Italgas SPA (ISIN IT0005211237)- follow & SELL

People who follow my blog for some time know that timing of purchase and sales of stocks is not one of my strengths. I usually buy too early and sell too early. Italgas is one of the very rare exceptions:

When I looked at Italgas and then bought it end of November, I really managed to buy at or very close to the absolute low after the company had been spun off.

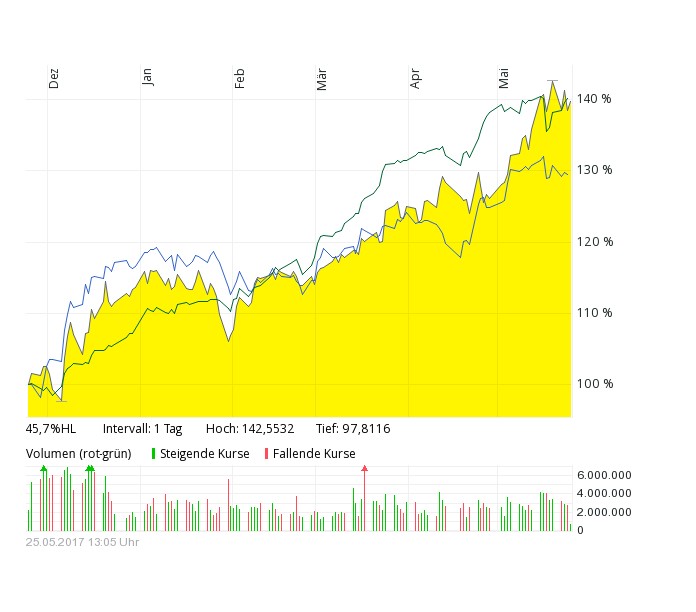

Looking at the stock chart we can see that Italgas outperfomed the broad index (lower blue line) but mostly mirrored the Italian small cap index with a slight outperformance if we consider the dividend which was paid early this week (0,20 EUR/share).

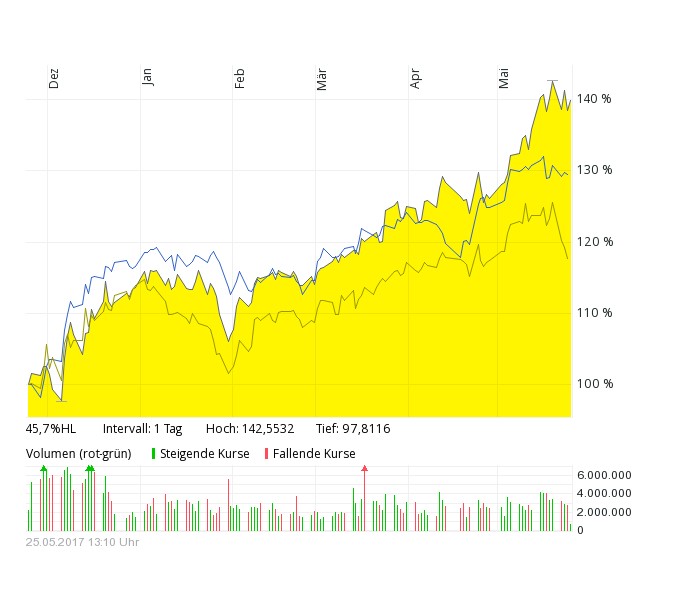

A second comparison shows that it looks like that Italgas performed better than its former parent company SNAM which itself underperformed (lowest line):

So I do think that the overall increase of around +50% can mostly be attributed to the overall recovery of the stock market and not to an individual development of Italgas or to the fact that it was a spin-off.

How did the business develop

When we look at the 2016 result presentation one can note the following points:

- guaranteed returns decreased by 0,6% – 0,8% but still above 6%

- net debt amounted to 3,6 bn (slightly lower than my estimate)

Q1 2017 looked surprisingly good with revenue up +9,8% and Profit up even +16%. Debt further decreased to 3,5 bn EUR. That looks good but clearly 2016 was not a good year for Italgas.

Unfortunately they do not disclose the regulated asset base (RAB) in the presentation which was the basis for the investment case and ist the benchmark for the valuation.

If we assume that the regulated asset base remained at around 5,9 bn EUR, debt is at 3,5 bn and market cap 3,75 bn, the current EV multiple would be around (7,25/5,9) ~1,23 times.

What to do now ?

This is what I wrote last year:

On average, such assets have a private market value anywhere between 1,0 and 1,5x RAB (based on EV).

For Italgas, the RAB is 5,9 bn EUR (5,7 bn direct, 0,2 indirect).

The current valuation a 3,15 EUR/share looks as follows:

Market value: 2,5 bn

Net debt: 3,7 bnEV = 6,2 bn or around 105% of the RAB.

So Italgas is clearly trading at the lower point of potential ranges.

A Valuation at the top of the range (1,5x) would mean around 8,9 bn EV and ~6,37 EUR per share. The middle of the range (1,25x) would be 4,54 EUR per share. At the lower end (1xRAB), the stock price would be ~2,72 EUR per share.

So we now reached the mid-point of the valuation relatively quickly, including the dividend we are now already above the base case.

At the current stage of the process with regard to regulation, I do not think that Italgas should trade at a premium because as I described in the post, there are significant uncertainties.

On the other hand, one could also argue that maybe one should ride the positive momentum a little bit more. Despite the negative press about Europe and the Euro, fundamentally things look better.

However, I bought Italgas as a special situation with a countercyclical aspect and not as a speculation on the Italian recovery. A quick recovery might be even not so good for Italgas, because then there might be significant more interest for the ubcoming auctions.

I also think that if one wants to bet on an Italian recovery, financials would be the more interesting play.

Clearly Italgas could go up further, especially as still lots of money is flowing into “infrastructure assets”, but for me it is clear: I will sell Italgas at current prices until the end of the month and realize the quick (and lucky) gain of around +53% including dividend.

Hope you did not sell yet (specially not on the 29-30. May)… unless you wanted to extend your legend…

If I say that I sell, I sell. And yes, that’s part of the “legend”. Buying too early and selling too early explains most of the outperfomance 😉

oh no!

…you are seriously funny sometimes..

😀

A nice write up V&O. I enjoy reading about spin-offs, they often seem to have a good potential to out perform their parent company. Better to stick to your thesis than speculate about further gains…

don’t sell, simply put into your brokers account a trailing stop loss and ride the chart further up, unless you feel that the prices will collapse in the summer doldrums.

that would be an alternative….but I also need some cash to increase my Sapec position 😉

Beyond putting a stop loss, there should also be a sell order at a target price, defined by (eg) the upper level of P/BV.

Would Romgaz after the recent increase in price would fall into the same bucket? The P/BV there is around 1.2 at the moment.

hmm, at Romgaz I am not sure. I have already sold out (too early9. Romgaz is less about regulated assets though.

Well done, and great article and analysis as aways