Staffline Group Plc (ISIN GB00B040L800) -Growth machine or Brexit victim ?

Due to the well-known Brexit troubles in the UK, my contrarian instincts seem to motivate me to look more at UK companies these days. One of the UK companies on my watchlist was Staffline Plc, a recruitment and “human resources outsourcing company”.

![]()

The company got on my radar screen because friends mentioned that it looks like an interesting company and that the have a “great CEO”.

Those are the usual multiples:

Market Cap 232 mn GBP

P/E 2015: 15,6

P/E 2016: 7,4

EV/EBIT 11,7

EV/EBITDA 7,0

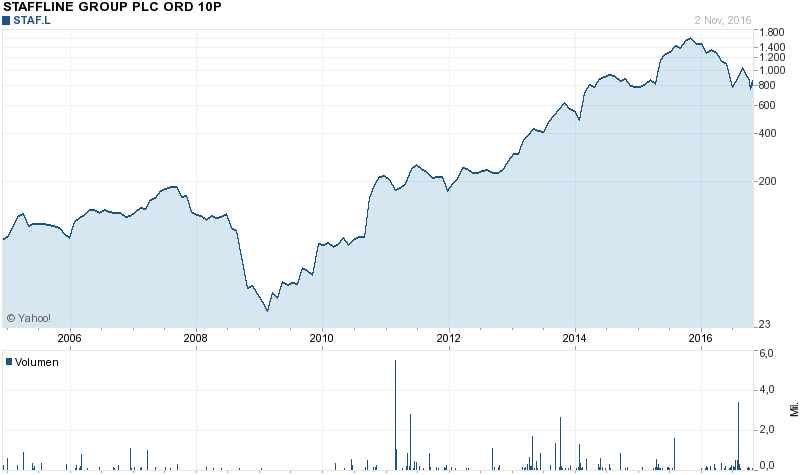

The company grew sales almost 10-fold over the last 10-12 years. Interestingly however GAAP EPS in 2015 was at the level of 2006.

The share price shows nice growth over many years but a significant draw down (.50%) from the top in November 2015 (so the drop began before Brexit):

In principle, an asset light service company at single digit P/Es could be quite interesting.

As always I start my research with reading the last annual report.

However pretty soon I discovered a couple of things I didn’t like at all such as:

– only adjusted numbers on page one (no GAAP)

– sales growth ambition (“biggest”)

– many acquisitions in 2015 (and the years before)

– “bullshit vision” statement

– concentrated customer base, little barriers to entry

– “adjusted EPS” target for bonus plans

– declining cashflow

– management stock plan with automatic cash conversion (no long-term ownership)

– not really good returns on capital

– “roll up”

On the plus side I only found those points:

+ relatively low base salary for management

+ good organic growth in 2015

+ relatively cheap based on 6M profit

+ they try to be the “trusted temp worker agency”

The CEO Andy Hogarth

Andy Hogarth seems to be an interesting person with an unusual background as this article lines out.

I also watched this video interview with him:

One thing becomes very clear: They are very focused on making acquisitions and there is very little talk about return on investment etc. but about market share and international expansion.

What I didn’t find very reassuring is the fact that since 2008 he sold around 50% of his shares. His stake dropped from 14,85% in 2008 (3.1 mn shares) to 1.6 mn (5,8%) now.

Staffline as a direct major Brexit victim:

One of the question is of course how someone who “rents out temporary employees” is affected by Brexit. In Staffline’s case I found this statement quite interesting:

The introduction of the National Living Wage (“NLW”), which will increase the minimum wage from the current £6.70 to £7.20 in April 2016, will no doubt start to encourage more people to enter the labour market. The further increases due to be introduced in the period until 2020 when it is set to be at least £9 per hour are also likely to further encourage not only current UK residents to enter work but also to further encourage people from Eastern Europe to come to the UK, supporting our growth and increasing the supply of labour. Current levels of NMW for unskilled workers vary across Europe, from £7.11 in France, £6.29 in Germany, £6.09 in Austria, £3.38 in Greece, £1.84 in Poland and £1.42 in Lithuania. Whilst this significant increase in UK wages may encourage an increase in migration from Europe it is likely to further widen the supply pool of labour, thus helping Staffline to continue to grow.

Staffline has several offices in Poland. I haven’t s seen more information within the annual report, but my guess is that part of Staffline’s past success was “importing” workers from Eastern Europe to UK.

In the 6 month report t to increase the dividend by 40hey say the following:

BrexitAt present, it is less than a month since the citizens of the UK voted to leave the EU.In that short period we have not seen a reduction in demand for our services or in availability of contractors. Whilst it is too early to tell what the long -term impact of Brexit may be, as the market-leading provider of temporary workers, our scale and capability has enabled us to manage a gradual tightening of the labour market and gives us confidence that we will continue to do so. Staffline benefits from a reliable workforce of over 263,000 available contractors on our database. Furthermore, any tightening in the labour market is also likely to help the Employability side of our business as this may make our Work Programme candidates easier to place.

So there seems to be some “natural hedge” with their social welfare business but overall I do think that lower economic activity in the UK is clearly not good for Staffline and their old core business will potentially suffer quite significantly. For me this is very different from a case like Majestic which only is exposed to secondary effects.

Other things

What really irritated me was that they announced to increase their interim dividend by 40%. I think the intention was to show (short term) confidence but in my opinion this doesn’t look like smart capital allocation.

Summary / Applying the filter

At that stage, Staffline has already been “filtered out” and I won’t analyze it deeper. There is a relatively high uncertainty about their future business prospects, they are directly impacted by the Brexit in their core business.

On top of that I don’t like roll ups as I find it very difficult to understand any year to year numbers with so many acquisitions. For me, the CEO is also too focused on sales growth. There is of course the chance that they successfully grow further, but the risk is also that they hit the brick wall at some point in time.

So time to move on to some other (UK) stocks….

Tried to get tax rebate for two friends a nightmare very dodgy dealings going on with this company avoid it like the plauge.

bloody hell, today Lavendon is up 36%, apparently it’s going to be taken over. My greedy self whispers “I should have bought some more”

wow, good pick 😉

With Brexit driving jobs elsewhere, I guess much less recruiting in UK, particularly for the City (highest margins). This may put pressure in such agencies, with substantially lower results.

May this bring an opportunity to recruiters with the largest shares of operations in continental Europe, DE/NL?

Have you looked at Harvey Nash? Seems to fulfill more of your criteria. Cheaper/less of a rollup. Seems to be underperforming in terms of margins but that could be upside at 20% FCF to mkt. cap and EV (no net debt)

The Harvey Nash I found had 17.7m borrowings and 10.9m CCE in H1 2016. So where is the ‘no net debt’? 2.6m net profit on 377.6m revenue. Their OCF in H1 is just 1.5m and FCF should be negative. The Market Cap is around 42.2m GBP. So how do you come up with 20% FCF/Market Cap? Perhaps I took a look at the wrong Harvey Nash (http://www.harveynash.com/pdf/2016-09-HN-Interim-Results.pdf) but from what I see I’m less than impressed.

Well, wc is seasonally high due to vacation allowances, so normalizing for this you het net debt of 3mln. In terms of FCF, Harley nash ‘sold’ a division for which the cash out was paid in h1. This depressed fcf by 6mln. This division bled About 3mln of cash annually. It was the cause of all the capitalized rd over the past 2 years. Im guessing they had commitments outstanding which would have continued the cash outflow. Thats likely why they paid to get rid of it. harvey nash wont win any prizes for this, but stripping this out and you get to close to 20pct fcf yield.

I have gone through all the UK recruiters and I also think that Harvey deserves a deep look and is disproportionally cheap versus its peers. Having said this, I must also say that I have found quite weird and irritating the way the management reported the disposal of the German business and also the first half report.

I see that the CFO is on his way out. Maybe some change at the management level will do good…

Good performance in the interim sector can be found at CRIT and Synergie in France and CPL resources in Ireland.

Hi Nerval,

the stock performance of Synergie since 2012 is impressive. But I don’t like their cashflows. Always lower than their net income and in H1/2016 it is negative. And when you take a look a their long term chart you can see every single crisis (1998, 2000, 2008, 2011). So for me this is a typical ‘let’s wait for the next crash’-stock. Never heard of the other two… CPL resources looks interesting at first sight.

Ennismore is long CPL resource.

ttheir short writeup

Click to access NL%20OEIC%20Aug%2016.pdf

I had a look at several ‘temporary workforce’-Companies (Manpower, Adecco, Randstad …) and they all kind of looked the same with numbers comparable to Staffline. They also almost always grow by taking over smaller competitors and their cashflows usially suck. I didn’t buy neither of them. The only company here left on my ‘to analyse’-list is Robert Half. This one might also be kind of interesting for you because David Einhorn burned his fingers by shorting it 🙂

Thank you for the nice post.

Looking at the whole sector in the UK I see prices have come down quite a bit and while the usual ones (Page and Hays) look fairly valued, other companies have rerated to historically low multiples.

This is of course a quite cyclical sector and perhaps Internet is making things harder than a decade ago.

I wonder if you or anybody else has found one or more names in this space which they find worth spending time on.

Thank you

Brunel is a name that pops up often on screens of “value” investors. Very cyclical, because of their high exposure to the oil & gas sector, but very conservatively financed. Stock performance ytd is about -20%

Roll-ups vary from value-destroying to very value-creating in my opinion. Look at Teledyne or Berkshire Hathaway. Look at Judges Scientific in the UK or Constellation Software in Canada. When acquiring selectively on low valuations, ROIC can be significant. In this case it sounds like the management isn’t cut out for value creation, though.

Berkshire is not a roll-up but an old school conglomerate. Roll-ups are usually active within one sector. And yes, some of them work. But many don’t.

True enough – that just makes their model less likely to succeed, though (at least according to conventional wisdom). Some of my favorite companies are roll-ups. Especially when you can avoid paying for any future acquisitions and the owner-operator is a proven outsider/capital allocator. Did you look into Judges Scientific at some point or do you categorically avoid roll-ups?

I try to avoid “true” roll-ups in prinicpal. An acquisition now and then is OK, but if this is the only way to grow (like at Judegs) than I am a little bit sceptical. If you time it right it could be OK.

Judges have seen 8-10 % organic growth historically, so that’s not true 🙂 Today’s price doesn’t require any more acquisitions to be a great buy. However, any 3-6x EBIT acquisition with the high qualitative hurdle Cicurel employs would create significant value.

I haven’t looked deeply into judges, but I find it hard to really see what their organic growth is.

In the intereim statement for instance they talk of great organic growth in the US although in Pound most of they growth most likely came from currency gains.

I don’t know Judegs very well, but roll ups have a lot of possibilites to fudge the numbers, even (or especially) “organic growth” numbers.

Yes, that’s why I always analyze the incentive structure – Judge’s CEO owns 15 % of the company as the largest shareholder, and looking at his way of treating the shareholders (huge honesty about problems, addresses the shareholders in the annual report “your company have..” etc.) he has no incentives or reason whatsoever to “adjust” organic numbers. That’s why I partly trust him when they state the historical organic growth have been around 10 % – but you can also roughly confirm this by using revenues of the acquisitions at the acquisition date.

My central question about Judge: As far as I understand, the production of machines and instruments is a highly cyclical branch. With brexit the european cash sources for british research institutes and universities will run dry – and it is far from secured that UK will fill the gaps.

How are the buffering abilities for judge in recession times, how ill their companies stand the heat?

UK is only about 15-20 % of Judges’ sales, so a weak UK market can be partially offset by growth in China and US, for example. A weak pound is very good for them. However, how cyclical their markets really are remains to be seen, but the cycles shouldn’t coincide too much internationally and I wouldn’t call them “highly cyclical”. In case of tough times, they have strong cash flows and a solid balance sheet so I’m not at all worried. In the long term, more measurement, education and research and development will drive their organic growth. In the short term, one could be worried that Judges’ own R&D may suffer a bit if their customers in the UK reduce their spending (as i suspect UK research/education institutions are more important than other customers for R&D-cooperations/codevelopments).

another very interesting post, thank you for sharing your thoughts and your screening criteria.

I couldn’t agree more about how little value a roll up could offer to an investor, as Capita (CPI LN) shareholders about it..

In your quest for UK value, have you considered Lavendon (LON LN) ?

No, I haven’t looked at them. Anything special there or just cheap ?

I like Lavendon and I own it for three reasons:

a) robust balance sheet with real tangible assets and reasonable leverage (rare qualities for an equipment rental business, if you compare it to Ashtead, United Rentals, HSS)

b) focused on a specialist niche (escalators and ladders), so they can attract better utilisation rate

c) today’s RNS shows business moves to the right direction