Arcadis NV (ISIN NL0006237562) – One deal too many ?

Arcadis is a stock which popped up in my “BOSS score model” which I still use regularly to find ideas. It is a Dutch based Design, Consulting & Engineering company with global reach and a diversified business. Historically, they have consistently produced ROE’s of 20% and grown nicely.

Some key figures:

Market cap 1,7 bn EUR

P/B 1,7

P/E 19,5 (2014), 11,6 (2015 est)

EV/EBITDA 10,4

The company trades at a ~20% discount to Peers like AF AB, Ricardo or SWECO.

What I did like about Arcadis at “first sight”:

+ consulting is capital light business

+ potential growth areas like infrastructure, water, urbanization

+ ROIC as relevant measure for compensation

+ organic growth as target for compensation

+ well-regarded in the industry

What I didn’t like so much:

– large project exposure

– China / EM Exposure (26%)

– Utility exposure (22%)

– big M&A transactions in 2014

– annual report focuses on adjusted numbers

– debt significantly increased, far above target

Hyder Consulting acquisition in 2014

In 2014, Arcadis did several larger acquisitions, the largest one being the UK listed Engineering company Hyder Coonsulting Plc. After the first bid, a Japanese bidder emerged and at the end they had to pay around 300 mn GBP for a company that earned around 6 mn GBP in 2014. This really looked expensive and is maybe one of the reasons why EPS in the first 6 months 2015 fell from 0,77 EUR to 0,70 EUR per share.

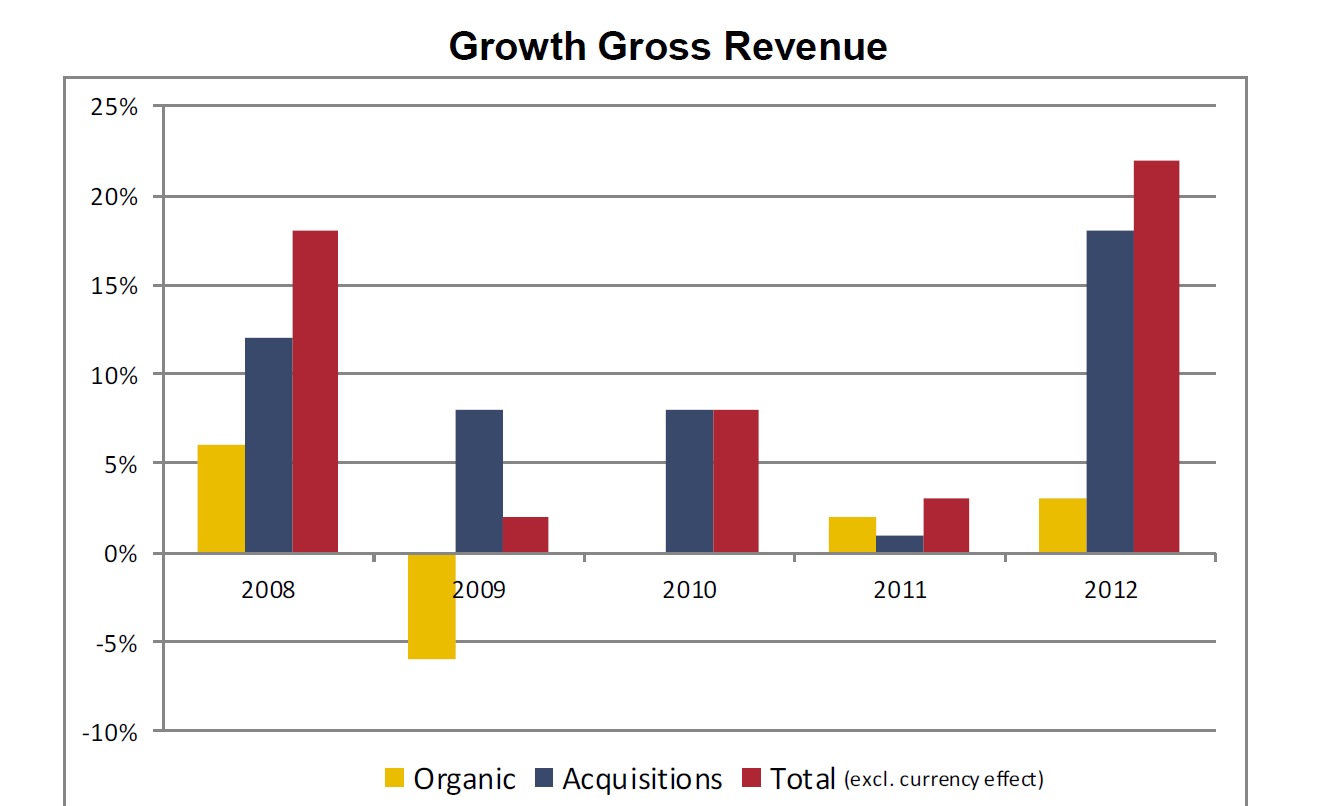

Looking into historic annual reports one can see that there was little organic growth for many years (page 15) and growth was driven by acquisitions:

Arcadis looks pretty much like your typical “roll up”, gobbling up competitors one after the other. However with the Hyder deal, it looks like that they made maybe “one deal too many”. Debt is now clearly above their own targets and business is not doing well. They acquired Hyder for their Asian presence which maybe looked like a good idea last year.

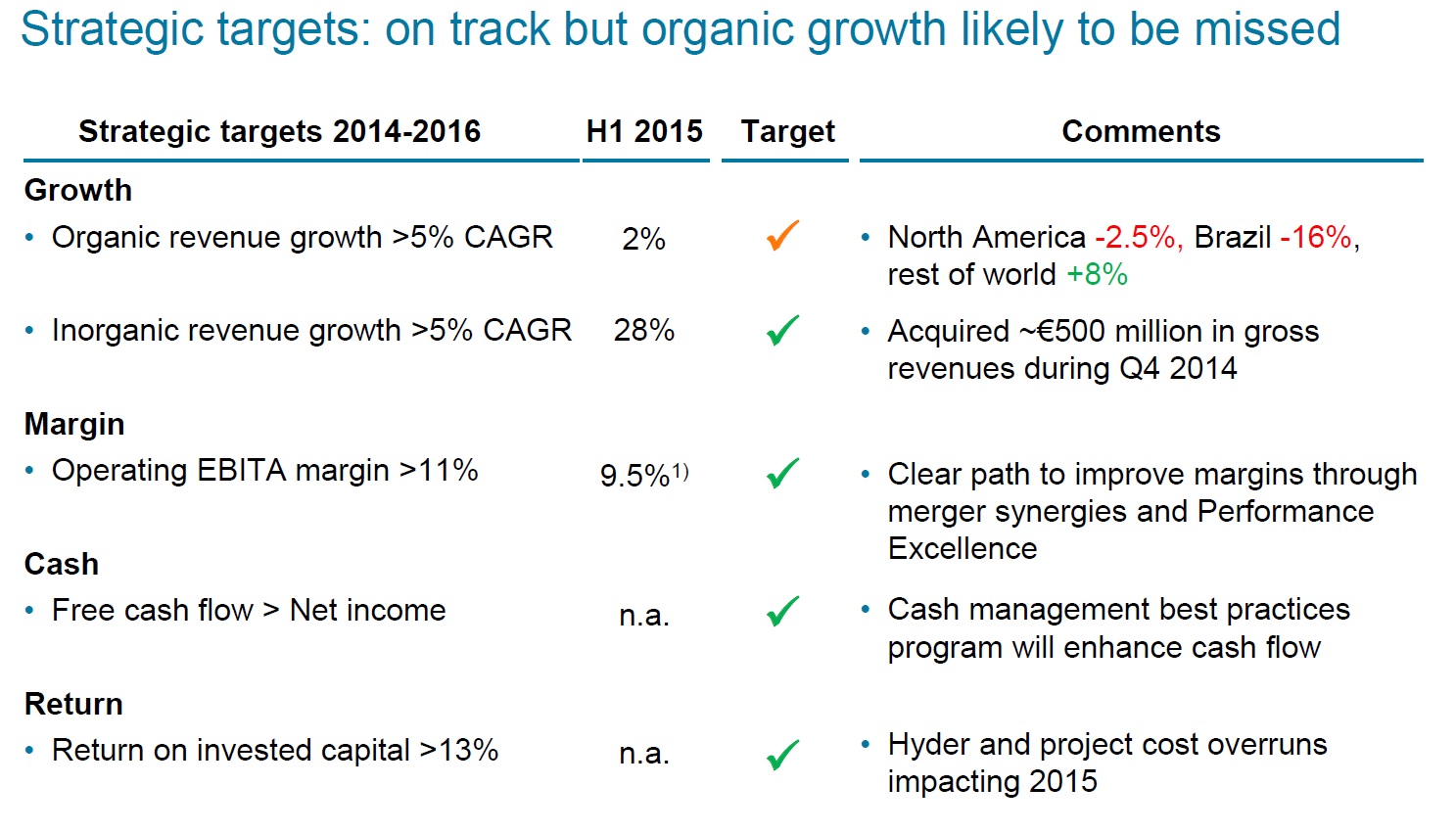

Management incentives: The reality test

When I did read the annual report 2014, I really like the fact that management seems to be incentivized on ROIC and organic growth. However, this is the score card they presented with their half-year numbers:

At first sight the source card looks, great, everything green, only organic growth “orange”. A closer look actually shows that the only target they hit was actually external growth which in itself is a pretty stupid target. All the other targets were either misses or not available.

This slide alone to me indicates that management doesn’t take its stated goals that serious. Yes, on paper it looks great but such a “target achievment assessment” is clearly a joke.

Summary:

Although the “roll up” strategy seems to have worked for some time, in my opinion there is the risk that the 2014 acquisition spree was maybe too much. If they can make the acquistions work, the stock would be relatively cheap, but combined with the current debt load the stock is now much riskier than it was in the past. Bilfinger is a good example how a seemingly working “buy and build” strategy can implode over night.

It is also a good lesson in checking if a compensation system which looks good on paper is actually implmented and followed or if management just adjusts everything to look good despite not achieving the targets.

So I will watch this from the sidelines although I like the business and industry in general.

Looks like they added another trick. Including asset sales in their net income growth estimate.

From their Q3 update, yesterday:

“Arcadis expects 2015 revenues to grow by about 30% and anticipates net income from operations to increase by approximately 20%, supported by the planned disposal of non-core energy assets.”

Management Incentives could indeed be a problem. The last time I looked in depth at Arcadis was in October 2012. At the time there were 14% options outstanding vs shares outstanding. In the year 2011 alone the number options granted were 3.5% of outstanding shares. In their financial communication they tend to focus on topline growth. But as a result of the continiously expanding number of outstanding shares the EPS growth from 2009 to 2014 was only 7% (and that is not annualized) vs. 48% revenue growth & 31% EBIT growth. Could the shareholder structure be an explanation for the bigger focus on management/employee value creation vs. shareholder value creation?

JJ,

this is definitely an issue. When management does not own a sizeable “outright” stake in the company but only gets options “on top”, then the behaviour is often not fully aligned. If you are long options, you have an incentive to increase volatility as this increases the option value. I think this has happened here.

mmi

Agree with most parts of the write-up:

– they overpaid for the acquisitions last year

– they do use adjusted numbers for non-recurring items

– Organic growth has averaged only 1% in the 2009-2015 time period

– the scorecard is a joke

Some counter points:

– Re adjustments, deal transaction costs are truly non-recurring. Some of the integration costs too. A portion of the restructuring costs are probably recurring (there is a always a problem somewhere) but you can estimate this amount and back out a true EPS

– Leverage is high but not scary high. They did an equity raise last year to finance the acquisitions. You cannot take FY14 debt vs FY14 financials because the acquisitions were not included in the P&L yet. You cannot take the H1’15 debt load vs LTM financials because its a very seasonal working capital cycle (big outflows in H1 and big inflows in H2). You need to take the average of H1 and FY. At the end of FY15, the leverage ratio will be 1.5x and under 2.0x when averaging over the year.

– What large project exposure are you referring to? They have some old environmental projects in the US which went bad. This had a single digit million impact, hardly a fiasco. The old Arcadis had average contract values of Eur 100k. They did larger projects like the Kingdom Tower in Saudi Arabia but a lot of it was small design stuff like a building entrance under larger framework agreements with multinational clients. Now I dont know how this has changed with the most recent acquisitions but certainly historically there has not been much volatility from large projects

– And because historically they had many smaller repeat projects, they were relatively well insulated during the financial crisis. 2009 organic revenue growth was -4%. Despite margin declines, EBITA decreased ‘only’ -6.1% due to acquisitions. So the earnings profile at least has been relatively stable. And they can cut variable costs significantly like they are showing in Brazil at the moment.

So what is a relatively stable ok business worth. It does compound at about 10% (3% divi + 6.4% EPS growth 09-14) even if that growth is acquisition driven. Its not exciting but at what point does it become good enough? We are probably closer now than we have been for a while. Private market value is probably higher than current price.

Disclosure: no position but watching

Hi,

thnaks for the comment. Yes, the “large Project risk” referred to Kingdom Tower and US Projects, but thank you for the clarification. The historic stability was actually the reason why I decided to look deeper into the Company. But I do think that the volatility will be higher going forward.

I agree that if they reach their Goals, the current Price might look already OK, but there is risk to that which in my opinion Needs to be compensated by a somehow lower Price.

My “Gut Feeling” would be that I would require a 15% p.a. return on Arcadis to make it worthwile.

mmi

The IRR will depend on your exit multiple. My 10% p.a. calculation (probably more like 8-10%) is based on EPS growth and dividends excluding any change in multiple.

I would argue there is limited downside to the 10x 2016 EPS / 10% 2016 FCF / 6.6x 2016 EBITDA and the business might go back to 12-14x earnings if the environment is more benign (note it has traded at above 15x recently). This re-rating could get you to 15-20% over the next 2-3 years. From that you may want to haircut the exposures you mentioned (oil related Middle East, Brazil, etc).

The stock may well have found a bottom but its not exactly exciting unless it has taken over.