Good or Bad Capital Allocation: Example SAP SE (ISIN DE0007164600)

In my previous post on capital allocation, I had mentioned SAP as a company which might have overpaid for an acquisition. A reader commented that SAP is a good capital allocator because they increased EPS over the last 10 years.

Increasing EPS itself in my opinion is not a “proof” for good capital allocation. Actually, this itself says nothing at all. If you have a stable business, just retaining earnings and doing nothing will increase EPS as long as interest rates are positive. Good capital allocation is when you create value from retained profits.

The best way to find out if value is created is to look at how returns on equity and return on capital develop over time.

Let’s take a look at SAP over the past 17 years with some per share numbers:

| EPS | BV | Dvd | FCF | Net debt | ROE | ROIC | Sales | |

|---|---|---|---|---|---|---|---|---|

| 1999 | 0,48 | 2,04 | 0,19 | 0,23 | -0,6 | 26,9% | 21,1% | 4,1 |

| 2000 | 0,50 | 2,30 | 0,19 | 0,31 | -0,8 | 23,3% | 19,4% | 5,0 |

| 2001 | 0,46 | 2,47 | 0,20 | 0,49 | -0,3 | 19,4% | 21,8% | 5,8 |

| 2002 | 0,41 | 2,28 | 0,15 | 1,10 | -0,9 | 17,0% | 23,4% | 5,9 |

| 2003 | 0,87 | 2,94 | 0,15 | 0,99 | -1,2 | 32,7% | 31,2% | 5,7 |

| 2004 | 1,06 | 3,69 | 0,20 | 1,30 | -1,2 | 31,6% | 30,5% | 6,0 |

| 2005 | 1,21 | 4,67 | 0,28 | 1,09 | -2,7 | 28,9% | 28,8% | 6,9 |

| 2006 | 1,53 | 5,04 | 0,36 | 1,22 | -2,7 | 31,4% | 30,5% | 7,7 |

| 2007 | 1,58 | 5,30 | 0,46 | 1,27 | -1,7 | 30,2% | 28,8% | 8,5 |

| 2008 | 1,62 | 5,93 | 0,50 | 1,53 | 0,8 | 27,0% | 24,3% | 9,7 |

| 2009 | 1,47 | 7,13 | 0,50 | 2,35 | -1,3 | 22,3% | 19,8% | 9,0 |

| 2010 | 1,52 | 8,26 | 0,50 | 2,19 | 0,8 | 19,8% | 17,1% | 10,5 |

| 2011 | 2,89 | 10,67 | 0,60 | 2,80 | -1,3 | 30,6% | 22,6% | 12,0 |

| 2012 | 2,35 | 11,85 | 1,10 | 2,75 | 2,1 | 20,9% | 16,5% | 13,6 |

| 2013 | 2,79 | 13,43 | 0,85 | 2,74 | 1,1 | 22,1% | 17,1% | 14,1 |

| 2014 | 2,75 | 16,31 | 1,00 | 2,3113 | 6,1 | 18,5% | 12,7% | 14,7 |

| 2015 | 2,56 | 19,43 | 1,10 | 2,5063 | 4,2 | 14,3% | 10,2% | 17,4 |

One doesn’t need to be a genius to see some trends:

Yes, EPS have increased over the 17 year period significantly as did FCF. On the other hand however, ROE has decreased significantly, ROIC even more as SAP has started using debt in the recent years. The one item that has constantly increased is sales. Especially the last 2 years do look very bad compared to historical numbers.

SAP did pay out dividends but retained the majority of profits (retention rate in aggregate ~68%) and used some debt.

Let’s look how they spend they spent the retained money on

This is a list of large acquisitions they made since 2010:

07/2010: Sybase 5,3 bn (EV/EBIT 30)

02/2012: Succesfactors 3,3 bn (EV/EBIT 28)

10/2012: Ariba 4,3 bn (EV/EBIT 29)

12/2014: Concur 7,2 bn (EV/EBIT 30)

Without the smaller acquisitions, those 4 acquisition represent 20,3 bn EUR Investment or 16,50 EUR per share. This compares with 14,86 EUR total earnings in the same 6 year time period and 15,3 EUR “free” cashflow.

If we look at the table above, the impact of the acquisitions so far doesn’t look that good. Yes, there was a one time jump in earnings in 2011, but since then earnings per share have actually dropped, so clearly the 3 later acquisitions did not add a lot of positive impact so far.

One could even say that SAP returned a lot of money to shareholders, however not to its own shareholders but to shareholders of other companies at “juicy” valuations.

I am pretty sure management has very good arguments (i.e. change to cloud/SaaS) to explain all this in a very positive light this but overall this doesn’t look so good from a capital allocation point of view. Why is that so ? Often a deeper look into management compansation is helpful.

Management incentives /RSUs

As I mentioned in the previous post, the two most important things are in my opinion :

What do companies actually do and how aligned is management with shareholders.

At SAP, top management owns hardly any shares. Bill McDermot owns ~ 4mn EUR in shares which is around 4 month of his 2015 salary (he got paid 10 mn EUR). Interestingly he owns almost 3 mn EUR in Under Armour shares….

SAP pays a lot of bonuses:

The Executive Board compensation package is performance based. It has three elements:A fixed annual salary elementA variable short-term incentive (STI) element to reward performance in the plan yearA variable long-term incentive (LTI) element tied to the price of SAP shares to reward performance over multiple years

So let’s look at what they disclose about those bonuses:

The variable STI element was determined under the STI 2015 plan. Under this plan, the STI compensation depends on theSAP Group’s performance against the predefined target values for three KPIs:non-IFRS constant currency cloud and software growth;non-IFRS constant currency operating margin increase; and non-IFRS constant currency new and up sell bookings.

So the short-term bonus clearly only relies on some internal metric which has nothing to do with return on capital etc. I am not even sure if this is based on organic growth or if, more likely, M&A contributes positively to those targets, independent from the price being paid.

The long-term plan grants so-called “RSU” to the board members, which are some kind of shadow-stock. This then gets automatically settled in cash when the RSU are “vesting”. Interestingly the amount of the RSUs is determined as follows:

The number of RSUs an Executive Board member actually earns in respect of a given year depends on the Company performance against the objectives for that year (a year is a“performance period” in the plan). The objectives derive from SAP’s strategy for the period to 2015. The plan objectives relate to two KPIs:non-IFRS total revenue and non-IFRS operating profit.

Again, the amount of stocks granted does not depend on what they earn on capital but on (easy to manipulate) non-IFRS numbers.

RSUs- aligning management with shareholders ?

The argument of a “compensation consultant” now would be: The fact that the RSUs gain value with the stock price, the interest of the recipients is fully aligned with shareholders.

My personal experience with RSUs however is very different. The biggest problem of RSU’s is that you never own the shares. You only receive a cash payment usually based on the stock price at one or several days within a year. You can not decide for instance to hold the RSUs for longer if you think the stock is undervalued. The RSUs also have no rights on dividends. So paying out dividends actually lower the value of a RSU.

Also, for management it is very easy to cash out, as RSUs get exercised automatically. If they would own “real” shares they would need to disclose those sales to the market

In my experience, the RSU system leads to 2 major management reactions:

First, they try to get as many RSUs as possible by beating self defined an easy to beat targets and secondly, they try to talk up the stock price shortly before the date when the final payout is determined. Both are not aligned with long-term share holders and are not really helpful in creating long-term shareholder value.

In many German companies, those RSU “Mid term” plans were often introduced “on top” of the previous salary and annual bonus, which in my opinion further weakens the link between shareholders and management.

In my subjective opinion, SAP’s management compensation is a typical “other people’s money” scheme with only very little (long-term) alignment between company and shareholders.

Does it matter for SAP ?

Some people might argue: Why should we care about ROEs etc. at SAP ? This is a software company, so other factors (usually Non-GAAP) are much more important.

In my opinion, this is wrong. We buy stocks because the companies make profits. Either the company pays out the profits or it invest it on behalf of the shareholder into value creating new projects. One can argue about adjusting certain metrics, but in any case, reinvesting profits into overpriced M&A trnasaction is definitely not value creating, even in software.

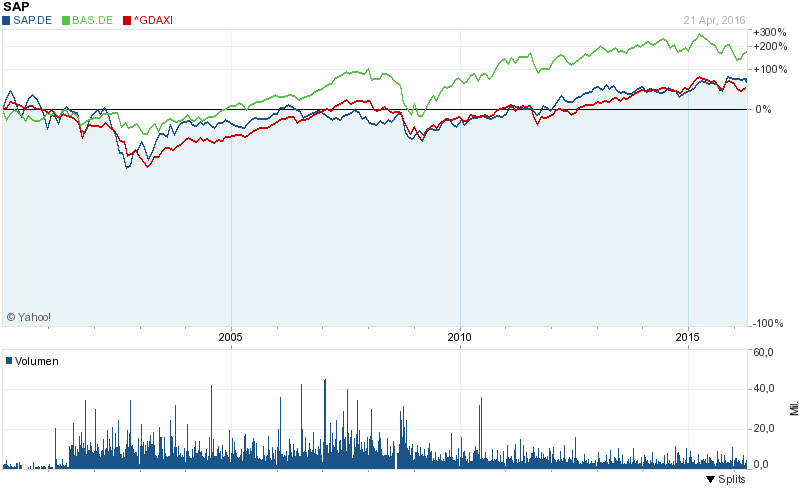

Let’s look at the long-term stock price development of SAP:

So we can see, yes, SAP over the last 15 years or so has beaten the DAX by a small margin. But if you consider that the DAX includes some very badly run companies such as the banks, E.On, RWE, this is not such an achievement.

If you compare for instance SAP with BASF, a well run company but with a much tougher, capital-intensive cyclical business, it is quite easy to see that BASF seems to have created a lot more shareholder value than SAP despite the fact that the business itself should be a lot better.

It is always hard to quantify qualitative aspects, but I do think that the relatively weak alignment between shareholders and management play a role in the rather weak performance. It is a little bit surprising as one of the co-founders of SAp, Hasso Plattner is still head of the supervisory board but maybe he is so busy sailing against Larry Elison that he forgot to better incentivize the management.

Summary:

SAP is in my opinion a relatively typical example of a large, publicly owned German company. Management is not well aligned with the long-term success of shareholders but rather is incentivized to pursue growth for the sake of growth.

In SAP’s case they can build on a solid foundation of a dominant business software product, but at least looking at the last few years, they did not much to create additional value.

It looks like that the incentives favor acquisitions which add to Top line or other “non GAAP” measures, but actually making money on the M&A investment itself is not a priority. This, in my opinion, is one of the big differences to the “Outsider Companies”: A typical Outsider CEO wants to make actual some “real” money on M&A:

Within a shorter time frame, SAP could still be a good investment, but personally, I would be very carefull to invest long-term into the stock. It looks like that SAP prefers to pay out its profits to the shareholders of acquisitions targets without creating a lot of value instead of returning money to its own shareholders.

Alignment of management and shareholders is something I did already include in the past in my investment process, but I will focus on this even more in the future.

Overall it might be fun to more systematically look at this aspect. Maybe this would make a good ETF…….

Edit: For the fun of it, check this out on SAP from Quora

Any opinion on SAP after the recent drop of more than 25% recently. Bill McDermot has long been gone.

No. SAP is to big and complex for me to gain any kind of “edge” so I stay away.

This post is more than a year old. but from the side of a software engineer I see that their inovations like HANA and Cloud are very hot and next step will be AI!

Next years they will deeper diving into the asian market.

You have to compare SAP to Oracle, Salesforce.com and Microsoft these are competitors of SAP.

Then you will get another view of the metrics!

Wie kann man denn das Management der SAP SE anhand des fehlenden Commitments kritisieren und gleichzeitig bei einer Dt. Pfandbriefbank (!!!) investiert sein? Ich kann es leider nicht nachvollziehen.

Gruß

Ich denke mal dass du mein blog nicht regelmaessig liest. Die pfandbriefbank laeuft bei mir als “special situation”. Da gelten andere kriterien als bei den langfristigen titeln. So schlecht ist aber die kapitalallokation der “neuen ” pfandbriefbank nicht. Non-strategic abbauen und neugeschaeft akquirieren ist m.e. ok

.

Your verdict on SAP is understandable, by and large. My 2 cents on the investment case:

1. Acquisitions in the software industry cannot be judged very well (at least I feel not capable) by solely looking at the group ROIC. As acquired code / technology is capitalized on balance sheet in contrast to proprietary R&D, ROIC will inevitably suffer even from value creative acquisitions. Under the former CEO Kagermann, SAP abstained from larger acquisitions until 2007, officially because it felt acquired software would endanger the “consistency” of their offer. This viewpoint was obviously modified with the take-over of Business Objects in 2007 and the series of further acquisitions thereafter. So it is no surprise that ROIC came significantly down after 2007.

Notwithstanding, the acquisitions you mentioned had price tags between 28- 30 x EV / EBIT, which imply transaction ROICs of 3.3-3.6% (before taxes !). So they are clearly no examples for good capital allocation, no doubt about it.

2. The real weakness of SAP in the last decade in my view was their total inablity to develop proprietary cloud solutions despite commanding one of the largest developer pools in the industry. SAP tried to build something internally several times (i.e.”Business by Design”) but commercially, every attempt was a complete disaster. So SAP felt under pressure “to do something” about it, and started to go shopping. While 1-2 cloud acquisitions appear understandable against that backdrop, it remains the management’s secret why it had to be four cloud acquisitions (Success Factors, Ariba, Fieldglass, and Concur) until now.

3. What is the upside risk for the SAP share? Well, if the company continues to do large scale software acquisitions for premium prices, the share will remain a non-performer. But what if not? Remember, already in the past SAP turned their acquisition strategy by 180 degree, from “no acquisition at all” until 2007 to “let’s buy one software company every year for whatever price” thereafter. As SAP is now the largest cloud company in the world, it has theoretically the resources to build and market their own cloud applications on a grand scale, besides their still very profitable, market leading on -premise business like their ERP solution. That’s how you create value in the industry: Not by acquiring, but by successfully building and selling your own code, and as of today, SAP is in theory in a privileged position to do so. Not extremely likely, but the probability isn’t zero, either. And even strategies and management boards can change at some point in time.

Nice post. Overall I share your opinion about the capital allocation (and the reasons for it) at SAP. Just wanted to point out that ROE remains roughly constant. In 2015 there were exceptional items regarding employee layoffs. Taking them into account the ROE remains at ~20%. Nonetheless, it’s clear that the ROE in the last years only remained at ~20% by making (cheap) debt, thereby lowering ROIC.

I haven’t looked that deeply into SAPs numbers, but in my experience, “one offs” are often not really “one offs”.

Hi how do you see some new value coming up. Do you think Apple is becoming reasonably priced? What about BP with 8% dividend? Maybe there are some good opportunities coming up. How do you see this?

To be honest: I have absolutely no idea. However, a dividend alone is never an argument to buy a stock.

How was the valuation (P/E ratio) SAP, BASF at the beginning of the shown time horizon. Part of the underperformance might have to do with high valuation of SAP compared to BASF, something that has nothing to do with management or capital allocation in the following years

no, lower multiples (or contracting multiples) are almost always a function of deteriorating fundamentals. In SAP’s case I am clearly not the only one noticing this. BASF by the way trades at pretty low multiples too, no excuse here.

In 2000, BASF reached a PE ratio (adjusted) of 24.5 and SAP a ratio of 147.

If you are saying “BASF seems to have created a lot more shareholder value” in the last 15 years, don’t forget the IT bubble.

Who said that SAP is a good capital allocator because they increased EPS over the last 10 years?

It wasn’t me.

I’m just saying: Not really good, not really bad.

What else could they do? The alternatives would have been worse in the long run.

I took my freedom as writer to make it more dramatic. But yes, I was you who mentioned that the increase in earnings is somehow a positive point for SAP. Which in my opinion clearly isn’t.

In the long run, we are all dead, but in any case, for the time being, Concur’s shareholders are much happier than SAP’s.

Or to phrase it in another way:

SAP seems not to be able to reinvest the money they earn into their core business.

So they have 3 possibilities what to do with that money:

1) Keep the cash on the balance sheet and wait for opportunistic action

2) return it to shareholders via dividends/buybacks so that they can decide where they want to put the money

3) aggressively buy other companies and thereby give the money to other shareholders

I am not convinced that 3) is the best long term strategy for shareholders. However it is without doubt the best strategy for managment pay under the current incentive system.

During transition from mainframe to client/server, SAP was a pioneer. With SaaS, some competitors were ahead and now SAP needs a broad set SaaS solutions to stay relevant in tomorrow’s world. A me-too move wouldn’t be enough.

Your possibilities 1) and 2) would mean higher ROE and ROIC today but also a slow death.

Not necessarily. First, Sybase and success factors had nothing to do with cloud. Sybase was clearly the attempt to annoy arch enemy Oracle.

Instead of Concur, they could have actually hired some smart people. Would have taken maybe longer but much cheaper and better for shareholders. However Management would have gotten less bonus.

Again, I do think that the incentives are not well aligned at SAP.

How you come to believe that Success Factors had nothing to do with cloud? It’s pure cloud.

The HANA project began in 2007 at the HPI and development by SAP started in 2009. In May 2010, SAP announced it would be acquiring Sybase. Sybase had much more database know-how than SAP and was strong in mobile (Afaria, Mobile 365, SUP).

According SAP, HANA is primarily designed for the cloud.

I guess SAP, as well as their main competitors, is trying to hire all smart people they can get.

Unfortunately, SAP has to adjust now.

Excellent post.