Exotic securities: Gabriel Finance 2% 2016 Evonik Exchangeable (ISIN DE000A1HTR04)- Free options anyone ?

Background / Evonik

Evonik is a German specialty chemical company with a total market cap of ~12 bn EUR. The company went public in 2013, however the majority is still Government owned via RAG (“Ruhrkohle AG”), the German coal mining “run off” company.

Private Equity shop CVC bought a 25% stake in Evonik in 2008. At the end of 2013, CVC issued a 350 mn “exchangeable” bond which exchanges into EVONIK shares if certain thresholds are hit.

The “exchangeable”

Just for clarification: An “exchangeable” bond is a “convertible” bond which is NOT issued by the company of the underlying shares but by someone else. But let’s look at the bonds:

Volume: 350 mn EUR

Maturity: 26.11.2016

Coupon: 2% (semi-annual)

Denomination: 100 K EUR (so not for retail investors…)

Exchange ratio (Nominal/number of share): 2.821,8774 shares per 100 k

Strike price/break even: 35,437 EUR

Stock price “cap”: 130% (Gabriel can call the bond if the share price hits 130% of the exercise price)

So far the structure is fairly typical for a normal “convertible/exchangeable” bond:

– as long as the stock stays below the “strike” one will get back the nominal amount (plus coupons)

– if the stock rises above the strike, one can exchange the bond into the shares and realize the upside which equals a call option on Evonik

– however the upside is “capped” at around 130% of the strike which is similar to a “short call” option on top of the long call

Technically, the bond can now be evaluated by calculating the value of the long call option minus the value of the short call and add this to the “Pure” bond value, which is the nominal plus the coupons discounted back at the “risk adjusted” rate.

The NPV of the long option is around 2,6% of the bond nominal, the short call is worth around -0,5% under standard settings. So this would add almost 100 bps p.a. in option value to the bond. As the bond itself trades around 98%, together with the 2% coupon it looks like that the buyer gets a juicy 3% yield plus a free option on Evonik, so almost a “no brainer” trade in the current interest rate enironment (2 year swaps are at 0,25% p.a.).

The “exotic” feature: The “short put”

But not so fast. CVC has built in something which makes this bond “exotic”: The issuing entity, Gabriel Finance has no additional support from CVC. The issuing entity owns the shares and the shares are pledged to the bondholders, so far so good. But what happens if the stock of Evonik falls below the assumed exchange ratio ? For this case, they have allocated an additional amount of shares to the bond holders, in this case the same amount of shares as are actually the underlying of the bond.

However, even this additional amount of shares might be insufficient if the shares would fall further. We can easily calculate the share price at which the original shares and the additional shares are not sufficient anymore to cover the principal:

“break even” = 350 mn / (original shares + additional shares) = 17,70 EUR er Evonik share.

So what happens if the share price drops below 17,70 EUR ? Well, the bondholders will not get the principal back but whatever the pledged shares are worth at that point in time. (Remark: I did not find out is there is the risk of an insolvency procedure or not)

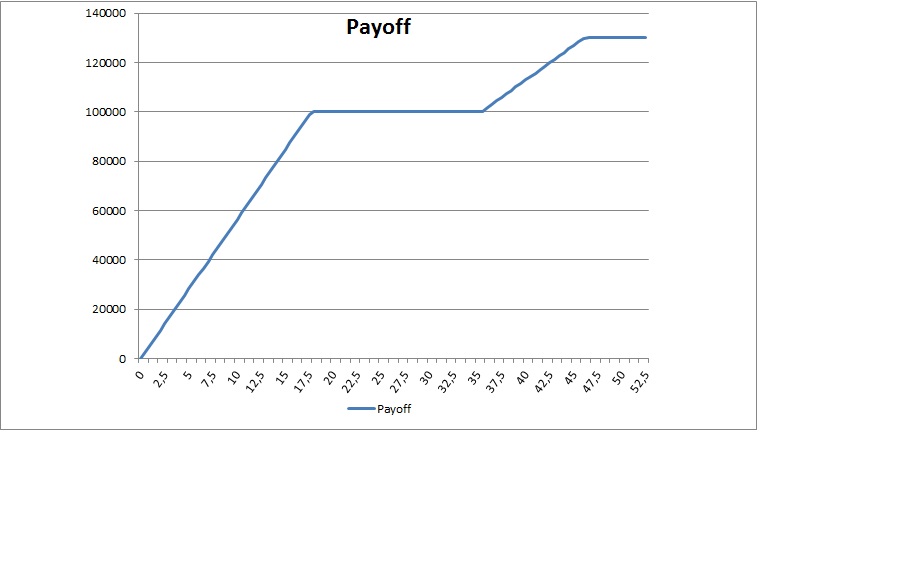

With a normal exchangeable, the issuing entity would have to make up the shortfall with any other asset they own but in this case, there is none. It is maybe easier to understand if we look at the final payout of the bond in relation to the then prevailing Evonik share price which I graphed using Excel:

In order to correctly value the whole “option package”, we will therefore need to

+ add the value of the long call

– subtract the value of the short call

– subtract the value of the put option.

Beware of the Skew

Valueing long dated stock options is a tricky thing. The major input clearly is the volatility of the underlying stock which has a major impact on the value of the option. The volatility to use depends on a couple of things, among others how far the option is out-of-the money.

In our case, the following effect is important: If you have both, a put and a call option for the same stock with the same “distance” to the current price, the put option is usually more expensive than a similar call which means you have to pay a higher volatility. Nobody knows really why this is so but it is a fact and is called the “Volatility skew”.

Finally, another “exotic feature” needs attention: The mechanics explained above mean, that in th positive case, you are long around 2821 shares per bond in th upside case. However, once you hit the downside trigger at 17,70, you are suddenly short 2×2821 shares.

So you need to buy twice as many puts at 17,70 EUR than you could sell calls on the upper end (that’s also the reason why in the Excel graph above, the slope in the downside case is much steeper than in the upside case).

Valueing the whole “package”

So in order to find out how attractive this bond is we need to calculate the “option adjusted” yield of the bond by adding/subtracting the option values to the purchase price and then calculate the yield with the 2% coupon (implied volatility for short call and short puts +6% vs. long call):

| EUR | In % of Nominal | |

|---|---|---|

| Purchase price | 98000,00 | 98,0% |

| minus long call | -2624,35 | -2,6% |

| Plus short call | 1608,47 | 1,6% |

| Plus short put (2x) | 5643,76 | 5,6% |

| “Option adjusted” Purchase price | 102627,88 | 102,6% |

Based on the adjusted purchase price of ~102,6%, this results in an annualized yield of ~0,78% p.a., which is ~0,5% above swap but hardly super attractive.

Summary:

Unfortunately, the Gabriel/Evonik exchangeable is not the nice 2% carry plus free option trade I was hoping for in the beginning. Depending on the assumptions with regard to volatility, the bond actually looks like fairly and efficiently priced. For a pure bond fund who can invest into the bond on a fully hedged basis, this still has some spread left, but if you want to achieve “stock like” returns, then the risk/return profile is not overly attractive.

Clearly my assumptions with regard to volatility are debatable and you could price the short options cheaper, but with options I prefer to make mistakes by being too conservative on the short side. On top of that, as I have mentioned a couple of times, I am not comfortable with German law for bonds and unfortunately this one is issued under German law which makes it relatively easy to change important features of the bond such as coupons and maturities.

Even if one is really bullish on Evonik, buying the underlying stock would be the better choice in my opinion, so for the time being the Gabriel/Evonik exchangeable is not interesting for me, especially as I don’t like the “Black Swan” exposure via the short put.

Thanks for the post. I was looking myself to this bond but was unable to find the prospectus. Could you indicate where you found it?

someone sent it to me…

mmi,

thank you for your detailed analysis of this security.

Also I found your recent opinion on emerging markets interesting.

Milud

A convertible that I bought already some time ago that might be interesting would be Austrian company Immofinanz (XS0592528870). One also gets a ~2% yield until 2018. While the option is not in the money currently, it was so before the ukranian trouble started (they have quite some russian assets). _If_ that is sorted out I’m hoping for at least 20% upside until 2018. If not unless it totally escalates I think at least the 2% YTM are not in danger.

#tilo,

Austrian based real estate companies go into my “too hard” pile…