Gaztransport (GTT), Cheniere (LNG), Swatch

Gaztransport – Dodged the bullet..

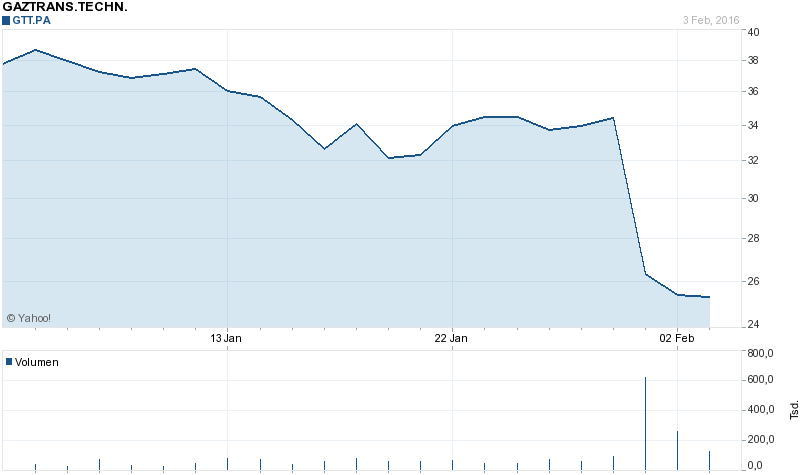

Well, that was quick. 2 weeks after I reviewed Gaztransport, they have dislosed the following:

2016-01-29Paris, 29 January 2016 – GTT (Gaztransport & Technigaz) announces that it received today a notification from the Korea Fair Trade Commission informing the company that an inquiry has been opened into its commercial practices with regard to its Korean shipyard clients.

The result: The stock price dropped ~20% in two days:

As I have mentioned, the Korean shipbuilders were in parallel trying to develop a competing technology, but so far without success. It looks now that they try another option in order to cut into the nice margins of GTT.

At that point in time, I have no clue how serious this is. In any case, this clearly increases the risk.

That’s what I wrote 2 weeks ago about how to value GTT:

Under those assumptions my results were the following:

10% discount rate: 20,80 EUR per share

15% discount rate: 14,26 EUR per share

So now one could clearly challenge my “model” and tweak it somehow, but in general it looks like that GTT is not a bargain at current prices (34 EUR). To me it rather looks like that the current valuation already implies a certain value for the LNG ship fuel “option”. Therefore GTT at current prices is not interesting to me as an investment.

I think we are now, with this “open conflict” closer to the 15% requiement, so the current price at around 24-25 EUR still does not look so attractive.

I found some research on Bloomberg from JPM. They expect that this inquiry can go on for up to 10 years and referred to a similar issue with Qualcom. More interesting were their pricing assumptions. They have a price target of 48 EUR based on these assumptions:

We value GTT using a DCF biased triangulation of DCF, PE and EV/EBITDA. Due to GTT's niche business model, it has few close peers. Hence we assign a lower weightage for the multiples based valuation (25% each) and use a peer group consisting of O&G engineering companies and LNG ship-owners. Our Dec-16 €48 price target is based on the triangulation of: (i) DCF (50% weightage) using 10.4% WACC and 3% TGR from 2020E; (ii) our 2017 earnings and 13x PER; and (iii) our 2017 EBITDA forecast and 10x EV/EBITDA. Our target multiples are at ~10% premium to GTT's peers considering its advantaged business model and above average revenue visibility.

“Triangulation” sounds fancy, but the main issue is the following: In none of the 3 approaches they actually account for the inherent cyclicality of the business. I personally think this is a big mistake and clearly results in a value which is too high at the high point of the cycle (now) and too low at the low point of the cycle (in a few years maybe….). Plus 10% WACC with the risk above looks “optimistic”.

Cheniere Energy (LNG)

I came across Goldman research for Cheniere the other day. They have a price target now of 52 USD (down from 90 USD 18 months ago). I looked at Cheniere 1 year ago and didn’t like it at 75 USD, so maybe it’s worth a look now at 29 USD ?

In typical sell side fashion, they produce a lot of smart sounding stuff including a couple of pages of numbers.

The one million Dollar quote was however the following:

Bearish investors viewed our discount rate (7.5%) and interest rate (5%)

assumptions as too low given recent midstream volatility and Cheniere’s

current debt yield of ~8%. We estimate each +/- 100bp discount rate

change impacts NPV by $2, and each +/- 100bp change to interest rates

impacts NPV by $1.50.

I found this quote absolutely hillarious. So nowadays one is called a bearish investor if one uses current, observed market rates to value a company ? It is bearish to assume that the cost of equity should be higher for an ultra-high leveraged company than its obeserved cost of debt ? Funnily enough, the current yield on the outstanding convertibles is ~11%. If we use the GS sensitivities from above, I think the current price seems like a “fair” price.

For me this is a clear sign that especially for leveraged Energy companies, there still seems to be systematic “over optimism” at play and the Energy bear market seems to have a good way to run until the “optimists” use more reasonable assumptions.

One other thought: Most of the research focuses on the “guaranteed” revenues of the 20 year contracts. I am not so sure about this. First of all, a “Guarantee” is only as good as your counterpart and the creditworthiness of the off-takers (all energy companies) is rapidly deteriorating. Secondly, I do not know if the contract counterparts of Cheniere are actually fully guaranteed subsidiaries of the big energy companies or lightly capitalized subsidiaries.

Thirdly, one would really need to look at the contracts themselves. Often those companies include some fine print which might allow countereparts to “wiggle out” of a contract if they really want to. Overall, in my opinion, assuming “Guranteed” revenues AND using a low discount rate in combination is very optimistic.

Swatch Group

Swatch Group released 2015 results yesterday. Sales in Swiss Franc were lower in 2015 than in 2014, operating earnings were down-17%, net income was down -21%.

According to them, the reduction in sales was exclusively due to the siginficant downturn in Hongkong. The results are of cours a function of the strng Swiss Franc, where they have all their costs. They also want to release some smart watches in 2016, but I am not sure if they are not too late with that effort.

In parallel they announced a 1 bn CHF share repurchase agreement. AT first, this sound like a smart capital allocation strategy.

At a second glance however, I am not so sure. In an internview, Hayek said he is doing it to “punish short sellers” who have “Manipulated his share price”. Additionally, Swacth will not commit to cancel the shares but keep them for potential “other uses”.

I think for the time being I will remain on the side lines. I would consider buying at a level of around 290 CHFs if gets to that.

One interesting comparison is Richemont. They issued a Q4 trading update a couple of days ago. Their sales at least were better than Swatch witzh a light gain. As Richemont only sells luxury watches, one can assume that the lower prce sgement of Swatch (Swatch, Tissot) indeed might have been negatively effected by msat wtaches and/or fitness trackers.

Timely exit on GTT. Well played!

That was luck in the first place. Normally I would prefer to hold my investments longer but in that case for some reason the price shot up right after I bought it.

Can’t understand why it dropped really. Will you consider a re-entry sub-20?

Barclays with soem views on Cheniere’s contracts and counterparts:

Cheniere Energy

When the going gets tough, the customers can’t get going

Stock Rating/Industry View: Overweight/Neutral

Price Target: USD 64.00

Price (04-Feb-2016): USD 27.56

Potential Upside/Downside: 132%

Tickers: LNG

How good are the contracts?

Customers can’t just cancel a contract because the terms aren’t as favorable as when they signed it. When customers initially signed on the dotted line for the contracts on Sabine Liquefaction and Corpus Christi, LNG prices were in the double digit range and the economics of Henry Hub sourced LNG was wildly “in the money”. Fast forward to today, that spread has deteriorated and while the contracts on Train 1 are still in the money, the concern is that spot LNG prices are eventually going to decline to the point that all contracts will be out of the money. We have been repeatedly asked how good these contracts are, and if we are to assume that Cheniere is holding up its end of the contract on the operating side, the only way the counterparties can legitimately get out of a contract is to go bankrupt and have the contract rejected in bankruptcy court.

Sabine Liquefaction customers: At KOGAS, Gail, and Centrica, the contracts are actually signed at the parent level (Korea Gas Corporation, GAIL (India) Limited, and Central plc). The contracts at BG, Gas Natural Fenosa and Total are signed at subsidiaries (BG Gulf Coast LNG, Gas Natural Fenosa, and Total Gas & Power N.A.), but are guaranteed by the parents/holdcos (BG Energy Holdings Ltd., Gas Natural SDG S.A., and Total S.A.). While technically the parent for BG is BG Group plc, BG Energy Holdings is a direct subsidiary of BG Group plc and the holding company for all of the Group’s trading subsidiaries.

Corpus Christi customers: Similarly, contracts with Pertamina, Endesa, Iberdrola, EDF and EDP are signed at the parent levels. Gas Natural Fenosa also has a contract at this facility with a similar setup to what it has on Sabine. The contract at Woodside Energy Trading is backed by Woodside Petroleum, LTD, the parent company.

In short, none of these contracts are signed with obscure subsidiaries that were they to go bankrupt, it would be of little impact to the parent. It’s the “top of the house” that actually has to go out of business. We would emphasize that all of these customers are either state-owned distribution, multinational utility or multinational oil and gas companies, all with investment grade credit ratings.

But still … why wouldn’t a customer try to negotiate or not honor the contract?

The negotiation question comes up as a function of two things – 1) contract renegotiations between midstream customers and producers in the U.S. that we’ve seen to date and 2) renegotiations on LNG projects abroad.

To the first point, we would say that the renegotiations are two-fold. Some midstream companies have actually renegotiated terms that are more favorable to them and these are mostly tied to contracts whereby the level of payment is linked to commodity prices. With the decline in prices, these midstream operators aren’t earning their rate of return and as a result, aren’t required to continue capital deployment (for example, well connects) until they are earning a return (hence, the “renegotiations” to get them there). While each and every contract is going to be different, they aren’t public so it’s difficult to discern what outs each side has and who has the leverage in various situations. It will also depend on what part of the value chain the operator is involved in. On the other end, midstream companies may be somewhat incentivized to renegotiate a deal if it looks like it would help the customer (such as a high yield producer) avoid bankruptcy. For Cheniere, all of the contracts are public and our view is that the customers can try to re-cut the contracts all they want (there is no word that they have tried to date), but there is little reason to from Cheniere’s perspective as there is minimal risk any of these companies are heading for bankruptcy. In the case that customers elect to not honor their contracts, all of the SPAs are “governed by and construed in accordance with the laws of the State of New York” so the matter would be brought to court in New York. We would also note that while regasification economics have not worked for years, none of the customers have reneged on the contracts and all terminals are still receiving the take or pay fees, which should lend some credence to the strength of the take or pay nature of LNG contracts in the U.S.

To the second point, from what we could tell (and we say this because the contracts aren’t public), non-U.S. LNG projects have price re-openers and language in the contracts that allow for renegotiations. It’s also not an apples to apples comparison because the contracts with the terminals abroad are for LNG, the commodity, while the contracts in the U.S. are for reservation of liquefaction capacity. There is a separate charge (115% of Henry Hub) for actually lifting the LNG and if the customer doesn’t want it, it won’t be paying for it. The customers view the terms of the U.S. LNG projects (such as destination flexibility, ability to not take the cargo, diversification from oil prices) as nice option values because it is different from their legacy contracts which have limited destination flexibility and a (fairly high) requirement to lift a certain amount of LNG. The whole point of option value is to pay for an asset or service even if there is some likelihood that the asset or service may never be used.

We think the distribution of inaccurate analyses and misinterpretations of the language in the contracts have fanned the flame of fear, making the market question everything it thought it once knew and the stock price reaction is overblown. While we are confident that the customers can’t and won’t be walking away or renegotiating the contracts with Cheniere, it’s difficult to disprove in the near term. However, we think some of this concern should dissipate once we see the facilities start up and at a minimum, customers paying the take-or-pay fee and at a maximum, seeing the counterparties lift gas from the U.S.

Interesting (and comforting), although I am afraid that, as you correctly mentioned, timing has been worst possible…

Thank you for this mmi

Hi, By anychance do you have the link of the Hayek interview? Because I can’t find any quote that you mention and I would be interested to read the full interview.

Thanks

sorry, no link. I have it from Bloomberg. They quoted an article from “Tagesanzeiger”:

Hayek will die Spekulanten abstrafen

Erstmals seit Jahren verzeichnet die Swatch-Gruppe einen Umsatzrückgang. Die Gewinnmarge ist jedoch nach wie vor hoch, der Konzern schwimmt im Geld.

Fertige Zeitmesser beim zur Swatch Group gehörenden Uhrwerk-Hersteller ETA am Standort Sion. Foto: Mario Fourmy (Laif)

Fertige Zeitmesser beim zur Swatch Group gehörenden Uhrwerk-Hersteller ETA am Standort Sion. Foto: Mario Fourmy (Laif)

Adrian Sulc

02:01

Nick Hayek sitzt in seinem Büro am Hauptsitz der Swatch-Gruppe in Biel und enerviert sich. «Gewinneinbruch» heisst es über die Jahreszahlen der Swatch-Gruppe. Tatsächlich ist der Reingewinn um über ein Fünftel zurückgegangen, der Umsatz um 3 Prozent. Hayek enerviert sich über die Bankanalysten, die schreiben, dass die Zahlen «unter den Erwartungen liegen».

«Wir haben immer noch eine Betriebsgewinnmarge von 17 Prozent!», sagt der Swatch-Konzernchef im telefonischen Gespräch mit dem TA. Und: «Die Swatch-Gruppe hat 2015 mehr Uhren verkauft als im Vorjahr!»

Dass der Umsatz und vor allem der Gewinn trotzdem gesunken sind, hat primär einen Grund: der starke Franken. Besser gesagt: der «extrem überbewertete Franken», wie Hayek sagt. Er enerviert sich wieder, über die Schweizerische Nationalbank, welche die Landeswährung den Spekulanten überlasse, anstatt der Industrie einen vernünftigen Wechselkurs zu sichern.

Starker Einbruch in Hongkong

Die Uhrenpreise in Lokalwährungen könne die Swatch-Gruppe nicht einfach erhöhen, sagt Hayek, «das ist ein Risiko, da sind wir sehr vorsichtig». Doch auch in Lokalwährungen betrachtet ging der Umsatz der 18 Swatch-Group-Marken um 0,9 Prozent zurück. Hauptgrund dafür ist Hongkong, wo die Verkäufe um 20 bis 30 Prozent eingebrochen sind – weil die einkaufsfreudigen Touristen aus China ausgeblieben sind. Die Swatch-Gruppe hat die Flaute in Hongkong dazu genutzt, das Händlernetz zu bereinigen und die Mieten der eigenen Boutiquen neu zu verhandeln. Eigene Läden hat sie aber keine geschlossen.

Aufgefangen wurde der Rückgang in Hongkong mit einem kleinen Wachstum in China und mit zweistelligen Zuwachsraten in Japan und praktisch allen europäischen Ländern. In der Schweiz hingegen ging der Umsatz zurück.

Was bedeuten die ernüchternden Jahreszahlen für die Mitarbeitenden? «Wir haben zwar weniger Gewinn gemacht, aber es sind immer noch über 1,1 Milliarden Franken. Es gibt keinen Grund, Leute zu entlassen», meint Hayek. «Wenn ein Unternehmen nur noch 1 oder 2 Prozent Gewinnmarge erzielt, fehlen Mittel für Investitionen. In diesem Fall habe ich Verständnis, wenn Abbau oder Verlagerung ins Auge gefasst werden.» Die Swatch-Gruppe hingegen investiere jährlich 500 Millionen Franken in die Produktionsanlagen in der Schweiz. Mit rund 8000 Mitarbeitern in seinen Fabriken ist der Uhrenkonzern einer der grössten industriellen Arbeitgeber der Schweiz.

Trotz den Investitionen hat die Swatch-Gruppe zu viel Geld: Die Gewinne sprudeln zuverlässig, die Eigenkapitalquote beträgt bereits eindrückliche 85 Prozent, und die Dividenden will Hayek nicht allzu hoch schrauben. Deshalb plant die Swatch-Gruppe nun ein grossangelegtes Rückkaufprogramm für eigene Aktien, wie sie gestern bekannt gegeben hat: Der Konzern will Aktien im Wert von bis zu einer Milliarde Franken zurückkaufen. Nick Hayek nennt drei Gründe für das Vorhaben:

Die Ertragslage der Swatch-Gruppe sei gut, dies gelte auch für den ersten Monat des neuen Jahres. «Wegen der Politik der SNB drohen uns Negativzinsen», sagt Hayek, «wir wissen nicht mehr, wohin mit dem Geld.»

Die Aktien der Swatch Group befinden sich im Mehrjahres-Tief. «Der Kurs ist manipuliert von Leerverkäufern», sagt Hayek, also von Anlegern, die auf einen fallenden Kurs spekulieren. Mit dem Rückkaufprogramm will Hayek diesem Preisdruck entgegenwirken. Tatsächlich ist die Swatch-Aktie gemäss einer Auswertung der «Finanz und Wirtschaft» derzeit die Schweizer Aktie mit den meisten Leerverkäufen. «So günstig kommen wir nicht mehr zu eigenen Aktien», betont der Swatch-Group-Chef.

Mit dem Rückkauf startet die Swatch-Gruppe bereits morgen Freitag. So schnell wird das Programm die Kurse allerdings nicht in die Höhe treiben. Denn für den Milliardeneinkauf gibt sich das Unternehmen Zeit bis Februar 2019. Und was passiert dann mit den Aktien? Anders als die meisten anderen Unternehmen will die Swatch-Gruppe mit ihrem Rückkaufprogramm nicht zwingend eine Kapitalherabsetzung durchführen (also die Aktien vernichten und damit den Wert der verbleibenden Titel steigern). Der Bieler Konzern behält sich vielmehr vor, die Aktien nach mindestens sechs Jahren Haltezeit als Zahlungsmittel bei Firmenübernahmen zu verwenden oder sie gar wieder an der Börse zu verkaufen.

Mit dem Vorhaben hat Hayek die Börse gestern überrascht und den einen oder anderen Investor verwirrt. So fiel der Kurs am Morgen um bis zu 4 Prozent ins Minus, kehrte nach der nachmittäglichen Telefonkonferenz Hayeks mit den Analysten kurz ins Plus und sackte danach auf minus 1,4 Prozent ab.

(Tagesanzeiger.ch/Newsnet)

Smart watches more popular than Swiss watches 😦

http://nypost.com/2016/02/19/smart-watches-more-popular-than-swiss-watches/

On Cheniere, you should read Chanos’s presentation, he has been very critic for a long time:

Click to access James%20Chanos%20Grant’s%20Fall%202015.pdf

There is also an interesting slide on guaranteed revenues:

“Are LNG Contracts Indestructible?”

“Petronet breaks contract with Qatar: It is cheaper purchase spot cargoes and pay $1.4B upfront fee than pay for the agreed-upon volume and price. Contract was in year 11 out of 25: Only willing to take 70% of agreed-upon volumes, when the minimum was 90%”

Matteo,

thanks for the link. Great stuff !!!

mmi

Cheniere:

Thank you for bringing this into discussion. My apologies as usual for the “book”.

This is one extraordinary complex project to value (operational risk, complex financial structure, changing dynamics in the energy landscape coupled with with tier1 revenues energy/utilities giants). I will use part of my conversation with mmi in order to present my views.

Just by looking at the explosive “cocktail” I do agree with mmi that one should be cautious because of the too many variables involved. Just only because of that a prudent approach should be used when it comes to the cost of debt. But let me play the devil advocate when regarding the quality of the revenues because I think you are referring to two sides of the same coin. Let me explain.

In my view, to have currently an 8% cost on the debt is simply a result of two factors:

a) A misperception on the soundness of Cheniere’s contracts.

b) A misperception of the relation between Cheniere revenues and the price of oil

Let’s analyze the first point:

a) Misperception of Cheniere’s contracts and its cost of debt:

To have an 8% cost on debt means nothing per se. Let me explain again. Usually an increase in the cost of debt precedes a lower equity valuation. That’s true (and logic) among other things because the fixed income universe is much reduced (in terms of investors) so the percentage of professionals taking decisions and following assets is relatively much higher/concentrated than overall equity universe. Ok. But does it mean that fixed income investors are right on this case? Let me put a question mark here.

In order to avoid a circular reference (is the debt currently yielding 8% because the contracts are not rock solid or is the equity so depressed because the debt currently yields 8%?) the question on the soundness of Cheniere’s contracts must be answered crystal clear and without any kind of doubt, otherwise the entire investment case and business model is worth zero.

If the contracts prove to be rock solid, one should not take current debt yields as reference when projecting 20 year cash-flows because they are just a mere opinion at one point in time (as the equity) and sooner or later they should have to reflect the creditworthiness of EdF, BG, Total, Iberdrola, Endesa, Centrica, etc. Example: Sabine Pass Liquefaction 6.25% 03/15/2022 currently yields 8.204 but just 1 month ago was at 6.806; and what is more important the bond traded above par until Nov ’15 (mmi correctly appointed that all defaulted bonds have traded above par at any point in time. I do plainly agree again).

I have read one of the SPA (Centrica) and the Iberdrola press release:

http://www.sec.gov/Archives/edgar/data/1383650/000138365013000038/exhibit101centricaspa.htm#sD0D7251BEF06DB89468C8E1F817A4F7F

http://www.sec.gov/Archives/edgar/data/3570/000000357014000114/cei2014form8kiberdrolaspa.htm

In my opinion these contracts are carved out in stone. There is no doubt that parents are taking responsibility for the deals. Cheniere approached these companies and offered them to supply LNG if and only if they would support fixed payments to finance the construction of the LNG export terminal. That’s simple.

To me those are strong binding commitments (do not pay attention to the fact that they are not signed. It is usual and common to file draft versions as long as they are identical to the original –something that could be easily checked in front of a judge).

So in my opinion, there is a market misperception based on the quality of the contracts.

Somebody could argue that there have been precedents regarding the breach of LNG contracts. That’s is correct (Petronet with Qatar) but please do not forget the context!:

http://www.qatarday.com/news/local/petronet-lng-breaks-qatar-contract-to-gain-from/25795

Petronet was paying under a semi-rigid fixed price structure 12.5$/mmBTU! Additionally, Cheniere business model is based on a pass-thru (forget about fixed prices) and that pass-thru would be based on the most liquid gas reference (worldwide): HenryHub.

Last but not least –and this is critical- as you will see on point b.2 the European counterparts would not want to walk away from the deal!

b) Misperception of the relation between the oil price and Cheneire revenues

As of late, Cheniere has been performing poorly, in line with the oil decline (even more abruptly because of point A).

And that makes all the sense. Mr. Market is correctly reading an oil linked-transaction. You have to bear in mind that correlation between Henry Hub and oil has been historically very high 0.8.

Two points/facts to object here:

b.1) 81% of the revenues are fixed no matter how the Henry Hub or the WTI price evolves. Those 81% revenues correspond to the fixed fee coming from their tier 1 customers and are partly inflation-adjusted. On top, those 81% revenues correspond on average to 2.5-3$/mmBTU which means that is a relatively small part of what an industrial customer currently pays for its gas in Europe (remember Petronet, although is fair to say that European industrial customers do not pay 12-13 $ mm/BTU either).

b.2) Mr. Market does not understand the nature of these agreements. This is not a case of spread arbitrage between the US and the Asian gas as I have read. This is about securing the natural gas at reasonable cost and by the time that those contracts were signed, this LNG was the most affordable source. And still makes all the sense when looking at the big picture for a 20 year timeframe!.

Think about this. Prior to this contract the sources of gas supply in Western Europe were basically a pipeline from Argelia (to Spain and France) and –of course- Russia (to Germany and Central Europe) and other LNG cargoes from Qatar, Egypt, Saudi Arabia and Trinidad&Tobago (to mostly UK, Italy and Northern Europe). Think about the implicit risk from those countries…Nevertheless those contracts are to stay (among other things because there are take or pay clauses) but the new demand additions are going to be partially satisfied thru Cheniere (US). This is not questionable to me.

European utilities are more than happy to –economically- secure that supply for the coming 20 years with prices linked to the Henry Hub (a much more liquid reference that NPB) while significantly reducing the geopolitical risk. This is killing the entire bear case for Cheniere. All the market thinks that the contract would be breached because the economic terms (gas from Asia) have changed. Wrong in my view. They should apply a 20 year timeframe logic to issue that assessment!.

On top, an important clue, “old” pipeline contracts are oil-linked (up to 70% of the price component).

So in my view, this contract is a win-win for both parties (Cheniere and its customers): it makes all the sense on its economics terms (per se) and fulfills an strategic goal of geopolitical diversification.

Once that we have clear points A and B, it is relatively easy to check on valuation. But, honestly I do prefer not to enter into that question in order not to distort the discussion (and among other things because somebody could use it as a reference and as mmi always correctly remind us you have to do your own homework in order to reach your own conclusions/decisions!)

As always, a pleasure to share my views with you, and thank you mmi for enabling the discussion.

Take care,

Dave.

Thank you for Chano’s info.

Nevertheless the context of the Petronet deal is extremely far away from the Chenille’s business model

Let me add some criticism to Mr. Chanos presentation:

– Slide 13: he is using a monthly (1 year) reference evolution to build a long term case of depressed pricing for LNG in the context of a 20 long-term asset discussion. It would be nice to put into perspective -at least- 10 years the gas prices.

– Slide 14: he is acknowledging the fact that the “old” gas business model with fixed price reference linked to oil –remember prices around 12-14 $/mm BTU) is struggling under the new reality (that’s correct but that is not Cheniere’s case). The problem for “old” contracts is the need to adapt to substantial lower spot Price (bad for them) but more importantly the need to be more flexible in terms of quantity/deliveries (Cheniere flexible business model does not rely on prices (pass-thru) nor quantities (it is not based on take-or-pay clauses) either.

– Slide 20: strongly disagree with the numbers. According to my own calculation Cheniere would get min. $2.6M EBITDA by 2021 only considering the fixed fees from 7 trains (you can check the contracts: there are $4.3 bn revenues coming from EdF, Iberdrola, Endesa, Centrica, etc. and approx. $1.7 bn in operational cost -excluding financials-).

– Slide 20: not only that Mr. Chano’s is missing $1 bn EBITDA from the fees but also estimates that Cheniere (having access to one of the cheapest gas sources) will not be able to generate sales for the remaining 15% capacity factor beyond 2021 (no comment).

– Slide 20: I am 100% on the rest of the “qualitative” coments: complex structure, operational risk, etc, etc. That is what is Cheniere.

Don’t get me wrong. I am not saying that Cheniere is a clear investment case: it is full of risk, no doubt. But let’s make a fair criticism, not by trying to present bear arguments from thin air.

You are placing an aweful lot of weight on that cyclicality in GTT, you even call it ‘ultracyclicality’. And yet you can only base it on one down move after recessionary years in western countries (2009/2010).

On top of that, LNG production and especially transport didn’t really kick off until the early 2000’s, one could argue that it hasn’t really started until 2005/2006 (see ‘IGU World LNG Report’).

What I’m trying to say is, that I think placing almost 100% of one’s analysis on three years of declining revenues (and two of declining net margin) is a bit short sighted. Especially since you see many moats and like the business model.

My 2 cents only though after looking into GTT following your initial post (and liking the company 🙂 )

FK,

I am not sure if my approach is “short sighted”. So far it saved me from a -30% price drop, but that could have been pure luck. I would call my apporach rather cautious, maybe over-cautious. In my experience, when dealing with cyclical industries, it pays to be over cautious in the long run. If you are over cautious but the valuation still looks attractive, then you can be pretty sure to get a good deal.

So what are Icahn and Klarman doing in Cheniere then?

Why is Klarman doing Forward Pharma?

0 logic. I am short and will stay short.

That’s a question I asked myself a year ago. I guess the made a mistake…

Since they are buying more and more I don`t think they consider it a mistake already.

I know we had this discussion already, but why is it hilarious to think that maybe the bond market is inefficient here? I personally do not know enough about LNG to make such a statement, but I wouldn`t go that far to say that it is clearly wrong not to use current yields from the bond market.

And if someone implies that the contracted revenues are safe, then it would be inconsequent to use higher discount rates imho, if he wants to know the fair value of the company given that his assumption is correct.

Well, the bond market could be wrong of course. But you can only tell afterwards. In my experience, bond markets are not perfect indicators but they are often more rational than stock markets. Why ? Because in the bond market your upside is limited, so you have to control the downside.

Not using current yields as a basis is already a directional bet that bond markets are wrong. You can do that, but it is risky. For me current yields should always be the starting point. If the stock is still cheap on that basis, you have much better chances that you get a good deal. If a stock only looks cheap by assuming a lot lower yield then this is already a pretty aggressive assumption. And aggressive assumptions and “margin of Safety” do not go together well.

I honestly never looked deeper into the complicated structure of Cheniere (which entities owns what) but it looks like that they have to refinance a significant amount of loans this year:

http://www.hydrocarbons-technology.com/news/newscheniere-energy-seeks-28bn-to-refinance-sabine-pass-facility-and-pipeline-in-us-4794143

I am pretty sure that this is not big fun for them and they won’t get it for 5%. Bad timing.

Of course you can only tell afterwards. But that holds true for the stock market as well. And why should bond investors be better assessors of the financial stability of this particular company than stock investors? They are both human beings reasoning about the future. By the way I am pretty sure that especially Klarman thinks a lot about risk in a way like a bond investor does it.

And as I have mentioned in a previous discussion: I am no big fan of using current yields as a starting point. It may sound stupid to you as a pro but I would consider myself biased. It is always just an opinion. It would be the same if Buffett would start his valuation of a company for Berkshire by looking at its stock price and considering it to be fair. So I think you should certainly look at the current bond yields, but not as a starting point.

It’s funny that you mention Buffett. In those instances where one actually could see how much return he requires (whenever there is a coupon involved), he always charged based on then prevailing market rates.

You can look at ALL his financial crisis deals (Goldman, HArley Dividson, Swiss Re) and compare the terms he charged with the secondary market prices of the equivalent securities of the same issuers. You will quickly realize that his deals always were (including his warrants) more expensive than market prices. Buffett is in my opinion very aware of market prices and takes advantage of them, but he never accepts less than market prices.

So again, starting with assuming different yields than current ones is in my opinion a big mistake, but on the other hand this is a “free market” and anyone can assume whatever she/he wants.

Why should he take less than the market offers if he can point to that in the negotiations? That just proves that he uses everything he can to earn the maximum. But in my opinion it doesn`t provide any insights on how he values companies.

To be more precise: If I was a distressed company and you were Warren Buffett, and if you think that 10 percent was the reasonable risk-adjusted cost for privately negotiated debt, but for some reason you think that you can charge me 15 percent (for example because of a wide-spread financial crisis and uncertainty in the market), you would charge me 15 percent. Not because you think the risk dictates the higher premium, but because you want to get as much as possible. That`s how Buffett`s privately negotiated deals should be viewed in my opinion.

Well, it is always kind of difficult to second guess what Buffett is thinking.

Let me try one more time to explain my poin of view:

If an investment (like Cheniere) looks attractive by using actual yields, then it might be a good deal with a rather large probability. In my opinion, it does not.

If an investment doesn’t looks very attractive at current market conditions, but maybe under more “normal” conditions, then in my opinion there is a lower probability that it turns out to be a good deal because maybe the current price is more adequate then the previous one (remember: there is also the Anchoring bias).

In my philosophy, I can never be sure about the success of a single investment. But I can try to maximise my returns by minimising the probabilities of a big loss. That’s why I would always use current market conditions as a starting point, especially when they are stressed conditions. Yes, I might miss some interesting opportunities,b ut as the now 5 year history of the blog shows, I avoided a lot of potential losers.

In summery, if your strategy is to avoid losers, then using current conditions, especially if they are stressed an absolute MUST.

If you are looking for winners and have the ability to pick them with good accuracy, then using “Normalized” assumptions works as well.

I think I understood your point of view already in the first place. Nobody doubts that your strategy works well, the track record speaks out for itself.

But obviously I haven`t done such a good job myself to state my point of view as clearly as I wanted to. So I would like to try it once again: I just don`t understand your logic here. In nearly every other aspect of your investing process you try to avoid biases and to think independently. But in starting with current yields you begin the process with letting the market tell you what he thinks about the company, especially if it is in distress or not. In my opinion it is very difficult to judge this particular question independently by yourself afterwards. I would see the 8 or 10 percent yield and think “Wow, they MUST have some big problems”. My ability to think independently would be gone then. But maybe you can handle this in a better way.

“If an investment doesn’t looks very attractive at current market conditions, but maybe under more “normal” conditions, then in my opinion there is a lower probability that it turns out to be a good deal because maybe the current price is more adequate then the previous one (remember: there is also the Anchoring bias).”

I think there is ALWAYS a higher probability that the current market price is more adequate than the previous one.

I would see the 8 or 10 percent yield and think “Wow, they MUST have some big problems”. My ability to think independently would be gone then. But maybe you can handle this in a better way.

Well that is actually the cornerstone of my investment philosophy. Especially in an environment like now, if somthing looks to good to be true, it is not true. There is a famous quote also used by Buffett which summarizes this very well

As you know, I do look at such situation and try to find out where the problem is. There are 4 potential outcomes:

1) I don’t find the problem. Then I assume I am the sucker and stay away. AerCap for me was such a case in principle.

2) If I find the problem, but I am not comfortable with taking the risk. Then I stay away. This is the case with Cheniere. I don’t want to bet on a succesfull refinancing in such a market and/or under water off-take agreements

3) I am in principle comfortable with the risk, but the price is not right. This is the current status with GTT. AT the right price I will take the risk

4) I like the risk and the price is right.This was the case for instance with PIIGS companiesin 2011/2012

I hope this ecplains it better. I agree that there might be a “sceptical” bias involved but I find that one quite helpful.

” “If you sit in on a poker game, and you don’t see a sucker at the table,” said Saul, “get up. You’re the sucker.”

As you know, I do look at such situation and try to find out where the problem is. There are 4 potential outcomes:

1) I don’t find the problem. Then I assume I am the sucker and stay away. AerCap for me was such a case in principle.

2) If I find the problem, but I am not comfortable with taking the risk. Then I stay away. This is the case with Cheniere. I don’t want to bet on a succesfull refinancing in such a market and/or under water off-take agreements

3) I am in principle comfortable with the risk, but the price is not right. This is the current status with GTT. AT the right price I will take the risk

4) I like the risk and the price is right.This was the case for instance with PIIGS companiesin 2011/2012″

Great summary for critical share analyses!

I totally agree after reading, but I have to admit that quite often I fell in the trap for rule 1

Would be worth a new blog entry!

I’ll think about it….

Don’t be offended by my comment Daniel, but I invite to read MMI’s post on lessons learned from the Globo fiasco.

I`ve read it already, but I can`t figure out what the story there has to do with our discussion ^^

Swatch – I still don’t get it MMI: why do you want to catch a falling knife?

(Contrarian-ism is surely not the answer to the question above :))

To give my last comment a positive spin: there are surely other Swiss opportunities with a better outcome prospect.

Take Syngenta for example – I bought it at 395 yesterday (post announcement) implying a 24.3% return on closing (expect end-2016, return calc inclusive of 2 special div of 11 and 5 CHF)

Downside is probably a 35% from here but the odds are massively in favour of the upside.

Tony

M&A arbitrage is something different, let’s see if the Syngenta deal closes. Swatch in my opinion is a very decent business for the long run.