Landis & Gyr (ISIN CH0371153492): Potentially interesting “Forced IPO” Special Situation ?

Background

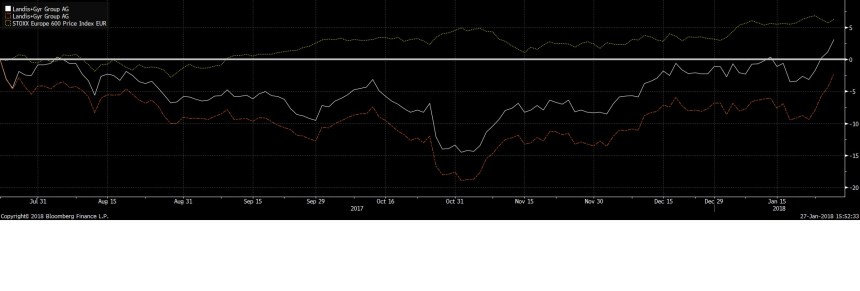

![]()

Landis & Gyr, the Swiss based company was on my research “to do” list for some time. Why ? Because it looked very much like a “forced IPO” special situation when in Summer 2017 then almost bankrupt Japanese Conglomerate Toshiba decided to sell Landis & Gyr which was deemed to be one of their crown jewels.

Toshiba itself had bought Landis & Gyr in 2011 for around 2 bn USD from a Private Equity Seller (Bayard) who in turn had bought Landis & Gyr from KKR (via DEMAG), another PE shop in 2004. Back then, Landis & GYr had around 390 mn EUR in sales and it was rumoured that the purchase price was quite low at around 100 mn EUR (those were the days…..).

Bayard, in a “Buy and build” strategy then had combined a couple of different “green energy” companies into Landis & Gyr in 2008.

Toshiba could sell Landis & Gyr at the upper range of the book building range (70-82) at 78 CHF/share. Before that it was rumoured that PE companies were interested but would not pay more than 2 bn CHF for the company. As we can see in the chart, since the IPO the stock is more or less flat, in EUR the stock is still down and has underperformed significantly against the European stock indices (-4,3% in EUR against +12,3% Stoxx 600):

Business: Smart metering

Landis & Gyr call themselves the globally leading company for “smart electricity metering and smart grid”. At first sight, this looks quite attractive, as both, smart grid and smart metering can only be more important in the future with renewable energy and electric vehicles.

First 6M report:

Looking at their first 6M earnings presentation, we can see some interesting things:

- ~55% of sales are in the “Americas” region but around 100% of the “adjusted” EBITDA is generated there

- Europe and Asia together run at a loss

- They love to adjust numbers to get from GAAP losses to adjusted profits

- They are very optimistic on growth until 2020 (“high single digit” CAGR)

The level of detail of this report is quite disappointing. They don’t explain why the US is so much more profitable and what part of the revenue is recurring or not.

I found this presentation from 2012, after Landis & Gyr was acquired by Toshiba. The most interesting thing is that between 2012 and the IPO, sales have hardly increased in USD. So the claim that from now on they will grow “high single digit” is not well founded from the recent past.

R&D

There is one interesting aspect: Landis & Gyr claims to spend around 10% of sales for Research and Development. The question I ask myself is how much of that is to simply stay competitive and how much to gain a competitive advantage.

Looking at their rather constant sales in the past and shrinking margins I would think that this kind of R&D is rather “Value preserving” compared to more “value enhancing” R&D.

IPO prospectus

Thanks to a good friend, I obtained a copy of the IPO prospectus. The most interesting parts were:

- the Americas segment contains a large project in Japan (TEPCO) which seems to be very profitable but ending soon (somewhere to the end they say that 12,5% of the sales in America are from Japan).

- It also contains a reseller contract with Toshiba in Japan which might not last too long

- They did have and still have significant warranty issues /around 50 mn per annum in 2015, 2016 and 2017)

- there is an underfunded defined benefit pension plan (03/2017 deficit ~50 mn USD), the gross value of the DBO is around 300 mn USD, however discounted at relatively low rates

- Goodwill & Intangibles are higher than equity

- R&D is split into R&D for new products of 73% and 27% for existing ones. However also “customization” of products seems to be accounted as R&D which in my opinion is pretty normal selling expense.

- As competitors, they mention among others listed competitors Itron, Honeywell and Apator (Poland)

- They are involved in a litigation against Toshiba in the US

- there is regulation that meters have to be replaced every 10-20 years in most countries

- Management received 0,4% of the shares as a kind of bonus

Quick Valuation:

Even if I accept all the adjustments, the company doesn’t look cheap: At around 200 mn EBITDA for the current FY, Landis and Gyr trades at around ((2387/1,07)+100+50)/200 = 12 x EV/EBITDA. This would be OK for a high quality and strong growth company. However as we have seen, growth so far is a promise and not the reality.

Based on actual EBITDA (43 mn in the first 6M), the stock rather trades at 30x EV/EBITDA.

Competitor Itron trades currently at around 14xEV/EBITDA but Itron’s numbers seem to be much higher quality than Landis & Gyr. Polish based Apator only trades at around 8xEV/EBITDA but seems to shrink.

A few comments on Toshiba

Just a few days ago, Toshiba has finalized its disposal of the troubled Westinghouse unit. So far they seem to have avoided official bankruptcy. There are rumours that Toshiba would also try to IPO the Chip business if a sale to Bain fails.

For hardcore deep value investors Toshiba might be worth a look into, also the sell side has become a lot more optimistic about Toshiba over the last months.

Summary:

Although at first sight, Landis & Gyr looked like a potentially interesting “forced IPO” by distressed Toshiba Group, the stock currently looks more than fairly valued, even accepting the many adjustments that management makes to turn a GAAP loss into an adjusted profit.

So far investor communication has been quite intransparent and the many adjustments made are normally a clear sign of weakness.

So all in all, Landis & Gyr for the time being doesn’t look like a very attractive investment and Toshiba seemed to have gotten a quite good price despite their distressed situation.

Luckily you side-stepped that dog. Well done!

The forced IPO of Landis & Gyr peaked my interest as well.

Plus the business seems attractive at first glance.

But maybe it is more like a utility than a tech/network/IoT play…

Anyhow, the price is way too high at the moment.

The only recent IPO which was interesting from a valuation

perspective to me was Jost Werke.

I would add Befesa to the list of recent cheap IPOs….

Befesa seemed to be more reasonably priced. But still a stretch for me.

A big part of their business has rather low margins and is higly

dependend on commoditiy prices (granted: they hedge a lot).

The regulatory apspect of their business model is interesting.

Without knowing the stock, at first sight it looks rather expensive from an EV/EBITDA perspective. Plus it’s a Private Equity IPO.

At the time of the IPO the market cap was below €1bn plus €450m in debt for a company that runs little monopolies and should have made €140m in EBIT. Today the market cap is 40% higher. I saw it at the IPO but I blew it.

Toshiba was much cheaper when the smoke cloud was still over them and before the equity issue which diluted existing shareholders 35%. There’s still deep value there, but nothing to shout home about.

The talks of bankruptcy were contrived. Total liabilities (including a massive pension deficit and the maximum nuclear project guarantees per construction agreements) of 20 trillion yen against a memory chip business alone that is worth 40 trillion yen fully valued and half that distressed, before even considering other arms and marketable securities.

The important insight which was missed by western observers was japanese culture itself: Toshiba and Shinzo Abe were more interested in avoiding the image blow of a delisting than they were about maximizing shareholder value. As such, the very shallow focus was — and in a way analysts continue making this mistake — on bankruptcy bankruptcy bankruptcy. It’s worth the look for those willing to do the work.