Special situation: Stada Arzneimittel AG – swimming with the sharks (again)

Disclaimer: This is not investment advice. please do your own research !!!

Stada is a company I had been looking at many times in the past. A business which in principle is quite good (Generics and OTC drugs) but the company was run by a long time CEO who acted as it was his own company without owning a single share. He paid himself huge salaries, employed his son in a non-sensical but highly paid job, the company afforded itself a huge corporate center and so on. As a result, the company created little to no shareholder value in the 10 years up to mid 2016. As a comparison, the 10 year return of Stada until 03/2016 was only around 1,8% p.a. compared to 7,5 % p.a. for the MSCI Europe health care index, a significant underperformance.

Then however something happened which is still very rare in Germany: A local activist investor (Active Ownership Capital) and some other funds acquired a significant stake in the company and pushed for change.

To cut a long story short: The activists succeeded in ousting the CEO (and most of his friends in the Supervisory Board) and replacing him with someone who seems to work more in the favour of shareholders. The story made some waves, among others even the Economist thought it was worth a story.

In February some rumours surfaced that Private Equity Groups would be interested in buying Stada.

The first non-binding bid came from Cinven at 56 EUR per share, followed by a non-binding offer of 58 EUR by Advent, another PE player. This was reinforced by a binding offer from Advent of 58 EUR plus dividend a few days later. and an undisclosed 3rd buyer seems to have offered 58 EUR as well.

After that, Stada decided to set up a more formal process and agreed to open its books in order to maybe get an even higher offer. In the following days many other rumors came up, such as Permira and Bain Capital would be interested plus some Chinese buyers as well (well, there are always Chinese buyers these days…).

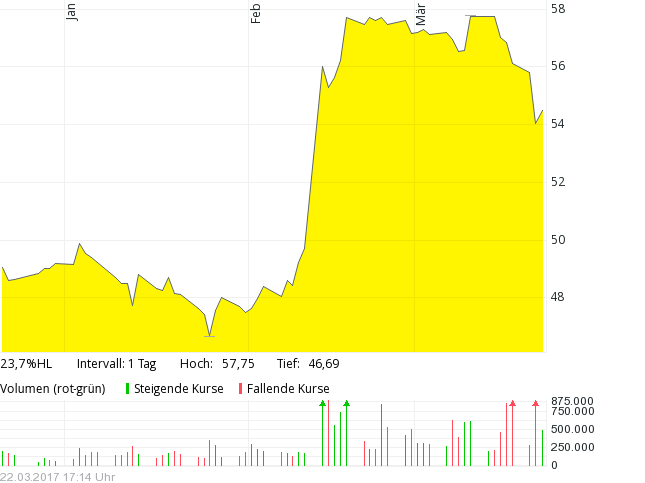

If we look at the stock chart, at first everything went according to plan and the stock price was slowly approaching 58 EUR:

But then in the last few days the stock suddenly dropped. What happened ?

2 things basically:

First, end of last week, Stada cancelled scheduled meetings with the current bidders at short notice.In the news it was speculated that they want to give more time for a 3rd bidder to come up with an additional offer. The official statement was like this

STADA confirms current media reports that the expert sessions which were planned as part of the structured bidding process have been postponed based on the decision of the Supervisory Board. The Executive Board and the Supervisory Board mutually agree that the indicative bids do not yet reflect the fundamental value of STADA. Thus, the company, for the time being, wants to provide the bidders the opportunity to increase their offers. STADA objects current media reports that the delay in the process is aimed to make another committee composed of a private equity company and a strategic investor enter the process.

This cost around 2 EUR in the share price as some investors thought that this also could mean something else.

Funnily enough, the very next day they increased their 2019 forecasts significantly.

- Significantly increased adjusted EBITDA target 2019 at Euro 570 to 590 million (previously: approx. Euro 510 million)

- Increased adjusted Group sales target 2019 at Euro 2.650 to 2.700 billion (previously: approx. Euro 2.600 billion)

- Adjusted EBITDA margin of about 23 percent expected mid-term

Then, as another surprise, beginning of this week Stada announced that they will not release their final 2016 numbers on Thursday this week but postpone it because of a “single digit million EUR issue” they need to still clarify. This again cost around 2 EUR in share price. Again the official release:

Bad Vilbel, March 21, 2017 – Today, on March 21, 2017, the Executive Board of STADA Arzneimittel AG informed the public that the press and analyst conference on full year figures 2016 have been rescheduled to Wednesday, March 29, 2017.

The reason for this decision is the fact that in the process of the consolidated financial statements a reassessment of a transaction was undertaken. This reassessment will be aligned with auditors before closing the consolidated balance sheet. The reassessment regarding consolidation matters might result in an impact on adjusted EBITDA in the mid-single-digit million euro range and in an impact on sales in the low double-digit million euro range. In total, the Executive Board does not expect any material changes in the full year figures 2016. Guidance for 2017 remains unchanged.

So where are we now ?

At the time of writing we have a stock which trades at 54,40 EUR where we have a binding offer from one party at 58 EUR plus dividend (0,70). We might see a potentially higher bid or for some reason the whole process falls apart and the stock might go down. The 3 month average before the bids surfaced was around 49 EUR per share which I would use as the “undisturbed” basis price.

I would make the following assumptions /scenarios

I do think that the probability of a deal happening is higher than 50% but not 100%. To keep it simple I would assume 75%. Within this 75%, I do think there is a smaller chance to get more than 58 EUR plus dividend. I would assume with a 25% probability we get 60 EUR plus dividend.

This leads to 3 scenarios:

Scenario 1 (25%): Deal fails and I lose -5,4 EUR or -9,9%

Scenario 2 (50%). Deal closes at 58 EUR plus 0,70 dividend and I earn 4,30 EUR or 7,9%

Scenario 3 (25%): Deal closes at 60 EUR plus 0,70 dividend and I earn 6,30 EUR or 11,6%

Weighted by the probabilities, this gives me a ~4,4% expected return for a relatively short period of time (3 months ?) which looks attractive.

Clearly the loss could be higher in scenario 1, but I think it is very clear that even if this process fails, at some point in time buyers will come back like in the Syngenta case. So I think the downside is really limited here. One of the big advantages is clearly that there won’t be any big issues with any regulatory approvals unless the highest bid would be from a strategic Chinese buyer. Plus, the PE buyers execute quickly which we saw in the Sapec case.

Summary:

From a return/risk scenario Stada is somewhere between Sapec (higher uncertainty, more potential return) and Actelion (high certainty, lower potential return). But still I think it is very attractive and a pretty straight forward case. In the current environment I also prefer a higher exposure to “special situations”. So I decided to invest 5% of the portfolio into Stada at the current price of 54,40 EUR per share.

Be cautious: This is shark infested territory

One word of caution here: Stada is a relatively well known name and the story is well published. So one should not assume that this is “easy” money. Rather this is a case of “swimming with the sharks” as one can assume that many professional players look into this and the discount really includes some kind of risk. I still think it is worth the risk but one should be aware that more “hiccups” are very likley. The price of Stada will most liekly not go up in a straight line to 58,70 but go up and down depending on many rumours. If you can’t stand this (like some readers in the Actelion case), don’t do it.

Again a disclaimer: This is not investment advice, PLEASE DO YOUR OWN RESEARCH

If someone did not tender it’s now good time to sell I think 🙂

Now that the tender was successful, people will play the “back-end” play. I think mid 70ies could be realistic for a squeeze out.

Oops, CEO + CFO (have to) resign!

https://www.bloomberg.com/news/articles/2017-07-04/stada-supervisory-board-said-to-discuss-replacing-ceo-wiedenfels

Seems to be something cooking…

Financing still active and acceptance threshold seems to be lowered to launch another bid soon?

http://mobile.reuters.com/article/idUSL8N1JQ4RI

Wie sehen Sie die neue Situation bei Stada und bleiben Sie bei Ihren Szenarien?

I will reconsider after my vacation. No need to hurry in my opinion.

It did not went through. Stock will fall tomorrow 😕

https://www.google.de/amp/amp.handelsblatt.com/unternehmen/industrie/milliarden-angebot-von-bain-und-cinven-die-stada-uebernahme-ist-gescheitert/19983650.html

Yes i have seen it. Should habe sold when aoc sold….

But i guess “it ain’t over until it’s over”

Das glaube ich auch. Soweit ich weiß ist das Problem jedoch das Bain + Cinven jetzt 1 Jahr lang kein neues Übernahmeangebot unterbreiten dürfen.

Die Sperrfrist von einem Jahr kann man umgehen, wenn der AR einem neuen Angebot zustimmt. §26 WpÜG 😉 (1) ist die Sperrfrist und (2) die Befreiung von der Sperrfrist

Ansonsten stünde die Aktie auch nicht bei 59 Euro. Da kann man ja kaum was gewinnen, falls das Angebot doch noch durchgeht

Bei rhoen und celesio hat es auch nicht gleich geklappt. Aber logisch ist jetzt “blut im wasser”.

According to Börse Online it could be the 27th until some new information about the deal closed or not will be released. We have to be a little more patient…

http://www.boerse-online.de/nachrichten/aktien/Stada-Aktie-Uebernahme-droht-zu-platzen-Was-Anleger-jetzt-wissen-muessen-1002118741

still no final count. at 12:30 yesterday, only 45% were tendered:

http://www.niddahealthcare-offer.com/websites/1006_ma/German/1900/news-detail.html?newsID=1631704

Will be close. But this morning there was a movement from 62.6 to 63.3. Could mean that something was leaked. Let’s see. Thank you as always for the great investment idea.

Maybe the downside is lower than many investors thought ?

Maybe the Chinese will return to the table ? With a slightly higher price or a lower acceptance level ?

This will be an interesting day tomorrow:

*BAIN, CINVEN: STADA-OFFERTEN-AKZEPTANZ 41,38% ZUM 21. JUNI

If you had to make a bet, what would you guess?

I think they will make the 67%. Rationality prevails!

I would think so. Anything else would be quite embarrasing for all parties involved.

45%… this morning. Slight increase.

http://mobile.reuters.com/article/idUSF9N1II014

isnt it better to sell the untendered Stada shares and buy the tendered one instead

It depends: If you think the acceptance will be very high, there will be a squeeze out speculation at a higher price that will benefit the untendered shares. Hence, a “premium” makes sense. With the tendered ones you get your money back earlier (if it works). My money is on the tendered ones. I like the risk/reward here.

Full disclosure: I tendered all my stocks as of today into the offer. There might be a chance later on to play the squeeze out.

Do you have any worries about a fail of the offer at all?

Only 21,50 % were tendered on 07. Juli.

Great that you now about the numbers of july….

oops, june of course

Aktuelle Annahmequote: 21,50 % (Stand 07. Juni 2017, 12:30 Uhr MEZ)

I have no specific insights. But normally, most institutional investors will only tender on the very last day which now would be the June 22nd.

Well, we will see.

Here it comes the counter bid at 70€!!

http://www.reuters.com/article/brief-advent-shanghai-pharma-said-to-con-idUSFWN1IH15B

Luckily I have not accepted the previous offer at 66€ yet.

Congratulations for the great discovery!!

thanks for the link. I will believe it when I see the offer…..

just one remark: As long as you keep your shares, it would not have hurt to accept the “old” offer.

As I have suspected, the offer was not for real….

http://www.handelsblatt.com/unternehmen/industrie/stada-bain-capital-und-cinven-muessen-wohl-keine-gegenofferte-aus-china-fuerchten/19851004.html

Should have sold at 67 EUR….

New offer from Advent? Stada SP > 67 EUR/s. Already handed my shares in.

No comments on Atlantia / Abertis ?

WHat’s your comment on this ?

There is little clarity. Both companies have significant political risk, specially Abertis with upcoming referendum in CAT. However governments in the mediterranean countries have little resources for public infrastructure, and continuity of toll roads seems granted for decades regardless on the political landscape.

Both companies seem compatible for their business, management style and geographical footprint: combining them potentially makes sense. Merger should bring no big issues from regulatory authorities, competition principles applied in other cases should not apply here.

I would expect Abertis shareholders to ask for an extra premium (5-10%) to current prices, (there is some margin in the current P/E, and potential savings/synergies) …. but the fact that current Abertis price is below Atlantis’ offer, reflects the uncertainty about the deal…

Congrat. !!

66€/ share

http://www.finanznachrichten.de/nachrichten-2017-04/40404080-stada-will-sich-von-finanzinvestoren-bain-und-cinven-uebernehmen-lassen-016.htm

wow, more than I hoped for. A lucky “easter egg”….

Well done !

Congratulations!

Reuters says deadline is Friday

http://de.reuters.com/article/deutschland-stada-idDEKBN17710W

yes, but that obviously doesn’t mean that they need to disclose anything.

Final bids due tomorrow – bids from 4 PE groups to now 2 PE groups…and Shanghai Pharma rumoured to be part of a consortium…hows everyone feeling about tomorrow???

I don’t think that there will be any news tomorrow, but who knows ?

only a side Information to Stada, but it seems that AOC is already “on the hunt again” and purchased a week ago a 5% stake in PNE Wind – also a company with a lively, interessting management history.

I have no idea about the Team size of AOC, but it seems that they have (now) the Management power available to start the next “active ownership”.

where did you get the information from? I think this is a “fake news”.

This has been released via WPHG on March 23rd. So no fake news….

I have read the Manager Magazin article. Very interesting. The Advent 4 day binding offer seems to have been a tactical move in order to kick start the formal bidding process.

where in the Manager Magazin article do they insinuate the Advent offer was a “tactical” move?

Towards the end of the article (page 64, second last column). They say that Rajan Sen from Advent decided to make a “tactical move” (in German: “zu einer taktischen Finte”) and issue a binding offer which is valid only 4 days. They knew that the offer would not be accepted. But the Supervisory board then had to formally open a sales process, otherwise they all could be sued by the sharheolders.

mmi

This could cause another hickup: Stada COE’s car has been wiretapped last year according to Manager Magazin:

http://www.manager-magazin.de/unternehmen/handel/stada-chef-matthias-wiedenfels-abgehoert-a-1139905.html

The “€58 + dividend” offer was valid until “February 27, 2017, and subject to the approval of the Company’s Executive Board”. I take it that this offer is no longer binding…

Good point. Need to check on this one. Where do you got this information from ?

Adevnts press release does not include this date:

https://www.adventinternational.com/advent-international-submits-binding-offer-for-stada-arzneimittel-aktiengesellschaft-to-stada-management-board/

https://www.stada.com/investor-relations/investor-news/detail-view/news/detail/News/stada-arzneimittel-ag-informs-about-receipt-of-binding-conditional-take-over-offer.html

ok thanks. Hmm, they submitted an offfer on February 23rd which was only valid 4 days. I kind of understand that Stada seems to play for a little more time in this case.

The stock ran up from 35 euros to 50 on speculation of a deal– so one could argue the break price is actually far lower than 49. The activists got involved last summer 2016. I have traded this but am not in it right now, feels like the company may be getting greedy and could ruin it for everyone? I do not know, hopefully it works…

well, one could also argue that the stock ran up because they now have much better managment (and board) than before who will remain even without a deal.

We will see….

There is a lot to be improved with regards to margins…but as you’ve highlighted the story is well known and I agree that the unaffected is a bit lower than EUR 49.

Some of my checks suggest that this reporting “delay” is just to allow for a 3rd bidder to emerge…have also heard that 2 parties have already dropped out.

Its an interesting situation but I feel like the rumours of Stada mgmt pushing for EUR 70 are a stretch – hard to justify the LBO math given sluggish top line.

Also – always remember who you are in bed with. This name is well picked over by pre-event / merger arb players – the stock is down ~5% MTD and a few have already been burned…could see some more de-risking…which could provide a better r/r

yes, that is clear. There could be more “hickups” on the way….

Agree with your logic on this one – but don’t you think will always trade with a bit of a spread given PE buyers / LBO contract? Wish there were more strategics involved. Have not been able to speak with any PE firms that passed, but would love to hear rationale as it seems everyone is showing up for the “gangbang”.

Also – I think undisturbed is a bit lower as this has been shopped for some time. Strategics would likely be attracted to OTC biz and PE would look at generics…but we all know pressure generics have been under.

yes, clearly this will trade at a spread until (and if) the transaction actually closes.

I think the “strategics” are hesitating to some extent because they don’t want to get heir hands dirty with the required cost cutting and seperation of OTC and generics. This is the service the PEs happily will provide for a “modest” fee…