Australian stocks: Contrarian opportunity or too early ?

Up until now, I only looked at one single Australian stock: Australian Vintage two years ago. I didn’t like it mainly because I thought the interests between Management and shareholders were not aligned. Interestingly the stock jumped in the last weeks after doing nothing for 2 years.

Australian stock market facts

Let’s start with some facts about the Australian stock market. According to Bloomberg, there are 2.059 Australian companies listed on the Australian stock exchange, total market cap is 1.59 tn AUD.

This compares for instance with 1.92 tn EUR and 1.285 stocks in France and 1.57 tn EUR and 1.167 stocks in Germany.

This comparison tells us two things:

First, compared to GDP, the market cap of Australian companies is relatively high. Germany has roughly 3 times the GDP of Australia and France is still twice as large as measured by GDP. Additionally, there is a surpisingly large amount of companies listed, which for Anglo Saxon countries however is not such a surprise.

Valuation

The ASX 200 index doesn’t look particulairly cheap with a trailing p/E of 24, although the dividend yield is close to 5%.

On the other hand, there are 149 stocks with a single digit P/E and an astonishing 589 stocks with a P/B of below 1. Clearly this is not a big surprise either. With mining and natural resources being in depression, a resource rich country like Autralie will have many companies exposed to this.

537 stocks do have a market cap of below 10 mn AUD, so micro caps are abundent dowen under.

The largest shares by market cap are the banks, Commonwealth Bank has a market cap of 131 bn, Westpac 109 bn, ANZ 75 bn and NAB 74 bn AUD. Especially CBA looks quite expensive at 2,1 times book but all banks are much more profitable than any Western peer with ROEs well in the 15% or so.

Stock Performance:

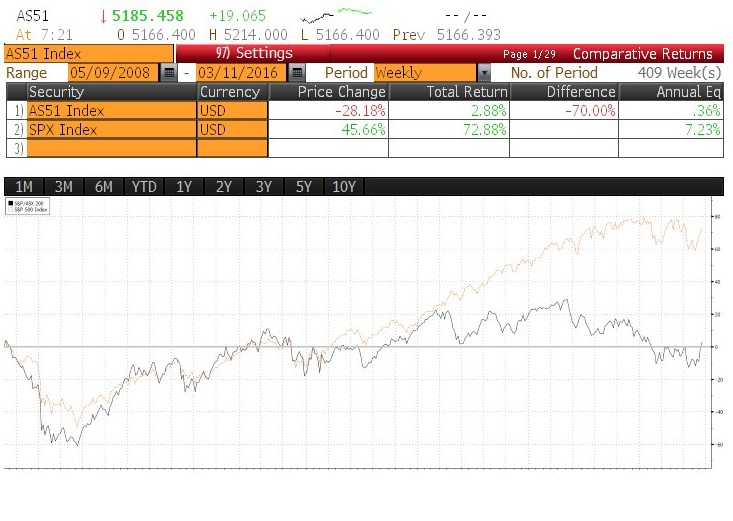

What’s quite interesting is the following: Including dividends, the ASX (in USD) is pretty much flat compared to its peak in 2008. If you would have bought the US S&P 500 instead, you would be up a healthy 72% instead:

So this is almost a “lost decade” for Australian stocks. In my experience, when people start talking of a lost decade for stocks somewhere, this is often a good time to actually own stocks as the next decade is often a lot better although it might not look so.

Dividends – “Franking Credits”

What is very striking at first sight is the fact that Australian companies pay out a lot of dividends. Double-digit dividend yields are not rare. Yes, interest rates are higher in Australia (2,7% for 10 year Govies) but still, normally this would be a reason for big concern.

However there is an interesting specialty with regard to dividends in Australia: They want to avoid double taxation of corporate profits and therefore every Australian holder of Australian stocks receives so called “Franking credits” when an Australian company pays dividends.

Those Franking credits can be used either to offset taxable income or to even claim a refund from the tax authorities in case the investor’s tax rate is lower than the one of the company. In extreme cases, someone who has a tax rate of 0% will therefore participate 1:1 without any corporate tax.

Depending on the investors tax rate, paying out dividends in Australia can therefore be more efficient than retaining profits and explains the relatively high payout ratios of Australian companies.

Macro: Problems, problems, problems – but everything is relative

Yes, Australia has many problems. A huge “hang over” from the resources boom for sure plus a veritable “housing bubble”. On top of that the Australian Dollar looks overvalued, so any investment in Australia is clearly exposed to FX risk.

Nevertheless, compared to other “problem countries”, Australia’s fundamentals still look relatively good: GDP is running at a healthy +3,0% growth rate, unemployment is at 5,8% and debt to GDP is around 35%. In Europe, any country would clearly love to have the “problems” of Australia. Even the perceived star performer Germany manages to grow the ecoenmoy by only 1,5% and has twice as much debt to GDP.

Why Australia and what I am looking for

When I did my first steps into Emerging Markets, I had to find out the hard way, that many of those markets are natural resource dependent (Russia, Brazil etc.) and, more important, corporate governance and general legal standards are very low. Sistema in Russia was the prime example: A very well run company but for some reason the owner got into troubles with Putin and lost his most valuable asset to a “friend” of Putin. So before looking into any of those markets, I think it makes sense to look into a market like Australia first. At least the corporate governance and legal system should be a lot better.

By coincidence, I bought the latest copy of Monocle, a travel/design/politics magazine that I like very much. The focus of that issue was Australia and the fact that according to their view, Australia has much more to offer than iron ore mining and LNG terminals.

The Monocle guys in my experience are often “ahead of the curve” in that regard, so I count that as a “sign” to at least look a little bit more into the Autrsalian stock market.

As I am not a Deep Value guy, I am not looking for asset plays far below book value. What worked for me in the past is more the following: “Good” and unspectacular companies which might have been “thrown under the bus” but do not have too much direct exposure to the problemativ sectors mining and housing. Preferably they have business models that I already encountered elsewhere and of course, reasonable valuations.

Timing & “outsider vs. insiders”

As always in such “contrarian” situations, the risk is high that I am too early and that I will make losses on the first few investments. Again, this is something I am prepared for from my previous adventures into the “PIIGS” and Emerging Markets. Also, there is clearly no rush to invest into Australian stocks. But I do have the hope that along the way I might discover some “Gold nuggets” among all the rubble.

Of course I am an outsider to Australia. Local investors will have an information advantage with regard to local markets, management etc. The advantage of an outsider however is that one can take things “in perspective”. Sometimes things look really bad from the inside but on a comparable basis much better then elsewhere.

Resources

I have already linked to the Forager fund blog. John Hempton from Bronte also sometimes writes about Australia in his fund letter, most recently he went short Australian banking related stocks.

Ben from Wertart Capital had two posts on Logicamms (Part 1 , Part 2), a deep value mining servicer.

There are a couple of stock forums like Aussie Stock Forum. If any readers can help me with good blogs, forums, please don’t hesitate to put them into the comments or send me an Email.

So stay tuned, I hope that I can look more deeply into at least a handful Australian stocks over the next months……

Have a look at Ansell Ltd. They make a frequently used but non-reusable product: condoms.

hmm, I am not sure if this is good business. There used to be a listed German condom producer (“condomi”) but it went bankrupt. Not much brand loyality there i guess…..

Hi, check out shareidea.com.au, it’s a new site that allows investors to share investment ideas. There is a group of quality contributors with some good ideas thus far. Mostly small cap industrials

I love FMG and I am long this company. In response to the iron ore price meltdown, they lowered capex, reduced net debt, delivered outstanding costs improvements and saved cash. IMO they did a very good job. They have recently entered into a strategyc agreement (which makes much sense) with the world’s biggest iron ore miner. Iron ore prices are rebounding. It is definitely worth taking a look at it.

Hi,

I’d like to throw in two interesting Australian stocks for the discussion:

Insurance Australia Group – tied to Berkshire Hathaway (Buffett’s sole Australian investment as far as I know). They are looking to grow in South East Asia. Dividend yield of 7,5%, but seeminlgy a bit expensive on a P/B of 1,92.

The second one is G8 Education – An acquirer and manager of child care centers. Looks like a roll-up strategy, they basically buy child care centers for a lower multiple than their stock multipe. Dividend yield of 9% and growing (the question is how long will they be able to grow?). This is also one of the larger positions of a quite successful mutual fund which is focused on small Asian Companies.

TCN is another potentially interesting one. They are in a joint venture with a tech company (Statseeker) that seems to be growing very quickly. Equity accounting hides this. Their other two companies are interesting too, one of which is based in Germany.

>

I think the low debt to GDP of Australia gives misleading comfort. I am reminded of Irelands very low debt to GDP before the housing crash and onboarding of bank debt to national balance sheet. Australia today has so many high level markers of a housing market in extreme territory, one wonders how they would look after a 30-50% house price fall.

John Hempton who you mention is bearish as is Kerr Neilson of Platinum. Both are highly respected managers with excellent long term records. You will note that Kerr Neilson runs many funds with different mandates and they all have great long term records and are currently very underweight Australia.

Thanks for the comment. Well, yes, that’s what I meant when I talked about “outsider” vs. “insider”. I could be very wrong but situations like this can create (in theory) opportunities.

If you would have asked Italians in 2011/2012 where to invest, they would certainly not have recommended Italy, although looking back there were some wonderful bargains to be found.

Clearly,. banks are not first choice in Australia and anything else directly housing related.

@ MMI: I will also quote John Hempton from Bronte Capital, the Amalthea Letter for February 2016:

“We remain short the Australian dollar. It is not a huge position but the relatively strong Australian dollar will mean Australian dollar returns for almost all Australian dollar denominated international funds will be weak.”

As you know Bronte is OK with his longs but really strong with his shorts, so I would think twice before betting against his shorts.

As he is short the Australian Dollar, he is (softly) shorting the value of all australian dollar nominated shares, calculated in Euro or US-Dollar.

In my experience, stock investors are very bad FX investors (myself included). Bronte is good on the short side with regard to single fraudulent stocks, I am not sure about their “macro capabilities”.

Make sure that your broker will cover those stocks! 😉

By the way, I am sure it will be under your screen but have you noticed Vienna Insurance Group?

best,

I have already checked, German brokers provide access to all Australian stocks, although at different price points per trade….

Vienna Insurance: Funnily neough, you are already the 3rd or 4th one who suggests them within the last few weeks. Short advice: Stay away, i said this already a few weeks ago.

The Australian Financial Review http://www.afr.com/

If you want to look into mining stocks, http://hotcopper.com.au/ may be useful (despite the name, they don’t discuss only copper-related stocks).

Take a look at the FIIG rate sheet too for corporate debt.

In Australia, be wary of complex listing structures and LICs, – a terrible structure.

Read Bronte’s piece on Asset security. If you want more, I can shoot some other stuff through. Essentially though, IB or Chess sponsored or not at all imo.

The funds management sector here has a lot of small, boutique outfits. They all write letters.

Hi

As I live in Australia I thought I’d share some ideas:

http://www.intelligentinvestor.com.au has a few free articles. I’m a subscriber.

Some ideas:

Computershare CPU.AX. World leading share registry provider. Cheap because of low interest rates as they aren’t earning much on their “float”.

GBST Holdings, (GBT)build back office systems for wealth management and pension companies. Have UK exposure.

Just Kapital (JKL) litigation funding company that has recently purchased a medical disbursement business where they purchase a specialist report on behalf of the plaintiff for say $1000 and two years later receive $2000 when the case is settled. https://www.livewiremarkets.com/wires/30191

CarSales (CAR) online car advertiser. They dominate the Australian market, have got some interests in emerging markets.

Silex(SLX) own some technology that enriches uranium. Not earning any money. Depends on whether GE in the US decides to use their technology to reprocess tailings. Plenty of cash.

Molopo Energy (MPO) , another speculative buy. Has plenty of cash, no longer explores for oil, but it in dispute with a Canadian party.

Ellix Medical Laser (ELX), Southern Dental (SDI) and Cogsgate(CGS) are on my watchlist. These are ones I’ve not yet had the time to look at properly or the price has gotten away from me.

And then there are the mining services companies. Forager’s June 2015 quarterly report has a good summary.

In general I don’t find people in Australia as willing to share ideas as they are in other countries.

I own all the stocks mentioned except those on the watchlist. SLX , JKL and MPO are small positions. CPU is still cheap, others have rallied in the last few weeks, with the exception of MPO.

I’m not sure that the pe of the Asx is 24, it seems quite high. The CAPE ratio is closer to 14. http://www.researchaffiliates.com/AssetAllocation/Pages/Equities.aspx

And last but not least, all announcements are listed at http://www.asx.com.au.

Mit freundlichen Grüßen

Christian (Ich bin Deutsch, aber verstehe nicht mehr viel )

>

Thank you, that was what I was hoping for 😉

read a post on boom logistics on Alpha vulture a while ago. Haven’t looked into the stock though as it has some serious commodities exposure.

thanks. I think Boom is more from the “deep Value Mining” corner….

For the mining – I would wait at least watch through summer – next cca three months may bring very misleading signal about the past long term 10y+ cycle in progress.

BHP CEO Says `More Bearish’ on Iron Ore as Price Surge Reverses

http://www.bloomberg.com/news/articles/2016-03-15/iron-ore-reverses-record-surge-as-china-demand-glut-woes-linger

Also many debt collection service companies like CLH had recently plummeted 50% or more in just few days and given huge Australian housing bubble and miners debts they may rise again soon.

You ma look at Japara Healthcare Ltd – JHC, I invested in them when they started – initially because I like and believe in what they set out to do for old people, and now it seems they are growing and doing better then I expected.