Agfa Gevaert (ISIN BE0003755692) -An Ugly Duck with some Golden Eggs in its nest ?

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

Intro

Agfa-Gevaert was on my research list for some time now. Fellow blogger Undervalued Shares than triggered my renewed interest with their post from a few days ago and one of my best “Special situations” ideas ever was a Belgian company (Sapec).

I’ll try to summarize the part of the post that deals with Agfa:

- Active Ownership, a relatively new but successful German activist fund (Stada) has build up a position (~14%] and board membership (actually the Chairman) in Agfa Gevaert, the traditional German-Belgian film / imaging company

- Despite having some interesting assets, Agfa didn’t create shareholder value over a long time

- opaque reporting and a 1 bn EUR pension liability made it unattractive to stock market investors

- In 2020, Agfa managed to sell part of its Healthcare IT segment for 975 mn EUR

- Initially, the stock went up to ~5 EUR based on the first info on the sale but hasn’t fully recovered yet

- Major question is how the cash will be used. A 50 cent tax free dividend and a 20% stock buyback seem to be likely. Part of the money could be used to plug the 1 bn EUR pension hole partially and part to develop the remaining most attractive asset, radiology

- Overall the author sees a good chance of the share price going to 5 EUR within the next 6-24 months

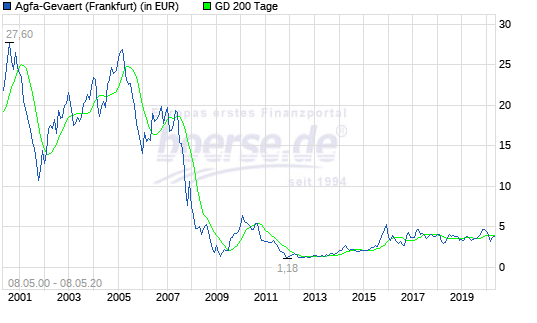

Agfa historically

The long term share price development looks quite depressing since the spin-off from Bayer AG in 1999, the company currently has a market cap of around 640 mn EUR (3,8 EUR/share):

Also looking at the 5 year figures we can clearly see that Agfa is not a beautiful swan in aggregate but a very ugly duck at first sight:

| Agfa 5Y | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|

| Sales | 2646 | 2537 | 2443 | 2191 | 2239 |

| Gross profit | 842 | 857 | 814 | 701 | 729 |

| Operating profit | 161 | 166 | 138 | 62 | 14 |

| Net income | 62 | 70 | 37 | -24 | -53 |

| Restruct. | -19 | -42 | -31 | -66 | -12 |

| Adj. Op. profit | 180 | 208 | 169 | 128 | 26 |

| Op CF | 149 | 142 | 40 | -44 | 123 |

| CapEx | -37 | -44 | -46 | -40 | -38 |

| Free CF | 112 | 98 | -6 | -84 | 85 |

| Dividends | 0 | 0 | 0 | 0 | 0 |

| Net debt | 58 | -18 | 18 | 144 | 219 |

| Gross margin | 31.82% | 33.78% | 33.32% | 31.99% | 32.56% |

| Operating margin | 6.08% | 6.54% | 5.65% | 2.83% | 0.63% |

| Net income margin | 2.34% | 2.76% | 1.51% | -1.10% | -2.37% |

| Adj. operating margin | 6.80% | 8.20% | 6.92% | 5.84% | 1.16% |

Sales have retreated for years and 2018 and 2019 Agfa had to book a loss on an aggregate basis. In a typical “stock screener” Agfa looks unattractive from almost any angle. The book value is low and has been eaten up by the pension deficit, aggregated EV/anything numbers do not look good because of the bad segments and the restructuring expenses.

Under the hood: Very different businesses

Under the Agfa “hood” however, Agfa has gathered a number of very distinct and different businesses. The main business lines are as follows:

- Healthcare IT (part of this was sold as outlined above) – 505 mn sales, 63 mn adj. EBITDA

- Radiology Solutions, another Healthcare tech business line that could be attractive – 536 mn Sales, 88.5 mn adj. EBITDA

- Digital Print & Chemical – at first look an “ok but not great” business – 355 mn sales, 29,5 mn adj. EBITDA

- Traditional Offset business which seems to be the least attractive part but has the largest share in sales – 843 mn sales, 16.5 mn adj. EBITDA

3 step Sum of part valuation

Whenever you have such a sort of diverse businesses under one roof, a sum of parts valuation makes sense. The problem with a sum-of-part valuation is often, that the value will never realize and value is destroyed along the way through bad capital allocation (good businesses are capital starved and the holes in the bad businesses get plugged over and over again). I guess this has played out at Agfa over the last decade or so.

In Agfa’s case however NOW there is a clear catalyst with the presence of an activist owner and a first realized transaction that shows the potential.

Step 1: Determining economic debt (Net debt / pension liability)

According to the annual report, net debt amounts to 219 mn EUR at the end of 2019 (I do conservatively not adjust for capitalized leases). With the proceeds of 975 mn EUR for the sale of the Healthcare IT business, net cash in theory would be ~760 mn or ~120 mn more than the market cap. In technical terms we would have a “negative EV” stock which looks like a nice and tasty free lunch and a no-brainer.

However the issue are pensions. As of year end, the recorded net liability was 1.028 mn EUR. As I have mentioned in the past, a pension liability has to be treated as financial debt. Also the net liability is not the best indicator.

For a “mark to market” we need to make a few assumptions:

- interest movement since December 2019

- development of trust assets

- Required Buffers

Agfa disclosed sensitivities of 75 mn EUR of the liability for a 0.25% reduction in interest rates. Looking at the market, we can see the following developments since year end:

UK 10 year Govies -0,5% lower

US 10 year Govies -1,20% lower

Germany 10 year Govies -0,25% lower

Unfortunately, we do not know the split of the reserves. We know roughly that Germany accounts for 700 mn unfunded reserves. Let’s assume that a further 300 mn are EUR denominated and the rest is split 50/50 between UK and the US, then we have the following economic decrease of the discount rate of ~0,58% or an increase of the liability of ~(0,58/0.25)*75 = 175 mn EUR.

A further assumption would be that the overall value of the investments remains stable (gains on bonds are eaten up by the losses on the stocks).

In addition, I will assume that a 10% Buffer on Gross liabilities (2.24bn) should be applied to adjust for other risks (mortality, inflation). This adds another 224 mn EUR to the MtM pension liability.

Overall indebtedness and EV for Agfa look like this:

| mn EUR | |

|---|---|

| Net debt 12/2019 | 219.0 |

| Net pension IFRS | 1028.0 |

| Mtm pension 2020 | 174.7 |

| 10% buffer on gross pension | 224.2 |

| Cash from Healthcare sales | -975.0 |

| Net economic debt MtM | 670.9 |

| Market cap (3.80) | 637.0 |

| Total EV | 1307.9 |

Step 2: Valuing the Businesses

HealthCare IT

The HealthCare IT division’s top line increased by 3.0%. Throughout the year, the HealthCare Information Solutions business continuously recorded solid top line growth, confirming its leading position in the German speaking countries of Europe and in France.

This is the part where they had actually done the first sale. We do not know the actual income attribution to the sold segment. A rough estimate would be that the sold entity has ~200 mn EUR sales.

For the Imaging IT Solutions business, the division focuses on generating ‘quality turnover’ in selected geographies and segments to further improve profitability. In spite

of the decision to wind down the Imaging IT Solutions from certain less sustainable

markets and segments, this business’ top line remained stable versus the previous year.

I assume the entity has the remaining 305 mn EUR in sales out of a total 505 mn for this segment. A potential comparable company to that segment would be Sectra AB from Sweden. Sectra has very decent margins (17% Operating margin) and is growing nicely. Sectra trades at around 8x sales and 82xPE. Agfa’s business clearly does not grow that much and is less profitable. However for a sum of part valuation I would assume 2x – 4.0x sales as a potential range of value estimates and I will use 3x sales as the midpoint which results in a value of 915 mn EUR (or 3/8 of Sectra’s multiple)

Radiology Solutions

In the Radiology Solutions division, the top line growth of the hardcopy and Direct

Radiography ranges was partly counterbalanced by the market-driven decline in Computed Radiography sales. Clearly benefiting from the reorganization of the distribution channels in China, the hardcopy business posted double-digit revenue growth. The top line growth of the innovative Direct Radiography solutions range was also based on increased service revenues.

I am not sure if it is 100% comparable, but it looks like that RadNet Inc from the US is somehow comparable, at least they also specialize in radiology solutions.

The company has around 1.1 bn in sales and is valued at ~730 mn Equity and around 700 mn in debt. That translates into roughly 1.3 times EV/Sales and around 9x EV/EBITDA. Agfas Radiology business had 536 mn EUR in sales and 88.5 mn EBITDA. If I average the two multiples, I get a value of 737 mn EUR for Agfa’s radiology business.

Digital Print & Chemicals

Based on its strong performance of its core businesses, the Digital Print & Chemicals

division’s topline increased by 5.5%. In inkjet, the ink product ranges posted volume and revenue growth. Large-format equipment sales were also up, based on the success of high-end systems such as the Jeti Tauro H3300 LED.

In the Industrial Films and Foils segment, the Synaps Synthetic Paper range performed

well, as Agfa’s paper range is being distributed in an increasing number of geographies.

The Electronic Print segment’s Orgacon Electronic Materials range also reported good

sales figures. Furthermore, the division is making progress in a number of promising

new business areas. For instance, the rise of the hydrogen economy is leading to an

increased interest in Agfa’s membranes for alkaline water electrolysis.

For this segment, I make my life easy: I just use Fuji Films from Japan as a proxy, which trades at 0,9x sales and seems to have a somehow similar business. With 355 mn EUR in sales, that results in a 317 mn valuation.

Offset Solutions

The Offset Solutions division’s revenue remained almost stable at 843 million Euro.

Mid 2019, the consolidation of the sales coming from the alliance with Lucky HuaGuang

Graphics started to show in the division’s top line.

The Offset Solutions division is active in structurally declining markets. The offset industry is marked by the strong decline in demand for analog prepress technology and

decreasing newspaper and commercial print volumes. The division also continues to

face price pressure, caused by intense competition, as well as high aluminum costs.

Going forward, new challenges such as the corona virus outbreak could also affect the

division’s results. The developments in the offset industry explain the booking of an

impairment loss by the Group in the fourth quarter.

This is clearly the weakest business. EBITDA dropped from ~40 mn in 2018 to 16 mn in 2019.

For valuation purposes I use avg 2018/2019 EBITDA of ~30 mn multiplied by 6, resulting in an EV of ~180 mn EUR

Step 3: Deducting for Corporate Center / overhead

As I have found no real numbers here, I do a “wild guess” adjustment of -100 mn for all corporate functions.

Bringing it together: Sum of parts

So this is the total summary:

| Total sum of parts | mn EUR |

|---|---|

| Net debt | -670.9 |

| Value Imaging business | 915.0 |

| Value Radiology | 737.6 |

| Value Digital & Chemicals | 316.0 |

| Value offset | 180.0 |

| Minus Holdco | -100.0 |

| Total sum of parts | 1377.7 |

| per share | 8.21 |

| Current share price | 3.8 |

| Theoret. Upside | 116.12% |

My quick and dirty valuation has resulted in a theoretical value of more than twice the current share price. Of course, as this is a “quick and dirty” exercise, I could be off several hundred mn EUR in any direction.

There could also be negative effects from Covid-19, although I guess the healthcare businesses which are the main drivers should be not affected too badly.

However, as the adjustments could go either way and my debt assumptions are rather conservative, the stock looks attractive at current prices.

Additional considerations: Time horizon, share buy back & Management incentives

First the time horizon: My theoretical value will not land on my bank account any time soon. So it is fair to assume that the stock price will only gradually move up to the fair value. My estimate is that the full value might only be realized in 3-5 years.

Another interesting aspect are share buy backs: If a stock is as undervalued as Agfa looks like, a share buy back can increase the upside considerably. Here is an example of a 200 mn EUR share buy back:

| Share buy back example | |

|---|---|

| Amount | 128,000,000 |

| Purchase price | 3.8 |

| Purchase Shares (mn) | 33.7 |

| Sum of parts value new | 1250 |

| Shares count new (mn) | 134.1 |

| Value per share | 9.31 |

| Value uplift | 13.5% |

| Upside | 145.3% |

All other things equal, a 20%/128 mn share repurchase would increase the intrinsic value per share by 13,5% and lead to a significantly better upside for remaining shareholders.

By coincidence, this 20% share repurchase was just approved in today’s AGM 😉

Management compensation and alignment with shareholders is unfortunately not super clear from the annual report. There seems to have been a special bonus for the sale of the Healthcare IT business but I did not find details. I didn’t find any details on the compensation package of the new CEO who started on February 1st 2020. The old management compensation plan was rather bad, with among others, absolute EBITDA being one of the targets without taking into account returns on capital. I guess the activist shareholder will align this going forward with shareholder value creation.

Why is the stock (still) cheap ?

From the outside, it seems a combination of bad management, “Bad screening”, difficult to understand structure and a 15-20 year stretch of stock market disappointment that explains the current valuation. The real question is: Why didn’t have anyone else the idea to “kiss this frog” ? I don’t know.

Risks:

There are of course many risks, Covid-19 is only one of them. Others are:

- UK pension plans are notoriously difficult to handle

- any of the businesses could take a turn into the negative and/or the adjusted EBITDAs are not sustainable

- Selling the German based offset business with its unfunded pension liabilities will not be easy.

- The Activist could sell out quickly and/or lose interest if they see a better opportunity etc.

- I am not an expert in healthcare stocks and my crude valuations could be WAY off any real value

On the other hand, other then many turnaround cases, the company has after the sale a lot of financial flexibility which you normally don’t see in such situations.

The just released Q1 numbers look relatively solid with debt debt having decreased by around 50 mn EUR and limited effects of Covid -19.

Summary:

My “quick and dirty” analysis resulted in a significant upside for Agfa Geveart shares. The presence of a good activist investor and an already executed transaction strengthens the case that the “Hidden” value will be actually realized over time.

Therefore I allocated a 5% position of my portfolio into Agfa as “special situation” at a price of ~3,80 EUR/share. My target would be all-in 100% gain over 3-5 years.

Why 5% allocation ? I do think the stock is as attractive as German Startups Group and FBD and therefore I weight them accordingly. As with the 2 other special situations, I do like the “idiosyncratic” risk aspects of the stock.

I fully exited Agfa Gevaert today. Main reason: Portfolio cleaning, kicking out lower conviction titles. I am also indirectly invested via the AOC funds.

Great work. Maybe an update at some point in the future ? What about radiology and why taking the multiple from radnet which has a stable model as a Service Provider rather than selling old fashioned radiology plates ?

50 mn EUR Share buy back announced today:

https://finance.yahoo.com/news/agfa-gevaert-group-launch-share-064500640.html

Not sure why this should make the company 50 mn EUR more valuable but I don’t want to complain either.

It is called “thesis creep” (look it up if you do not know) and it is dangerous:

1. Activist jumps ship – “No problem, the answer makes sense.”

2. No capital return – “No problem, bad time, they will do it later.”

3. Business not doing well – “No problem, it’s covid.”

Short interest is rising as well.

I would look at the original thesis and see if it is still intact. Looks broken to me.

Well if you say so…

To be honest: Yes, esp. the off-set business is doing worse than when I invested but this is indeed due to Covid-19. Stuff happens.

With your 1. & 2. I can still sleep very well and wait for the next 2-3 years.

I wonder whether the 50% of my former colleagues that work in Agfa are doing HomeOffice or in Mortsel. The other 50% have no material impact wherever they are. Maybe better they stay at home (where at least they cannot disturb)…

Actually, the activist didn’t quite jump ship but recently stocked up some more…

https://www.fsma.be/en/aoc-value-sas-3

Very interesting interview with Röhrig:

https://www.tijd.be/ondernemen/algemeen/ik-een-pitbull-zo-ga-ik-niet-te-werk/10253301.html

TLDR:

– No plan to exit Agfa, they see the potential to create value

– Obviously no plan to pay down the pension liabilities all at once: slice and dice-approach

– no decision to sell the remaining hospital software: Option to expand it from France/Germany to USA/UK

– cash distribution to shareholders later: “the cash does not run away”

Thx !!!!

Agfa released 6M numbers yesterday:

https://www.agfa.com/corporate/news-item/agfa-gevaert-in-q2-2020-strong-improvement-of-imaging-it-business-profitability-significant-covid-19-impact-on-printing-activities-regulated-information/

In my opinion OK, other investors might have hoped for more/better results it seems.

I think some investors hoped for some sort of cash return in the short term and got disappointed. But to execute share buybacks now would have been very ill-advised, when laying off workers and closing sites on the other hand – so I was actually expecting a delay here.

A slight negative was the size of the remaining HealthCare IT unit with only 117 M€ sales for H1 (and I see you have assumed 300 M€ for the full year as well), though the profitability here has been much improved so far with an EBIT margin of 8.8%.

Indeed, a huge cash payment might have been counterproductive for further value creation.

your “activist” chairman already steps down.

Yes. The official reason is that the current situation doesn’t allow physical presence for some time. That is plausible.

Dring the Q1 call the CEO did all he could to damper expectations about shareholder remuneration and reiterated two priorities: to reduce the pension liability (we will see some actions already in Q2) and to restore the profitability of the offset business, which – he said – will require a bit of cash. A new business plan may be prepared by the end of the year.

A dividend? This discussion will be revisited later.

The buyback? He did not want to make any comment at all.

It is possible that there is a lot of pressure from the representatives of employees or even the Government to deal with the giant pension liability and this is the priority for now.

I would be glad to hear informed opinions on this. Thanks

Well, I would say in the current environment, an aggressive share buyback and/or dividend would create a backlash.

As I laid out in the post, I hope for a little bit more than just a quick buyback/payout. Maybe some share holders have shorter time horizons and expected to make a quick buck after the AGM ?

Thanks for the writeup, interesting

A key question for me is the revenue and profit of the remaining Imaging IT solutions. I know they provide a revenue split between Imaging IT and HCIS quarterly, but the sale included some of the Imaging IT business in Europe. A lot of guesswork there.

BTW I find it astounding they won’t release that info until the Q2 results, even in response to a direct question from an analyst on the Q1 call. AO clearly have that info via their board seat and are allowed to add to their position in March, but the rest of us are stuck guessing? It’s very important to the valuation.

Yes, we do not exactly know what goes out. But I think the valuation in total is not depending on a few million EBITDA plus/minus in the imaging business.

Just had a glance over your calculations. If you like holdings with a discount to NAV, you can get that with the spanish “Corporación Financiera Alba”, where the discount currently seems to be more than 50%, or the french FFP (“Société Foncière, Financière et de Participations”, holding of the Peugeot family), where the discount is around 50% due to my crude calculation, and it seems, that there has not always been a discount that large, this also fluctuated a bit.

I don’t like that too much, because the discount will only be dissolved when they split up.

Thanks, I always like Discounts, but there should be some kind of mid-term catalyst or I would need to like the underlying asset really much.

Just a random thought:

Usually corporations use contractual trust agreements (CTA) to outsource and fund their pension liabilities.

Wouldn’t it make perfect sense for Agfa to set this up as well and buy back stock aggressively until it is priced appropriately to bring that in as “collateral”?

That way, they would be rewarding shareholders tax efficiently in short term and get rid of some of the pension liabilities on the cheap, both at the same time. This would create much more value, than simply paying down some of the pension obligations…

Not sure if this would be legally possible in Belgium, as there had been infamous examples in Germany (Arcandor if I remember correctly) where something like that didn’t worked out too well in the end…

After disposing parts of the pension liabilities, it should obviously be much easier to find a buyer for the remaining divisions or use some leverage to grow the radiology division.

Well, this would be financial engineering and might only work short term. A CTA doesn’t actually cap the economical position, it is just an accounting gimmick. I’ll prefer a more long term way of value creation 😉

The biggest uncertainty seems to be the scope of the Healthcare IT entity that has been sold. How big are the remaining parts? In that regard, no revenue or profitability numbers have been published. What do you think regarding your assumption on that matter? It is the biggest value driver in your valuation.

My assumptions are lined out in the post. Anything else is clearly uncertain but will become more clear over time.

I really like your thinking regarding the pension liability including the change of interest rate and the extra buffer. This seems like a considerate and conservative assumption to me.

The assumption regarding the Healthcare IT unit seems to be 975 (the unit sold) + 915 (the remaining parts) = 1890. This would result in lofty 30x EBITDA for the whole unit.

Being on the conservative side, my guess would be that most or even all of the Healthcare IT unit has been sold in the transaction.

My biggest fear is that the transaction could also include parts of the radiology imaging assets. Might be unlikely, but the disclosure about the scope of the transaction is not transparent, at least to me.

Nevertheless, I see upside from current levels, too. Hope that you are right!

To my knowledge, the sold Healthcare IT business only comprises ~200 mn in sales out of 500 mn. Radiology is not touched by the sale. Within Healthcare IT, the remaining part is Digital Imaging which seems to have some potential, but this clearly need to be realized. The majority of past profits with Healthcare IT come from the sold business.

As you can see at Sectra, potential valuations are indeed in the area of 30xEV/EBITDA in this area. Healthcare IT is pretty “hot” these days.

Thanks for the idea, are there any catalysts? Holding investments can be painful, look at Thyssen where some investors thought its an obvious long (elevator business worth more than total market value) which clearly has not worked out.

hmm, more catalysts that the sale of the IT business, CEO change, share buy back, CEO change in the off set division ? No, not at this time.

I still remember my good old times working in the Ministry of Photography in Mortsel (Septestraat, 27). This was the unofficial nickname of Agfa, which was crowded of ‘beamters’ (civil servants) who lacked totally of entreprenaurial spirit. This explains the performance of the company in the last 25 years. The upside potential I attribute to the (well deserved) lack of credit of the company to perform competitively.

An insider joke illustrated it: the day when Agfa had to make a few hundred employees redundant (as a consequence of photo business going digital), the COO of the company was approached by a journalist asking “how many people are working in the company?” to which the COO replied “Around 50%” (ie. the other 50% were basically doing nothing).

I wish my former colleagues all good in this transition period!

Upon

Nice joke indeed! And so true for so many companies!

Thanks for this insight. This is not an unusual behavior in once dominating companies.”Ministry of Photography” is great !!!

Now that I think of it. I should be among those profiting from the Pension Liabilities !!! x-D !!! Please don’t be harsh !!!!

sotp cases are always tricky. what is the numerical downside risk? have they announced to sell more businesses, otherwise only the buyback will support the share price.

Well, that is clearly part of the risk and the maximum numerical downside risk is always -100%.

I am not aware of a communicated disposal plan. My best guess is that they will try to get rid of the off set business. One indication could be the fact that the CEO of the offset division seems to have resigned according to today’s press release:

https://www.agfa.com/corporate/news-item/board-of-directors-annual-and-extraordinary-general-meetings-of-agfa-gevaert-nv/

A “slimmed down” radiology/imaging it company could trigger a decent revaluation of the stock. But we will see and it will take some time.

I like the answer regarding the (maximum) numerical downside risk!

Did you check if they still have these condaminated real estate from the good old film time on their balance sheet? This could be another hidden liabiity.

No, i didn’t do DD on each and every property they own. Do you have more information where that would have been ? Germany ?