Updates: Kinder Morgan (SELL), Deutsche Pfandbriefbank (PBB)

Kinder Morgan

Yesterday, I sold my complete Kinder Morgan position at ~21 USD per share with a total gain of around 25% (in EUR, including dividends). Why ?

When I bought the stock in April I argued like this:

For me, the “expected case” would be something like a 8% discount rate and 1% growth resulting in a fair value of around 25,60 USD per share. Also, under my assumptions, the downside is relatively limited. Based on 18 USD per share (at the time of writing), that would imply an upside of around +42% which for me would be an acceptable return over my typical 3-5 year investing period (plus any dividends).

So why did I sell out now and didn’t wait for higher prices ? Well, something has changed: Interest rates went up. Since April, the 10 year USD Swap rate went up by +0,90% and the 20 year rate by around +0,70% p.a. If we look at my valuation grid from back then we can see that the value reacts significantly to change in interest rates:

| EBITDA | 6,8 | bn USD | |||

|---|---|---|---|---|---|

| Net debt MV | 40 | bn USD | |||

| Shares | 2,231 | bn | |||

| 6% | 7% | 8% | 9% | 10% | |

| 0% | 32,87 | 25,61 | 20,17 | 15,94 | 12,55 |

| 1% | 43,03 | 32,87 | 25,61 | 20,17 | 15,94 |

| 2% | 58,27 | 43,03 | 32,87 | 25,61 | 20,17 |

| 3% | 83,67 | 58,27 | 43,03 | 32,87 | 25,61 |

| 4% | 134,47 | 83,67 | 58,27 | 43,03 | 32,87 |

| 5% | 286,87 | 134,47 | 83,67 | 58,27 | 43,03 |

In the 1% growth case, a 1% interest shift (which is what we have seen almost now) would lower the fair value from 25,61 USD to 20,17 USD per share, below the current stock price.

Maybe we will see higher growth now with Trump ? I do not know and honestly I don’t want to find out. For me, KMI was not a growth case but a “Contrarian Bet” and after the increase in interest rates and the positive performance, the stock in my opinion is now fairly valued. And as I prefer undervalued stocks, I sold my position. It might be too early, but that’s part of being a value investor.

Interestinlgy, Berkhsire has also reduced their position already in Q3 2016.

Deutsche Pfandbriefbank

Pfandbriefbank shocked markets on Wednesday with the following Adhoc news:

Munich, 13 December 2016 - Deutsche Pfandbriefbank AG ("pbb"), the legal

successor of Hypo Real Estate Bank International AG, Stuttgart, is the

issuer of credit linked notes of the "Estate UK-3" synthetic securitisation

transaction ("Credit Linked Notes"). These Credit Linked Notes hedge the

default risk from certain credit exposures of pbb, provided that the

conditions for the allocation of realised losses have been fulfilled in

accordance with the terms of the Credit Linked Notes. A default affecting

one of the hedged exposures ("Reference Claim No. 3") has caused a loss of

approximately GBP 113 million (please refer to pbb's ad-hoc announcement

dated 18 January 2016); pbb intends to allocate this loss to the Credit

Linked Notes. This loss allocation would trigger a total loss for Credit

Linked Notes Classes A2, B, C, D and E, and would reduce the nominal amount

of Class A1+ (of GBP 400,000) by approximately 0.1%.

Deloitte GmbH Wirtschaftsprüfungsgesellschaft, in its capacity as trustee

of the ESTATE UK-3 transaction, today notified pbb that in their view

doubts exist as to whether the loss allocation intended by pbb is

justified, and that the Trustee will appoint an Expert, in accordance with

the terms of the ESTATE UK-3 transaction, who will decide on whether the

loss allocation is in fact justified.

In the event of the loss allocation being fully or partially unjustified,

pbb would have to bear the losses to that extent. In pbb's opinion, the

conditions for the planned allocation of losses have been met.

The prospectus for the ESTATE UK-3 transaction is available on pbb's

website: https://www.pfandbriefbank.com/debt-instruments/securitisation/

estate-uk-3.html.

So what does this mean ? The predecessor of Pfandbriefbank has issued a Credit Linked note (CLN) for which PBB is still on the hook. One of the underlying credits defaulted and the Trustee is investigating this.

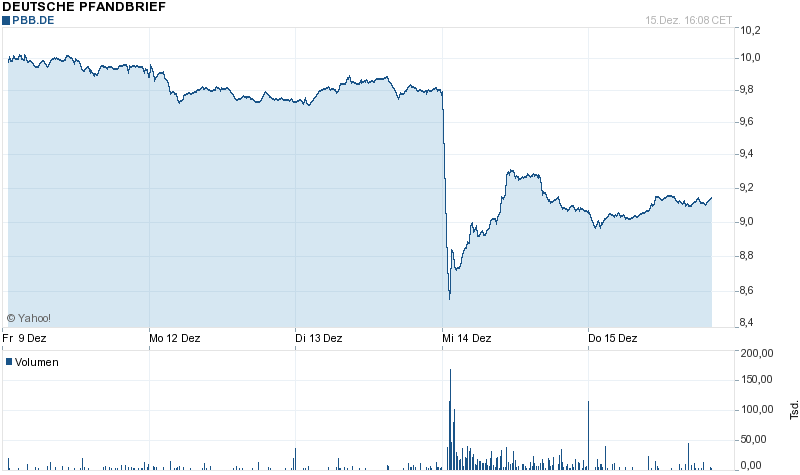

The stock of Pfandbriefbank directly dropped by 1,20 EUR per share, erasing 160 mn EUR of market value.

So the initial drop in market value was significantly higher than the potential damage. Plus, whatever claim would arise out of this, most likely it would be reduced by a tax set-off in my opinion.

After this knee jerk reaction, the stock price recovered to currently around 9,15 EUR, which represents roughly a 90 mn EUR loss in market cap which is approximately the after-tax loss if they have to fully pay for this. So the market seems to price this in as a 100% probability.

PBB references another Adhoc message from January 2016 where they already announced that the underlying loan had defaulted and that they expect the CLNs to be wiped out.

The new information is clearly only that the Trustee appointed an expert to assess the situation. So how relevant is this ?

I had a quick look at the prospectus and although I am not a lawyer, it looks like that the investors knew what they were investing into. This is from page 2 of the prospectus:

The payment of principal of and, due to potential principal reductions, interest on the Notes is conditional upon the performance of the Reference Claims as described herein. There is no certainty that the Noteholders will receive the full principal amount of the Notes and interest thereon and ultimately the obligations of the Issuer to pay principal of and interest on the Notes could be reduced to GBP 1 per Noteas a result of losses incurred in respect of such Reference Claims.

The most interesting part in my opinion is one page 105 which says this:

THE TRUSTEEPursuant to the Trust Agreement, the Trustee has agreed to serve in a fiduciary capacity to protect the interests of the Noteholders and the Senior Swap Counterparty. In particular, the Trustee will (i) verify the determination and allocation of Realised Losses, (ii) make required appointments of third party experts, and (iii) perform such other functions as are specified in the Trust Agreement. See “The Trust Agreement”.

Again, I am not a lawyer, but “fiduciary responsiblity” in this regard means that in the case of Noteholders being wiped out, the Trustee has no alternative other than to investigate this on behalf of the note holders. If the Trustee would not do this, they would run the risk to get sued by the creditors. So I think they would appoint an expert in any case to avoid any potential liabilities for themselves.

So the appointment of a third-party expert is “according to the book” and should have been expected by anyone with real knowledge.. The statement of PBB that in their opinion “the conditions for the planned allocation of losses have been met” is in my opinion a pretty strong statement and they would not make this without really having a positive opinion of their own lawyers.

In my opinion (and of course I could be totally wrong), this Adhoc news was a non-event. Of course the question could be: Why did the stock price drop so significantly ? This must mean that there is a problem. However in my experience, very few people these days are actually reading bond prospectuses so I think there is a high probability that this was an overreaction to a headline.

However for the time being I am also not increasing my position because my overall cash level is pretty low and I want to keep some flexibility going into 2017.

Is this a good time to invest back into Pfandbriefbank? Around 10EUR the Div yield is above 10%. The entity is still overcapitalized

Looks like Buffett has completely sold KMI:

https://www.bloomberg.com/gadfly/articles/2017-02-15/warren-buffett-and-kinder-morgan-not-buying-the-meadow

On PBB, I can see why investors would be freaked out. Not necessarily b/c PBB will take the losses but more for implication for other loans… I mean a 113mm loss on a 176mm loan was declared. That loan had an original LTV of 75%.. so the property is now only worth 63mm or like 27% of appraised value at time of underwriting!

So maybe all those 60% LTV loans are not as safe as they seem…

hmm, could be but in my opinion this is not so likely. Although I don’t know all the details it looks like that this transaction was not a “Normal” transaction. I guess they were surprised about the default, otherwise they would have left it with the Government as the other “real” problem loans.

You’re valuation work was based upon low interest rates. What would you have done if the stock went down instead?

If it would have been atill significantly undervalued, I would have kept it. If it would have been fairly valued despite going down, I would have sold it as well.