Spin off check: Getinge / Arjo AB (ISIN SE0010468116)

One upfront comment: I promise to use the auto correct feature of wordpress.com in 2018 as often as possible. However, as I do not have unlimited time to “polish” my posts, there will be always bad grammar and bad spelling as I try to focus my available time on analyis and actual content.

Already some week ago, Swedish based “Med tech” company Getinge AB spun off Arjo AB.

Getinge now seems to concentrate on developing, manufacturing, and selling equipment and systems for sterilization and disinfection in hospitals. Arjo seems to be more geared towards “mechanical” med tech products such as hospital beds etc.

The reason for the spin-off seems to be that Getinge was somehow unsatisfied with the development of their profits and therefore decided to spin-off its smallest and least profitable division. Interestingly, Arjo had been taken over by Getinge in 1995 and was before already a stand alone listed company.

This is how Arjo has been officially described by Getinge:

Arjo is a global supplier of medical devices, services and solutions that improves the lives of people affected by reduced mobility and age-related health challenges. In 2016, Arjo’s sales amounted to SEK 7,808 M and the company was present in more than 60 countries. Going forward, Arjo will focus on creating value in a market characterized by high growth opportunities, due to e.g. demographic changes with a rising number of elderly and those suffering from illness as well as an increase in lifestyle-related diseases. The goal for Arjo is to contribute to a more efficient healthcare system by becoming a market leader in long-term care, while maintaining the company’s strong market positions in acute care – within the segments in which the company operates.

So in principle this sounds interesting as this is clearly a growing market. However, looking at the 9 month report we can see that there are clearly issues at Arjo:

- Top line sales decreased -2-4% yoy for the first 9 month (before FX)

- EBITDA margin dropped from 20% to 14%

- Q3 loss of -0,26 SEK/share vs. 0,50 SEK/Share in 2016

- Operating CF 9 M 2017 -50% vs. 9M 2016

According to the report, most of this is due to separation costs. But even on an adjusted basis, operating profit went down yoy.

Including currency translation, Arjo made a significant negative comprehensive income for the first 9M 2017 (~30% of sales are in North America).

Other considerations:

As in many other cases, the parent Getinge decided to give a parting gift in form of some net debt to Arjos:

1) Allocated net debt is based on Getinge Group’s reported net debt as per September 30, 2017. Based on this date it was decided to allocate SEK 4,400 M of Getinge Group’s net debt to Arjo. Hence, Arjo’s net debt at listing will be SEK 4,400 M with adjustments for the cash flow generated from October 1, 2017 to first day of trading as well as potential currency effects

This seems to be around 4x actual 2017 EBITDA which is Ok but will certainly limit Arjo’s financial flexibility to a certain extent (Getinge says its 3,1 x “adjusted” EBITDA but I think this is too optimistic.).

From Getinge’s point of view the spin-off improves everything, margins, leverage ratio and growth (page 27). So the motivation to separate from Arjo becomes quite clear. Getinge’s profit halved since its peak in 2010/2011 and its share price is now at the same level as 10 years ago which results in significant underperformance against any applicable index.

One interesting point: The CEO of Arjo is the former “interim CEO” of Getinge. One other interesting point is that Arjo management has bought “synthetic options” on Arjo shares from the largest Shareholder, Carl Bennet:

As stated in the prospectus for admission to trading of the shares in Arjo, Carl Bennet AB has offered all board members elected by the general meeting and all members of the Executive Management Team in Arjo to acquire synthetic share options in Arjo issued by Carl Bennet AB. Today, the Board of Directors in Arjo was informed by Carl Bennet AB that everyone who has received the offer has acquired options. According to the notification, 9,190,469 synthetic share options have been acquired in total, at a price deemed to correspond to the market value of the options. The total market value of the options at the time of the transaction has been calculated to SEK 19.3 million.

The synthetic share options are related to the Arjo Class B share with a maturity of four years and may be exercised during the period 1 October–31 December 2021. The exercise price per option is SEK 29,60, which corresponds to 122 per cent of the volume-weighted average price paid for the Arjo Class B share on Nasdaq Stockholm during the period 12–18 December 2017. When exercising the option, the option holder will receive a cash payment from Carl Bennet AB corresponding to the number of underlying Class B shares each option represents multiplied by the market value of the share reduced by the exercise price. The option holder will not receive any cash payment if the market value is less than the exercise price.

Arjo has not been involved in the offer that has been provided by, and solely on the initiative of, Carl Bennet AB to the board members and the Executive Management Team in Arjo.

The amounts are not huge but what I found unique is that not Arjo has sold those options but the biggest shareholder.

One thing that has bothered me is the following: One of the rules of thumb is that spin-offs work best if the companies that are separated have been very different, i.e. were active in very different markets etc. With Getinge and Arjo, at least to me as a non-expert I would say that the businesses are quite similar.

They sell to the same clients (hospitals) and at least loosely related products. So from that perspective; I am not completely sure how much real value is created by the spin-off on both sides.

Quick and dirty valuation / Relative value:

Using Arjo’s 9M “actual EBITDA” of ~850 EBITDA, we could assume a full year EBITDA is around 1.100 mn SEK. with a market Cap of 6.500 mn SEK and 4.400 mn SEK debt, Arjo then is valued at ~9,9 EV/EBITDA,

For the Med-Tech sector, 9,9x EV/EBITDA is not that much. A peer group supplied by Bloomberg shows that EV/EBITDA’s of 15-20 times are not uncommon, however there is s clear correlation to profitability:

| Name | Mkt Cap | EV/EBITDA | EBITDA Margin | 5yr avg ROE | ROIC |

|---|---|---|---|---|---|

| Arjo | 6.51B | 9.9 | 14.73% | — | |

| AMBU A/S-B | 34.67B | 47.13 | 23.57% | 27.57% | 17.69% |

| STERIS PLC | 60.15B | 19.22 | 17.26% | 5.13% | 3.66% |

| Coloplast | 143.25B | 19.12 | 36.29% | 69.20% | 63.71% |

| W. Demant | 60.42B | 20.58 | 19.23% | 22.91% | 13.47% |

| CARL ZEISS | .54B | 24.32 | 17.28% | — | 12.22% |

| ESSILOR | 245.54B | 16.63 | 22.13% | 13.33% | 9.63% |

| P. Hartmann | 14.28B | 6.62 | 10.61% | 10.44% | 11.13% |

So if, and that is a big “IF”, Arjo could increase its margins, a higher EV/EBITDA could easily follow. However right now, Arjo doesn’t look “dirt cheap”.

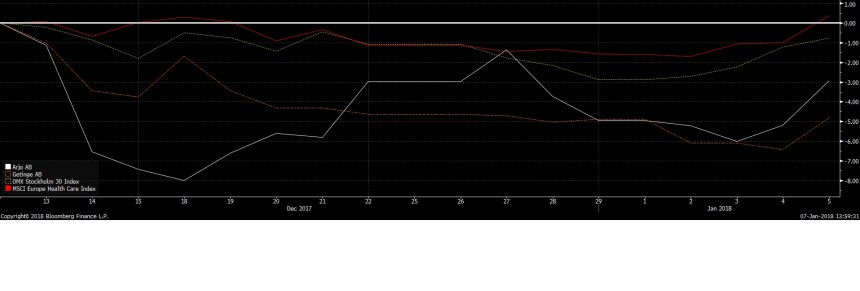

The stock prices so far:

This is the performance of Getinge & Arjo since the spin-off:

Both stocks have underperformed the Swedish stock market and the MSCI Healthcare index since the spin-off. Arjo even did a little better than Getinge. But so far nothing dramatic happened.

Summary:

Based on this first very brief analysis, Arjo doesn’t look that interesting too me. It doesn’t look extremely cheap and the underlying business’s clearly seems to be under pressure.

If they manage a succesful turn-around, then the stock could be interesting but as I know only very little about the health care sector, I prefer to watch this from the outside.

Getinge itself at a first glance also doesn’t look much more promising. As Arjo, they need to turn around their business and I know too little in order to have a qualified opinion on the potential of success.

For ref. Thales 51€/ share bid for Gemalto, with the later trading at 49.5. Seems a 3% gain, but wonder if any upside (or downside!) potential…

Thanks 😉

One upfront replay

I really enjoy your writings (along with OTC adventures you are my top blog to read). I never even noticed any grammar error and I really don’t think it worth worrying about