General Electric (GE) – Accelerated share buy backs as a fundamental warning sign ?

General Electric

GE for a long time was one of the bluest Blue Chips. Especially under Jack Welch, GE was a synonym for great management and clock work like profit growth.

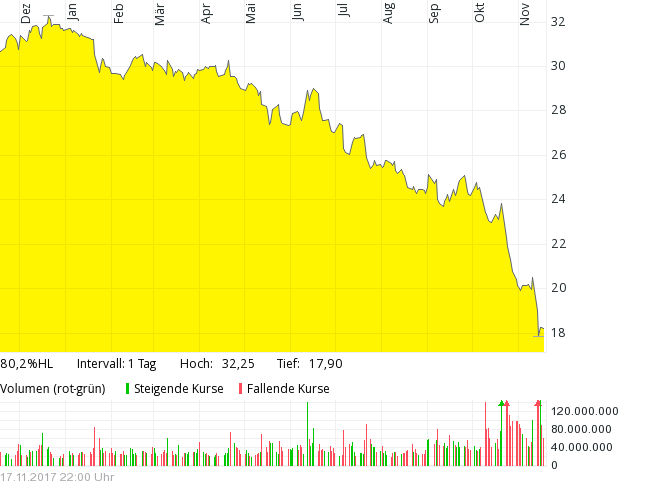

Now things look different. we just need to look at the 1 year chart:

Just out of interest, I looked at the Q3 report of GE. This report is really heavy stuff. Lot’s of Non-GAAP numbers and very heavy to digest.

However a few interesting facts:

- GE has been paying more dividend than they earned for some time now. For the first 9 months they paid out 6,5 bn USD and only earned 3,8 bn

- Comprehensive income was actually better than net income and increasing. 9M “other comprehensive income” was actually higher than normal net income

- Goodwill is now higher than equity (in 2016 still slightly positive): Another 30 bn are intangible assets. 25 bn USD Goodwill for Power and Oil &Gas each.

- Borrowing in the industrial segment has increased again this year

- pretty aggressive pension assumptions: 4,1% discount rate, 7,5% “Normalized” investment returns, 25 bn USD plus funding deficit. Gross liabilities of 72 bn USD (year-end 2016)

Share buybacks – should that have been a warning sign ?

In the past years many investors that were looking at a company were thinking like this: “Oh. company xyz buys back shares, so capital allocation must be great”.

GE is a pretty good counter example to that. This is from the 2016 annual report:

During 2016, we repurchased $22.0 billion of our common stock, including $11.4 billion repurchased under accelerated share repurchase (ASR) agreements.

In December 2016, we entered into an ASR agreement with a financial institution that allowed us to repurchase GE common stock at a price below its volume weighted-average price during a given period. During the fourth quarter, we paid $2.2 billion and received and classified as treasury shares an initial delivery of 59,177,215 shares based on then-current market prices. The payment was recorded

as a reduction to shareowners’ equity, consisting of a $1.9 billion increase in treasury stock, which reflects the value of the shares received upon initial delivery, and a $0.3 billion decrease in other capital, which reflects the value of the stock held back pending final delivery.

So if we look at only the final, acceleratet purchase: 2,2 bn USD for 59.2 mn shares means that they paid ~37,2 USD per share, almost 100% higher where the share is today. Now with the stock price at multi-year lows one would expect that they buy back even more shares.

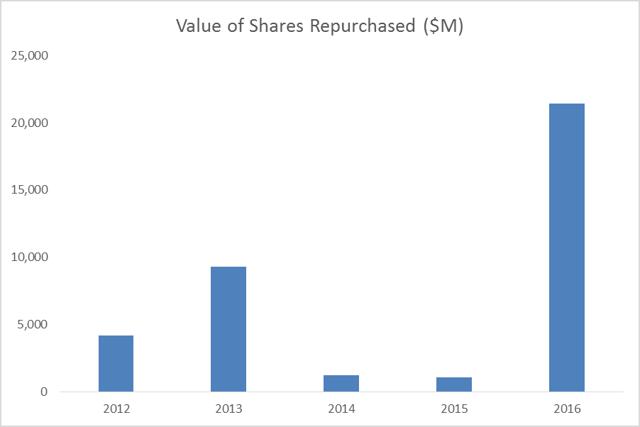

But now, according to the Q3 report, GE has repurchased only ~2,6 bn in own shares in the first 9M 2017 compared to 18 bn in the first 9 months 2016. It is also interesting to see that in 2014 and 2015 they only repurchased a net 1 bn USD in shares. This is a graphic of buybacks from a Seeking Alpha post:

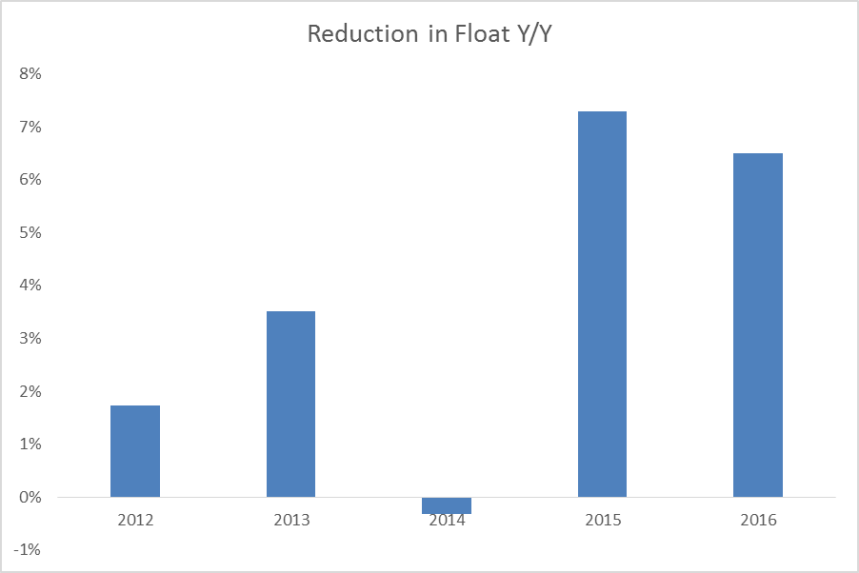

Share count reduction looked somehow better due to Synchrony “spin-off” share swap in 2015:

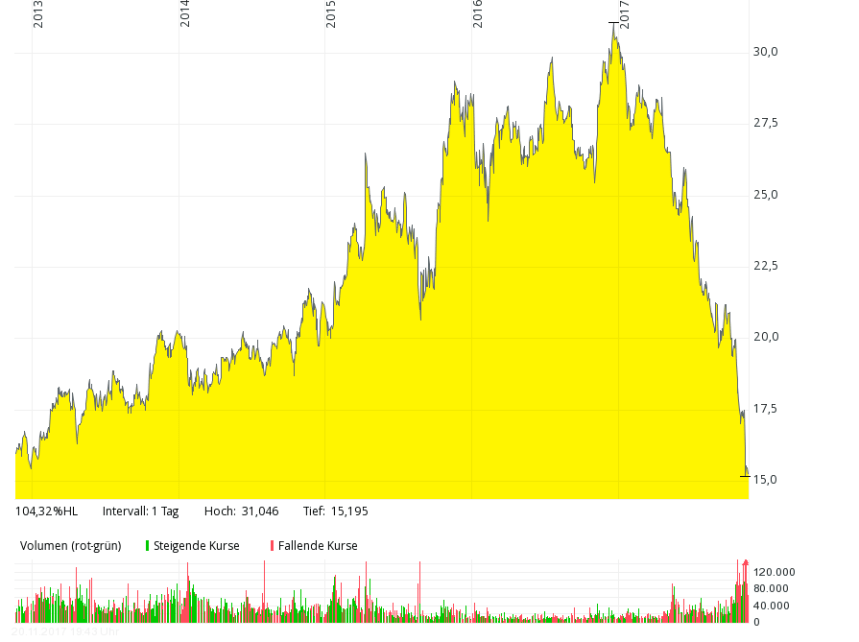

Nevertheless it interesting to look at the 5 year stock chart to see how stupid the huge 2016 repurchase looks like in hindsight:

Interestingly now the CEO speaks of selling strategic assets, a pretty hard turn from buying back 22 bn USD in shares the year before. Even the only recently acquired / merged Baker Hughes business seems to be in principle for sale.

Of course it could have been only bad luck, but with the long term nature of GE’s business, I would be surprised that they didn’t see it coming.

However, for such large companies like GE it seems to be almost impossible not to do huge buybacks when the stock price is still high but the outlook gets kind of not so good. It reminds me a little bit of IBM which also bought back massive amounts of shares at the wrong moment. It would be interesting to see if this is somehow a pattern in similar situations: Beware of huge stock repurchases at stagnating companies.

Maybe the reason is that stock options play a large role in compensation packages at US companies like GE and therefore management tries to keep up the price of the stocks as long as possible. A dropping share price leads to less money for everyone and good people might leave the company or ask for significant salary increases once the stock options get worthless ?

Warren Buffett to the rescue ?

Some commentators are speculating that GE would be a great fit for Warren Buffett, however in Summer Berkshire sold the last remaining shares in GE so I guess this is rather wishful thinking. Interestingly, Berkshire has been buying GE spin-off Synchrony Financial instead.

Some positives for GE

On the positive side:

- GE still contains some very good businesses like the Aerospace segment

- the bleak earnings outlook could be driven by the new CEO who wants to lower expectations as much as possible

- at least in the past GE was considered a well-managed company

On the other hand, the stock is not really cheap (18 times 2018 earnings) and it’s not clear if and when the main Power business turns around.

Summary:

Overall, reading a GE report is not much fun. There is a lot of incomprehensible Non-GAAP stuff which shows that GE does still kind of OK, but overall things look rather bleak. For me, GE is clearly a stock for the “too hard pile”. I think it might be more worthwhile to look at potential GE spin-offs for time being than going deeper on GE itself.

Experience shows that if a behemoth like GE gets into trouble, it usually takes quite a long time until things really turn around.

GE is also a good example that even huge share buy backs are not the silver bullet for value creation if the underlying business is struggling. In GE’s case it was mostly only delaying the inevitable drop in the share price when profits continued to shrink in the core businesses.

While I know management ultimately makes the decision (and there is a lot that has seemingly gone wrong here), it’s hard to knock the company on the 2016 buyback without directly pointing the finger at Trian and Nelson Peltz. Spend a few minutes searching around and you will see headlines like Trian urges GE to accelerate buybacks.

You have to wonder if GE’s CEO/Board made a deal – knowing accelerated buybacks might not be the best idea – in order to avoid a proxy battle and keep their seats.

Good point. Sometimes activists can really hurt companies. I guess peltz has sold his stocks some time ago….

robert honeywill on seekingalpha had some very good fundamental analysis on ge over the last few months.

In June there was a Bloomberg article about their pension shortfalls, buybacks, and Nelson Peltz.

https://www.bloomberg.com/news/articles/2017-06-16/ge-s-31-billion-hangover-immelt-leaves-behind-big-unfunded-tab