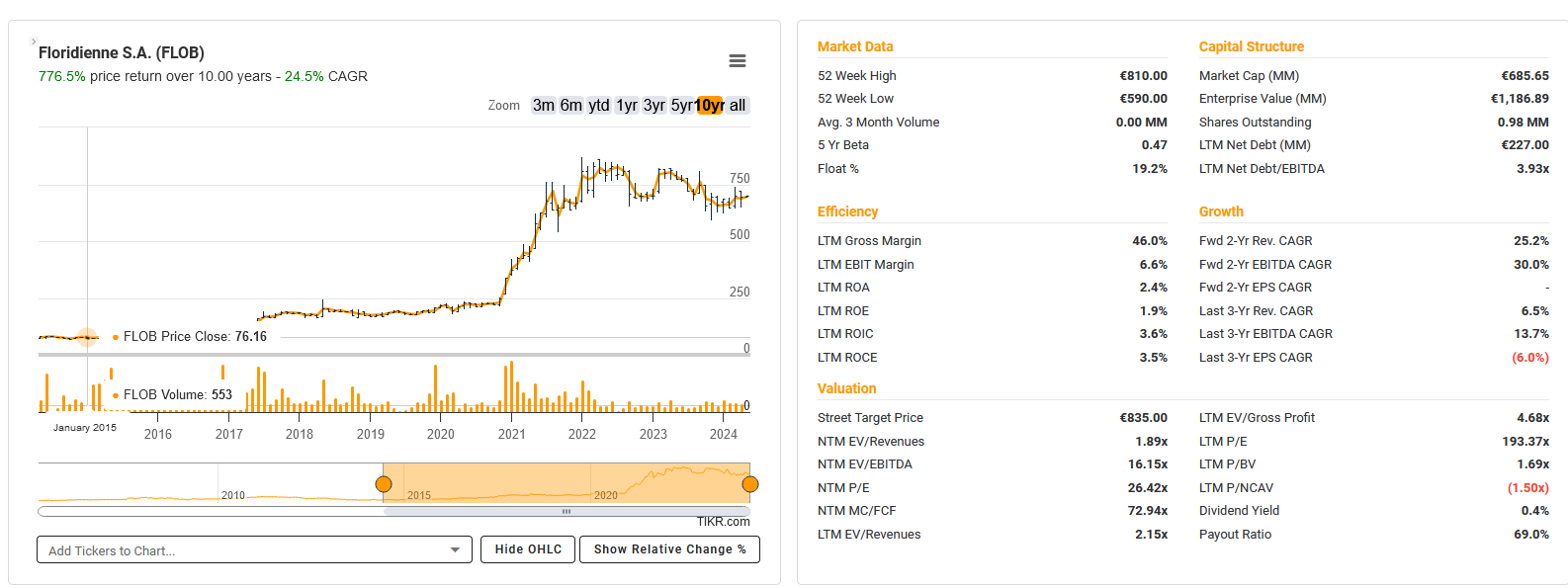

128. Floridienne

Floridienne is a 686 mn EUR market cap Holding company that produces an amazing wide variety of products, from Chemicals to Gourmet Foods and also recycles Batteries. Equally amazing has been the performance over the past 10 years:

The stock first climbed slowly, but then took of like a rocket in 2021, doing overall 8X over the past 10 years.

If I understand correctly, their largest division, Biobest, offers biological solution for Farmers to fight insects and diseases. And they just did a very large acquisition in Brazil at year end 2023. The P&L does not really tell the story why the share price went up so much in the last year. Maybe some readers know more ? Happy to hear. Anyway, this is clearly one to “watch”.

129. Roton

This Expert Market stock actually traded in 2024. According to Euronext, this seems to be an insolvent coal mine. “Pass”.

130. Old England

This Expert MArket stock traded last in 2015. “Pass”.

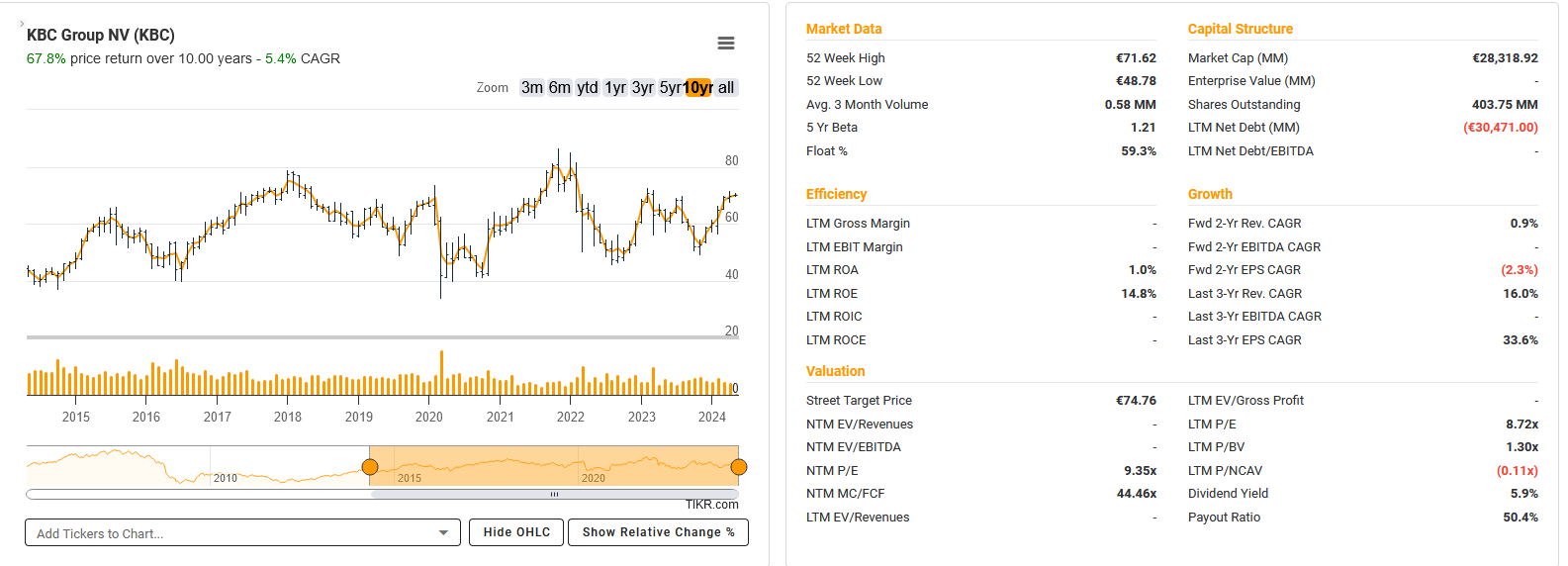

131. KBC

With a 28 bn market cap, KBC is clearly one of the larger European banks. Looking at the chart we can see that the share price has been oscillating up and done without a trend for some time:

As many other banks, the stock is quite cheap at a P/E of 9. The ROE is quite good, on average like 12-14% p.a. which explains the 1,3x P/B valuation.

This is clearly a decent bank but not what I am looking for, “pass”.

132. Moury Construct SA

This 218 mn EUR market cap construction company, owned 60% by the Moury family, has a quite unusual chart for a construction company:

The stock more or less tripled over the past 3 years:

Looking at the details, Moury could actually increase earnings by 6x over the last 6 years. To be honest, I did not find out why Moury has done so well over the past 3-4 years, maybe again, some of my readers could enlighten me why they have done so well.

One interesting aspect is that Moury always looked extremely cheap based on EV multiples, most likely due to prepayments from clients.

In any case, this is a “watch”.

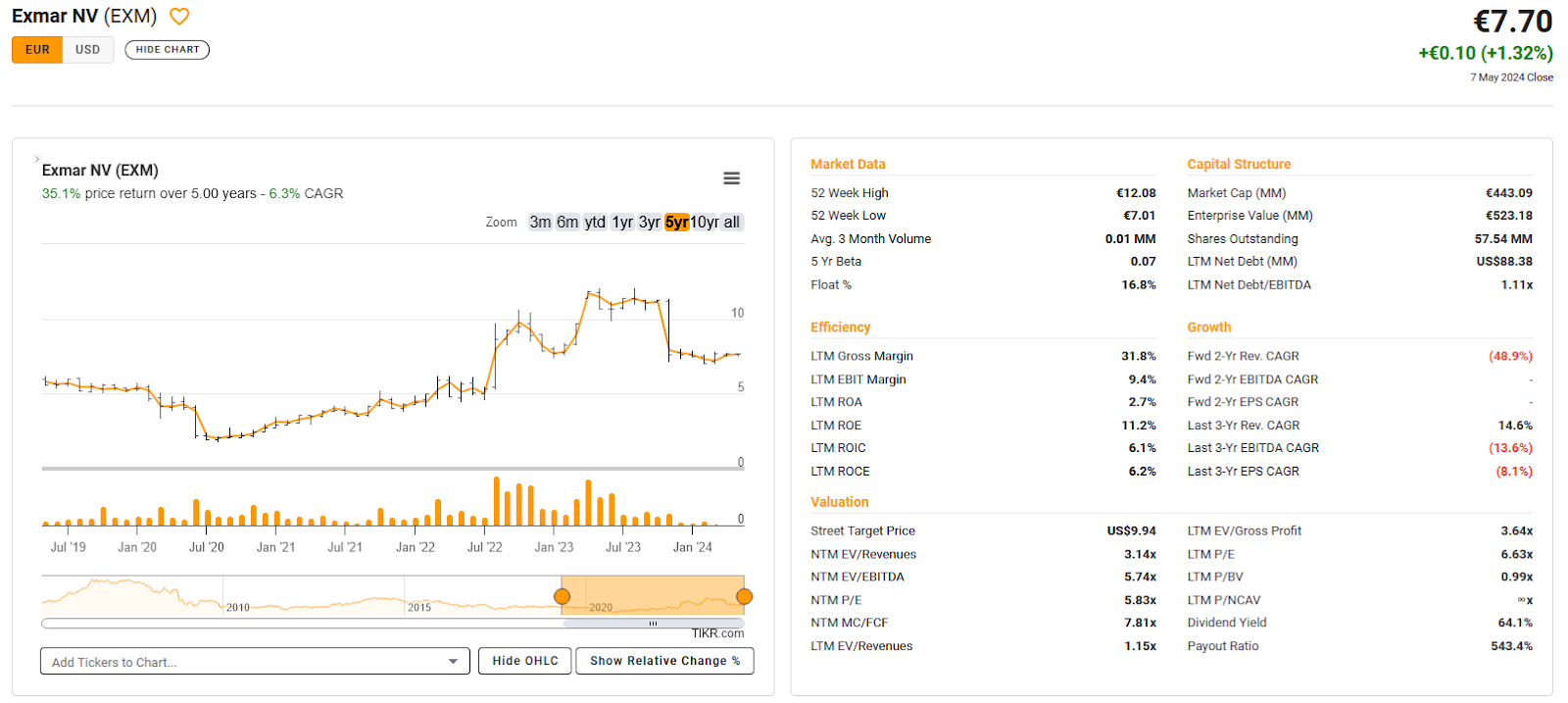

133. Exmar

Exmar is a 434 mn EUR market cap shipping company and an “Old friend of the blog”. I invested into Exmar as a special situation in 2022 when it became clear that they would divest theri LNG assets at a very high price.

The paid out a fat extra dividend of more than 5 EUR per share in 2023. Earnings for 2023 have been very solid and the stock looks cheap. It seems that the generational handover within the Savery family just happened in January. In the annual report 2023 they mention Green Ammonia as a major driver for the future. Overall, despite the volatility of shipping, this stock is a “watch”.

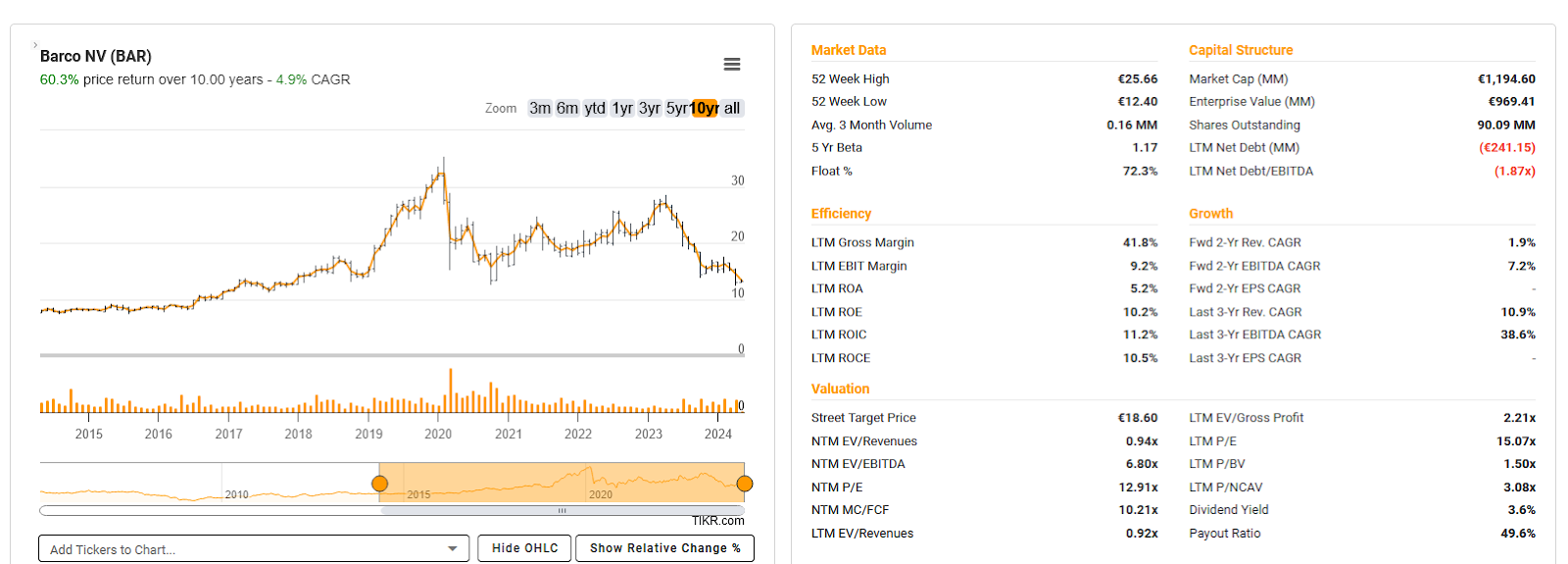

134. BARCO

BARCO is a 1,2 bn EUR market cap that “develops visualization solutions for the entertainment, enterprise, and healthcare markets in Belgium and internationally.”

The stock of BARCO has been quite volatile as we can see in the chart:

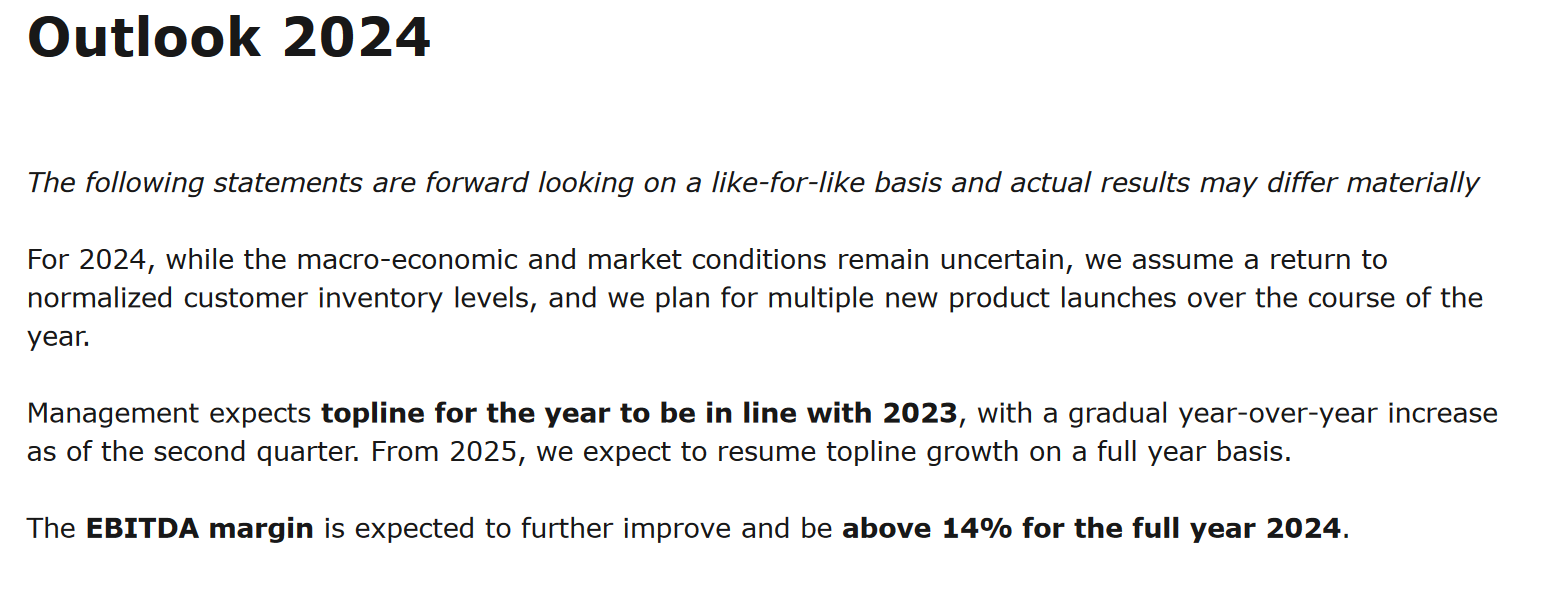

Barco runs 3 segments, Healthcare, Enterprise and Entertainment. 2023 numbers were quite solid. Barco has also give a quite optimistic 2024 outlook with further margin increases:

Interestingly, the company has a significant net cash position. Q1 was relatively weak, however management confirmed the 2024 outlook.

Overall, this looks like a potentially interesting situation, so I’ll put them on “watch”.

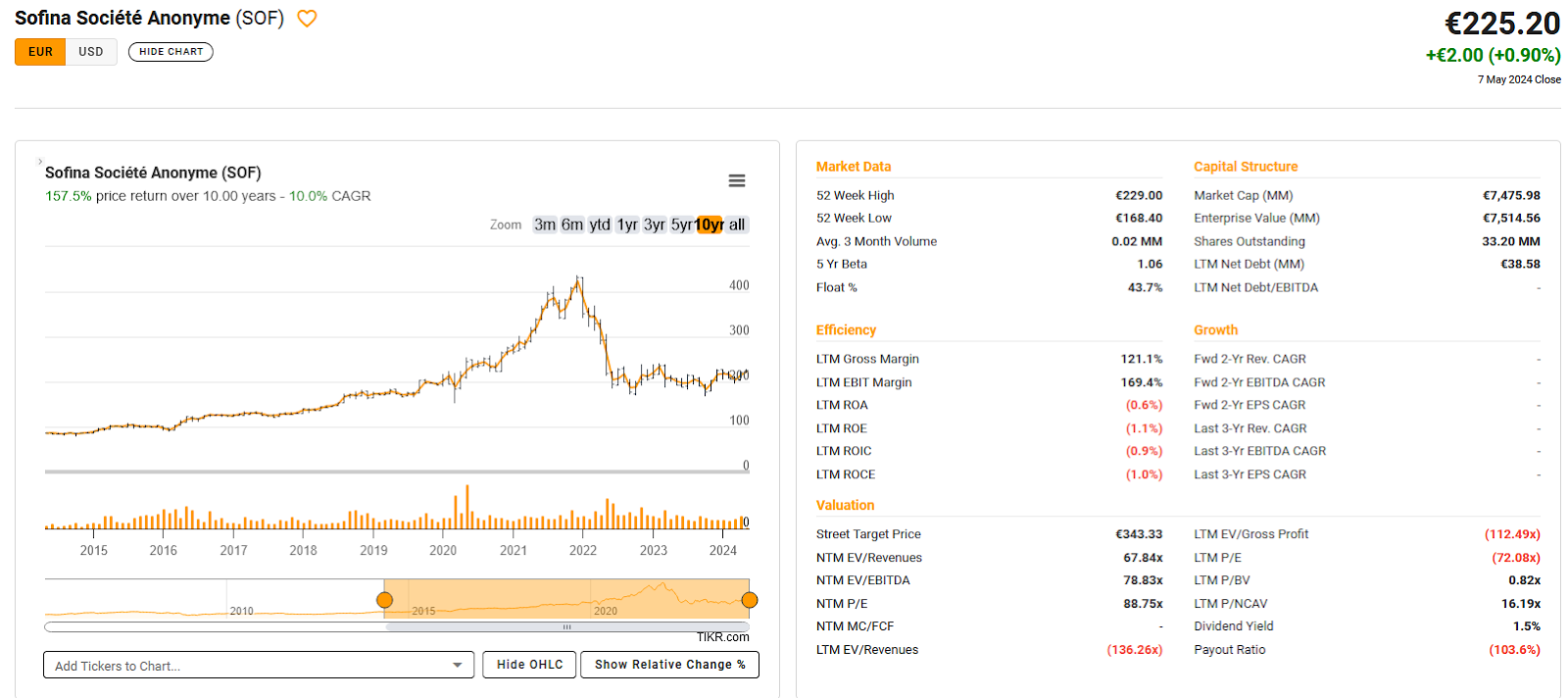

135. SOFINA

SOFINA, with a market cap of 7,5 bn EUR is one of the largest Belgian Investment companies.

Looking at the stock chart, we can see that SOFINA participated in the Covid Bul-run but then lost almost -50%:

This is a decent page from their IR presentation showing both, the general portfolio set-up as well as the NAV discount:

Digging one level deeper, the portfolio looks quite “Techy” with Bytedance (TikTok) as the second largest direct holding.

For someone interested in a diversified Tech/VC Portfolio, this could be interesting, for me it is not the right thing, therefore “pass”.

136. Charbonnages du Bois-du-Luc

This Expert Market stock has been traded last in 2015. From the name it seems to be a (Former) coal mine. “Pass”

137. BOUWONDERNEMING VOORUITZICHT

This Expert Market Stock has also traded last in 2015. “Pass”.

138. Growners

Growners is an Expert Market stock that according to Euronext “specializes in professional real estate trading services”. Last trade was in 2021. “Pass”.

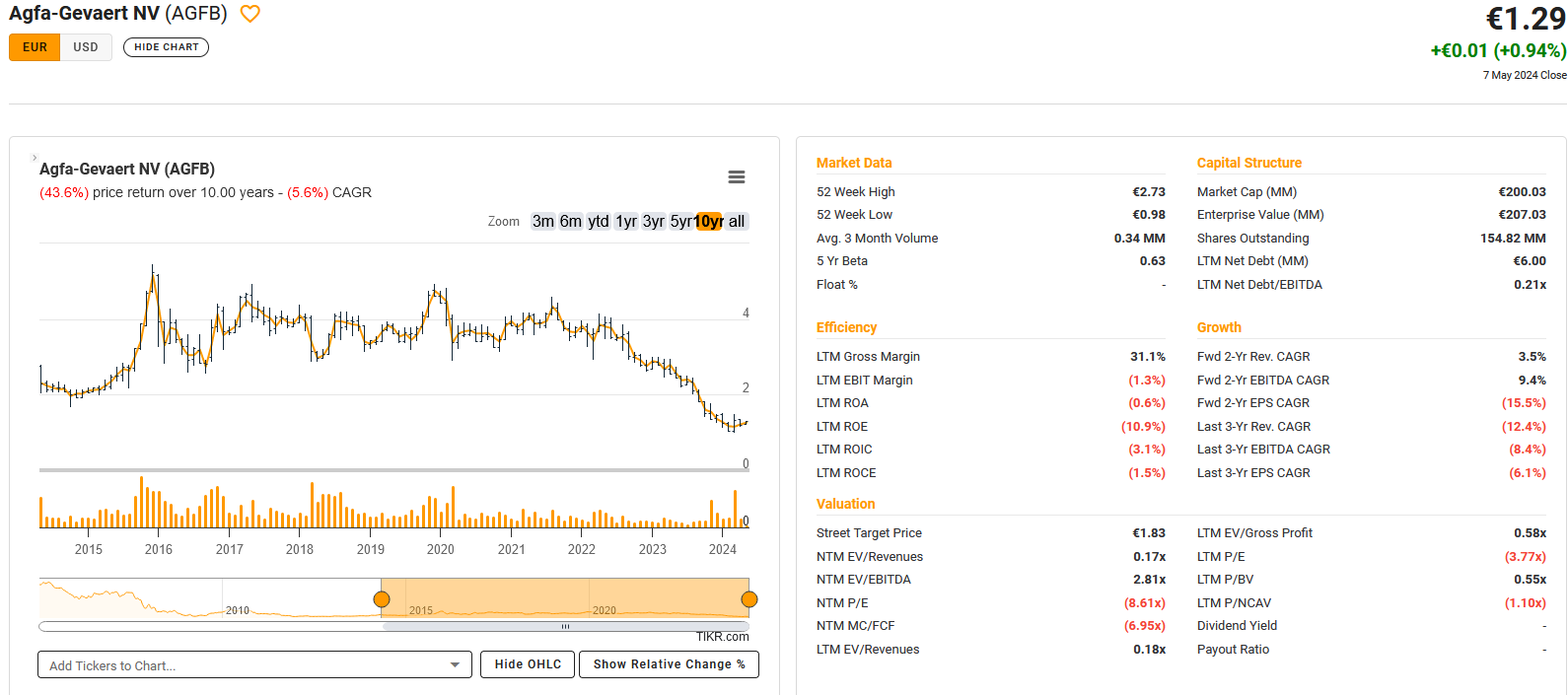

139. AGFA Gevaert

AGFA is a 200 mn EUR market cap company that was part of the V&O Portfolio only a few months in 2020.

Back then, it looked like an interesting “Some of the parts” turnaround story with an activist present.

But obviously that hasn’t worked out as we can see in the chart:

Although they got rid of the offset business to german Aurelius some time ago, all the remaining divisions were struggling, especially the largest one, Radiology which seems to have significant China exposure.

Nevertheless, I would want to make a deep dive into AGFA at some point, therefore I’ll put them on “watch”.

140. TISSAGES BRUGGEMAN

And yet another Expert Market stock which traded last in 2015. “Pass”.

Hi,

Here a reader from Belgium.

About the Floridienne rocket climb:

Biobest did a series of capital increasese to finance it growth, financed by external partners (PE mostly)

and those capital increases repeatedly valued Biobest at a considerable amount of money.

The latest one, in 2023h2, for the big Brazilian acquisition you mentioned, raised > 350 MEUR

https://www.floridienne.be/wp-content/uploads/2024/01/FLO-G01-20231226-Acquisition_Biotrop_EN_v1.pdf (bottom)

with Floridienne ending up with 59% stake in a company valued at 1465 MEUR,

so Floridienne’s stake is valued at 865 MEUR.

There are close to 1M shares, so you don’t need a calculator for the per share numbers 🙂

Some extra history:

In the past , the value of Floridienne was not so transparent (e.g. a holding, but no NAV). Very low free float also, so no professional investors. Amongst the many, many businesses, it had some businesses that did not perform very well. It’s historical core, Floridienne Chimie, struggled for years and even went into „chapter 11“ in 2014.

But Biobest was growing nicely, first through rather small acquisitions in a very fragmented market.

As these acquisitions expanded (Australia, US) and grew in size, Floridienne had no longer the capital to finance the grow path and needed external investors. A series of capital increases followed, more and more fresh capital at a valuation that went up considerably:

https://www.floridienne.be/wp-content/uploads/2018/05/20180503-Capital-increase-Biobest-EN.pdf 10 MEUR new capital @ 155 MEUR valuation (pre-money, equity value)

https://www.floridienne.be/wp-content/uploads/2021/06/FLO-G01-20210609-Augmentation_capital_BBE_MERIEUX_EN.pdf 10 MEUR @ 450 MEUR

https://www.floridienne.be/wp-content/uploads/2023/02/FLO-G01-20230203-Augmentation_capital_BBE_EN-1.pdf 100 MEUR @ 1.000 MEUR

https://www.floridienne.be/wp-content/uploads/2024/01/FLO-G01-20231226-Acquisition_Biotrop_EN_v1.pdf 365MEUR @ 1.100 MEUR

These valuations by professional parties propelled the Floridienne share price upwards.

One of those investors is Sofina: a very big name in Belgium. First through Merieux, then directly. In fact, Biobest is in the list of Sofina’s biggest participations you posted in the article.

The downside of all this external capital is that Floridienne’s ownership of Biobest has been watered down considerably: from close to 100% -> 59%.

A personal note:

I only now took the time to create an accout to comment, but I’ve reading your blog since 2017, when I stumbled upon it when searching for more info on the SAPEC special situation.I learned, amongst other things, how such a situation looks from a foreigners (tax) perspective.And again for Exmar.

Always interesting to read!Much appreciated.

Keep up the good work!

Main concern here is how to immunize my equity portfolio against prospective/imminent(?) headwinds. Not that easy…

I think you can remove Galapagos from your “watch list”.

That’s a full bullshit company imho

The reason why Gilead is a shareholder:

Gilead made a big bet on their JAK inhibitor filgotinib, but it didn’t get approved in US as originally planned.

https://www.gilead.com/news-and-press/press-room/press-releases/2019/7/gilead-and-galapagos-enter-into-transformative-research-and-development-collaboration

and later on they pivoted to CD19 CAR-T. Not really familiar, but it looks like me too.

you have an overview here

https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9175669/

Thanks. Appreciated.

Galapagos got a lot of money from Gilead for filgotinib, wich looked very promising, but then it went wrong @FDA.

Now, they have recently sold filgotinib, and are basically an early-stage biotech company again without earnings. But, atypically, with a big cash war chest. You can be sure however that cash will be spent gradually on research costs and/or acquisitions. The result/value of which is anyone’s guess. That’s why the market values the cash at a discount.

Cash vs. Market Cap (in billions of € )

The discount won’t disappear quickly.

And 1/3 of the initial cash has been spent over 4 years.

But still, a 50% discount is a lot.

I think Barco is a serious opportunity here. The CEO seems to think so too, and he has bought €12-13m in shares over the past two weeks. The Chairman’s PE (3D) has also bought €3-4.https://www.fsma.be/en/transaction-search?issuer=159092&date%5Bmin%5D=&date%5Bmax%5D=Entertainment and Healthcare are growing markets and will come back after the recent destocking. Barco has a dominant position in both. Well, the cinema part of Entertainment is not a growth market, but I hear they have close to 65% market share in new projectors after Sony pulled out (vs 50% in installed based). The only doubt is Clickshare, but it’s been a doubt for more than 5 years and keeps staying relevant so there must be something to it. Very clean balance sheet with all the R&D (c. 12% of revenue per year) expensed, which suggest healthy new product pipleine ahead.

Agfa is incredibly cheap but less well positioned. 50% of their radiology profits comes from consumables (hardcopies), which is a declining market (to the benefit of Barco’s screens). I do think they have an opportunity in hydrogen, but they need a lot of capex (50+m) to exploit it, which they do not have. They are probably trying to sell the software business which is nice but I don’t think can competer with Carestream (Philips). Pension liability something to bear in mind, but higher rates help.

Thanks for the insights

How important is the medical monitor business for BARCO? Are they at risk due to the technical gap between dedicated medical screens and premium gamer/corporate screens narrowing considerably in the last few years?

Flatscreens for medical use are typically certified by some regulatory instance. I wonder if other screens would undertake the pain & costs of certification. I used to work close to both Agfa and Barco digital imaging tech teams.

All the hydrogen economy predictions and fantasies are blatant nonsense to me. I am quite sick of technically unqualified big mouths. But I guess free of speech is about that