French update: Installux, G. Perrier & Thermador

Installux

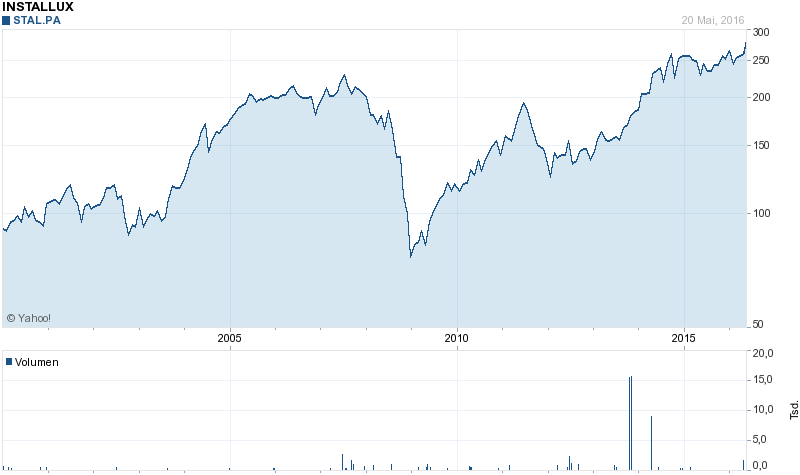

Installux released 2015 results a couple of days ago. EPS went down slightly from 28,12 to 26,63. With 31,7 mn EUR or 104 EUR per share, at the current share price of 271 Installux trades at an adjusted P/E of 6,3x.

The decrease in profit seems to be attributable to a reserve for a legal dispute in the Roche Habitat subsidiary. Roche Habitat is still the “problem child” and the only subsidiary making losses. The annual report states however that the restructuring is well on track and that sales at the division increased by 13% in 2015. If that division turns around, this could easily add 1-2 EUR per shar in profits in 2016.

Installux is maybe not a great company but a solid and very resilient company and at the current valuation still a very good “hold” in my opinion. Interestingly enough, Installux trades near its all time high:

G. Perrier

G. Perrier released its annual report 2015 some days ago.

2015 EPS was 2,65 EUR per share vs. 2,50 EUR. Cashflow generation was exceptionally good so that they now have 38,8 mn EUR or ~10 EUR per share in Cash. At a current share price of 35 EUR per share, this means that adjusted for cash the P/E is below 10.

The first quarter looks pretty Ok as well. Overall, this quality (boring) company is still very reasonable priced and will remain a core position of my portfolio.

Thermador

Thermador released 2015 numbers and the 2015 annual report already some weeks ago. Stated EPS were 4,55 EUR vs. 4,47 in 2014. This includes two companies (Mecafer and Nuair France) that Thermador acquired in 2015. Without the acquisitions, EPS would have gone down by a low single digit percentage.

As Thermador is highly geared towardsFrench construction activity, the performance itself is quite good, the business seems to be very resilient.

Adjusting for around 4,50 EUR cash per share, the trailing P/E is now around 15,5 which clearly is not that cheap anymore. The current share price clearly implies EPS growth in the next few years (Bloomberg estimates are ~10% EPS growth for 2016 and 2017). This is something one will need to watch. 2015 earnings were still below the 2007/2008 level despite higher sales. If they actually grow earnings like estimated, the price is pretty OK, if not, the stock would be more or less fully priced in my opinion.

Besides your french aversion for some time, some good stockpicks for french market @ http://www.independance-et-expansion.com (http://www.independance-et-expansion.com/documentation-18.html provides the resp. portfolio composition).

thanks for the link. One remark: with 25% of my portfolio invested in French small caps, I don’t think that this should be called an “aversion”.

Hi Your Self

I also think that G. Perrier is an excellent boring company and one of my long-term positions.

I don’t know if you have had the opportunity to talk to them directly recently.

Something which I don’t understand is why the energy sector (Ardatem) is growing so slowly. Ardatem is exposed to the nuclear and EDF has massive CAPEX which should benefit Perrier.

hi Anton,

as you might know, I am an armchair Investor, meaning that I usually don’t talk to management. So I don’t know why they are growing not more strongly in that sector.

mmi

Ooops, sorry about the wrong name. I don’t know how I came up with that name.

The thing you said about the risk of anchoring is true. I can’t get out of my head the entry price of my investments, the forecasted exit price, previous peaks and minimums, etc., and that surely affects my valuations.

Thanks a lot for your answer and your blog.

Although I am not sure to whom you refer by “martin”, I will still try to answer:

1. I have no fixed pprice to exit. For me this is always relative. Putting up a fixed number increases the risk of “anchoring”. Using a flat figure like 400 is in my opinion also not very clever.

2. I have looked at GEA, but for me the business is too much project driven.

Great update. Two questions, Martin:

1) I think that Installux is a well-managed company in a bad industry, with no moat whatsoever. I am happy to hold the shares as long as they are undervalued and the company keeps a healthy free cash flow. However, I always have a hard time deciding when to sell. I’d say around 400, for a market cap of 120 M€. At which price would you sell right now?

2) What do you think about French GEA, a classic among value investors?