Cars.com (CARS) – Interesting spin-off opportunity ?

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

![]()

Cars.com is a recent (May 31st) spin-off from publishing company Tegna, which itself is a spin-off of the Gannet publishing Group. Interestingly, Gannet/Tegna only bought control of cars.com in 2014 for a total value of 1,8 bn USD.

Cars.com – The business & Market

Cars.com is a typical “Online classified” business, meaning that it collects offers of merchandise (in this case cars), aggregates and sorts them and then shows it to as many potential customers as possible.

The economic value of such a “service” is relatively easy to explain: For a potential customer, it saves time because he can look at and compare different offers at one place. For the sellers, such a service is basically an advertising and/or sales channel which ideally reaches many potential customers.

Classifieds and especially online classifieds normally tend to concentrate towards one or two major players per market. The reason is relatively easy: Sellers want as many customers as possible and buyers want to have as many offers as possible. So for a seller it makes sense to post his offers on the biggest platform and potential buyers naturally look at the biggest platforms first.

However, cars are not actually sold on cars.com but they “only” generate leads to car dealerships which then again will ultimately sell the car to the customer. So the business model is not so different from for instance Trivago. In comparison to Trivago however, the market power of the suppliers is to some extent lower as there seem to be 40.000 or more car dealerships in the US of which cars.com seems to have signed up at last half of the existing ones.

In cars.com case, the money is mostly made by paid subscriptions from car dealers who pay for the right to list their inventory on cars.com. A relatively smaller share of sales comes from advertising of car manufacturers (~18-20%).

Cars.com segments their business into “retail” and “wholesale”, which however is a little bit misleading. “Retail” for cars.com means that they sell the listing directly to car dealerships. “Wholesale” means that someone else is selling the subscriptions. This seems to be a result of the buy-out in 2014. From the link above:

Effective today, McClatchy, Tribune Publishing Company, The Washington Post and A. H. Belo entered into new, five-year affiliate agreements with Cars.com that allow each company to continue to sell Cars.com products and services exclusively in their local markets. The affiliate agreements increase the wholesale rate at which the affiliates purchase Cars.com products.

The US car market itself is huge. According to the latest cars.com presentation, 17.6 mn new vehicles and 44 mn used vehicles are sold every year in the US, resulting in annual sales of ~1 Trillion USD. 30 bn USD a year are spent on advertising in this sector of which only a relatively modest amount is currently spent on online marketplaces.

Competitive environment

Cars.com is clearly not the only player in this space. Other popular US sites offering similar services are:

- Truecar (listed company, more on that below)

- CarGurus (just IPOed, see below)

- AutoTrader (part of Cox Communication)

I looked at the sites and at first glance, CarGurus seems to look a bit sleeker. TrueCar shows “discounts” everywhere whereas Cars.com rather seems to focus on car search. TrueCar seems to charge only for actual sales generated through its site whereas Cargurus seem to have the same “subscription model” as cars.com

From my superficial research, I didn’t find an “undisputed leader” in this field. Rather each site seems to have strength and weaknesses. There is also the rumour that Amazon wants to enter the market. However I am not sure if and what kind of competitive advantage Amazon could achieve in this sector.

Competitor TrueCar

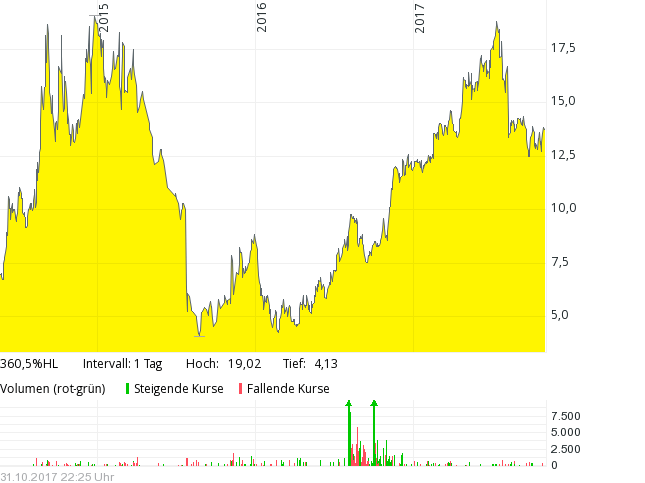

Truecar has been IPOed in May 2014. The stock price has been quite volatile so far as we can see in the chart:

As mentioned above, Truecar doesn’t sell subscriptions to car dealers but charges for actual sold cars resulting from their referrals (~300 uSD per sold car). Truecar has been growing sales from 80 mn in 2012 to 277 mn in 2016 but they have been loss making for every single year, even on a “Non GAAP” basis. So despite the growth, there is really the question if they have a valid business model at all.

Truecar had big issues in the past and the founder seems to be a difficult guy. On the other hand, Trucars seems to tackle a pain point for many US car buyers: they don’t want to haggle on a price and Trucar seems to be successful in achieving certain discounts for new cars and avoiding the unpleasant haggling. However, growth rates have been softening to single digits since 2016 but somehow profitability is still an issue. In my opinion there is no proof that as a business model Truecars is better than its competitors.

Competitor CarGurus

Cargurus has been IPOed just 3 weeks ago and took off like a rocket. The company was founded by Tripadvisor Co-Founder Langley Steinert who, of course wants to make Cargurus a “Tripadvisor for car dealerships”.

Other than Truecar, CarGurus is already profitable but still growing quickly. They have a similar business model like cars.com, selling subscriptions to car dealers. Interestingly they now seem to have more dealers under contract than cars.com, increasing the number by 50% before the IPO. It remains to be seen how much they can grow from here. Truecars for instance showed similar growth rates before the IPO but then growth rates declined rapidly. Cargurus tries to expand internationally which normally is really difficult in online classifieds. I quickly checked the new German site but so far it looks like a joke. I was for instance not able to find a single 5 series BMW in Munich (they actually call it 5 series in German, not 5er…), which shows that they are very far from having anything competitive to the “big 2” mobile.de and Autoscout24.

A quick comparison of Truecar, Carguru and Cars.com

When there are several listed companies in the same market sector, I always find it interesting to compare them based on general P&L statement categories. Although there are often differences how to report certain items, it can often be quite revealing. This is a comparison based on 6M 2017:

In this case, the most obvious difference is clearly sales & marketing spend in % of sales. Cargurus spends more than twice in relative terms on sales and advertising compared to Cars. com with Trucars in the middle. It is also interesting how much Cars.com seems to spend on technical and development. If I look at the website, I don’t see any differences. Cargurus looks like a very lean organization. Truecar looks bad almost from any angle.

Cars.com has actually lowered marketing spend in absolute numbers in the first 6M 2017 vs. the year before. I am not sure what the reason is for this, as one can easily see that the direct competitors are spending money like crazy. Maybe Tegna didn’t allow them to increase marketing spend ?

The Cars.com spin-off so far:

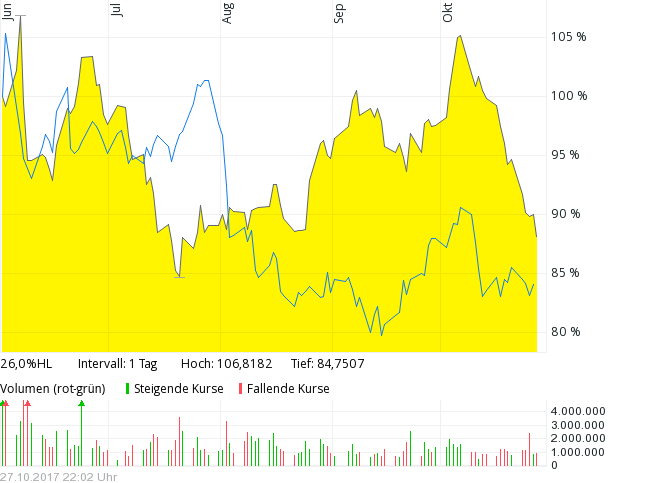

Interestingly since the actual spin-off, cars.com has outperformed Tegna but underperformed the overall market (cars.com solid yellow):

One of the reasons why cars.com has not performed well might be the 650 mn USD “Parting gift” from Tegna in form of a special dividend cars.com had to pay before the spin-off which had to be financed by a corresponding loan.

Relative Valuation:

Globally, besides cars.com there are 2 other listed “cars only” online classifieds: UK-based Auto Trader plc and Carsales.com from Australia. Scout24 from Germany is a mixed real estate / car online classified company.

| Market Cap | EV/EBITDA | EV/Sales | EBITDA Margin | 1Y Sales Growth | |

|---|---|---|---|---|---|

| CARS.COM INC | 1.721,7 | 10,2 | 4,0 | 37,0% | 0,2% |

| TRUECAR INC | 1.548,9 | #N/A N/A | 5,8 | -5,7% | 16,1% |

| CARSALES.COM LTD | 3.351,2 | 19,9 | 7,9 | 47,4% | 8,2% |

| AUTO TRADER GROUP PLC | 3.288,4 | 17,2 | 13,5 | 67,8% | 10,6% |

| SCOUT24 AG | 3.700,9 | 19,7 | 8,9 | 46,8% | 9,6% |

| Cargurus INC | 3.430,0 | 250 | 10,0 | 10,4% | 70% |

| Avg. (ex Truecar, Cargurus) | 18,9 | 9,0 |

It is easy to see that Cars.com looks cheap based on “static” multiples like EV/EBITDA or EV/Sales. On the other hand, at least in the first 6 months there was no growth and profitability is lower compared to the established players from other countries.

To put it in simple words: Although cars.com has the same amount of sales as Truecar and Carguru combined and is actually quite profitable, Enterprise Value is only 50% of the combined EV of the direct competitors.

We can also clearly see the reasons why the company is cheaper than similar global companies: It doesn’t grow at the moment and is less profitable. On the other hand, this also means that there could be significant leverage in the future. If , for some reason, growth would increase and profitability would increase, there could be a “double whammy” for any potential shareholder.

However it is maybe not totally fair to compare cars.com with companies in other countries as selling cars in the US is somehow special. This is from the Truecar Slate article linked above:

What Painter learned from CarsDirect, and a failed car venture he tried called Build-to-Order, is that the auto franchise system is so protected by state laws, and so politically powerful, that it’s nearly impossible to defeat it in any battle. (As his buddy Elon Musk has discovered while trying to set up Tesla dealerships.)

Management

This is from the S-1 registration document

Alex VetterT. Alex Vetter, 46, serves as the President and Chief Executive Officer of Cars.com. Alex has served as President and Chief Executive Officer of Cars.com, LLC since 2014 and previously held a variety of roles spanning product development, customer service, training, operations and sales, since the launch of Cars.com in 1998. From 2006 until his elevation to President and Chief Executive Officer in 2014, Alex served in a variety of senior management roles for Cars.com LLC, from Senior Vice President, Sales to Executive Vice President and Chief Operating Officer.

So the CEO is working almost 20 years in the company and seems to have started even in sales. According to Bloomberg, he owns about 3 mn USD in shares which is Ok, but not great.

I didn’t find a lot of him, more recent 2 minute interview is here:

Before the spin-off, they hired an experienced CFO. This is an interesting passage from the CFO interview:

MS. SHEEHAN: The wonderful thing is that Cars.com has many of the IT and financial systems already in place, separate from Tegna. That gives us a step forward in not having to create and build that kind of infrastructure.

As Chairman of the board, Cars.com seems to have appointed a very experienced guy:

Scott Forbes

Scott Forbes, 59, is expected to serve as Cars.com Chairman of the Board of Directors following the completion of the distribution. Scott serves as Chairman

of two LSE-listed companies: Rightmove, the UK’s number one online real estate company, and Ascential, an international business to business media company.

He currently serves as a member of the board of directors of Travelport Limited and was previously Chairman of Orbitz Worldwide until its sale to Expedia in

September 2015.

Salaries for management are relatively modest compared with typical Silicon Valley companies. The CEO’s base salary is around 450k, including bonuses he received 1,5 mn USD in 2016 which for an US company is not that much.

So overall, cars.com seems to have solid management in place but shareholder alignment could be better in my opinion.

Potential fundamental catalyst: Unfavorable contracts liability

At the end of 2016, Cars. com recorded a 44 mn USD “Unfavorable contracts liability” which seems to be expensed at a rate of ~25 mn USD per year. There is not a lot more information about this topic apart from this section in the S-1 document:

In connection with TEGNA’s October 2014 acquisition of the 73% of Classified Ventures, LLC that it did not already own, Cars.com entered into new

affiliation agreements with a group of media organizations that formerly owned Classified Ventures, LLC. In addition, in connection with TEGNA’s June 2015

spin-off of its publishing business as a standalone public company, now operating under the name Gannett Co., Inc., Cars.com entered into a new affiliation

agreement with Gannett Co., Inc. and its newspaper subsidiaries. Pursuant to these affiliation agreements, all of which expire in either 2019 or 2020, Cars.com sells

advertising packages and dealer solutions at wholesale rates to these counterparties, who have the exclusive right to market these products in their relevant territories. Cars.com does not have control over these counterparties, and any deterioration of the business prospects of or underperformance by these

counterparties may reduce the revenues that Cars.com earns through wholesale channels.

My interpretation is that those “wholesale” contracts are quite unfavorable to cars.com and that the expiration will be positive. Either they might manage to negiotate better terms or they can take over the distribution themselves. All other things equal, this looks like a small “fundamental catalyst” for better profits from 2019 on.

Pros & Cons

As always a quick list of Pros and Cons for the stock:

Pro

- Capital light, high gross margin business

- Economies of scale / market place model (two-sided), cars.com currently #1

- subscription model accounts for 80% of sales (recurring revenues)

- CEO = Co-Founder, 130k shares/3,1 mn USD shareholdings

- distorted P&L (separation costs, depreciation)

- no big stock option grants etc.. modest salaries

- relatively cheap valuation

- potentially positive effects of spin-off on morale and business development

- little operational change as cars.com was run as a separate company before

- potential target for take-over and/or activist

- smaller “fundamental catalyst” from 2019/2020

- underlying business still growing (online marketing for car dealerships)

Con:

- extra debt from spin-off

- assets almost completely intangible

- lower site visits 06/2017, stagnating sales

- “old school online” business model (30 people producing content, plain vanilla subscription model)

- Management solid but no significant ownership

Investment case (at ~24 USD/share)

If I use the “adjusted EBITDA” numbers, the annual run rate should be around 220-240 mn of EBITDA. Based on a EV of around 2,3 – 2,4 bn USD , we have a valuation of roughly 10 times EV/EBITDA. Taking into account the current issues, would assume that a 12-13 times EV/EBITDA valuation would be “fair”. This would translate into a potential upside of 23% to 36% all other things equal. This is a modest under valuation but not spectacular.

However, one could also hope that after the spin-off things might improve, either via getting back onto a growth path or increased profitability which then could lead to clearly better outcomes. In a “Blue sky scenario” for instance, I could assume that they will grow EBITDA 5% p.a. over the next 3 years and reach 45% EBITDA margin. With a modest multiple expansion to 12X EV/EBITDA this translate into a ~90% upside.

Of course, things could also turn out to get worse after the spin-off. However in my opinion there could be some kind of downside protection due to the fact that there is no controlling shareholder. I could easily imagine that either an activist shareholder could enter the picture or a potential strategic buyer might become interested. As it is extremely difficult to enter online classifieds from the outside, cars. com could be an interesting target for an international player. This is a quote from an Australian Investment website:

We presume, though, that McIntyre is aware of the May 2017 listing of US company Cars.com (NYSE: CARS). Cars.com is one of the leading online classified companies for the US automotive industry. Incidentally, in the US Cars.com competes with market leader www.autotrader.com, owned by Cox Automotive, which now owns Carsales’ Australian competitor www.carsguide.com.au.

Carsales could be interested in buying Cars.com for two main reasons. For one, the US company is cheaper. Cars.com trades on an enterprise value to earnings before interest, tax, depreciation and amortisation (EV/EBITDA) multiple of 11 times next year’s earnings. Carsales trades on 17 times, so in theory the Australian company could benefit from ‘multiple arbitrage’ if it bought Cars.com.

More importantly, Cars.com operates a business model that Carsales might consider old-fashioned. Cars.com makes most of its revenue from selling online advertising subscription packages to about 20,000 car dealers across the US. These packages allow dealers to showcase their vehicles on its site.

I could imagine that also other Groups look at cars.com already as this is one of the few reasonably priced online classifieds businesses available for an acquisition.

So all in all I do think that cars.com has an interesting risk/return profile. Although it is not “rock bottom” cheap, i think there is significant upside with limited downside.

I think the situation is quite similar to Tripadvisor: Both companies are “first wave” internet companies with a good brand and lots of traffic, but have some issues with growth under their legacy business model and mobile. Personally, I do like the online car business better as the competitive dynamics it travel make things harder for “marketplaces” due to the dominance of the 2 big OTAs Expedia and Booking.com.

So overall I think it is not unrealistic to expect a gain of ~+50% over the next 3 years based on some multiple expansion plus some positiv fundemantal developments.

Why is the stock cheap ?

As always, one needs to think about why the stock looks cheap. In my opinion those issues could explain it:

- no growth at the moment

- one-off costs in 6M 2017 numbers

- lot of (Legacy) intangible write-offs

- “parting gift” of 650 mn debt

- Investor relations not very inspiring, listed competitors, esp. CarGurus “more sexy”

- low analyst coverage (only 5 analysts from companies I have never heard about)

- no confidence in management

Summary:

All in all I find the Cars.com spin-off interesting. Compared to peer companies, the stock trades at a clear discount although the company is still the market leader in the largest market in the world.

There are clearly risks to the downside and the stock is clearly not a “Graham type value stock”, but I do find the risk/return profile interesting. On the other hand, there is also a good chance that the company on its own might get back onto a growth path.

Therefore I have invested 3,4% of the portfolio into cars.com at a price of around 23,85 USD/share.

Further research links

Click to access 4b5dcfb9-5df0-4142-94ea-471a086e62c9.pdf

https://seekingalpha.com/article/4079053-cars-com-spin-requires-discounting-appeal-lures

https://www.glassdoor.de/Bewertungen/Cars-com-Bewertungen-E34989.htm?countryRedirect=true

http://www.mahesh-vc.com/blog/online-classifieds

https://fastbuyinc.com/blog/are-sites-like-truecar-edmunds-carscom-hurting-dealers-bottom-line/

http://www.insider-car-buying-tips.com/car-buying-websites.html

https://forum.dealerrefresh.com/threads/cars-com-vs-autotrader-vs-cargurus.5153/

I sold cars.com today at ~12,70 USD per share resulting in a loss of ~-44% since I bought them. Ugh.

Looks like cars.com is revisiting it’s November lows on soft EPS reported.

MMI and others, what do u think?

Maybe a tighter FED and higher interest rates could actually be a tailwind for the used car industry? Or is it that wages matter much more?

Contrary opinion from Stefan Waldhauser

https://www.high-tech-investing.de/single-post/2018/03/27/Carscom

I think he has a different focus. I don’t claim to invest in “tech leaders”….

Time to unload some?

Why ?

And what else to buy ?

Any information why Starboard Value sold a significant stake?

No.

today up 8% as Starboard Value bought 9.9% Stake in Cars assuming it’s undervalued: https://seekingalpha.com/news/3319042-cars-com-plus-8-percent-starboard-9_9-percent-active-stake-disclosure

In future it will go up when starinvestor memyselfandi007 buys 😉

Thank you for nice investment idea as always!

Like the story on this one. Where I come unstuck is whether they will just get into a spending war with Cargurus on sales and marketing and erode margins.

Hello MMI,

I have been reading your blog for several years now and I generally like your investment angles and ideas a lot. Coming from the industry, Ibanker CF & CM, I’m impressed with your insights. For instance, I worked on Acomo back in 2010 in ECM (sole global, EUR 40mio subordinated convertible).

Regarding CARS, bought some shares two weeks ago, also bad timing… Highly cash generative (market cap / FCF approx. 10x), low capex requirement and distorted figures due to spin-off and goodwill amortisation. My worries are more regarding lack of visible track record (Tegna / IR doesn’t provide (full) data for 2014/2015 and earlier) and possible bad capital allocations. It’s high cash generation can enable the company to repay debt quickly but bad / expensive M&A is a risk I see. What’s your take on lack of visible track record and capital allocation?

Regards,

Joost

Hi Joost,

thank you for the comments. I share your concnerns on track record and capital allocation to a certain extent. But this is of course the issue with spin-offs in general and one of the reasons why they are often too cheap. What I do like is that the CEO is an “old timer” and they seem to have a really good board which might mitigate some of this risk.

mmi

wow, spectacularily bad timing from my side….Although I think the Q3 numbers are quite OK.

But it looks like we have “hammer time” for many internet related stocks.

Truecar is down 35% today – probably Q3 earnings missed?

Maybe also something to do with the fear of an increase in marketing spending for tripadvisor and the like (also down 23% today)?

Thanks for the comment. Looks like the time for growth is over at Truecar:

Click to access TrueCar_Q3_2017_Earnings_Presentation_11.6.17_vF.PDF

No growth vs. Q2. Plus revenue per deal is declining. Not good. Will be interesting to see how cars.com will report.

BCA Marketplace is more interesting

and why exactly ?

Will let you figure that out at your own pace 🙂

It’s hard to get excited on that basis…….

Here is a clue to wet your appetite:

Pengana likes Motorpoint. The largest holding in their fund in a matter of fact as of yesterday’s report.

BCA and Motorpoint share a similar business model, market, revenue stream and sourcing channels (unlike cars.com)

OK just spent my morning on Motorpoint. I still prefer BCA simply because of the fact that it is further upstream in the than Motorpoint (and Cars.com) in the transaction chain.

A couple of questions:

1) What type of investment do you consider it to be? Boring?.

2) The competitive advantage is due to the network effect … if this was a good business, I think Amazon will enter the business and I think it will easily overcome barriers to entry. What do you think about it?

Thanks for the post¡¡¡

1) Special situation (Spin-off)

2) I think it is too small for Amazon. Profit pool is not big enough in my opinion.

I think you have understated the value of the wholesale contract resets, for what it’s worth.

What is the value in your opinion ?

Great that you look into Cars.com. In the beginning, I reached the same conclusion, cheap compared to peers and good-quality business. And cars.com had replatforming over the past year. So the traffic and sales have stagnated for a year. If the replatforming completed and the growth returned, there will be a huge upside.

However, after studying CarGurus, I am a bit concerned whether cars.com can grow anymore. Mobile is becoming the platform for car buyers. 78% of CarGurus` users are from mobile, compared to cars.com`s 52%. Visits are much higher in CarGurus. I am not so sure that cars.com is more superior at PC side but not good at mobile side. But based on cars.com`s longer history than Cargurus, cars.com should be originated from PC. I think that`s why cars.com had done replatforming. But I am sure whether cars.com can gain more ground in mobile as CarGurus is the clear leader in mobile.

On the other hand, if cars.com wants to win in mobile, it has to spend more to acquire users, which means maybe marketing spend % will rise to Cargurus` level, which means cars.com margin will suffer. Even if sales can grow, profits may not grow.

And the industry is really crowded and competitive. Just a few thoughts to share with you. For me, cars.com has to be cheaper to get me interested in buying it.

As I mentioned, cars.com looks a little bit similar to Tripadvisor. But we we will see. Personally, I think Cargurus has timed its IPO very well. Their growth will most likely level off pretty soon.

Nice investment, especially as no growth is priced in.

Here is another soon coming spin off:

La Quinta Holdings Looking To Spin Off Real Estate

http://www.stockspinoffs.com/2017/02/13/la-quinta-holdings-looking-spin-off-real-estate/

That reminds my a bit of Joel Greenblatts Marriott example…

They keep their roalyty business and get rid of their own hotels.

Unfortunately I know little about hotels and even less about (US) real estate.

This will probably work given the time frame but what do you make of longer term trends?

http://www.autonews.com/article/20171105/INDUSTRY_REDESIGNED/171109944/bob-lutz:-kiss-the-good-times-goodbye

well, that’s I risk I need to take. Same as Admiral.

20 years he says… I doubt so.

Unlike cars, infrastructure takes a very long time.