Arcadis is a stock which popped up in my “BOSS score model” which I still use regularly to find ideas. It is a Dutch based Design, Consulting & Engineering company with global reach and a diversified business. Historically, they have consistently produced ROE’s of 20% and grown nicely.

Some key figures:

Market cap 1,7 bn EUR

P/B 1,7

P/E 19,5 (2014), 11,6 (2015 est)

EV/EBITDA 10,4

The company trades at a ~20% discount to Peers like AF AB, Ricardo or SWECO.

What I did like about Arcadis at “first sight”:

+ consulting is capital light business

+ potential growth areas like infrastructure, water, urbanization

+ ROIC as relevant measure for compensation

+ organic growth as target for compensation

+ well-regarded in the industry

What I didn’t like so much:

– large project exposure

– China / EM Exposure (26%)

– Utility exposure (22%)

– big M&A transactions in 2014

– annual report focuses on adjusted numbers

– debt significantly increased, far above target

Hyder Consulting acquisition in 2014

In 2014, Arcadis did several larger acquisitions, the largest one being the UK listed Engineering company Hyder Coonsulting Plc. After the first bid, a Japanese bidder emerged and at the end they had to pay around 300 mn GBP for a company that earned around 6 mn GBP in 2014. This really looked expensive and is maybe one of the reasons why EPS in the first 6 months 2015 fell from 0,77 EUR to 0,70 EUR per share.

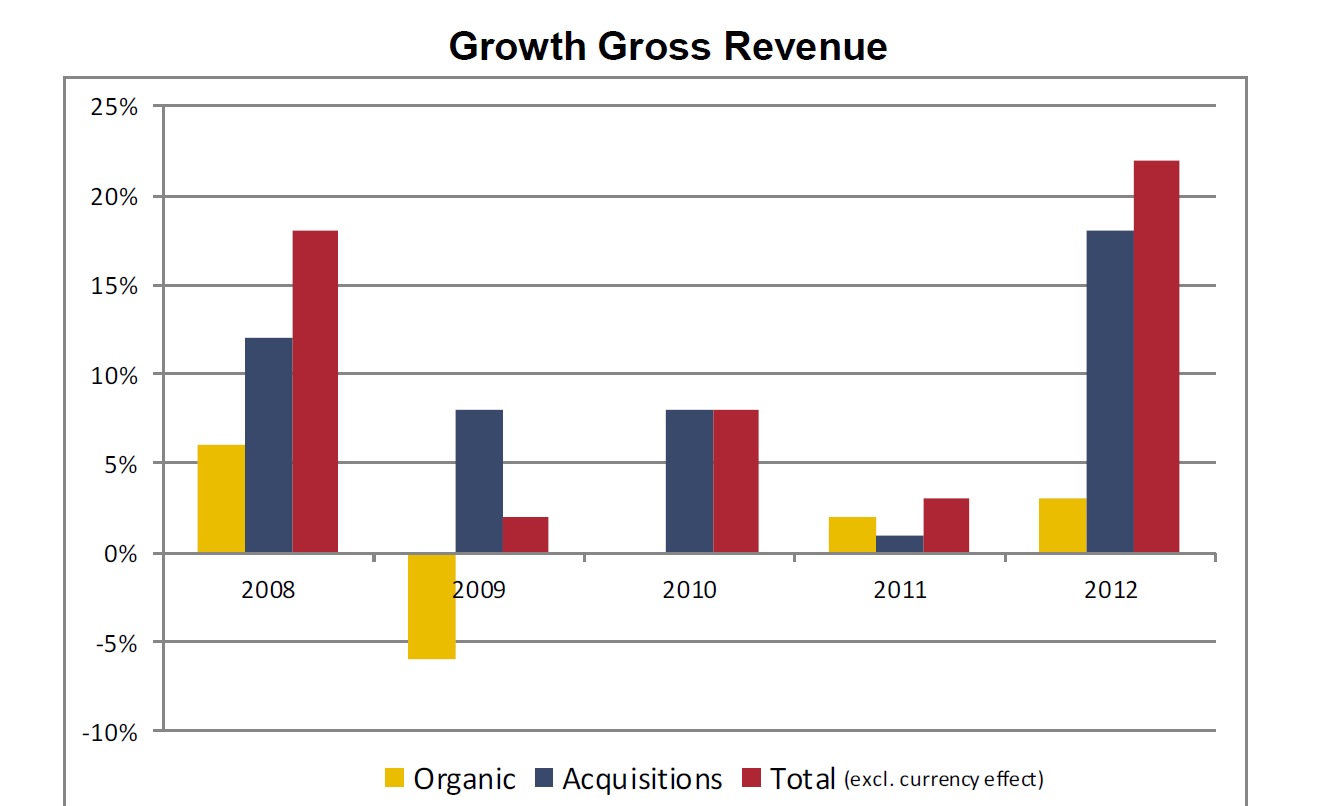

Looking into historic annual reports one can see that there was little organic growth for many years (page 15) and growth was driven by acquisitions:

Arcadis looks pretty much like your typical “roll up”, gobbling up competitors one after the other. However with the Hyder deal, it looks like that they made maybe “one deal too many”. Debt is now clearly above their own targets and business is not doing well. They acquired Hyder for their Asian presence which maybe looked like a good idea last year.

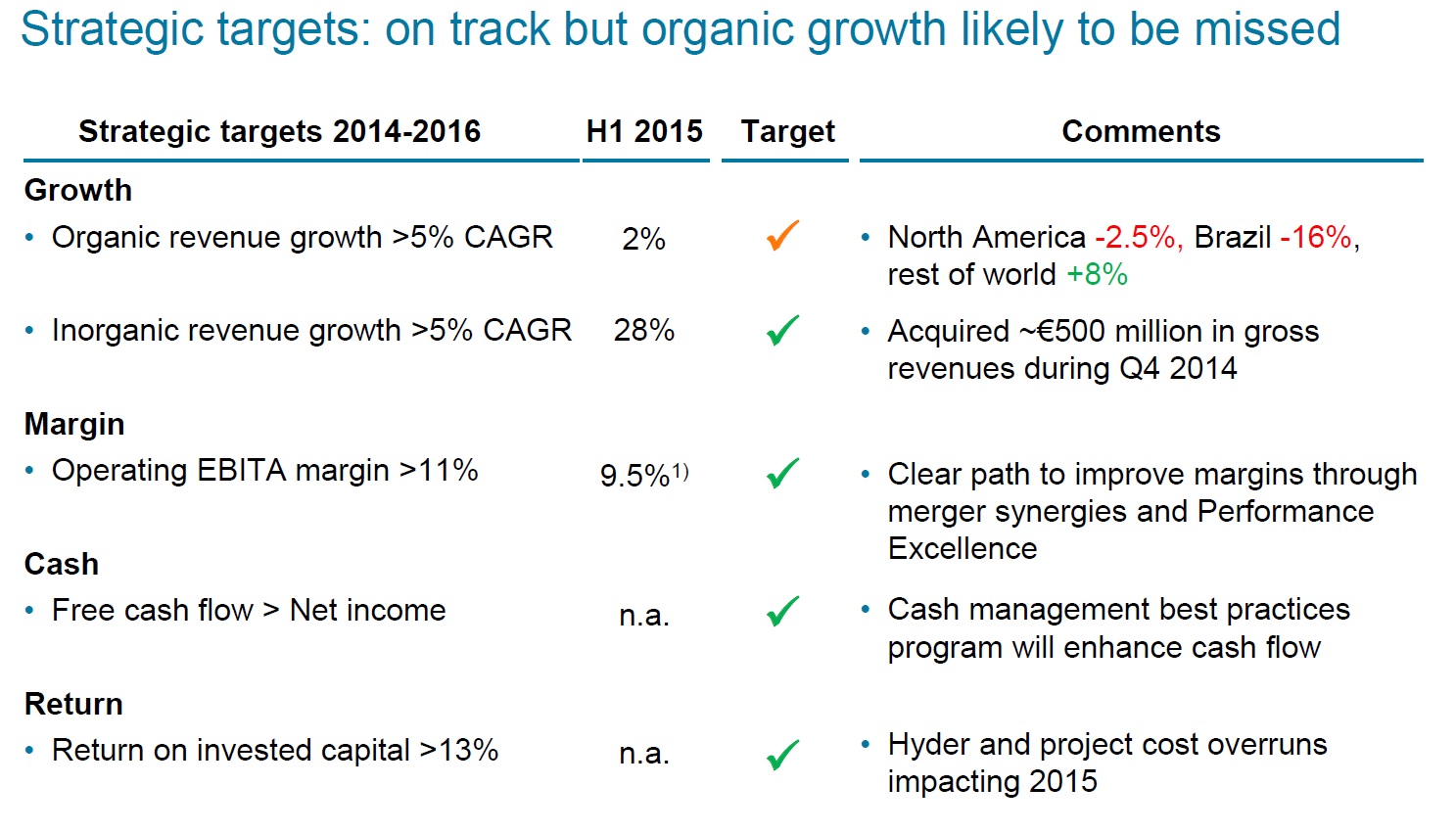

Management incentives: The reality test

When I did read the annual report 2014, I really like the fact that management seems to be incentivized on ROIC and organic growth. However, this is the score card they presented with their half-year numbers:

At first sight the source card looks, great, everything green, only organic growth “orange”. A closer look actually shows that the only target they hit was actually external growth which in itself is a pretty stupid target. All the other targets were either misses or not available.

This slide alone to me indicates that management doesn’t take its stated goals that serious. Yes, on paper it looks great but such a “target achievment assessment” is clearly a joke.

Summary:

Although the “roll up” strategy seems to have worked for some time, in my opinion there is the risk that the 2014 acquisition spree was maybe too much. If they can make the acquistions work, the stock would be relatively cheap, but combined with the current debt load the stock is now much riskier than it was in the past. Bilfinger is a good example how a seemingly working “buy and build” strategy can implode over night.

It is also a good lesson in checking if a compensation system which looks good on paper is actually implmented and followed or if management just adjusts everything to look good despite not achieving the targets.

So I will watch this from the sidelines although I like the business and industry in general.