Spin-off/IPO updates: Metro/Ceconomy, Brighthouse Financial, ALD SA

Metro/Ceconomy

I had briefly written about the Metro/Ceconomy Spin-off in January. After some legal hassles, the spin-off took place last week last.

This is what I wrote back then:

With 327 mn shares outstanding, this would translate into ~6,20 EUR per share as a lower bound value for Ceconomy under my (very rough assumptions).

It think at or below this price, Ceconomy could be an interesting “Ugly duck” spin-off investment.

Interestingly, Ceconomy had a very good start, opening around 9,40 EUR and has gone above 10 EUR per share, far above my buying threshold.

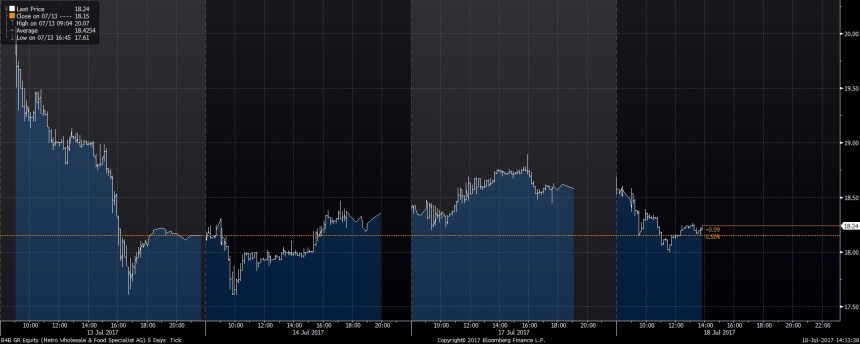

Even more interestingly, the “good business”, the Metro Cash & Carry opened at ~20 EUR but then dropped quickly to a low of around 17,70 EUR as we can see in the chart:

This lead to the strange effect that the 2 parts at the end of the day were worth around -10% less than on the day before. The reason in my opinion is most likely technical selling pressure from Index investors. Ceconomy, the smaller part remains in the MDAX, whereas Metro C&C as the spin-off for the time being has dropped out (but is expected to get back in September).

Interestingly, the CEO of the spin-off announced that he bought shares for 1 mn EUR on the second day.

For me this led to a change in plans: Instead of buying the “ugly part” I bought a 3% position at ~18 EUR per share in the Cash and Carry business which in my opinion looks quite attractive (at an estimated 9x EV/EBIT).

Another observation: Although the Metro Pref shares always traded at a discount before the spin-off, after the spin-off, both pref shares (Ceconomy and C&C) trade at a small premium to the common shares. Doesn’t make sense and I cannot explain that.

Metlife/Brighthouse Financial

With record day tomorrow July 19th, MetLife, the US insurance giant will spin-off its retail insurance subsidiary named Brighthouse Financial. The reason behind the spin-off is mostly that Metlife wants to get rid of their “systemically important” designation plus the fact that the retail business is not deemed overly attractive.

It will be interesting to see how that Spin-off performs, as again, index investors might need to sell and the business in general is not at the top of the list of most investors.

The P&L for the current year looks ugly, which clearly doesn’t add attractiveness. On top of that, the company has significant exposure to Variable Annuities which could be problematic in adverse market scenarios.

Voya Financial, the former ING subsidiary is the closest comparable stock, so it will be interesting to see if Brighthouse trades at a discount or premium to Voya. If Brighthouse trades down to a relative discount, it could become interesting as a potential “ugly duck” spin-off opportunity.

ALD SA

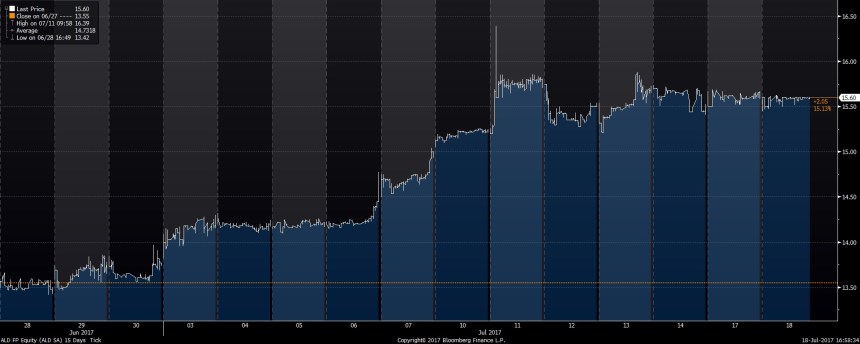

Without big advertisements, SocGen, the French bank IPOed 20% of their car leasing arm ALD a few weeks ago. Interestingly the offering didn’t go well and had to be priced at the lower bound of the initial range (14,20-17,40) at 14,30 EUR.

The stock then lost further and only recovered more recently as we can see in the chart:

I haven’t looked deeply into the company but a trailing P/E of 12 looks not too expensive for instance compared to Sixt Leasing which trades at 15,5x trailing earnings.

2 years ago, Credit Agricole did a similar structure with Asset Manager Amundi which has performed very well since then.

Maybe time to revisit the ugly duck Ceconomy now?

Significant Assets:

150 M€ stake in Mvideo (15%)

330 M€ stake in FNAC darty (~25%)

280 M€ stake left in Metro (6,39%)

This alone covers ~70% of the current market cap of Ceconomy (1,1 bn€).

On top comes the operating business which is in trouble but still profitable, FCF was quite ok last year and they are still going for 400 M€ EBIT next year. You have previously estimated an EV of 1,9 bn € for the operating business (based on the 400 M€ EBIT less the minoritys), which might overall be too optimistic but there could still be some value here…

Hmm, i am not such a fan of “cigar butt” investing These days.

Metro is FREE FALLIN’ … https://www.youtube.com/watch?v=rqDq3eyTGck

Is the Metro investment thesis still intact? Worrying continued share price fall!

I am a bit worried too… maybe we got it wrong and should have recalled Terry Smith’s points on Tesco: focusing on actual value creation (ROCE-WACC) the attractiveness of Metro is low. ROCE seems to be 10.6 % (*) and WACC is ~ 8.0% (#). probable little value creation…. Recalling TerrySmith, low value creation should be a long-term indicator of share price evolution…

Maybe the market is more concerned about the value creation, rather than METRO’s cheap valuation (EV/EBITDA basis)…. :-s

Hopefully the reported RoCE and WACC (~Cost of Finance) are correct…

(*) pg.51 in http://www.metroag.de/~/assets/metro/documents/financial-statements/2016-17-metro-annual-report_en.pdf?dl=1

(#) http://reports.metrogroup.de/2015-2016/annual-report/combined-management-report/economic-report/earnings-position/value-based-management.html

^ I acknowledge that the cost of debt is very low (2.4%), … but this seems to have no influence

hmm, for a real estate intenisve business, the value creation looks ok (without having verified the numbers). And of course the hope is that after the separation, things become better. On the other hand, they earn most of their money in Russia and Turkey. Which at the moment is a problem.

Separation? Are they separating again? I did not know…

Anyhow, 2.5% value creation is very low, specially wrt to alternatives… Should they keep the Wholesale distribution alone (RoCE 15+ %), then things would be nicer indeed (Still not optimal!)… If you suggest that in the pipeline there is a Real / WholesaleMetro separation, I think that is indeed the way to go… but I am not aware of such.

Oversold or time to give up and sell? Another one for the “mistakes” list. My averaging down has cost me a 3% portfolio hit!

I don’t think you can argue like that. WACC of 8% with cost of debt of 2.4% implies already 5.6% belongs to shareholders. If you want to know if growth is good or bad you need to consider the Return on Incremental Invested Capital and see if it is above WACC. But all of this is kind of wacky anyway if you think the business becomes better. This would imply high ROIIC and therefore over time higher ROCE. That’s what MMI is expecting, if I am not mistaken.

Indeed assuming that the 5.6% difference is value earned by shareholders is totally wacky… Experience confirms it…. My concern is that the difference ROCE-WACC is very narrow, and only if increased, value would be created impacting long term the share price / value of the company.

Metro: Russian LFL of -9% does not look good. Everything else they published is not that bad, I think.

Metro already started the ski season going downhill … Any idea where is it heading to ?

What is your opinion on the investigations concerning insider trading against CEO and board director at Metro?

Doesn’t paint a nice picture quite honestly…

I just know what is in the news. The CEO however is not part of this investigation to my knowledge.

You are right, it is the COO.

aktuell entwickelt sich der “ugly Part” Ceconomy wesentlich besser als Metro Food. Heute mit Zahlen

http://www.finanznachrichten.de/nachrichten-2017-10/42044567-dgap-news-ceconomy-ag-ceconomy-mit-solidem-vierten-quartal-prognose-fuer-das-gesamtjahr-bestaetigt-deutsch-016.htm

Gute Beobachtung. Bislang aufs falsche Pferd gesetzt 😉

Ich auch…

Laut Medien-Berichten prüft Metro einen Rückzug von der Börse.

http://www.manager-magazin.de/unternehmen/handel/metro-olaf-koch-prueft-rueckzug-von-der-boerse-a-1169095.html

Danke. Metro hat schon offiziell dementiert…….

Metro back in MDAX soon.

http://www.finanznachrichten.de/nachrichten-2017-09/41640350-index-monitor-metro-und-grand-city-properties-steigen-in-mdax-auf-016.htm

Adding up the balance sheets for Ceconomy and Metro Wholesale leads to confusing results: I find that the combined Goodwill (and consequently the equity) is now almost 2bn€ lower than before the spin-off.

Can anybody make sense of that? The demerger report reads to me as if assets were transferred to Metro Wholesale only at book value. In consequence, even the “true” P/B-ratio for Metro Wholesale could be much lower than it now appears.

I think P/B is not a very good measure for Metro (and most other stocks…)

Metro Q3: https://www.metroag.de/mediacenter/termine/2017/08/31/ir-conference-call-q3-2016-17

my conclusion reading and listening: numbers OK, analysts especially interested in russian-business outlook and real estate.

add-on: the for me rather surprising drop in price today seems to be related to the bleak numbers and outlook of the French competitor Carrefour.

However, the French Metro + acquisition in France seemed to work quite well (Ceo mentioned successful 100 day plan, without providing specific details / numbers).

any other thoughts / views / conclusions?

I see it the same way- The numbers look ok, even Real was doing somewhat better.

Wondered if you had any updated thoughts on Brighthouse financial? I see the shares have fallen a bit, but am yet to look at in detail. No worries if you haven’t either.

Ich park es mal hier rein:

MDAX reentering

“Die nächste reguläre Index-Umstellung findet zum 18. September statt. Etwaige Änderungen in den Indizes DAX, MDAX, TecDAX und SDAX wird die Deutsche Börse am späten Abend des 5. September bekannt geben.”

http://www.finanzen.net/nachricht/aktien/index-monitor-im-september-werden-mdax-und-sdax-aufgewirbelt-ansonsten-ruhig-5619924

BHF: Nicely, quietly collapsing…

Hi MMI,

I think there are a few issues weighting on the price:

1. Real. Capital intensive + lower margins. I think part of their margin problems is from higher than average salaries (something they are working on) plus separate corporate headquarters (working on it too). On the prospectus they say they could sale the business if restructuring doesn’t work out. On the other hand, I think 3% margins are not that bad considering who they are competing against (Aldi, Lidl, Edeka and Rewe have a combined 85% market share, vs. Real’s 6%). As a reference, they sold their Real operations in Eastern Europe three years ago for 1 billion euros (7-8x EBITDA assuming 5-6% margins there).

2. German Cash & Carry margins. They’ve had negative EBITs for the past years, but restructuring seems to be on track and they expect to get positive margins next year.

3. Russian Cash & Carry margins. This is a huge part of their EBIT contribution, where it margins in the low teens until this last year, where pricing pressure has increased and they’ve been forced to cut margins. I think they’ve reinforced their long-term competitive position, actually.

4. Metro Wholesale keeps all the debt (and the assets) of the former Metro. “Nice” debt schedules plus fixed interest, so it shouldn’t be a problem.

5. Debt levels are (according to my numbers) 25-30% higher due to seasonal reasons (working capital). Full year results should bring debt levels down.

Therefore I think most of the factors are non-structural and the business should be worth 20€ easily, assuming they maintain sales, 3% EBIT margins long term (5% EBITDA + 2% capital intensity) and a 40% tax rate.

One of the things I don’t seem to grasp is the tax rate. I just take it as a given, I guess. Metro pays regularly 40% of its PBT in taxes. How come it has such a high tax rate? Anyone? Thanks in advance.

German corporate tax typically is above 30%, but could be that they have impact of other tax levels wherever they operate… Or maybe bribery payments is considered an uncontournable tax… 😛 …

Hi, thanks for the comment.With regard to tax: It could be that they have non tax deductable losses somewhere. So gross taxable income is actually hihger that stated PBT and this could explain the high tax rate on stated PBT.

Dear MME, many thanks as always for the interesting post. Would you have also a target price at this stage for this investment position? .. or will you maybe just wait the next earning report to make yourself an idea?

no target price but i do think that 20-30% upside witinh 2-3 years is not unrealistic…

ALD seems really interesting. Good company, nice prospects.

They claim to be #3 worldwide. Do you know who the other top 2 are?

https://www.societegenerale.com/en/ALD-automotive/business-model

Being hosted by SG secures good financing terms, although debt and interests are raising. It will be good to track if CF improves.

I will keep reading.

Thanks for your post

The other 2 are Element Fleet and LeasePlan.

Of course, debt is rising when they finance more cars than the year before.

A steel manufacturer also needs more iron ore to make more steel (usually).

I expected Metro(b4b) to drop once again today. And MMI getting very excited about it, driving him on yet another shopping spree… for more B4B ! hihihi

Note: no comments in the two new posts allowed

thanks. Somehow WordPress has changed the default settings…

Simple question: Which WKN do you buy? BFB001 or BFB002?

I only buy the common shares (001).

Bought one more tranch of Metro. 6,4% of portfolio. Let’s see if this was a wise decision 😉

Houraaaa !!!!

By the way, Metro seemed to have anticipated a fair equity value of 8.9 bn € for the wholesale & food division, see the english joint demerger report on pages 93 and 95. Another hint that 50% upside is not all that far fetched.

???

I’ve read in the joint demerger report, that Metro apparently hired an audit firm to value the MWFS division – if you compare those results (8.9 bn €) to the current market cap (~6 bn €), the division could have an upside of 50%.

11.5% fall accumulated since demerger. Is all this explained by technical sale by index – tracking investors, or there is stg else?

I don’t know. There was no fundamental (bad) news since then.

Probably the new Metro MWFS getting rated at Ba1 by Moody’s, makes for some pronounced selling by index-trackers… Despite its stable outlook, Moody’s also expects strengthening in the next 18-24 months… Yet, index trackers follow actual ratings, not expectations… hence the pronounced selling.

Any other insights would be welcome! 😉

Interestingly, in Bloomberg one can see 3 Hedgefunds being short Metro Wholesale (in % of marketcap):

Hengistbury -1,02%

Pelham -1,11%

Marshall Wace -1,39%

Pelham & Hengistbury are also short Ceconomy but to a smaller extent.

Maybe they play the spin-off from both sides ? First the way down and then back up ? Interesting.,,,

According to Bundesanzeiger additional short positions for Metro AG (???)

Citadel Europe 0,51%

Pelham another 1,84%

I guess Metro AG is now Ceconomy….

So far, there were roughly 25 Mio. shares (of 360.121.736 shares, plus 2.957.517 preferred shares) traded on Xetra. According to comdirect, the vast majority gets traded in the final auction which appears to me kind of funny.

It is important to point out, that Metro is not all C&C. The Real-Stores do not seem not very well-run, compared to their competitors. Also many of these stores are rented in shopping-centres that were build in the 90s. It will beinteresting to see if their costs for renting go up (in the locations also desired by their competition) or if they decrease rental space (and revenue) once lease-contracts expire.

yes, that is clear that Real is not a “beauty”.But even if I assume 0 value for Real (which might be optimistc ?), I still think that the stock could be significantly undervalued. If you look at Osram for instacne, there the soin-off has really “unleashed” a lot of energy. If something like this happens at Metro, this could become very interesting.

Yes, I would agree. If you look at the egos that were involved (for much too long) separation is a logical step.

But the pockets of Kaufland (Lidl), Edeka and REWE are quiet deep. Real has to invest heavily to keep up in the fierce German retail-market. Metro C&C seems to be in a better position, although some of their high-margin products might be harder to sell in the future given the price-comparability through e-commerce.

Note: REITs with activities in Germany and focusing on Commercial renting space are showing quite good business figures; rents they get are quite generous, I guess. For REAL, if prices commerical rents are already competitive, I cannot see big risks in their rents increasing (even if interest rates increase a bit)

Bravoooooo !!!! 😀

On a first glance the growth since 2011 from ALD (page 9) looks very impressive. are you planning a article on them?

http://www.aldautomotive.com/Portals/international/Documents/2016%20Annual%20Report.pdf?ver=2017-03-22-181220-713

I am also waiting for Metro Cash & Carry, but not yet study thoroughly. Maybe you can also take a look at another recent spin-off, Cars.com in US. It`s auto-buying information website, like Auto Trader in UK. It drops a lot recently, which makes it EV/EBITDA at 9.5x, a lot lower than peers.

thanks for the comment. I think I accidently disabled comments on that post until one hour ago………

Yes, i want to look more into ALD. “Specialty finance” companies are clearly interesting.

Wow, no interest from your readers. That increases the likelyhood of the ideas performing well. 🙂

Do you think about doing more work on ALD? I started and I like what I read so far.

It’s probably not the strongest model I have ever seen, but I think there are true advantages for corporate customers beyond optimizing their balance sheet (i.e.lower costs).

http://www.aldautomotive.fi/en/for-customers/service-leasing/production-vehicles

They are the largest European multy-brand and should have certain scale benefits.

What I also found notable in the prospectus is that remuneration is quite modest (not banking style at all).

Interestingly they booked a 15m provision in 2015 after the VW scandal broke (80% of their fleet are diesel cars). A year later they reversed 14m thereof.

.

bought soem more (0,5% of portfolio) today…..

What’s the intrinsic value of the C+C share today?

No idea. What do you think ?

I think it’s looking like another Majestic

Which means what exactly ? I still like Majestic. If you mean that B4B is not a +50% in 6 month trade, you could be right.

Maybe not a 50% in 6 month… but maybe a +10-15% in 3 months if selling pressure from Index investors gets reversed when MetroC&C makes it back to the index (specially if you bought in a lucky dip… today at 17.3 !). This is kind of pseudo-timing the market. (same may happen during buyback periods with the buying pressure, but I guess MMI will bring up some objection to that!). Wait & see.

I see a 30-50% upside fwithin 2-3 years. Short term, a lot will depend on pure luck 😉

increased position to 5,2% of portfolio.

Hourraaaa !

now 5,6%…should be enough for now 😉