Hastings Plc (ISIN GB00BYRJH519) – the “next Admiral” or an accident waiting to happen ?

The company

Hastings Plc, a UK-based direct insurance company was IPOed in 2015 at 1,70 GBP per share (IPO prospectus). To call Hastings a “Mini Admiral” is actually very close to the truth.

The company was founded as an underwriting Agency in 1996 by an American called David Gundlach who then sold the company 10 years later. Via a couple of more transformations (MBO etc.) Hastings then was finally brought to the stock exchange. Interestingly, according to some sources, Gundlach had worked at Admiral before so it is no surprise that Hastings looks pretty much like a 1:1 copy Admiral:

They only do direct business, reinsure significant amounts of their premiums and make their money mostly with anciliariy products and fees instead of investment returns like “classical” insurance companies. They only exception is that they don’t run a price comparison website (PCW) but they sell almost all policies via PCWs. Like Admiral, they have branched out into home insurance from

Hastings currently has a market cap of ~1.5 bn GBP and trades at an estimated 17,6 times 2016 earnings.

The business model

The business model is very similar to the one of Admiral which I described some time ago on the blog. In comparison to traditional insurance companies they sell direct and do not retain a lot of premiums. They make most of their money with ancillary products and fees. According to their segment numbers, insurance only creates 20% of their profit, 80% comes from “other stuff”.

Here are two interesting bits from the IPO prospectus. First on the role and relationship of PCWs:

The Group’s contractual arrangements with PCW providers can be terminated upon one to three months’ notice and prices are typically renegotiated on an annual basis. Any change in the Group’s arrangements with its PCW providers or a termination of such contracts by the PCW providers, with or without fault on the Group’s part, would increase the acquisition costs for new and/or renewal business, which could have a material adverse effect on the Group’s business, financial condition and results of operations.

and:

PCWs’ primary sources of revenue are fees which are paid by the insurer or intermediary after a customer selects and purchases a product that has been returned in their search query. The largest PCWs in the UK by new motor insurance business volumes are Comparethemarket.com (owned by BGL Group), Gocompare.com (owned by esure), Moneysupermarket.com (a publicly-listed company) and Confused.com (owned by Admiral Group) (Source: eBenchmarkers). The Group sources the majority of its policies sold to new customers through these four PCWs.

So they are clearly dependent on the PCWs. As there are 4 large ones in the UK, this seems to be a competitive market but if there was further consolidation it could get more difficult and more expensive.

One major risk of this business model is clearly that at any point in time the PCWs could decide to integrate them further down the sales “funnel” and start selling the highly profitable ancilliary products on their own. As Hastings wons around 80% of their profits with other stuff then the core insurance, this is very relvant for them. In Italy interestingly the market leader facile.it has just started going into this direction.

Interestingly, both Admiral and Hastings have been growing quite strongly in the UK, both in 2015 and 2016, whereas the other 2 listed direct insurers, Direct Line and Esure seem to be somehow struggling with either very low or no growth.

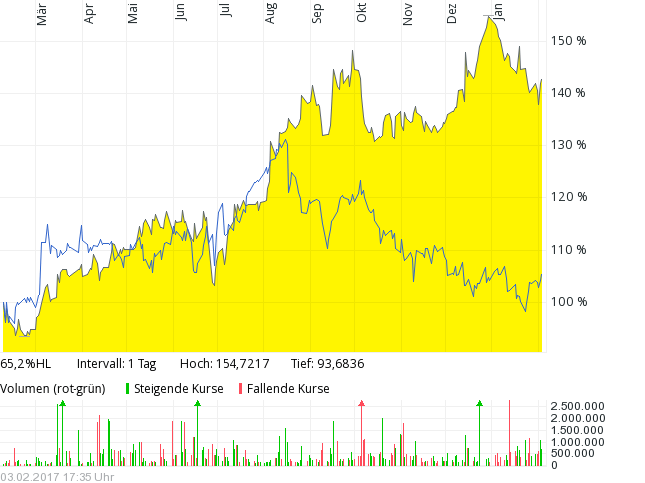

Hastings has outperformed Admiral quite significantly over the last 12 months as we can see in the chart:

I am not really sure why this was the case but most likely this is a function of the higher (top line) growth of Hastings and the projection of this growth into the future.

Pro /Con view

Positives:

+ strong growth in the UK

+ focused and lean business model

+ interesting organizational structure (retail vs. underwriting)

+ relatively good reporting

Negatives

– CEO and CFO are all hired from external, founders are long gone.

– CEO was actually a banker before (which is odd for an insurance company)

– Largest shareholder is a Goldman Sachs led investor group which is selling down shares.

– CEO and CFO pay themselves much higher salaries than Admiral directors

– not as profitable as Admiral (loss ratio is 10% higher for UK motor)

– still significant debt

– more aggressive reserving

– UK only

Reserve risk & IBNR reserves

One of the biggest issues with insurance companies is the problem, that the amount of losses a company reserves in any given year is hard to verify for any outsider. There is significant leeway either to reserve conservatively or aggressively. Especially for fast growing insurance companies, over aggressive reserving can be mitigated by an ever-increasing stream of incoming insurance premium until that stops.

A prime example for this was for instance FBD Insurance from Ireland which I covered last year. Everything looked good for a couple of years, the company was growing and gaining market share, but then the Irish market turned and BOOM…..

A special case within the opaque insurance reserves are the so-called IBNR reserves, which stands for “incurred but not reported”. This category has to be used especially then towards the end of any reporting period when you know that accidents have happened and you will very likely receive a claim in the future, but it has not been reported yet.

As information in such cases is not very good, there is a lot of leeway to set those reserves. Conservative insurance companies use this category to manage and smooth their profitability. So in good years one will see higher IBNR reserves, in bad years those reserves will go down and turned into profits.

This is a quote from Hastings annual report with regard to IBNR reserves:

Estimating the reserves required for claims incurred but not reported (‘IBNR’) to the Group involves significant judgement and the use of actuarial and statistical projections. This includes whether any of the larger bodily injury claims will result in any periodical payment orders (‘PPOs’) which are payments made periodically over several years or even the lifetime of a policyholder. PPOs and potential PPOs increase the complexity and uncertainty of the estimation of reserves due to the increased range of assumptions required. There is a risk of misstatement of IBNR liabilities due to the claims data, a key input to the reserving process, being incomplete or inaccurate

So they clearly acknowledge that judging those reserves is difficult. WHat I find interesting in Hasting’s case is the following:

For some strange reason, the percentage of IBNR claims ceded to the Reinsurer is much higher than for the normal reserves. Hastings has a 50% Quota share program plus an “Excess of loss” contract which means that losses ceded to reinsurers should be somewhere above 50%.

If we look at page 112 of the 2015 annual report, we can see that the percentage of ceded claims for normal claims vs. IBNR looks like this:

| 2014 | 2015 | Avg | |

|---|---|---|---|

| “normal” | 61.08% | 59.30% | 60.19% |

| IBNR | 72.73% | 69.61% | 71.17% |

So in general, they assume a 11% higher ceding rate for IBNR reserves than for the normal reserves. In my opinion this is strange. Fundamentally, the claims underlying the IBNR reserves should be similar to the normal claims and have roughly the same ceding rate than the normal reserves. The effect of this higher ceding rate is easy: It increases profits for Hastings if I assume that the reinsurer is responsible for those claims.

For any auditor, this part is very hard to audit as the reserves depend very much on Management’s judgement.

Clearly there could be an easy explanation for that but it is very hard to verify for any outsider.

Reserve quality & Management

This brings me to another point: With the IBNR example, I am just scratching at the surface of the complexities in an insurance balance sheet.

Therefore management plays a very large role when trying to assess an Insurance company. Ideally, management has a long track record and a significant long-term stake in the company.

In Hastings case, the company is run by a banker with little or no insurance track record. He seems to have some skin in the game but compared to his salary this doesn’t look too impressive. The CFO has among others worked as a CFO for a division AIG which had notoriously under reserved its insurance book

So there is clearly a risk that they have a much stronger focus on the short-term than for instance Admiral, where the founders are on board for 20+ years. Which in turn increases the risk that something similar to FBD might happen down the road, especially if they continue to grow aggresively into a “softer” market.

Summary:

Hastings clearly tries to be the “next Admiral”. So far, growth has been great and results pretty OK. However for me, Hastings is not a company I would invest into.

From the outside, their reserving looks aggressive and I am not convinced that Management runs this with the view on really long-term success. Maybe I am biased here but an Investmentbanker as CEO and a former AIG guy as CFO is not my dream combination for an insurance company.

However one has to acknowledge that they have come a long way and that they clearly don’t make life easier for my portfolio company Admiral and even less so for guys like DirectLine and Esure.

Nevertheless, for Hastings shareholders, the question will be how far they get in the UK and if they are able to make the switch into international territory before their growth fades out. In this regard, Admiral clearly has a 10 year advantage,

Hi,

Thanks for the very good article as usual.

Just wanted to come back on the IBNR % of ceded vs normal reserve and trying to find an explanation.

Do you think that this may be explained by a more conservative reserving policy for IBNR ? Because of their excess loss reinsurance contract if they over-reserve IBNR then they should have a much higher ceded ratio than in the normal reserve? And then when they receive the claim they could release some of it and the % of ceded come back because of excess loss ?

It could be one explanation, but I agree with you, I did not participate in the IPO due to the track record of the CFO and his underreserving at AIG and the fact that they were growing at the time when ADM LN said that they were “on the side line” (2013-2015)

Interestingly, PE funds still own 60% of the company today and despite the strong rally, they have not sell yet.

Nice analysis, as always. Especially the part on “IBNR % ceded” and management.

In my previous company, a big reins. IBNR size was often same size as case reserves…

Yes, reinsurance companies use ibnr reserves to manage volatility

Correct me if I am wrong. With such a short-tail business shouldn’t you see quite early if they are too aggressive?

Not as long as they are growing quickly.

Nice write-up and an interesting company. I am long Admiral too, and I often asked myself: what if I had bought around the IPO. Clearly it would have been great, BUT

In insurance I really like to look at the loss ratio development for at least 5 years backwards. That is hard to do around IPO. Did they disclose the loss ratio development in the prospect?

So, with todays knowledge: I never would have invested in Admiral around IPO (too risky) and I completely agree with your conclusion to not invest. Maybe in 5 years…

(And thanks for the info with the AIG guy, although it may be unfair to him)

Best

Tom