Banking stocks part 2 – Handelsbanken, Lloyds, Van Lanschot, Pfandbriefbank, Citizen (and yes Deutsche again)

This is the follow-up post to the one from last week about banking stocks in general and Deutsche Bank in particular.

Damodaran on Deutsche Bank

Before moving on to my own stocks, again Deutsche Bank. Prof. Damodaran did value Deutsche Bank last week and came to the following conclusion:

At the current stock price of $13.33 (at close of trading on October 4), the stock looks undervalued by about 36%, given my estimated value, and I did buy the stock at the start of trading yesterday.

What he basically does is that he assumes an ROE of around 9,44% after ten years and capital costs around the same number,wich at the end of the day is assuming some kind of mean reversion and a Price to book value of ~1 in year 10.

What I do like about Damodaran that he always makes his assumptions very transparent. So it is quite easy to disagree with him on certain assumptions which I do not want to do here. I want to make another, more general point:

Assuming “average ROEs” in 10 years and a cost of equity at around 10% will turn almost any European banking stock into a great investment at current valuations which are a fraction of book value in general.

However in my opinion the biggest issue with Deutsche bank is the following: The management and the Chairman of the Board at the end of the day do not care about shareholders. They will do everything to protect the bank in its current form. Instead of selectively selling business to increase capital, they will happily sacrifice the shareholder and issue a lot of new dilutive stock if they have to. I think the probability of a dilutive capital raising is quite high.

Back to my own banking stocks – what to do now ?

My readers know that I do have quite some Banking exposure. Within my special situation bucket , I own Lloyds, Pfandbriefbank, and Citizen Financial, on top of that I own Van Lanschot as a “boring” value stock and Handelsbanken as a core holding.

Together, that is almost 15% of my portfolio. In general, all banks are impacted by the flattening of the yield curve and the spread compression and my timing and the fact that I kind of overweight banking stocks was clearly not optimal.

However I would compare banks in the current situation a little bit like Oil companies: For those who produce at a really low cost, you can still make money and over time, competition might go away to a certain extent, especially if you make your money in retail.

So for Handelsbanken, I am still quite optimistic as I consider them “best in class”. They do have a cost advantage and are well run despite a recent CEO change. Of course, we will mabye not see the growth I assumed in the initial case, but the downside risk should be limited as well. Looking at the stock price we can easily see that Handlesbanken has done much better than the European banking index and also slightly better than local peer SEB.

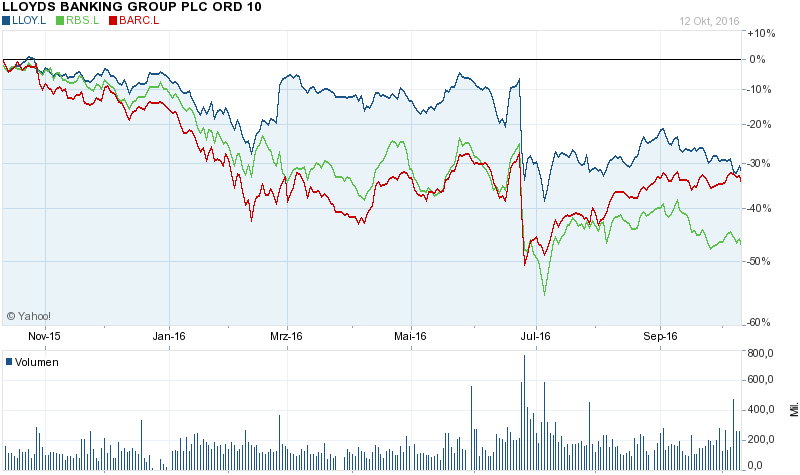

With Lloyds, I clearly didn’t take into account the Brexit with its drastic impact on UK interest rates. I still belive that they are the best “big” UK bank, but it is hard to justify an overweight. That is the reason why I cut down my overweight compared to the other banking stocks to fund the (undisclosed) UK Small cap.

At least my assumption that Lloyds is the best of the big 3 UK banks is somehow validated by the stock price, as Barclays did slightly worse and RBS much worse:

I am not sure to be honest what to do with the stock. If UK interest rates stay where they are, this is clearly a game changer for all UK banks. Also I find it difficult to turn a special situation (gone wrong) into a long term investment. I do think there might be better UK opportunities out there.

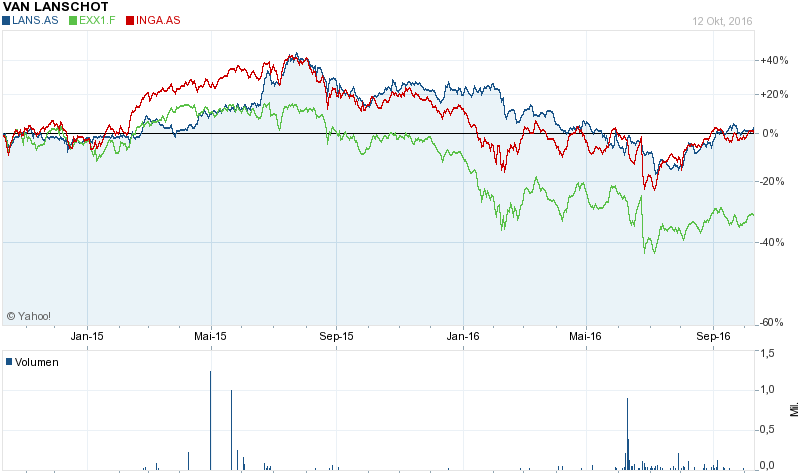

For Van Lanschott, the current EU environment means that the turn around will be much slower than I anticipated. I will need to check how they progress in their private banking business which in my opinion gives them a better chance to increase profits. But it needs to be seen if they can really grow that part.

The chart shows that interestingly Van Lanschot trades pretty much in line with ING but significantly better than the banking index:

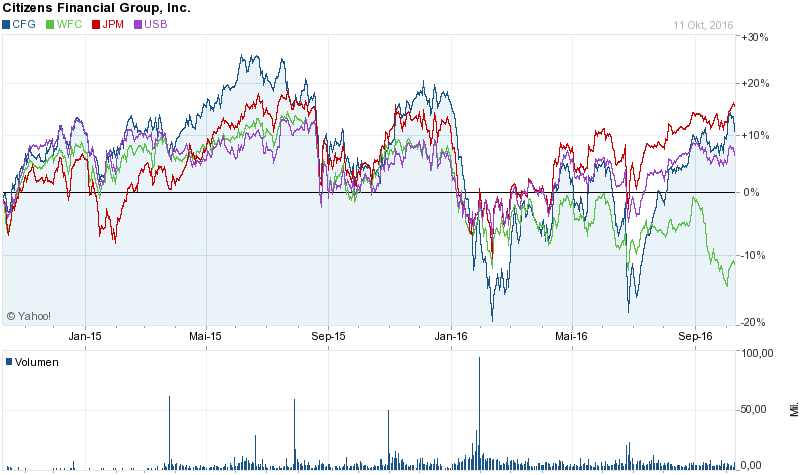

Citizen’s in the US is less effected from the ECB’s aggressive move into Corporate bonds, but Janet Yellen already indicated 2 days ago that she might be willing to follow the same road if things are gettng tough in the US once again. So no reason for complacency.

Citizen’s stock has done comparably OK if we compare against JPM, Wells Fargo or US Bancorp:

I still think it could be an acquisition target, on the other hand it was a special situation (RBS forced sale) and I am not really convinced for the long term.

Pfandbriefbank finally is the most interesting case. As a pure mortgage lender with the Pfandbrief as financing instrument, they are to some extent less negatively effected. However, especially in the mortgage market the non-traditional lenders are moving in aggresively. This already led Pfandbriefbank to drastically cut their growth targets and target an entry into the US market.

Personally, I don’t think that this is a good idea. No one is waiting for Pfandbriefbank in the US and USD funding for European banks is not cheap. I still think it would make a lot of sense to combine Aareal and Pfandbriefbank in order to cut costs.

However we can clearly see that Aareal bank has done better over the last year, but clealry Deutsche Bank and Commerzbank are much worse.

Pfandbriefbank sits on a lot of Excess capital, especially now that the Heta case seems to be resolved in their favour. I am a little bit irritated that managment is always talking of potential significant higher capital requirements (Basel IV) without giving specific details.

For the time being I will keep the shares but I am not 100% happy with managment.

Summary:

Overall I think within a bad secor, my stock picks did relatively well.

I do think within my own banking “portfolio”, the “special situation” Citizens and Lloyds are the first stocks to go if I have better ideas. Van Lanschot and Handelsbanken are more longer term cases which look more difficult right now then when I bought them but are still intact. Pfandbriefbank still has the best prospects among the special situations and will stay for the time being as well, but one has to watch management closely.

https://www.euronext.com/en/cpr/van-lanschot-kempen-return-capital-eur1-share-20-december-2017

1 EUR per share returned

Macroman had an interesting post today. Let me quote some part of it:

“Basel III is a bigger issue. If McHenry’s letter to Yellen is properly representative of new policy then it hits the EU head on. The EU has been proudly touting its new banking regulations which should identify weak banks (yes, done in style) and be part of the path towards a unified European financial system, whilst also allow the politicians to wave a huge moral flag in triumph. But what happens if the US banks are suddenly told they don’t have to play by the same rules? They instantly have a competitive advantage unless the EU backtracks and loosens Basel III in response – Highly unlikely for them to do such a massive U-Turn just because Trump has pushed them into a corner – or they immediately remove the US’s European banking licenses if they don’t comply. ”

I wonder if this is positive for Pfandbriefbank if they really want to set foot in the US.

Also, what about French public finance if Le Pen would be elected?

If Le Pen is elected and France would actually exit the EUR, PBB has a BIG problem.

do PBB currently have a significant exposure to French government bonds?

I’d assume that unlike bonds, loans are to be repaid in EUR, regardless of any currency change France might do.

They have 3 bn “public sector” exposure. I am not sure if loans are automatically repaid in eur. Actually i think it depends on the governing law in the contract.

Pfandbrief crashed a bit today….

Yes. That was interesting. If you read the news it looks like a loss, but that is not clear yet in my understanding.

It is a likely loss…

why ?

Greenlight has just acquired a 5% stake in PBB

thank you. Einhorn bought well cheaper than I did 😉

https://www.pfandbriefbank.com/investor-relations/pflichtveroeffentlichungen/mitteilungen-nach-21-ff-wphg/detail/8494.html

To drop another name: Have you looked at the Bank of the Internet? http://www.wertpapier-forum.de/topic/36703-bank-of-internet/page__view__findpost__p__1042322 – it looks quite interesting: http://de.4-traders.com/BOFI-HOLDING-INC-8597/fundamentals/

PBB – 1. share your concerns. They have no idea what kind of jungle they are about to enter (US East Coast) and think they can amend ignorance through syndication. Good luck!

2. was the lawsuit about Genusscheine a HETA thing or are those two different issues ?

Hi, I’m just starting to look at LLoyds. I think the original reasons you bought were valid – a company thats’s slowly, structurally recovering from past excesses, in an industry with few players. I don’t think rates will go negative – I saw an article with Mark Carney saying he considered 0.25% a floor for interest rates (sorry, lost the link), so we are at the bottom. Long term, I think UK will be fine with Brexit.

I think the risks are:

– UK is due for a cyclical downturn in property: http://www.tradingeconomics.com/united-kingdom/housing-index. We never know when it will happen, but I’d probably limit my position to half. I’m only really comfortable buying in a recession… *after* the downturn.

– Short-term currency exposure when buying a domestic UK company: How far will the pound fall while Brexit is sorted out? I have no idea.

– A high percentage of LLoyds earnings is from ‘trading’. Some of this is for their insurance products (“participating investment contracts”), but even after I remove that part, its 35% of operating income in 2015. Some years its higher that net interest income!

The annual report says they do not do proprietary trading, so this must be from market-making operations (e.g.: selling OTC securities to clients at a markup), or from the change in value due mark-to-market accounting requirements.

But expect the trading income to be volatile year-on-year (not necessarily in line with the economy). I need to factor that in for returns and PE valuation

I think the stock is a little cheap, but not very cheap. The reasons for it being cheap will go away. Brexit will happen, then be a non-issue. ZIRP will end sometime (no sign of it yet, but once we can see it, so can everyone else).

You can short out your GBP exposure pretty easily.

My favourite EU Bank ist clearly ING. They have a good to excellent cost position, have cost leadership in the german market with ING-DIBA and as a mainly retail bank seem not to be exposed too strongly to some actual risks (e.g. oil and gas). They are earning good money and in a Position oft strength decided now to further cut costs by reducing their workforce in NL and B. Do you agree wirh my positive view?

ING has some relatively signifcant commercial banking as well in Benelux….

Hi, thanks for the write up!

Speaking of banks I wonder if you’re familiar with Customers Bancorp (CUBI:NYSE). It is a fast growing bank with a low cost business model focused on opening only very few branches thus reducing overhead costs. Most importantly the bank is run by an outsider type CEO, Jay Sidhu who previously built up Sovereign Bank before selling it to Santander. During his 20 year tenure at Sovereign he compounded shareholder value at 17% which is pretty impressive, especially for a bank. The stock currently also seems more than fairly valued at 1.2 times book. There’s also a good write up on it in VIC. Think it is an interesting opportunity presently among banks.

never heard about them. Sounds interesting though.

What do you think about DNB? One of the lowest C/I-ratio in the world, P/B ~1.

I don’t really know them….

Isn’t DNB strongly exposed to Oil and Gas (e.g. Seadrill)? That could become quite a nightmare.

Around 10 % of loans exposed to oil, gas and shipping. Page 179 https://www.dnb.no/portalfront/nedlast/no/om-oss/resultater/2015/konsern-aarsrapport-dnb-2015.pdf

The whimsy of the posting icons is an interesting contrast to the seriousness of the content.

I think it’s a bad time for Pfandbrief to grow or even maintain their existing size given where their equity is priced. I think they should focus on shrinking their business and using any equity freed up to buy back stock. Clearly that is not a road management wants to voluntarily go down. Thing needs a serious activist.

any thoughts on Bank of Ireland? They are still in private ownership and I wonder if Euro does not break up; brexit is not severe on Ireland and Deutsche does not need state assistance, could they move up 50%?

I have never really looked at them….

Bank of Ireland is a very good bank with some of the best interest income in Europe. Thanks to the rapid rise of real estate prices in Ireland (20%/year), the stock of NPLs (mostly from soured mortgages) reduces steadily. Unfortunately, those margins attracted the ire of the schizophrenic Irish government, which now wants to cap mortgage rates. You can also imagine that they will force the bank to lend to lower quality borrowers (if that reminds you of what led to the 2008 crisis, no surprise). One other large cloud is the fact that 50% of their loan book is in the UK (they provide banking services through the post office). Finally, valuation is quite fullcompared toother european banks (deserved because it is better) and market does not take it kindly when there are potential bad news.