Special situation quick check: Syngenta & ChemChina

Syngenta ChemChina offer

After the failed attempt of Monsanto to buy Syngenta last year, Chinese conglomerate ChemChina made an offer for Syngenta a couply of weeks ago. Other than with Monsanto, the Syngenta board already approved the take over.

The offer itself is as follows:

ChemChina will pay 465 USD. On top of that, anyone who buys Syngenta shares now, will receive the normal dividende of 11 CHF and a 5 CHF special dividend.

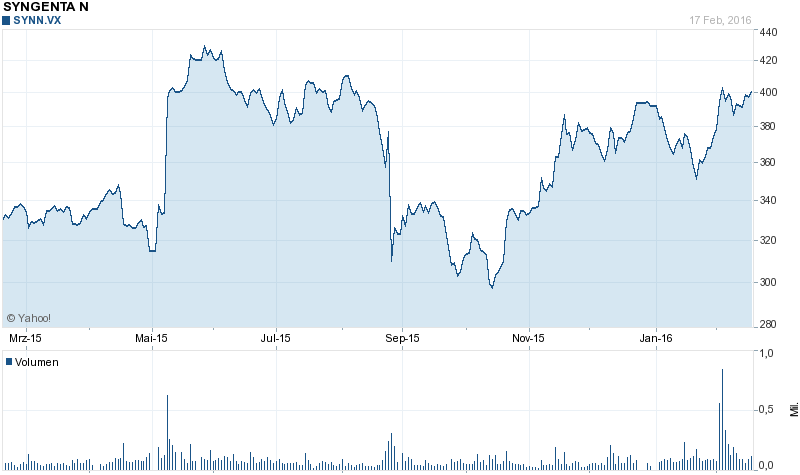

If we expect closing at the end of the year, the potential return would be (in CHF) at a current price of 400 CHF:

-400+(465*0,994)+11+5= +77,75 CHF or a potential 19,4% return for 10 months.

This looks very attractive. However the merger arbitrage/event market is a very competitive one and those spread usually don’t come “for free”. So why is there such a large spread ?

US regulatory risk

I guess the most obvious reason is that investors fear that US regulators will try to kill the deal. Syngenta has a signifcant US business. There are several rumors around why the US authorities might challenge the deal, most recently some in connection with the Zika Virus.

The Committee on Foreign Investment in the US (CFIUS) will review the deal because Syngenta, through its US research and production facilities, plays a key role in the US food industry.

The Zika virus problem could force CFIUS’s hand, sources said.

“CFIUS focuses solely on whether an acquisition represents a national security risk,” a Beltway CFIUS expert not involved in the merger told The Post. “I certainly think Zika will be a factor.”

From what I found on the net, the problem is that the CFIUS never really explains their actions, so it is very difficult to judge as an “amateur” what the chances will be. A professional hedge fund clearly has the money to pay for advice, most likely from former members of the CFIUS. This is clearly an information disadvantage form me as small investor.

China FX issues

Another problem I could see is the fact that ChemChina needs to come up with around 44 bn USD in USD financing and this could be difficult if there would be really turmoil in China in the meantime.

They haven’t even refinanced their Pirelli bridge loan yet and at least in the Pirelli case they don’t seem to guarantee those loans:

The new refinancing will be non-recourse to ChemChina, but will have elements of support from Pirelli’s Chinese owner, bankers said.

So I guess the ~20% discount is basically a mixture of regulatory risk and financing/China turmoil risk.

On the plus side, even if the ChemChina deals would fall through, there still could be other players interested such as German chemical Giant BASF.

Is Syngenta then an interesting special situation investment ?

What is bothering me is the following: As I said before, this area is very competitive and Syngenta is a liquid stock (50-100 mn CHF a day) and I do not have any special insights into the situation.As discussed before, I guess I have even an information disadvantage.

The potential downside for a failed bid is at least -25% when we look at what happened after the Monsanto bid:

So if I assume a simple 50/50 probability, my expected value is negative.

Every “event driven” fund is clearly looking at Syngenta which in turn means that they seem to price the risk at the current price and assume a slightly better chance than 50%.

However I clearly have no basis to assume any higher percentage for a succesful outcome.

All in all, in the past it never had paid out to invest into such a situation with an information disadvantage, so I will stay away from this one.

Now offering the same YTM as Kuka!

Nice jump. Comgratulations if you were invested.

Ha 🙂 Never mind the comments trail below…

I think I will hold this one to “maturity”….

EU protectionism at unprecedented levels!

mmi ever think about this one now. time has come closer. annualised yield much higher and imo 95/5 probability of completing early next year

Depends also how the uS election works out. When Trump wins, then it will be much more difficult to close this (in my opinion).

Yacks!

Downside of 25% on Syngenta is an unlikely scenario (one that might be deserving of a cheap significantly-OTM put to capture that tail), particularly as Monsanto, a larger target, is also in play from a willing cash bidder at >20x EV/EBIT, which is roughly equivalent to the Syngenta bid (if this annoying wrinkle wasn’t present, this might be a straightforward arb to straddle by capturing directionless volatility).

Without the imprecision of placing a value of Syngenta, we’re left with the observation that Syngenta & Monsanta generally trade at a premium multiple (currently 15x – 22x normal earning power) to peers and Syngenta specifically has traded at a premium price path since the recession. Peers such as Monsanto and Agrium are down 7-10% since just prior to Monsanto’s initial bid announcement (May 2015), thus, without giving any benefit to the premium relationship, that should imply a $65 downside. Of course, we could comp it to other fertilizer cos such as Yara, K+S and Potash, but that would strike me as a touch disingenuous since those guys are primarily in the fertilizer/potash business, not the crop nutrition engineering in a general sense. One can see the divergence in both sub-groups’ price paths during down markets. Nevertheless, it’s worth noting that the latter have fallen 25%-45% in the same period. So lets give this tail benefit of the doubt and call Syngenta’s downside range $60 – $65.

At $75 immediately following Brexit, wall street was therefore pricing in a 60-70% probability that the Syngenta/ChemChina deal doesn’t go through. At current prices, it’s down to 50-60%, so price paid tilts the risk-reward paradigm significantly.

Laut der NZZ hat Chem China bei einem Veto der US Behörden sich die Möglichkeit vertraglich festgeschrieben, ohne Strafzahlung aus dem Angebot an Syngenta aussteigen zu können.

Interesting case. On financing, a deal that size and that strategic by a state company is probably gov policy, and the Chinese gov has about 3.5 trillions of USD to spend so shouldn’t be a problem.

You know I am invested in this one – increased my stake holding to 4.6% of total allocation on the latest pull back as well.

“(465*0,994)+11+5” – what is the 0.994 adjustment factor?

50:50 odds? We certainly disagree on this front.

I appreciate that your forte is fundamental research. Event-driven is a different set of skills and you are right to stay away from strategy you have less comfort on-boarding

From my end, this is the strongest announced M&A deal in my view currently in the market (save Home Retail Group giving 8.5% total return at today’s prices) and am happy to allocate 10% of my funds in event-driven long only strategy (no arb, not good at it)

Tony

The “adjustment factor” is yesterdays USD/CHF exchange rate.

And yes, “event-driven” is all about disagreeing on the odds of the event happening.

So what is your explanation why the spread is so wide ? Are all other market particpants stupid ?

MMI I respect your work and am not calling anyone stupid or ill informed.

It just happens that we see odds differently. I have been investing in M&A arb since 2010 and have so far had a 71% success rate.

On the other hand, I approach all investment on a relative agnostic basis…. which in a wired way empower me to compare the incomparable (swatch v.s. syngenta for example).

The USD rebasing is subjective. For a GBP investor, Fx worked in their favour making this element irreverent. You can model hedging here, but then have to be fair and do the same for the turkish lira bond.

The outcome on this situation is binary as you know BUT I did quite well historically trading the spread: For example, I bought here at a 25% total return and will be selling down at a tighter contraction. I don’t always hold to crystallise the binary event.

Again – no one is stupid here. It just happens that I have a good grasp of the above.

(and what happened to the contrarian in you any ways? :))

well, the contrarian in me says that the spread is too wide. As you might know, I do “special situations” since I started the blog (AIRE, WestLB, Depfa LT2, Celesio, Rhoen just to name a few) and privately over 15 years now. My “success rate” has been always high when I had a special insight and low when I had none. And here I have no special insight.

One has to walk the extra mile to match your Tonellerie Frere performance 🙂

I am still wondering why you are using the USD as a base currency by the way? I got the feeling from your portfolio and this blog that you are a German based in Germany!

I don’t use USD as a base currency. I only adjusted for the fact that The ChemChina Offer is explicitly in USD, whereas the current share price and dividends are in Swiss francs.

Precisely my point:

In my case I rebate the $465 to GBP and the CHF16 to GBP as well.

USD:CHF kind of irrelevant to a EUR denominated folio…

A small matter anyways – was just cross-checking if my logic was wrong.

Apologies about ruminating on this, but I had said on Friday (above):

“save Home Retail Group giving 8.5% total return at today’s prices”

As you saw, a counter-bid was pencilled in last minute over the weekend, doubling my previous returns to say the least…. This is the carrot in this game.

Not to add salt on an open wound, but just to share my rational around this style of investing (sharing is the ethos of this blog after all).

Thanks for writing about this, I had wondered whether it was worth taking the risk but couldn’t nail it down.